US Debt I: Trump vs Powell.

President Donald Trump wants lower interest rates. He blames Fed Chair Jerome Powell for keeping them too high. He has been saying so since his first term in office as President. He said so again on June 27: “I think we should be paying 1% right now, and we’re paying more because we have a guy who suffers from, I think, Trump Derangement Syndrome.” That’s after he reiterated that “I’d love him to resign if he wanted to; he’s done a lousy job."

Trump has also been frustrated by the Bond Vigilantes. On April 9, he was forced to postpone imposing his April 2 “Liberation Day” reciprocal tariffs on America’s trading partners for 90 days after bond yields spiked on the resulting turmoil in the capital markets (Fig. 1 below). He acknowledged as much that same day (April 9) when he said, “I was watching the bond market. The bond market is very tricky; I was watching it. But if you look at it now, it’s beautiful. The bond market right now is beautiful. ... I saw last night where people were getting a little queasy.”

{kind=link}

If the Fed were to lower interest rates, Trump’s expectation is that the entire yield curve would decline, saving the US federal government “hundreds of billions of dollars.” Last week, on his Truth Social site, Trump shared a handwritten note he wrote to Powell. “You are, as usual, Too Late,” he wrote. “You have cost the USA a fortune and continue to do so. You should lower the interest rate by a lot! Hundreds of billions of dollars being lost! No inflation.”

However, Trump also realizes that bond yields wouldn’t necessarily follow short-term interest rates downward: After what happened in early April, he knows that the Bond Vigilantes could spoil his victory by pushing bond yields higher.

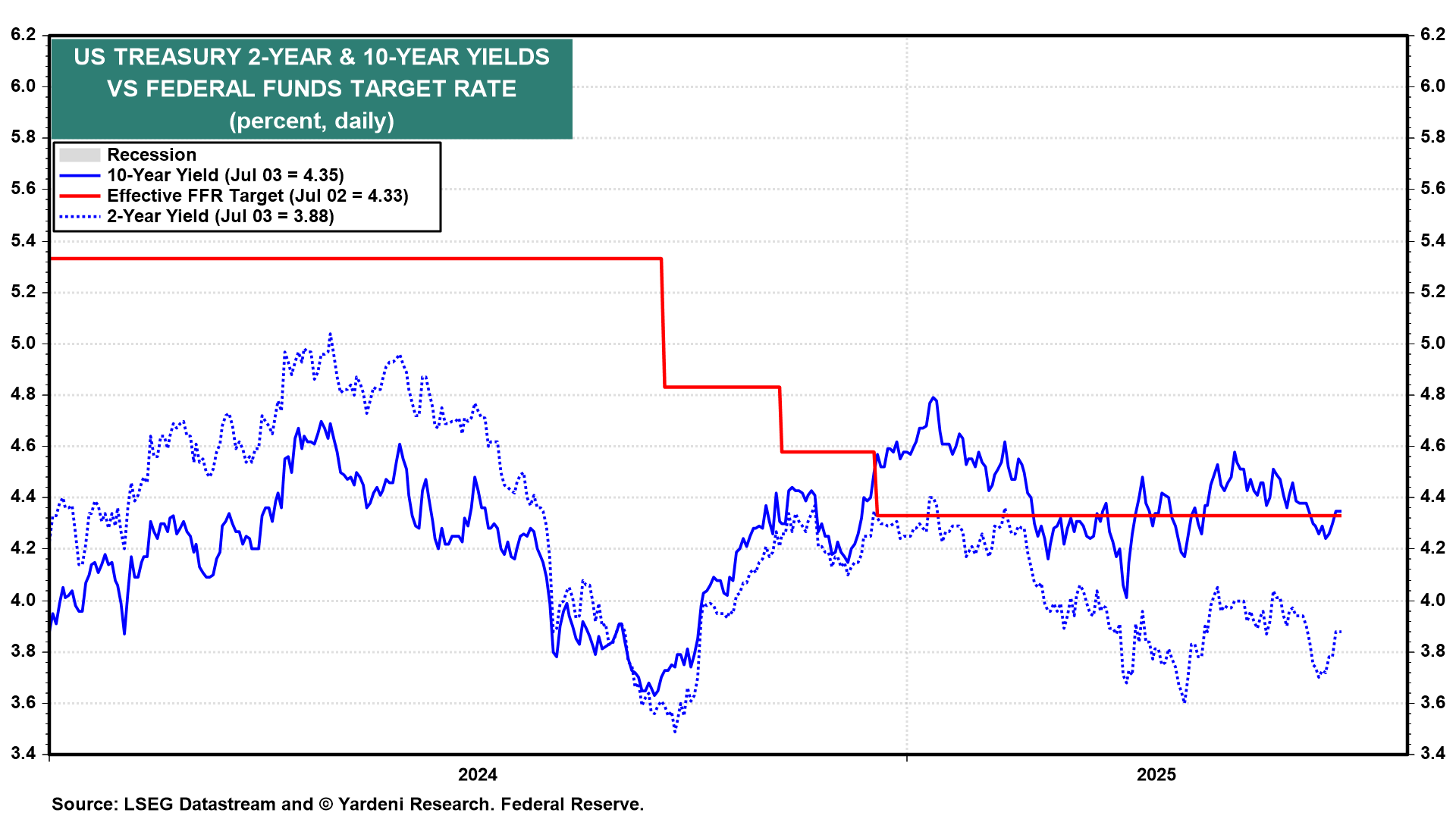

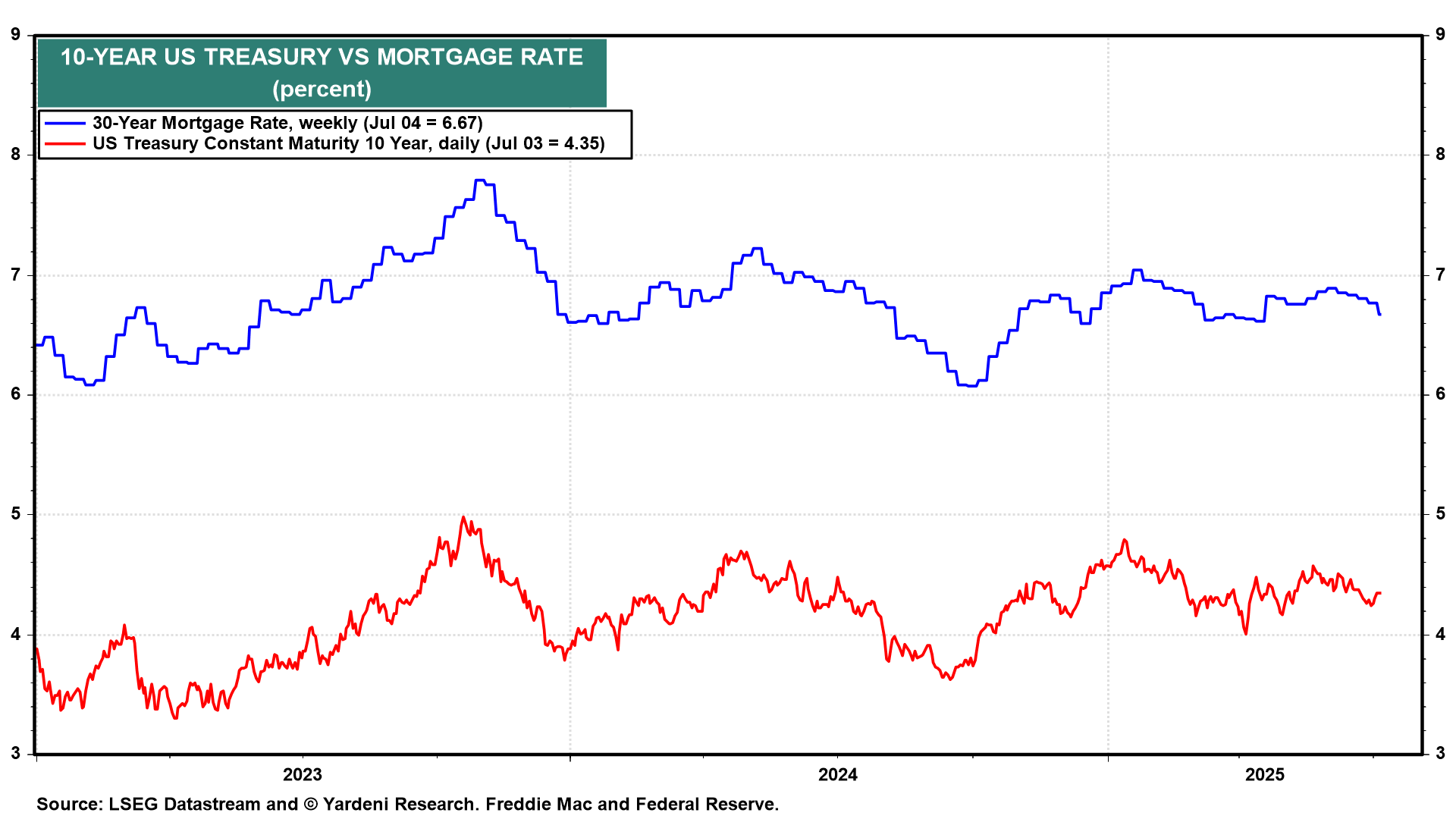

That’s what happened last year from September through December when the Fed cut the federal funds rate four times by 100bps in total (Fig. 2 below). The 10-year bond yield (and mortgage rates) rose by 100bps (Fig. 3 below). The Bond Vigilantes recognized that the economy wasn’t as weak as Fed officials thought at the time. We did too, and we predicted that the bond yield would rise in response to the Fed’s unwarranted easing.

{kind=link}

{kind=link}

US Debt II: Trump’s Gambit.

Trump has a plan for dealing with Powell and the Bond Vigilantes. Last week on Sunday, June 29, in a pre-taped interview with Maria Bartiromo on her Fox News show Sunday Morning Futures, he said, “I don’t want to have to pay for 10-year debt at a higher rate,” when talking about financing the US government debt. When Maria asked the President how he was going to deal with the $9 trillion in debt that is due this year, Trump said he was going to refinance it as short-term debt because “we have a stupid person” at the Federal Reserve. He added, “Then we’re gonna get somebody into the Fed who’s going to be able to lower [the rates].” He noted the rates should be at 1% or 2%: “You know, if you look at Switzerland, they’re the lowest right now. They’re at much less than one point, and frankly we should be there, too. …”

So according to this plan, the Treasury will issue more Treasury bills and fewer notes and bonds over the rest of the year through next year until Trump appoints the next Fed chair, who then will lower interest rates so that the maturing Treasury bills can be refinanced with longer-maturity debt at the then-lower interest rates. Brilliant!

Not so fast: It would be brilliant except for a couple of loose ends:

(1) Fed Chair Jerome Powell’s term as Fed chair expires on May 15, 2026. However, he could stay on as a Fed governor until his term in that position expires on January 31, 2028. Fed Governor Adriana D. Kugler’s term expires on January 31, 2026. Trump could fill her open position with someone outside the current Fed roster, such as Treasury Secretary Scott Bessent or another Trump loyalist, including current Fed Governor Christopher Waller.

But Trump loyalist or not, the next Fed chair will still need to work with the other 11 voting members of the Federal Open Market Committee to make monetary policy decisions. In the past, Fed chairs have succeeded in persuading the majority of their voting colleagues on the Federal Open Market Committee to vote for their policy stances. There rarely have been any dissenters, and when there were dissenters, they were few in number (one or two).

A Trump loyalist as Fed chair might have more dissenters or even more than enough of them to vote for a policy stance contrary to the one supported by Trump’s Fed chair. That would seriously weaken the power of the Fed chair and raise concerns about the internal conflict with the Fed.

(2) In addition, if Trump’s loyal Fed chair replacement manages to deliver rate cuts when they are not justified by the incoming data, the Bond Vigilantes might do what they did in late 2023, i.e., push bond yields higher. The Treasury might be forced to continue issuing more Treasury bills in the hopes that a reduced supply of Treasury bonds would bring their yields down. But the Bond Vigilantes might push back, recognizing that lower bond yields would cause the Treasury to rapidly increase the supply of bonds.