The week ahead is starting with another tariff whiplash. On April 2, President Donald Trump imposed hefty reciprocal tariffs on America's trading partners but postponed them for 90 days on April 9. On Friday, he threatened new tariffs on the European Union, Apple Inc., and perhaps Samsung and other tech giants to be named later. But on Sunday, he postponed Friday's June 1 tariff of 50% on the EU until July 9. So much for liberation from Trump's Tariff Turmoil (TTT). All of which gives this week's data an air of relative irrelevance as the White House zigs, zags, and zigs almost daily.

This will make upcoming speeches by Fed officials extra newsworthy, offering insight into how they think TTT might impact monetary policy. And in the aftermath of Moody's downgrading the US to "Aaa" on May 16, financial markets will pay close attention to events on Capitol Hill. Namely, how the deficit-bloating "Big, Beautiful Bill" that the House passed last week lands with Senate Republicans, as well as the Bond Vigilantes.

Let's briefly review this week's data outlook:

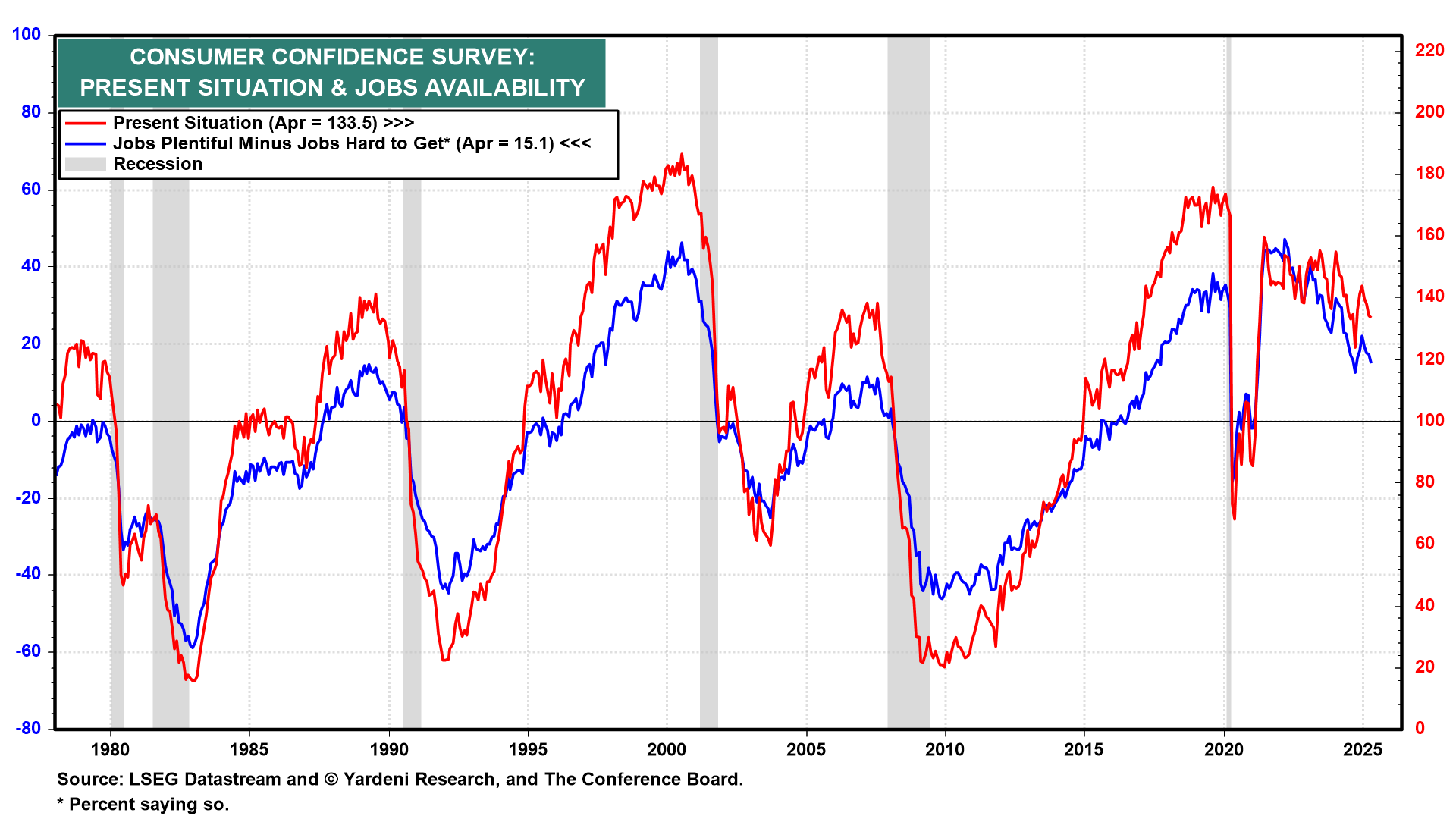

(1) Consumer confidence and sentiment. Trump's April 9 postponement of the April 2 "Liberation Day" tariffs by 90 days sent stock prices soaring. May's Consumer Confidence Index (CCI, Tue) is likely to reflect that V-shaped rebound. May's CCI survey should show that the labor market remains solid, which we expect jobless claims (Thu) to confirm (chart).

Yet the whiplash factor is worth keeping in mind for May's Consumer Sentiment Index (Fri), which could remain depressed by tariff worries and high inflation expectations. (The CCI is more sensitive to employment, while the CSI is more sensitive to inflation.)

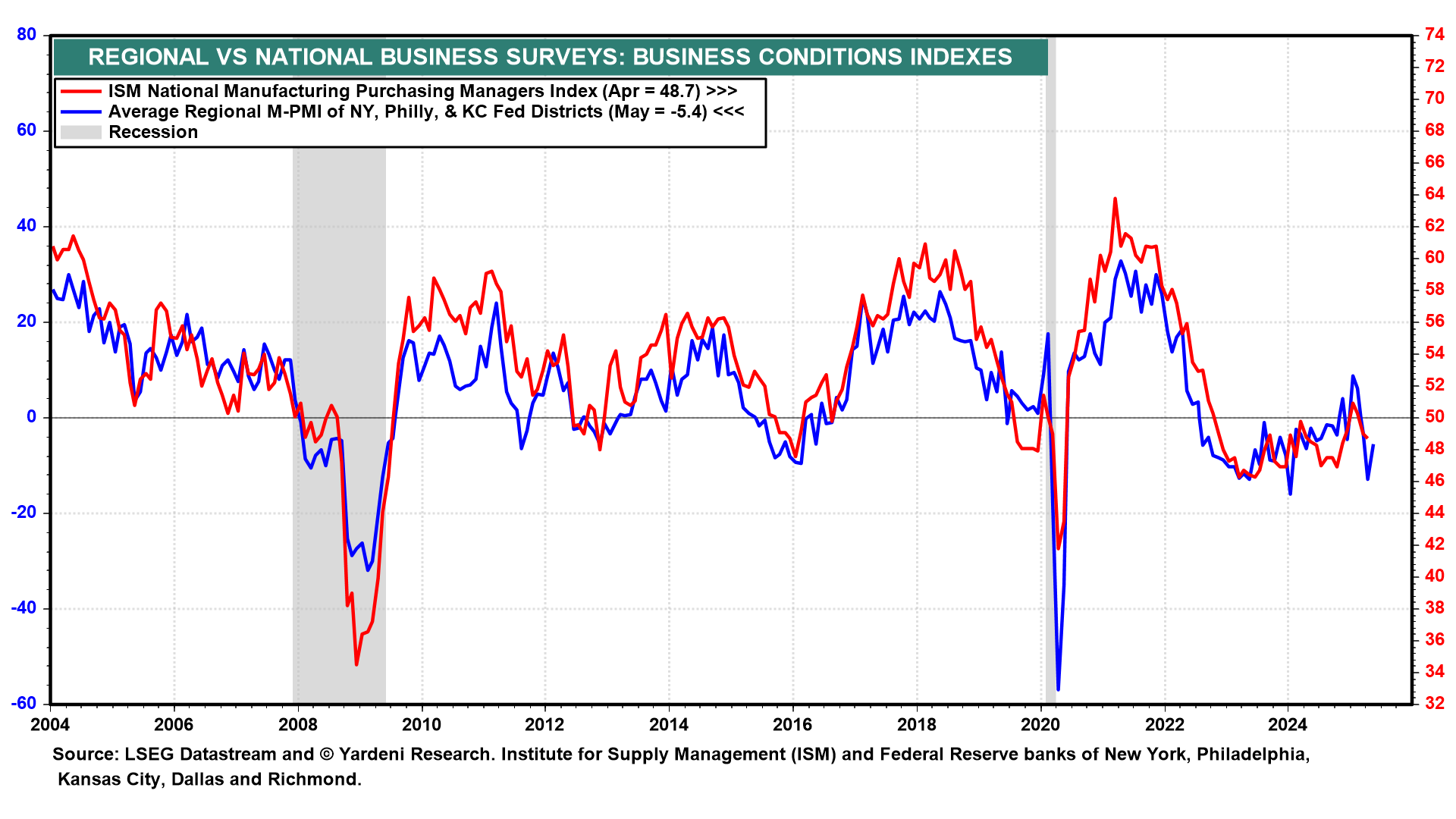

(2) Regional business surveys. The Dallas Fed's manufacturing outlook survey for May (Tue) is likely to show some improvement following April's grim -35.8 reading, the lowest level since 2020. We expect a similar pattern from the Richmond Fed business survey (Wed). The average of the NY, Philly, and KC Fed manufacturing indexes rebounded in May but remained relatively depressed (chart).

(3) Regional price data. Meanwhile, the stagflationary trajectory some worry the US economy is on may get some traction for the next few months. Case in point: The average of the NY, Philly, and KC Fed surveys of prices paid and prices received remained elevated in May (chart). This week's comparable Dallas and Richmond Fed readings are likely to confirm that inflationary pressures have been mounting in response to TTT.