We are thankful for your interest in our research. Happy Thanksgiving!

Now that the government shutdown is over, there is plenty of data again with which to assess the economy's performance. On balance, GDP growth remains robust despite lackluster labor market indicators. Consumers are consuming. Inflation is subdued just below 3.0%. The federal deficit remains enormous. Federal tax receipts confirm the economy is growing. Nevertheless, the Fed, which has already lowered the federal funds rate by 150bps since September 2024 through October of this year, is likely to cut it again at the December 10 FOMC meeting. So, the S&P 500 is back on track to hit 7000 by the end of the year in a Santa Claus rally. Let's review the recently released data:

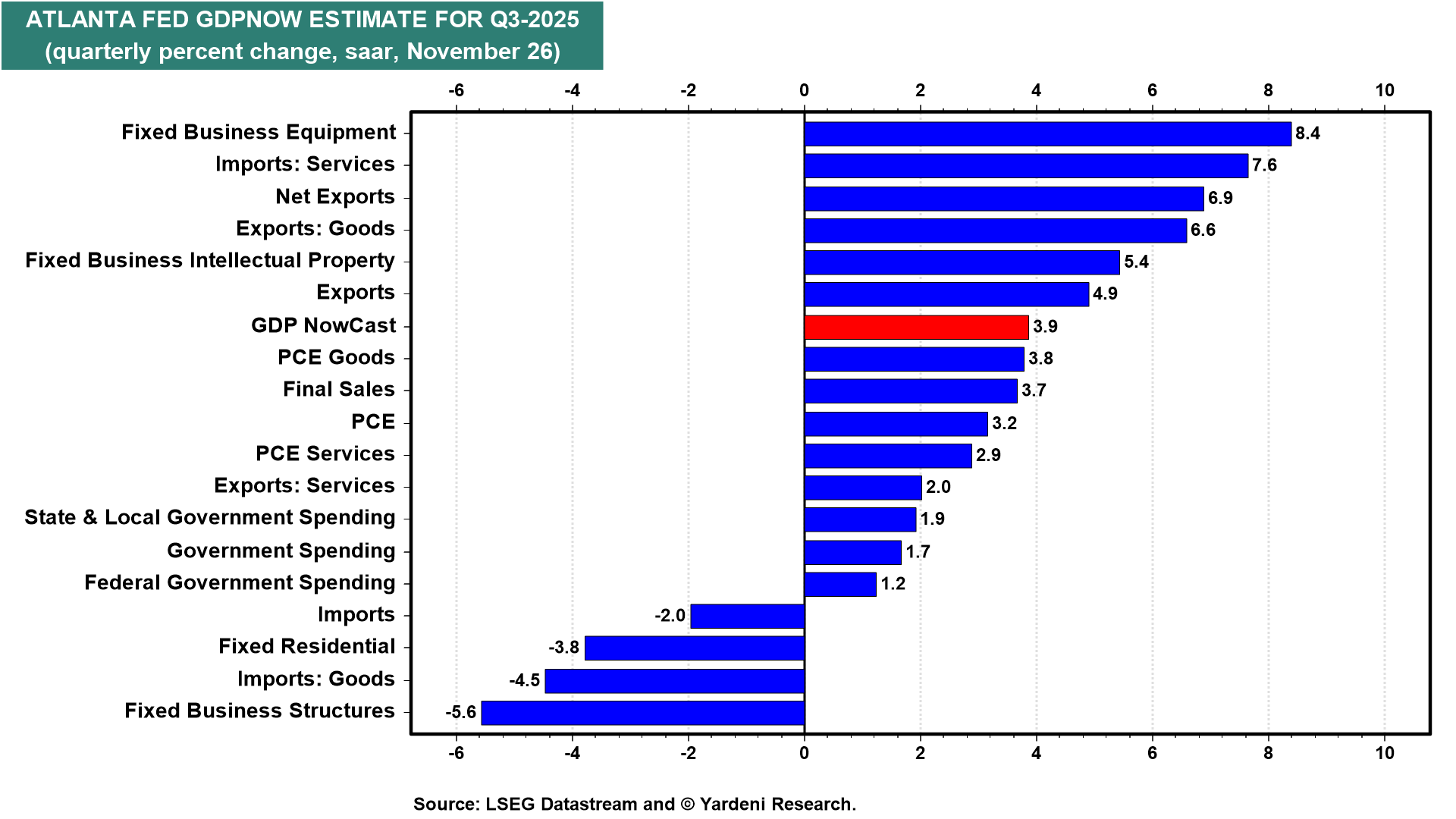

(1) Real GDP. The Bureau of Economic Analysis raised Q2's real GDP growth rate from the preliminary estimate of 3.0% (saar) to 3.8%. The Atlanta Fed's GDPNow model is showing that Q3 is tracking at 3.9% (chart). These are robust numbers, suggesting that productivity is also growing rapidly.

(2) Retail Sales. During September, retail sales rose just 0.2% m/m following a 0.6% increase in August (chart). Nevertheless, real consumer spending during Q3 is tracking at 3.2% (saar) according to the GDPNow model.

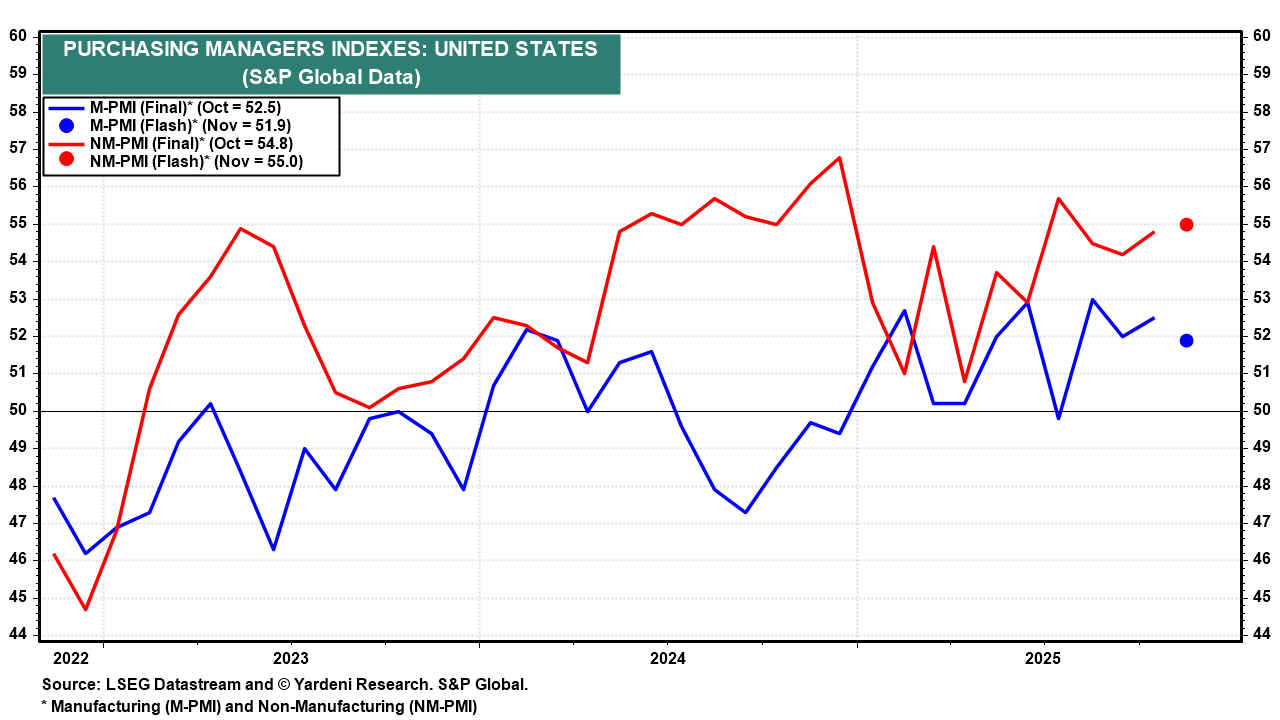

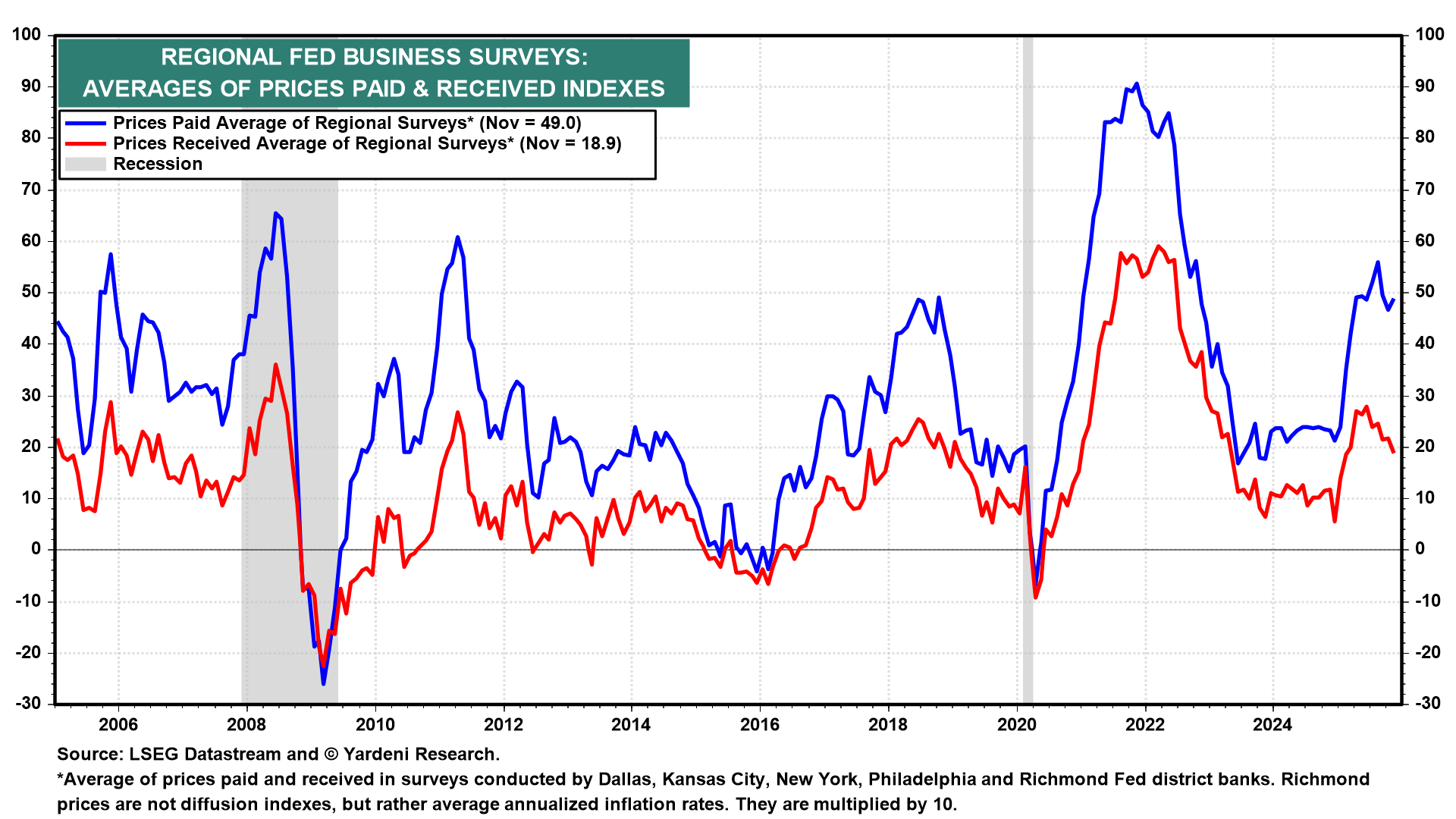

(3) Business surveys. The monthly regional business surveys conducted by five of the 12 Fed district banks show that manufacturing remained fairly lackluster during November (chart). Collectively, they suggest that the national M-PMI, compiled by the ISM, remained at or below 50.0.

The M-PMI compiled by S&P Global ticked down to 51.9 in November, but remained well above 50.0. The S&P Global NM-PMI ticked up to a strong reading of 55.0 during the month (chart).

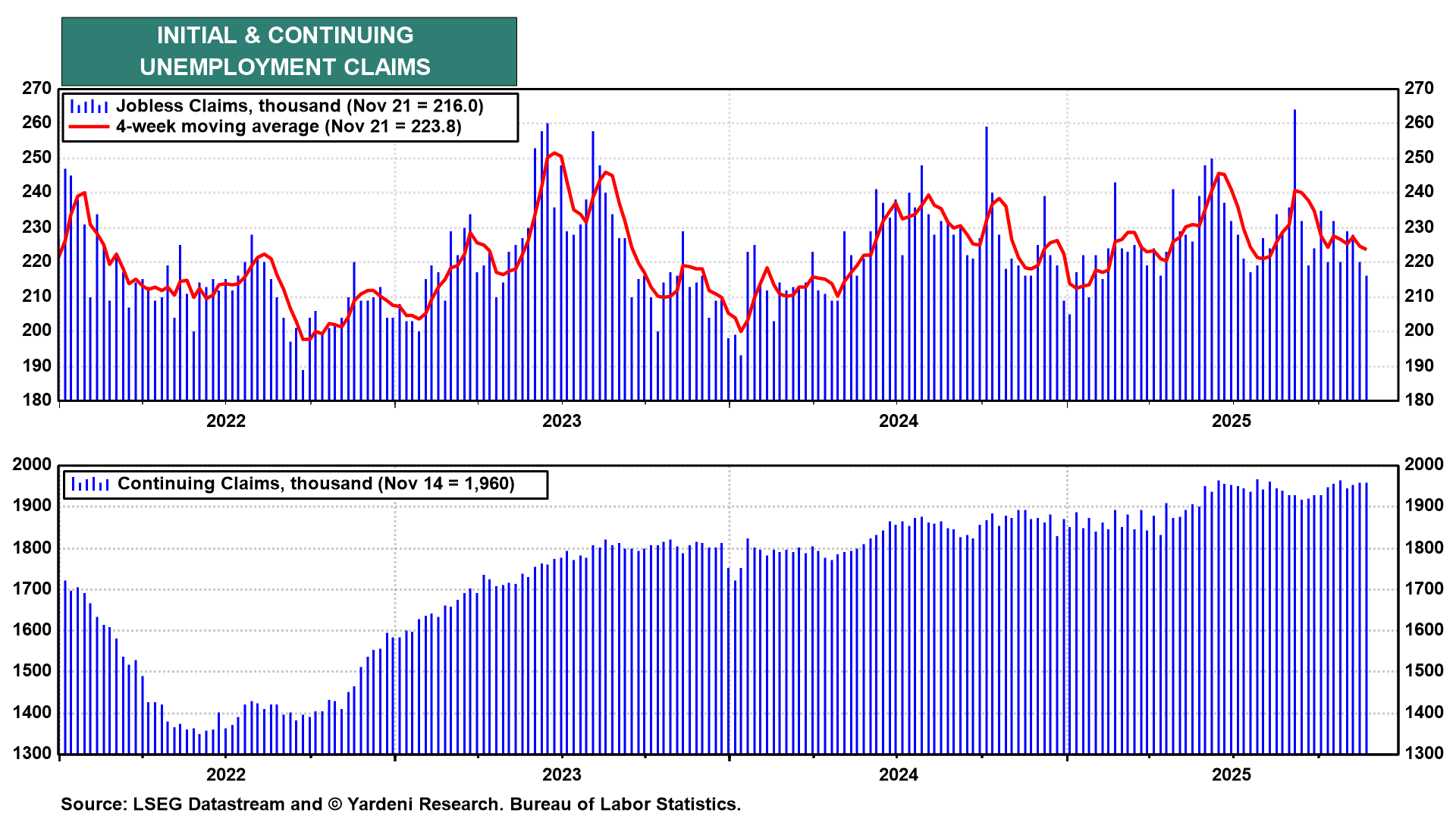

(4) Labor market. Initial unemployment claims fell during the week of November 21 to only 216,000 (chart). This suggests that layoffs remain low. However, continuing claims show that the duration of unemployment has risen because it is taking longer to find a job. This is why September's unemployment rate rose to 4.4% from 4.3% in August. Also more people were looking for a job that month.

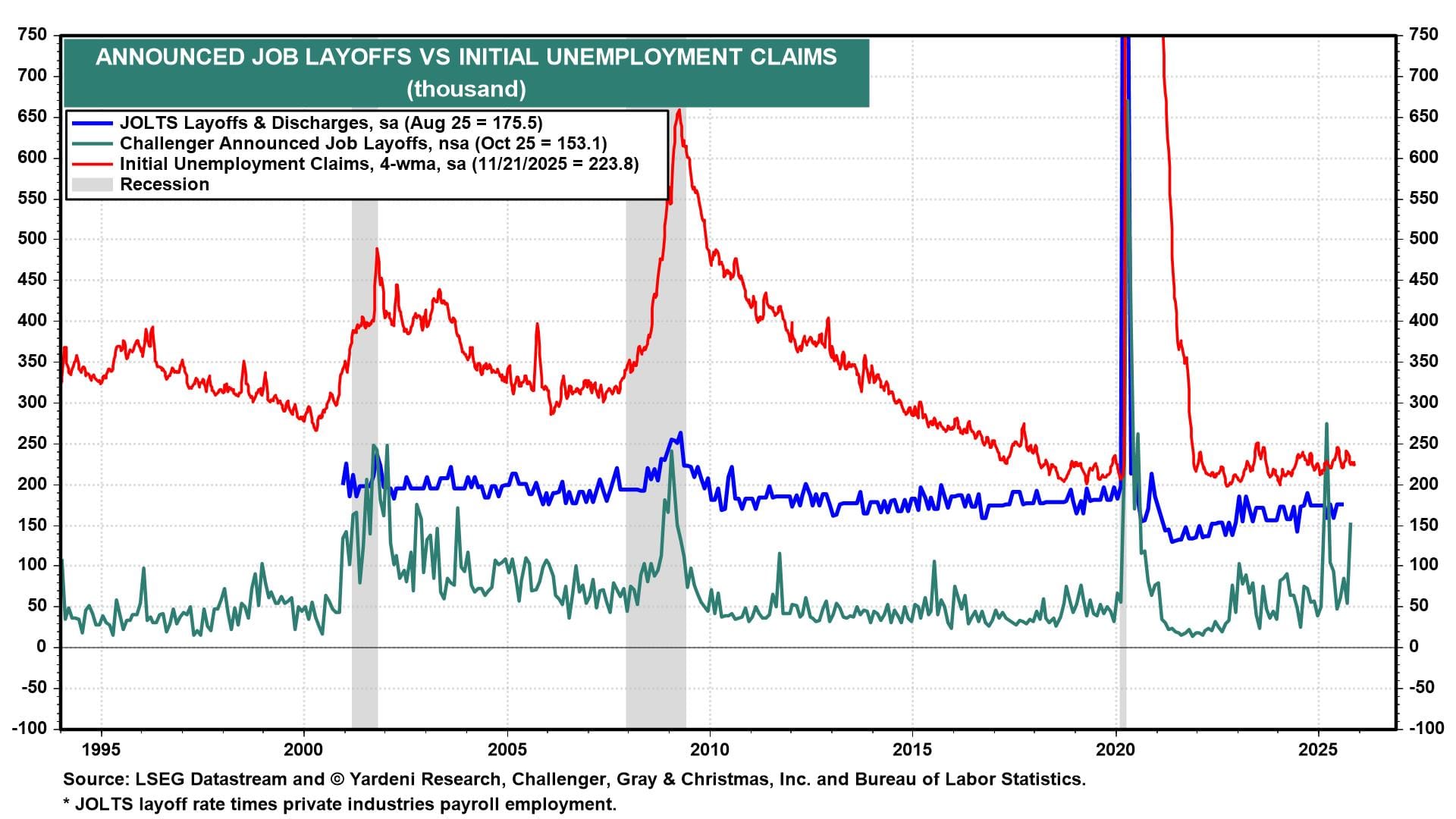

The Challenger report of announced layoffs rose sharply in October (chart). However, it is a more volatile and less useful measure of layoffs than weekly initial jobless claims.

The Consumer Confidence Index survey showed that "jobs available" remained relatively high this month at 54.5% (chart). The drop in "jobs plentiful" over the past few years mainly boosted "jobs available" rather than "jobs hard to get," which remains relatively low at 17.9%.

(5) Inflation. November's prices-paid and prices-received indexes, based on the averages of the Fed district surveys, suggest that inflationary pressures from earlier this year's tariffs may be abating (chart).

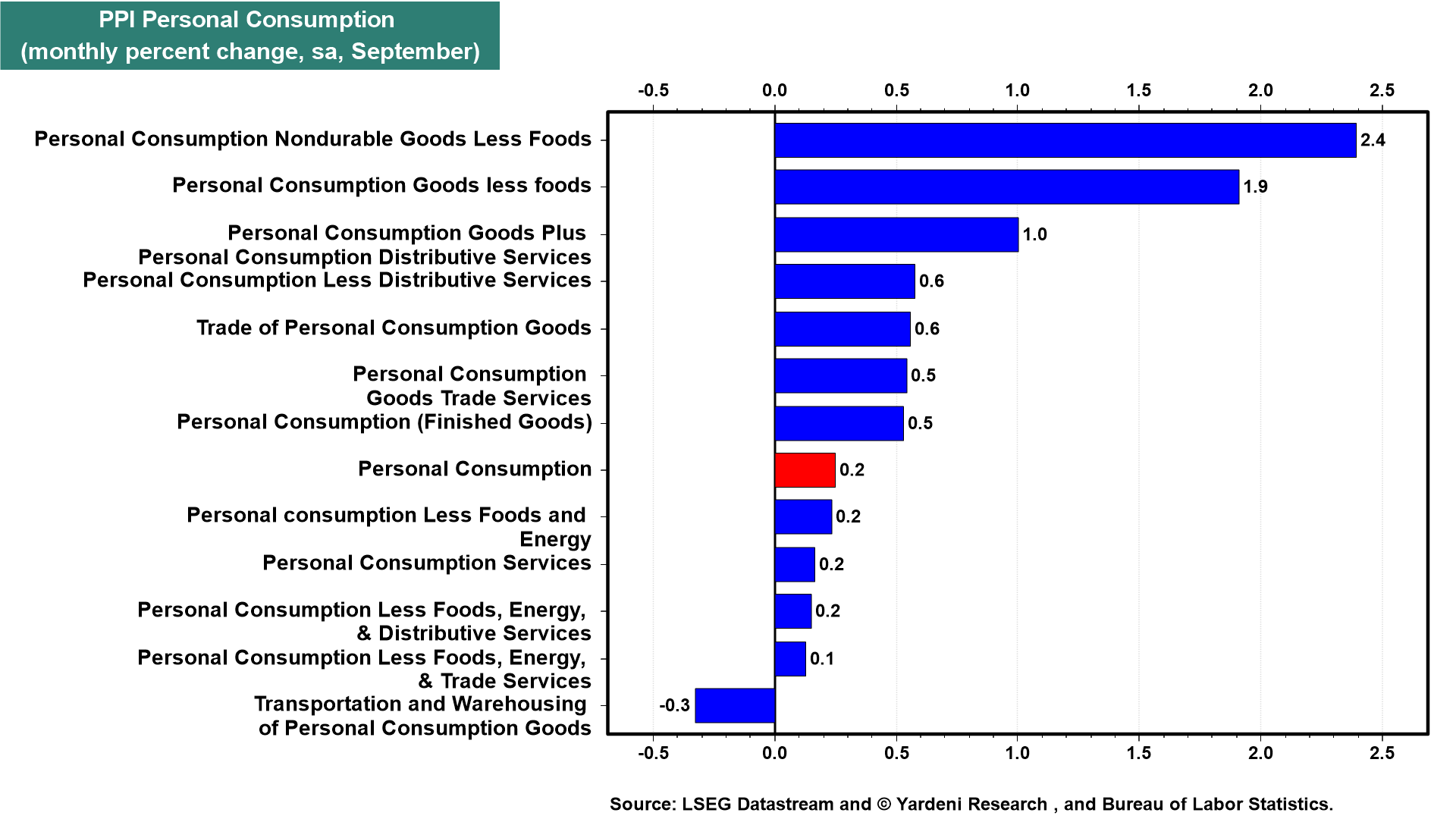

September's PPI for personal consumption rose only 0.2% m/m (chart). This measure of inflation was held down by very moderate increases in service prices, which more than offset relatively significant gains in goods prices. The Cleveland Fed's Inflation Nowcasting predicts that September's headline and core PCED rose 2.79% y/y and 2.85% y/y.

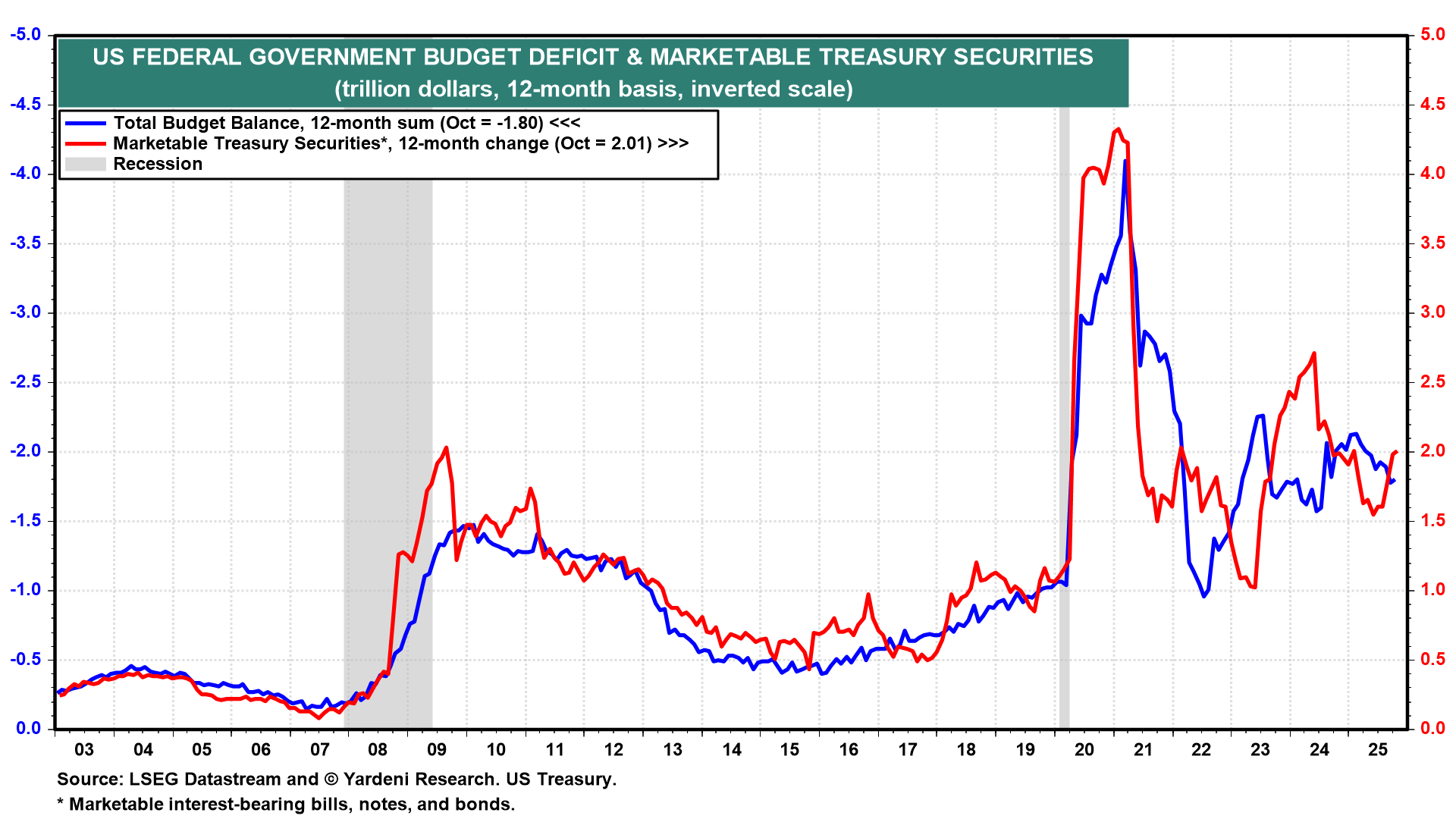

(6) Federal deficit. The annual US federal deficit totaled $1.8 trillion through October, while the Treasury raised $2.0 trillion over the same period. (chart).

Federal government outlays have flattened out in recent months at around $7.0 trillion (chart). Spending on social welfare programs rose to a record $3.6 trillion over the 12 months through October. Net interest outlays rose to a record $980 billion, exceeding the $910 billion spent on defense.

Federal tax receipts rose to a record $5.3 trillion over the 12 months through October (chart). Individual income tax receipts are still growing. Payroll tax receipts have stalled, along with payroll employment gains, in recent months. Customs duties are up by a record $230 billion over the past 12 months. Corporate tax receipts edged lower recently.