The Roaring 2020s has been a wild decade so far. During 2020, we all had to deal with the first wave of Covid. During 2021, we had to deal with another wave or two of Covid. During 2022, Russia invaded Ukraine, inflation soared, and the most widely anticipated recession of all times remained widely anticipated.

During 2023, that same story played out for most of the year but with a few additions: The Gaza War has been raging since October 7, 2023. China fell into a recession and repeatedly threatened to invade Taiwan. And of course, Fed policy was criticized by some for being too easy during the pandemic and then too tight (or not tight enough) as interest rates soared by 500bps or more, fueling fears of persistent inflation and a recession. There was one important difference between 2022 and 2023: Inflation moderated significantly during the latter year, heightening expectations that the Fed is done tightening and would be easing this year.

Yet during those four dangerous years, the S&P 500 advanced 47.6% from the end of 2019 through the end of 2023 (Fig. 1 below). Currently, investors seem to be carefree. Their mantra seems to be: “We have nothing to fear but fear itself.” Last year ended with a burst of optimism among stock market investors that triggered a powerful rally (Fig. 2). (Our mantra during carefree times like now is: “We have nothing to fear but nothing to fear.”)

At the start of last year, it was widely expected that the stock market would remain in a bear market during the first half of the year and rebound during the second half. At least that was the widely reported view of some of Wall Street’s leading investment strategists. The reverse happened: The S&P 500 rallied during the first half by 19.5%, fell into a 10.3% correction from July 31 through October 27, then experienced a meltup through the end of the year for a gain of 24.2%. When it had nearly achieved our year-end target of 4600 as early as July 31, we concluded that the remainder of the year might see the rally stall for a while.

This year, we wouldn’t be surprised if the S&P 500 stalls during the first half of the year and then rallies to 5400 by the end of the year.

Here are four of the clear and present dangers that we will be monitoring in coming days:

(1/4) Hawkish Fed talk.

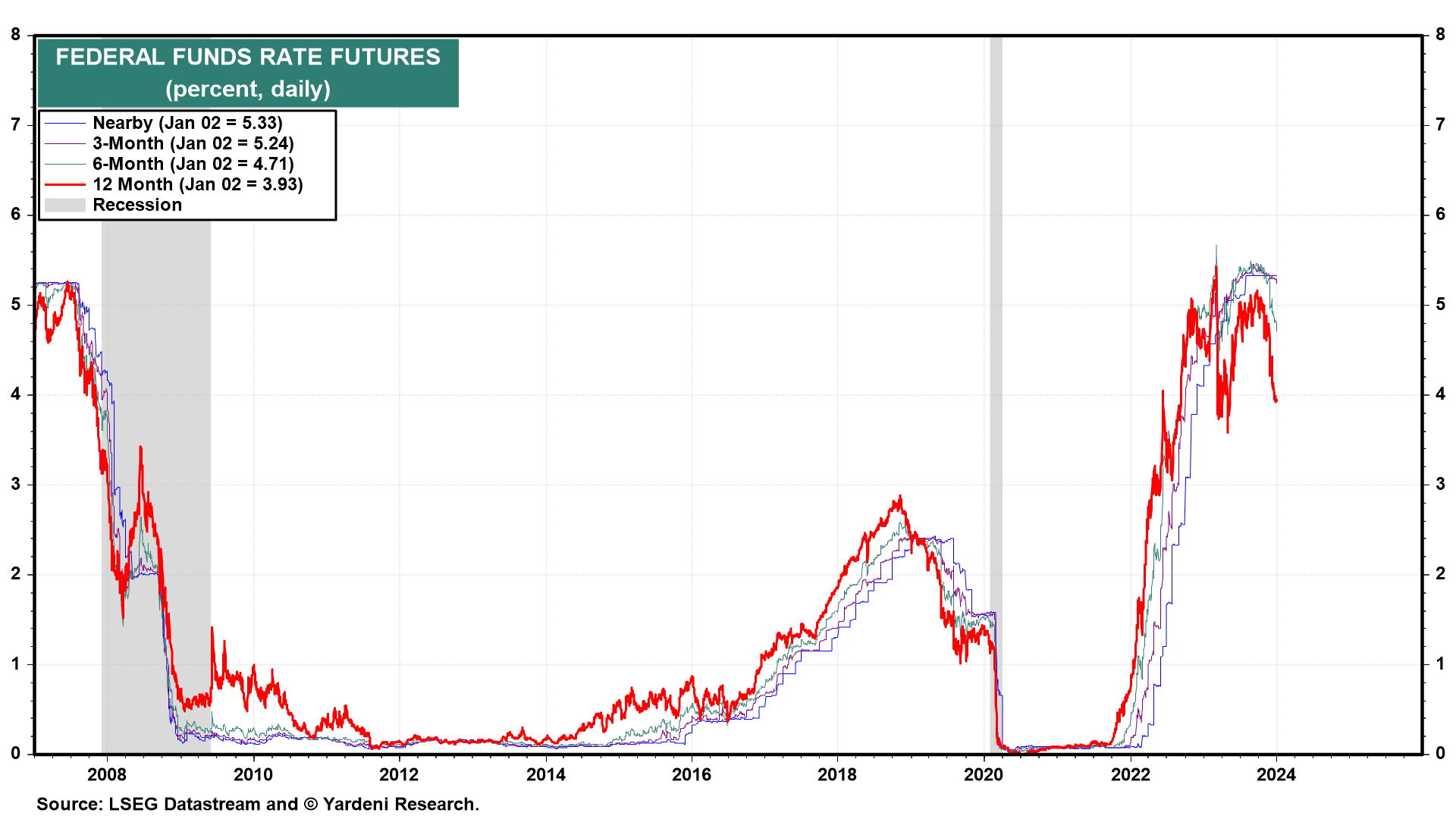

Odds are that Fed officials will start the new year by trying to lower expectations for rate cuts this year. At the end of last year, the 12-month federal funds rate futures yield was down to 3.95% (Fig. 3 below). That implies five 25bps cuts in the federal funds rate by the end of this year. The FOMC’s December Summary of Economic Projections implied three such reductions.

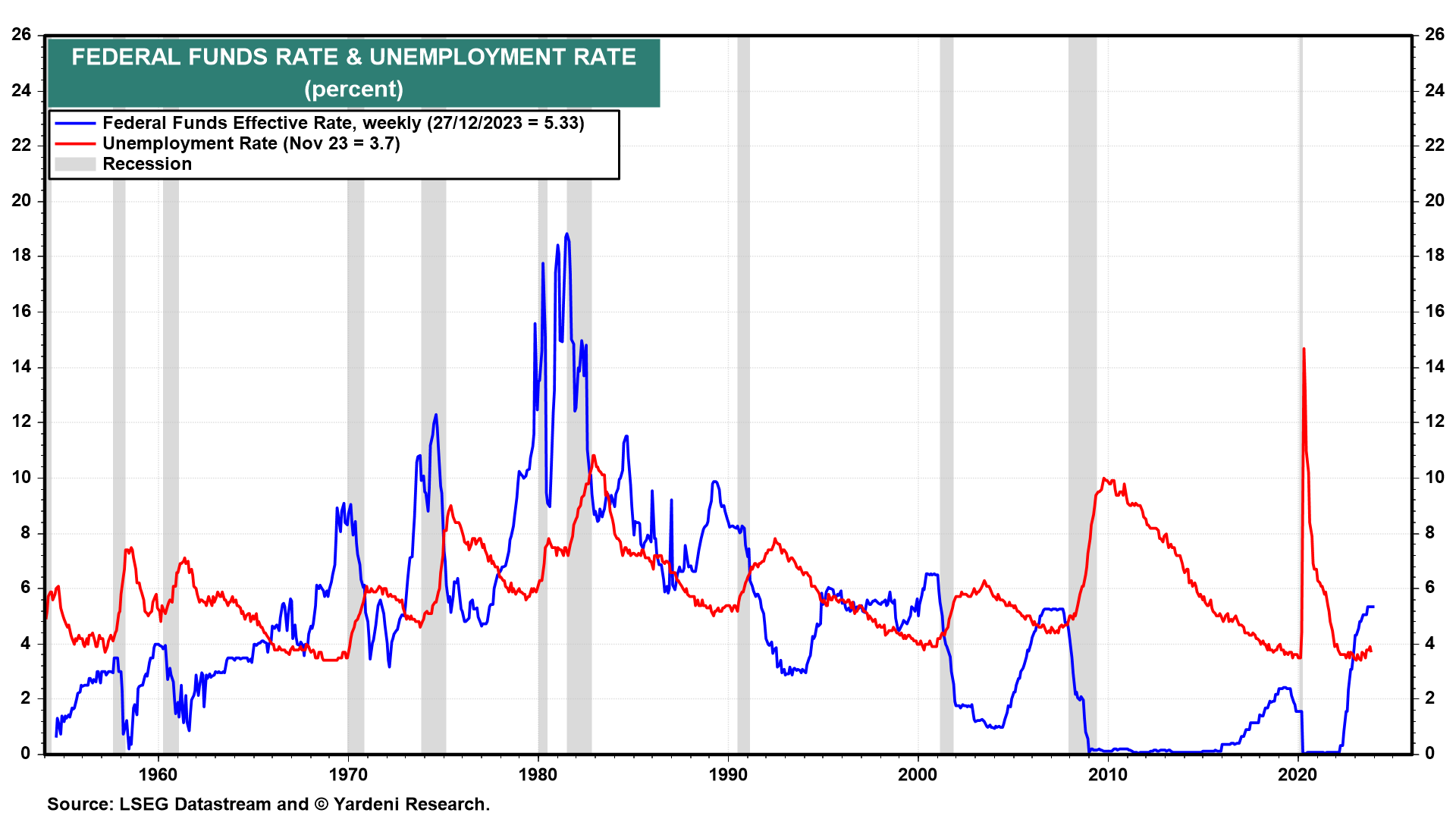

The stock and bond rallies since late October might have discounted an easier monetary policy this year than Fed officials are likely to deliver. That’s even if the inflation rate drops down to their 2.0% target ahead of schedule (Fig. 4). They will continue to be data dependent. As long as the unemployment rate remains below 4.0%, they are likely to hold off on easing, in our opinion. That’s because their worst nightmare would be a rebound in inflation.

Fed easing cycles are most pronounced during recessions. We don’t expect a recession this year nor do we expect that the Fed will have to ease significantly to avert a recession. The federal funds rate is inversely correlated with the unemployment rate, which we expect will remain under 4.0% at least during the first half of this year (Fig. 5 below). If inflation continues to fall toward the Fed’s 2.0% target and the jobless rate rises above 4.2%, then a more aggressive easing policy is likely.