Iran's Supreme Leader Ali Khamenei was killed on Saturday along with 40 other top Iranian leaders when the US and Israel launched a military campaign against Iran’s Mullah regime.

In a February 28 post on The Free Press, historian Niall Ferguson observed that President Donald Trump’s approach to dealing with America’s adversaries in Latin America and the Middle East isn’t regime change but regime alteration: “Indeed, regime alteration is the practical consequence of the approach laid out in Trump’s National Security Strategy published late last year. The strategy rules out the deployment of American ground forces, except for special forces. It requires a short time frame for military operations. It will disappoint those who want to fast-track Venezuela and Iran to democracy. But the lesson of Iraq has not been lost on Trump.” So no boots on the ground.

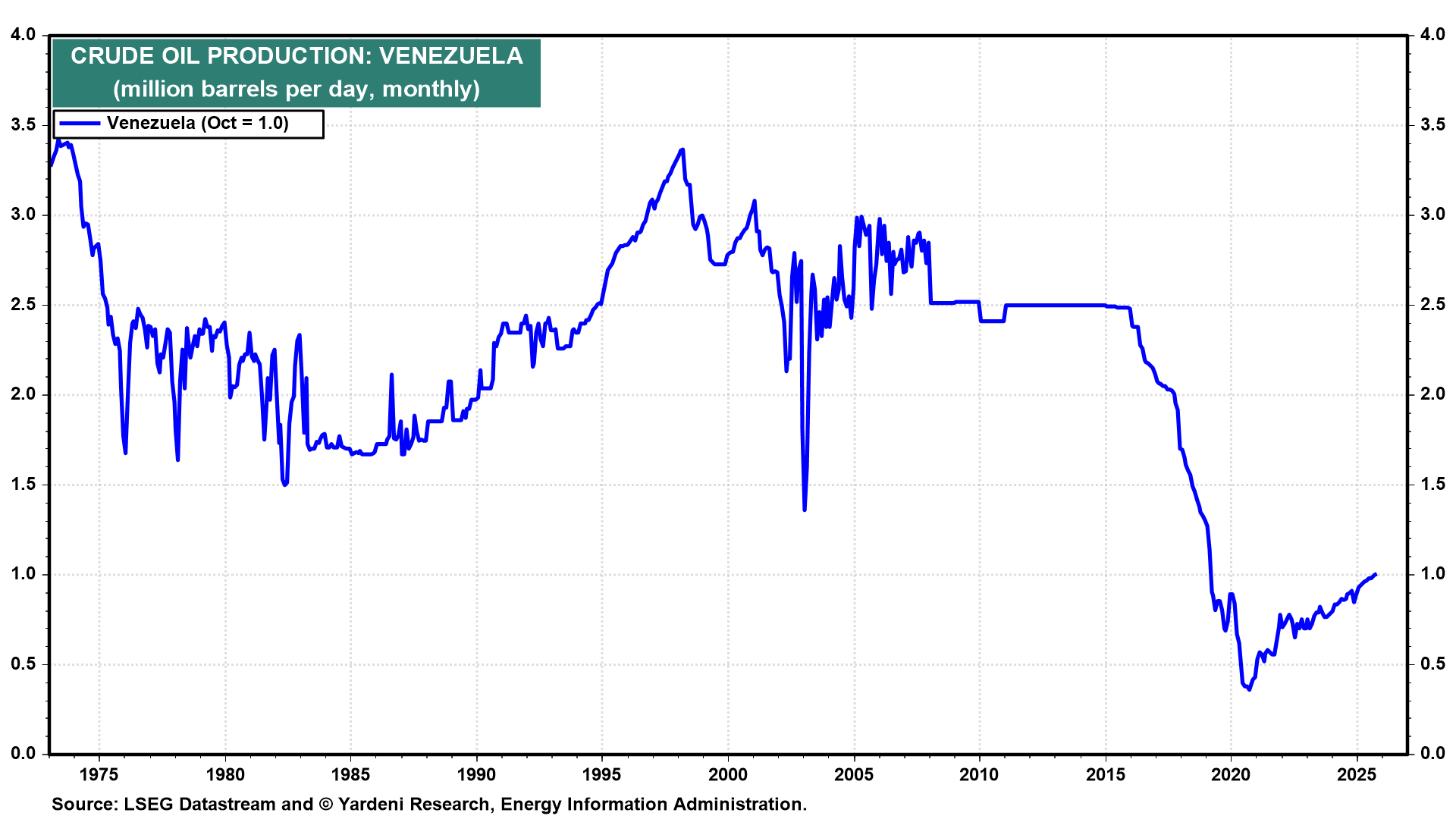

In Venezuela at the beginning of the year, Trump snatched President Nicolás Maduro and replaced him with Delcy Rodríguez, leaving the structure of the regime in place but requiring her to follow Washington's commands, including on the country’s oil production and exports (Fig. 1 below).

{kind=link}

Trump seems to be angling for a regime alteration in Cuba by cutting off the country’s access to oil from Venezuela. In Iran, Trump’s goal is to force the next regime to end the previous regime’s ambitions of building nuclear weapons, destroying Israel, and dominating the Middle East by supporting terrorist organizations around the region.

Now that the “Axis of Evil” has lost Iran and Venezuela, what will be the impact and reaction of its other three members, China, North Korea, and Russia? Losing Iran is a big blow to Russia, which received military equipment, especially drones, from Iran. China imports lots of oil from Iran and has invested significantly in the country. In North Korea, Little Kim is probably scrambling to fortify his bunker. China has seen America’s military might in action twice in Iran and once in Venezuela since the start of Trump’s second term. China’s leaders might now consider postponing any planned invasion of Taiwan.

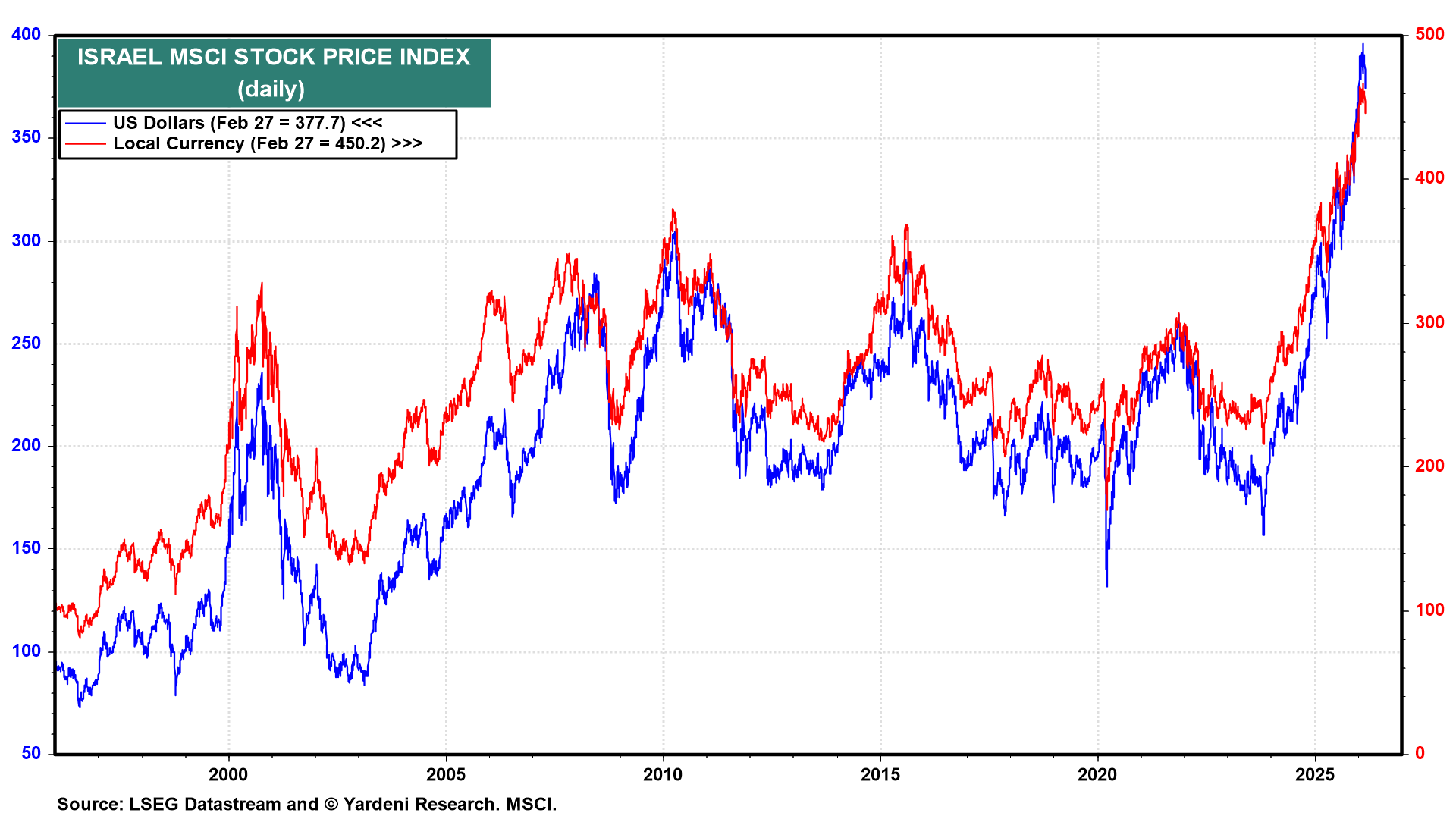

In the Middle East, the terrorist proxies of Iran’s Mullahs in Gaza (Hamas), Lebanon (Hezbollah), and Yemen (Houthis) have already been decapitated once by the Israelis. Now they’ve lost their puppet master in Tehran. The Abraham Accords are likely to be expanded to include more Arab countries. The Israeli stock market has been discounting this scenario for the past two years (Fig. 2 below).

{kind=link}

For the financial markets, the immediate issue is whether Iran’s decapitated regime will block the Strait of Hormuz. We are not military experts, but it seems to us that if that were going to happen, it would have happened by now. The probable reason it hasn’t is that the US and Israel have incapacitated Iran’s navy. At the same time, it is very unlikely that the two allies would have done any damage to Iran’s oil production and export facilities (Fig. 3). As in Venezuela, Trump probably expects to be running Iran’s oil business from the White House soon.

{kind=link}

Of course, in the next few days, oil prices could spike higher. Indeed, Reuters reported that Brent crude jumped 10% to about $80 a barrel over the counter on Sunday, according to oil traders, while analysts predicted that prices could climb as high as $100 (Fig. 4). Most tanker owners, major oil companies, and trading houses have suspended crude oil, fuel, and liquefied natural gas shipments via the Strait of Hormuz, trade sources said, after Tehran warned ships against moving through the waterway. More than 20% of global oil is moved through the Strait of Hormuz.

Meanwhile, on Sunday, Iranian Foreign Minister Abbas Araghchi said that a new supreme leader could be chosen within days. He also said that Iran has no intention of closing the critical shipping lane at present nor any plans to do “anything that would disrupt navigation at this stage.” That might be because reports indicate that a total of nine Iranian naval ships have been destroyed and sunk since the operation began on Saturday. Some of these are described as relatively large and important vessels. Trump also announced that the Iranian Naval Headquarters had been “largely destroyed” in a targeted strike.

In any event, oil prices are likely to fall in the coming months, assuming this war is short, as it’s bound to be. That should help to bring US headline inflation down to the Fed’s 2.0% y/y target. Lower gasoline prices will boost consumers’ purchasing power in the US and around the world (Fig. 5 below). Both US and global economic growth should benefit from lower oil prices. After an initial negative reaction to the war, stock markets around the world should resume setting record highs, especially in oil-importing countries throughout Asia (Fig. 6). So most emerging economies’ stock markets should continue to outperform (Fig. 7).

{kind=link}

{kind=link}

{kind=link}

We’ve held back on overweighting the S&P 500 Energy sector because we expect ample global supplies to offset near-term jitters about the outcome with Iran (Fig. 8). Events over the weekend suggest that the recent weeks’ energy stock rally might continue for a few more days and then fizzle in our short-war scenario.

{kind=link}

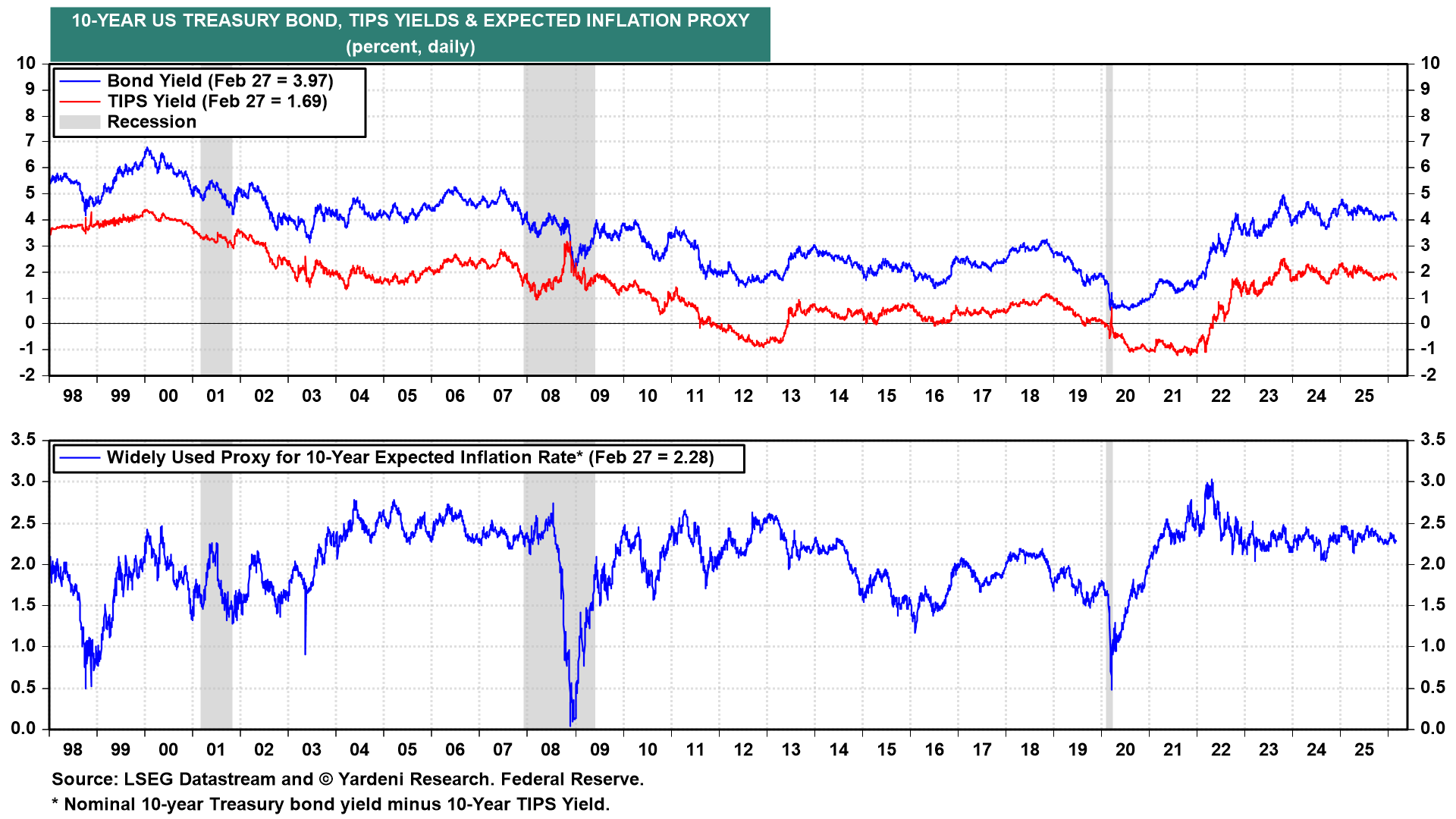

Geopolitics II: What About Interest Rates? On Friday, despite mounting evidence that another conflict in the Middle East was imminent, the 10-year Treasury bond yield fell below 4.00% (Fig. 9 below). That happened even though January’s PPI inflation rate was hotter than expected (Fig. 10). Furthermore, the January 27-28 FOMC minutes, released on February 18, were relatively hawkish, with some members of the monetary-policy committee explicitly raising the possibility of rate hikes assuming that there are no clear indications that disinflation is firmly on track. At the time of the meeting, the bond yield was at 4.25%.

{kind=link}

{kind=link}

Despite the decline in the yield since then, it remains at the bottom of a relatively tight range that has persisted for the past three years (Fig. 11 below). In the happy-go-lucky scenario we outlined for the Middle East and oil prices, the yield may continue to fall, as it has often tracked oil prices in the past, except for the past few weeks (Fig. 12). A faster decline in inflation because of falling oil prices might help incoming Fed Chair Kevin Warsh (assuming he is approved by the Senate) convince FOMC members to lower the federal funds rate (Fig. 13). We think that would increase the likelihood of bubbles inflating in financial asset markets.

{kind=link}

{kind=link}

{kind=link}

However, the US Treasury bond market may be signaling that the clear and present danger of financial bubbles lies in the private credit markets, as evidenced by the falling prices of ETFs that invest in private credit lenders. FOMC officials might be persuaded to lower the federal funds rate to avert a financial crisis starting in that market.

Of course, if something significant breaks in the private credit market, the Fed will rapidly create an emergency liquidity facility and lower the federal funds rate. The Fed has lots of experience doing so from its previous Whac-A-Mole play during the Great Financial Crisis, the Great Virus Crisis, and the Mini-Banking Crisis (Fig. 14).

{kind=link}

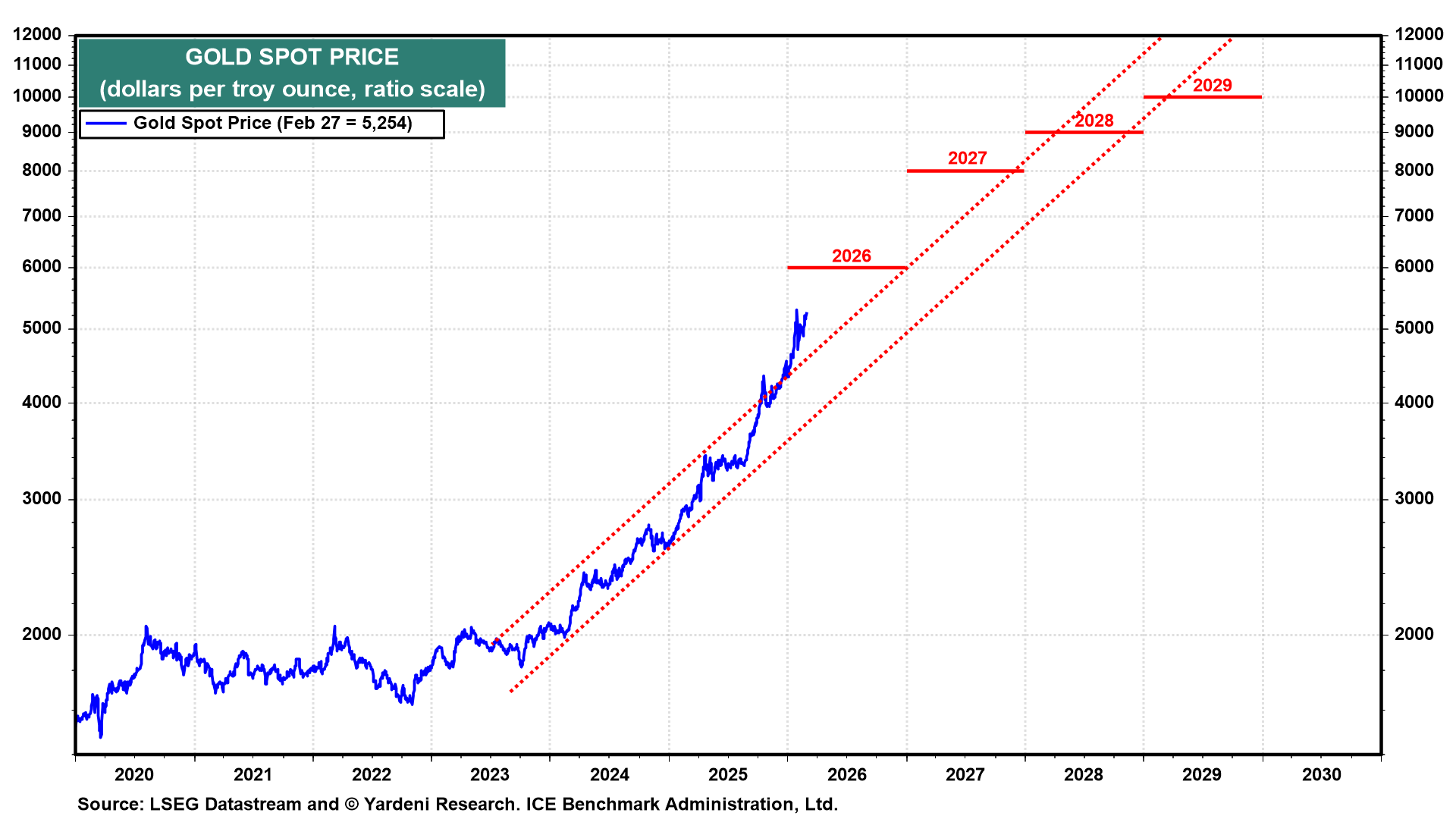

Geopolitics III: What About the Price of Gold? Of course, the US Treasury bond yield may also be falling because of safe-haven demand. The price of gold is likely to rise this week for the same reason, especially if the price of oil spikes. However, the latest developments in the Middle East over the weekend suggest that geopolitical risks are likely to decrease rather than increase, as discussed above. That’s assuming that the Iranian regime doesn’t rise from the dead. But that’s not very likely now that so many of its top leaders have been martyred and are presumably having lots of fun in the afterlife.

For now, we are still targeting $6,000 per ounce for the price of gold by year-end and $10,000 by the end of the decade (Fig. 15 below). But we would be inclined to book some trading profits in the event of a big jump to the upside in the prices of gold and oil, especially in the latter since we don’t believe a jump would be sustainable.

{kind=link}

Geopolitics IV: The Roaring 2020s & Beyond. We’ve been considering whether to revise our subjective probabilities for our three economic and stock market scenarios for the rest of this year. We’ve decided to leave them as is, notwithstanding the latest developments in the Middle East. In fact, these developments, and the happy outcome we discussed above gives us more confidence in them:

(1) Our Roaring 2020s base-case scenario remains at 60%. If the postwar outcome of our short-war scenario plays out, oil prices will be lower. Consumer confidence, purchasing power, and spending will get a boost from lower oil prices and greater stability in the Middle East. The odds of a recession and a bear market would remain low. Corporate earnings would continue to rise as both the US and global economies benefit from lower oil prices (Fig. 16). Our Roaring 2020s targets for the S&P 500 remain intact at 7,700 by the end of this year and 10,000 by the end of 2029 (Fig. 17). The Roaring 2020s would be followed by the Roaring 2030s.

{kind=link}

{kind=link}

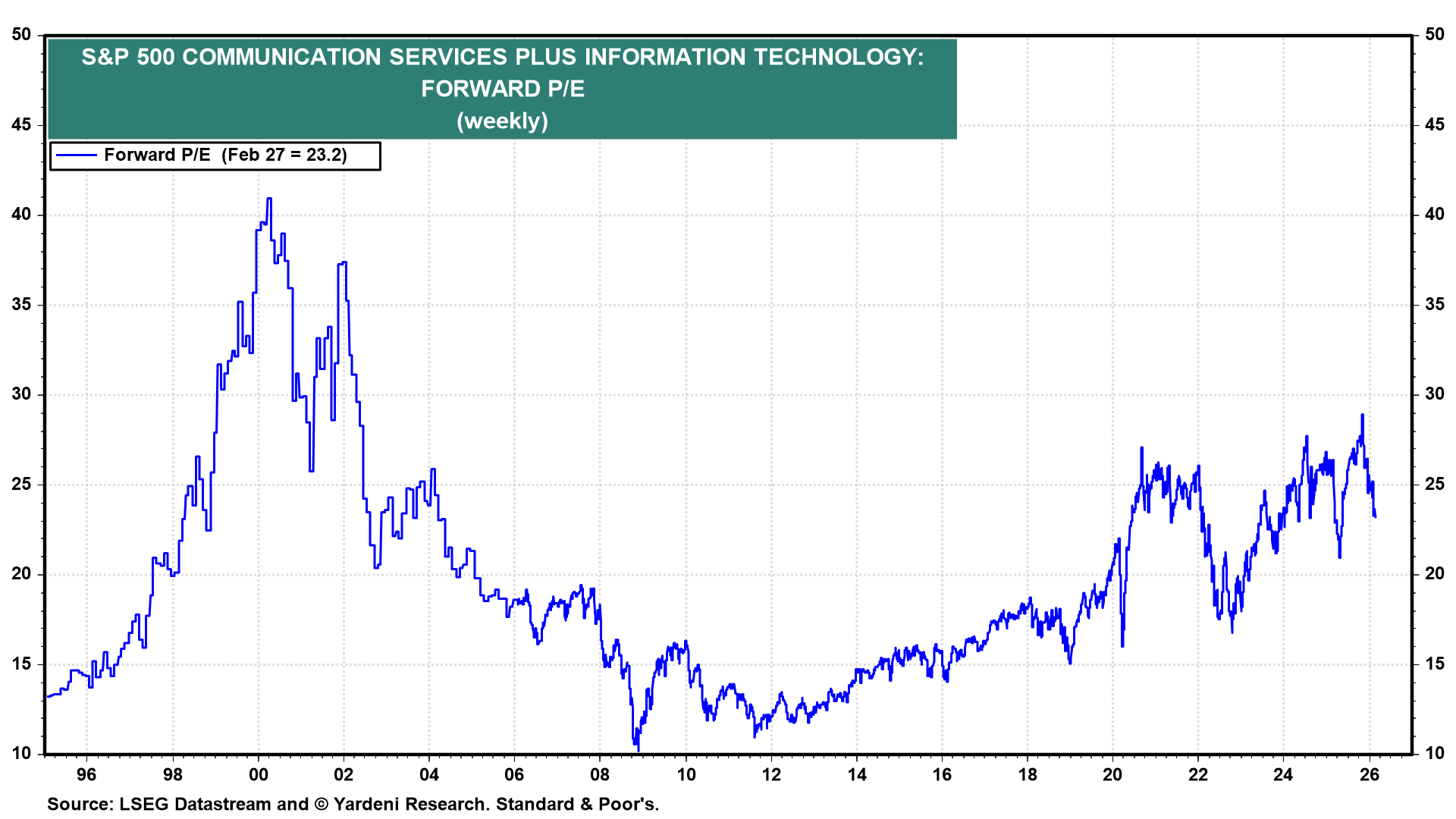

(2) Our Meltup scenario remains at 20%. We have been thinking about lowering the odds of our Meltup scenario given the weakness in the stock market so far this year, as the air is coming out of the AI stocks. However, we are encouraged to see that the decline in the forward P/Es of the Magnificent-7 has been mostly offset by rising valuation multiples among the Impressive-493 (Fig. 18 and Fig. 19). A happy outcome of the latest turmoil in the Middle East could certainly drive stock prices higher around the world.

{kind=link}

{kind=link}

Arguably, there was a stock market meltup last year in the S&P 500 Information Technology and Communication sectors, particularly the Magnificent-7. The stock market action so far this year shows that this excess is being cured by investors rebalancing to other sectors and to overseas stock markets (Fig. 20 below). A meltup doesn’t have to set the stage for a meltdown, and certainly not one that triggers an economic recession.

{kind=link}

(3) Our Meltdown scenario remains at 20%. We have previously identified the two biggest risks to the two bullish scenarios above as a geopolitical crisis, particularly in the Middle East, and a financial crisis, particularly in the US private credit market. Now we are thinking that the risks of the former are declining (in a short-war scenario) and that the risks of troubles in the private credit markets are increasing.

If the private credit market seizes up, the Fed will most likely respond rapidly with an emergency liquidity facility and cuts in the federal funds rate, as mentioned above. In other words, a meltdown scenario is likely to offer lots of good buying opportunities as the Roaring 2020s roar into the Roaring 2030s!

Of course, we could be wrong about the length of the war and the spike in oil prices. During the 1970s, the two oil shocks in the Middle East boosted inflation and interest rates and depressed stock markets worldwide. For now, we are still assigning a 20% subjective probability to our risk bucket of everything that could go wrong. Stay tuned.