Stock and bond prices fell today as oil prices rose back to around $100 per barrel. The US and Israel continue to pound Iran from the air, but Iran's regime continues to launch missiles and drones at Gulf nations and vessels, and Israel too. The WSJ reported today that "Israeli officials assess Iran's ruling regime is unlikely to fall soon, as its rulers remain in control and conditions aren't ripe for an uprising." The stock market may be starting to discount the possibility that the war won't be short and that the Strait of Hormuz may remain effectively closed for some time.

The S&P 500 is now down 4.4% from its record high on January 27. The Nasdaq is down 6.4% from its record high on October 28. We are still expecting a 10%-15% correction in both. Adding to the stock market's woes are rising bond yields. The 10-year US Treasury bond yield bottomed at 3.95% on February 27, a day before the war started, and is at 4.26% this evening. The financial markets are starting to discount that the war might be stagflationary.

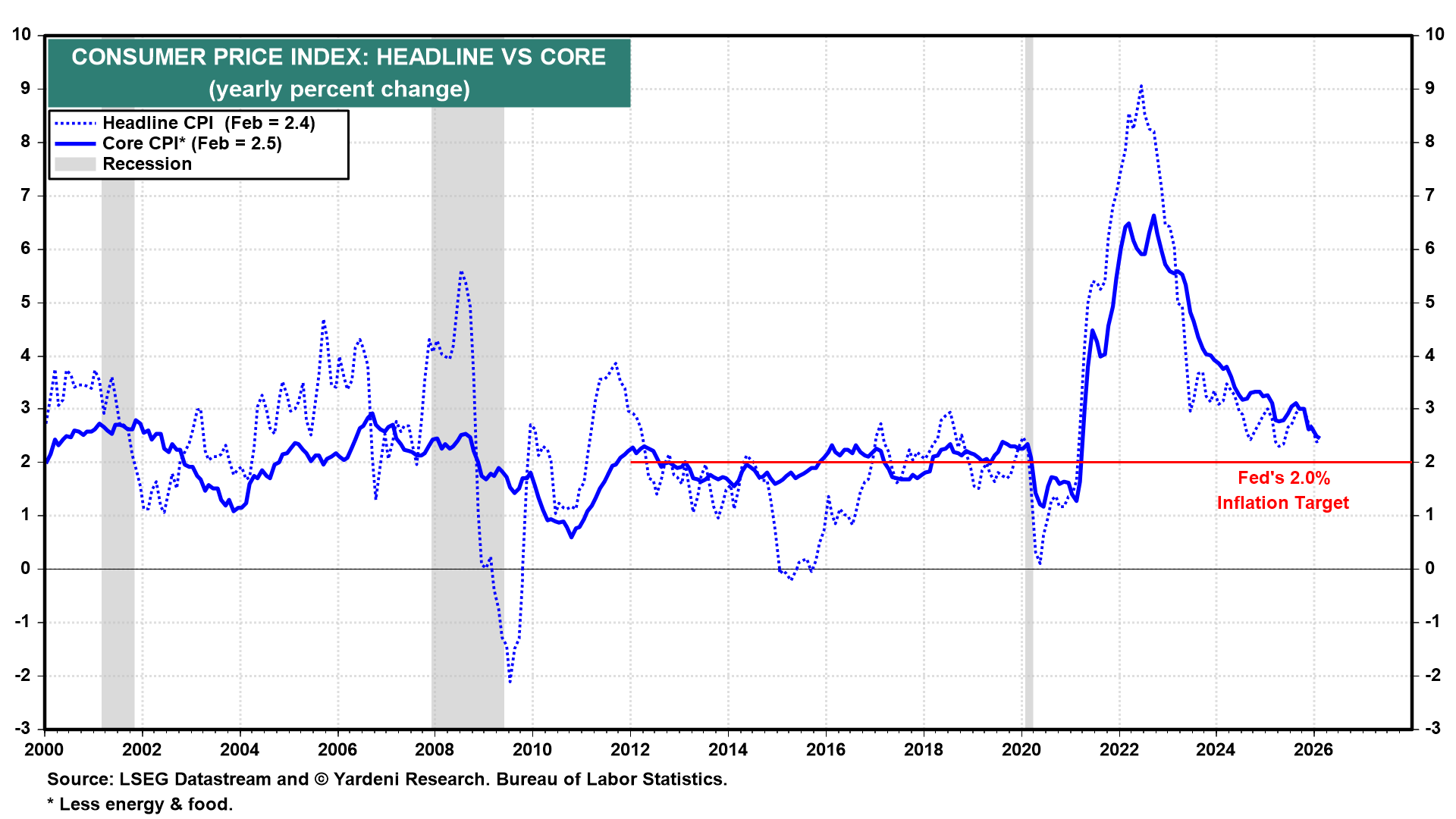

Let's briefly review the latest batch of US economic indicators, which are all pre-war:

(1) CPI. The bond market is starting to anticipate that the decline in inflation over the past couple of years, through February of this year, is about to be reversed by rising energy prices because of the war, rising food prices because of a shortage of fertilizer, and higher airfares as a result of more expensive jet fuel. Many other prices will also increase in the coming months because of the spike in oil prices. That's too bad because the CPI is almost down to the Fed's 2.0% inflation target (chart).

Excluding shelter, the CPI is up only 2.1% y/y (chart). The CPI's measure of rent of primary residence rose 3.2% y/y last month, well above the Zillow Rent Index (2.2%) and the ApartmentList Rent Index (-1.5%). That was the pre-war situation, which is no longer relevant.