On October 29, Fed Chair Jerome Powell said, "[W]hat do you do if you're driving in the fog? You slow down." He was referring to the lack of economic data due to the government shutdown. The Fed and the financial markets now have been deprived of two monthly employment reports. Add to the shutdown casualties list the October PPI and CPI, which would've dispelled some of the fog.

All this is complicating the debate about whether the Fed might cut rates next month for what would be a third time in 2025. It also adds drama to Fed speaking engagements in the days ahead. They include Governors Michael Barr opining on artificial intelligence and innovation (Tue), Christopher Waller speaking on payments (Wed), and Stephen Miran (Wed) speaking generally in a fireside chat over in the UK.

Regional Fed presidents speaking include: New York's John Williams (Wed, Thu), Philadelphia's Anna Paulson (Wed), Atlanta's Raphael Bostic (Wed, Thu), Boston's Susan Collins (Wed), St. Louis' Alberto Musalem (Thu), Cleveland's Beth Hammack (Thu), Kansas City's Jeff Schmid (Fri), and Dallas' Lorie Logan (Fri).

In other words, the Federal Open Mouth Committee will be very vocal this week.

Though the government won't be reporting official data in the week ahead, here's a look at other upcoming data releases likely to confirm that the economy is still growing and inflation remains above the Fed's 2.0% target:

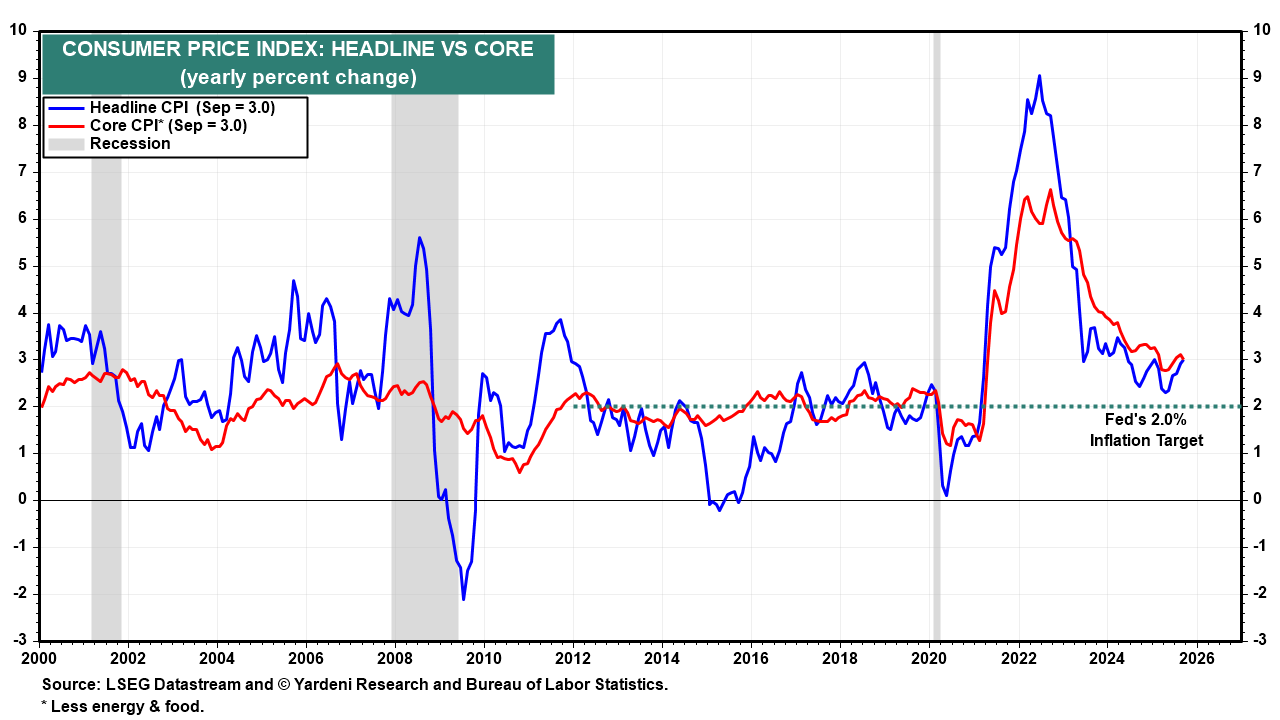

(1) CPI Inflation. The Cleveland Fed's Inflation Nowcasting shows that the headline and core CPI inflation rates rose 2.96% and 2.99% y/y, respectively, in October. In recent months, the CPI core inflation rate has been stuck around 3.00% (chart).

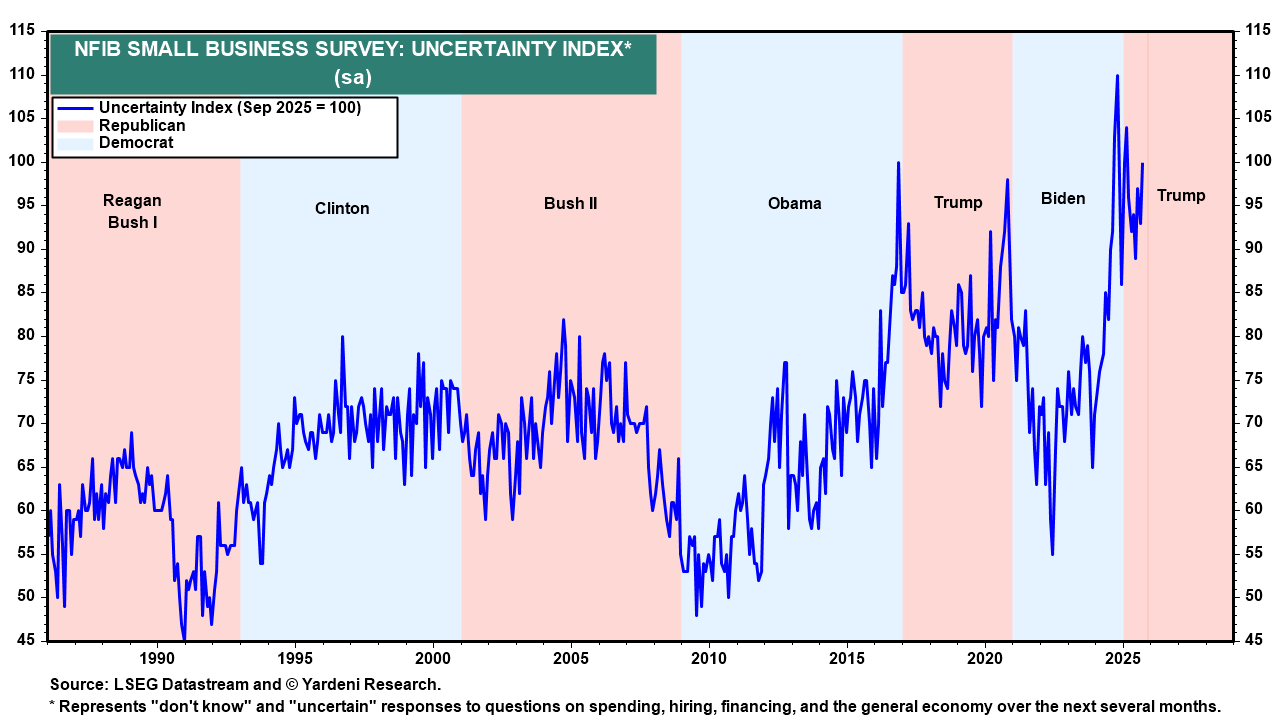

(2) Small business survey. October's small business owners' survey (Wed), compiled by the National Federation of Independent Business, is likely to show that uncertainty remains high due to the government shutdown (chart). That might continue to weigh on the survey's labor market indexes, which we monitor closely.

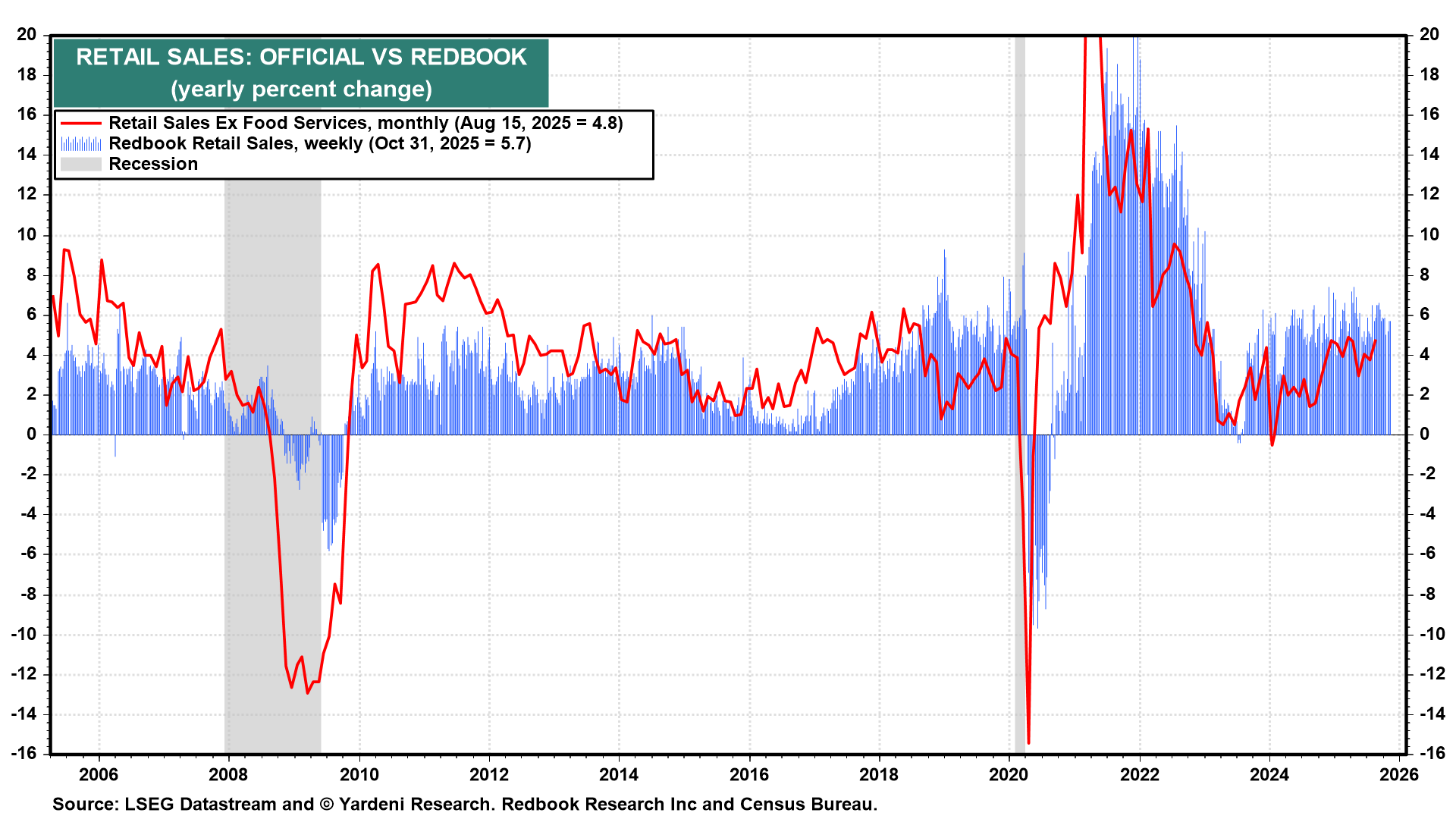

(3) Retail sales. Last week's Redbook Retail Sales Index (Tue), covering the tail end of October, rose 5.7% y/y, confounding the economic bears. Odds are good that the next reading will show that consumers are spending and that layoffs aren't widespread enough to weigh on consumer spending (chart).

(4) ADP weekly jobs data. ADP's national employment report will have market participants eyeing its weekly preliminary employment growth estimate (Tue) for any glimpse of clarity about labor market conditions amid the economic fog.