Now that the gavel has fallen on Donald Trump’s tariffs, the question is how the US president will try to save face. President Trump’s move on Saturday to slap 15% universal levies on the globe—up from an initial 10% on Friday—dispels the notion that Trump might’ve lost the taste for trade-warring. Where Trump takes tariffs now is anyone’s guess.

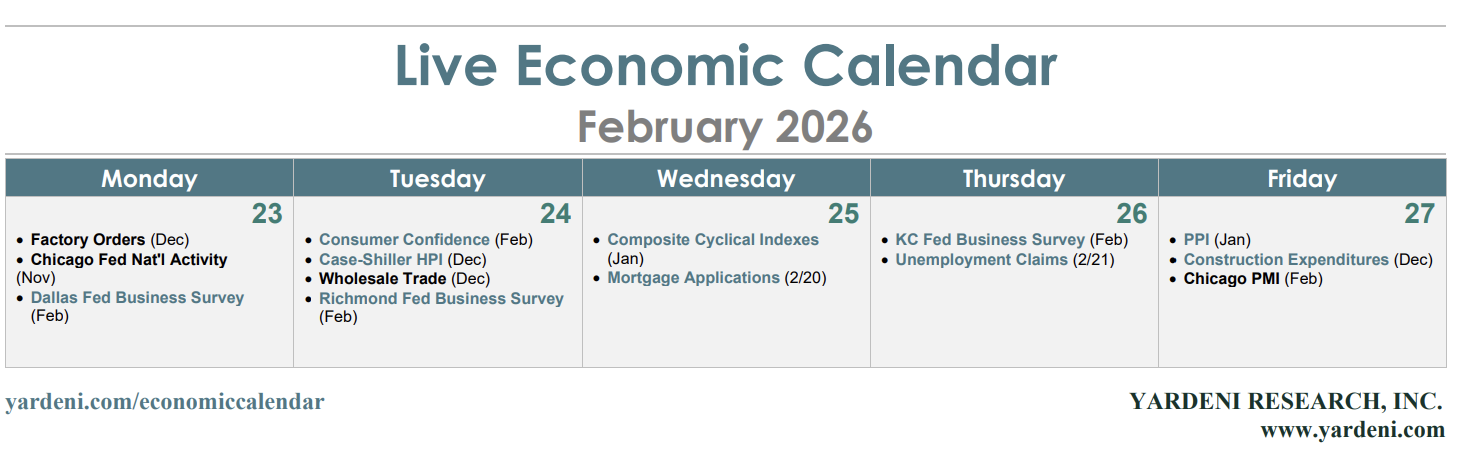

On Friday, the Supreme Court upheld a lower court ruling that Trump can’t bypass Congress and use the International Emergency Economic Powers Act (IEEPA) to impose global tariffs. Trump World claims that it has several workarounds. This uncertainty is sure to increase the drama surrounding Trump’s State of the Union address (Tue).

The same goes for the other international kerfuffle preoccupying world markets. Energy markets are on edge as the US military assembles the biggest collection of naval power and weapons systems in the Middle East since the early 2000s, and Trump hints at action against Tehran.

At home, the plot for Federal Reserve rate cuts has thickened, too. The minutes from the January Federal Open Market Committee meeting indicated that some officials think the next move could be to tighten. All this will increase attention on this week’s Fed members’ speaking engagements. Highlights include Governor Christopher Waller opining on the economic outlook (Mon) and tech disruption (Tue). Governor Lisa Cook tackles artificial intelligence and productivity (Tue).

For markets wary of AI-driven volatility, Nvidia’s Q4 earnings release (Wed) will serve as an economic indicator of sorts, along with the official ones scheduled this week. Here’s a look at those most likely to influence the timing—and, at this point, direction–of the Fed’s next move:

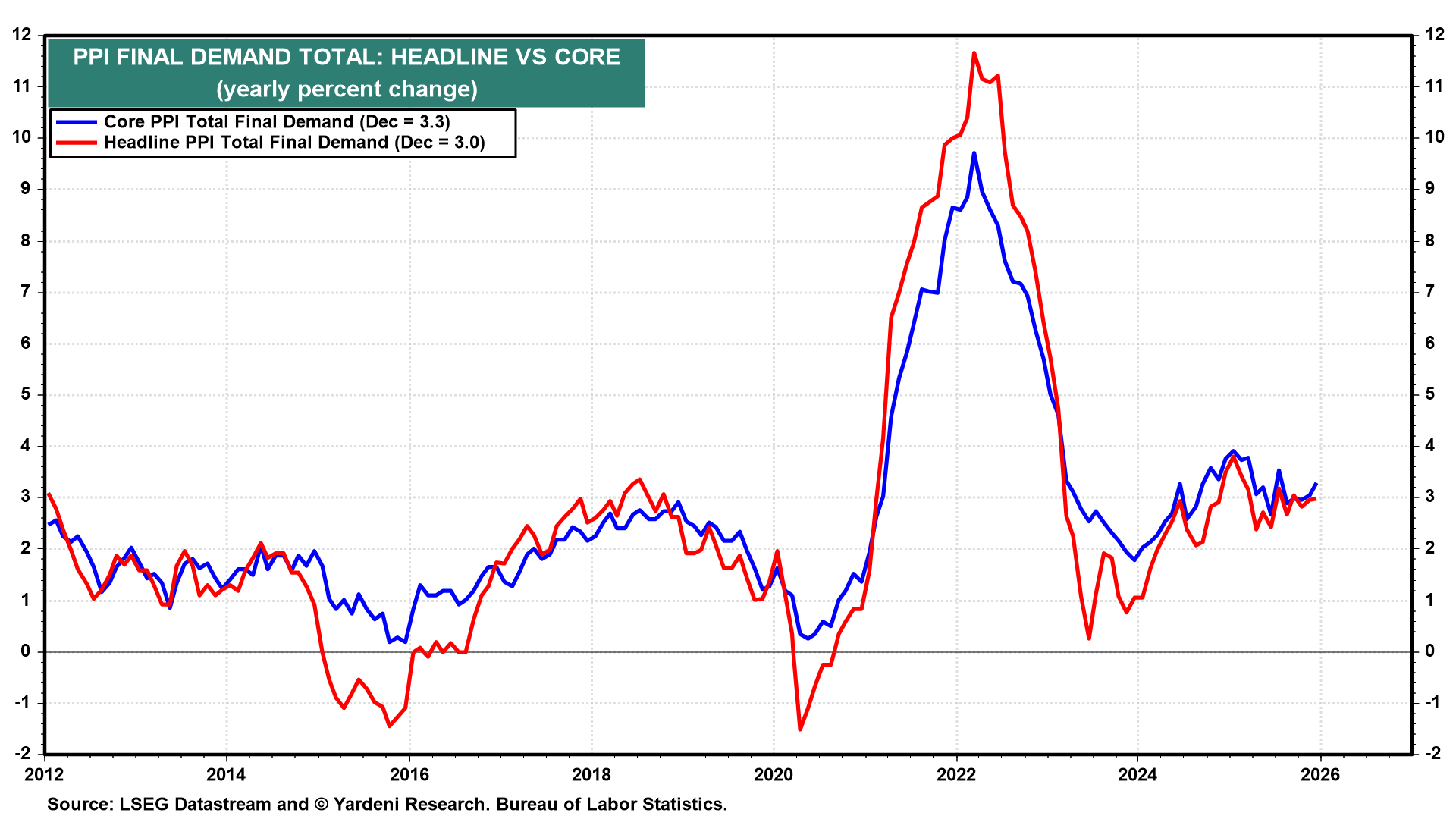

(1) Producer prices. Suspense abounds as the Bureau of Labor Statistics drops the January PPI (Fri). Forecasts are generally centered around 0.3% m/m for both the overall index and core wholesale prices (chart). That would signal something of a return to form following December’s 0.5% jump (up 0.7% for core prices).

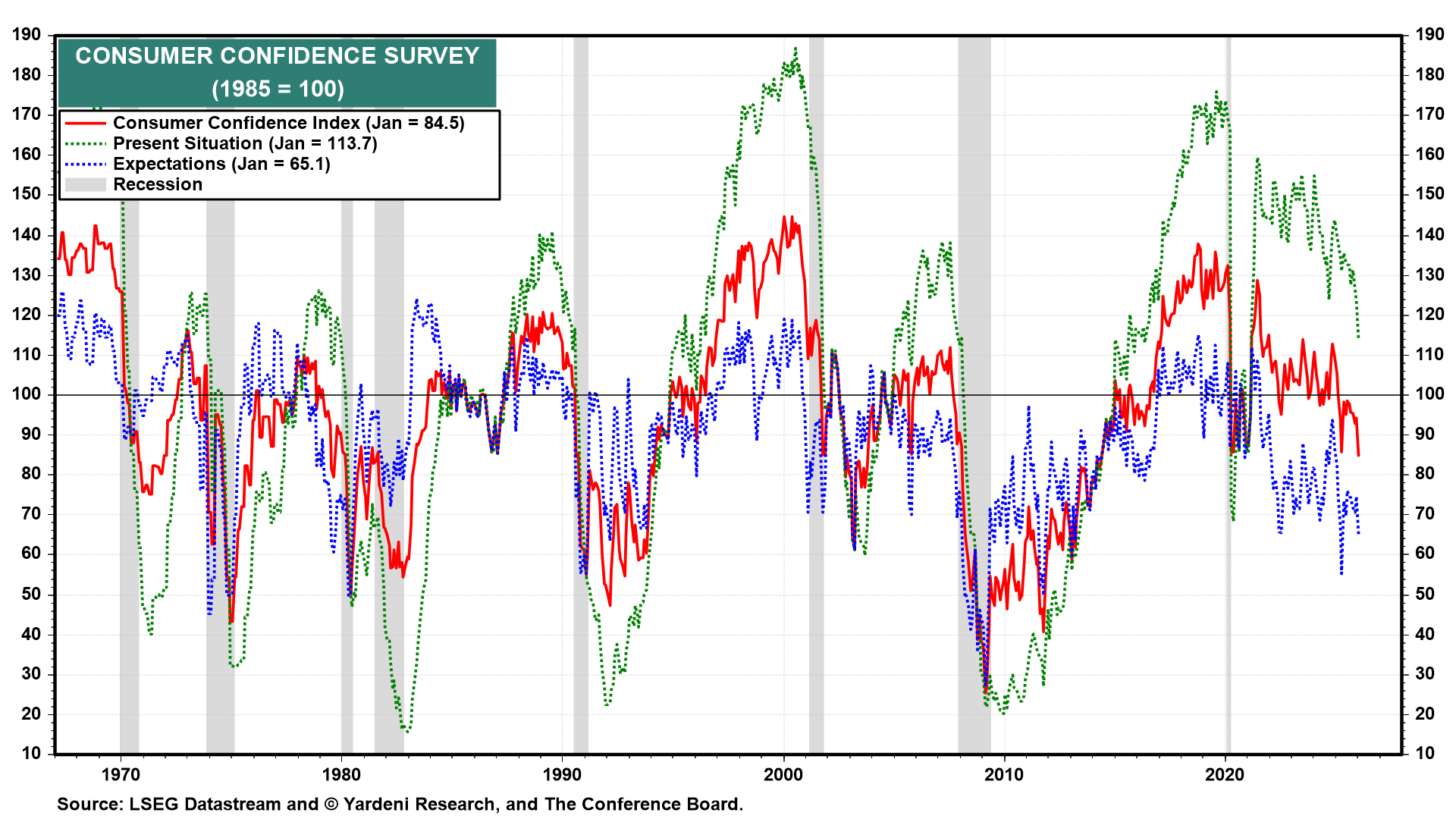

(2) Consumer confidence. The February survey (Tue) will provide an important reality check following a dismal January reading from the Conference Board. Last month, sentiment plunged to the lowest level—84.5—since May 2014 amid anxiety over labor market conditions (chart). With employment surprising to the upside in January, confidence likely stabilized or recovered some ground.

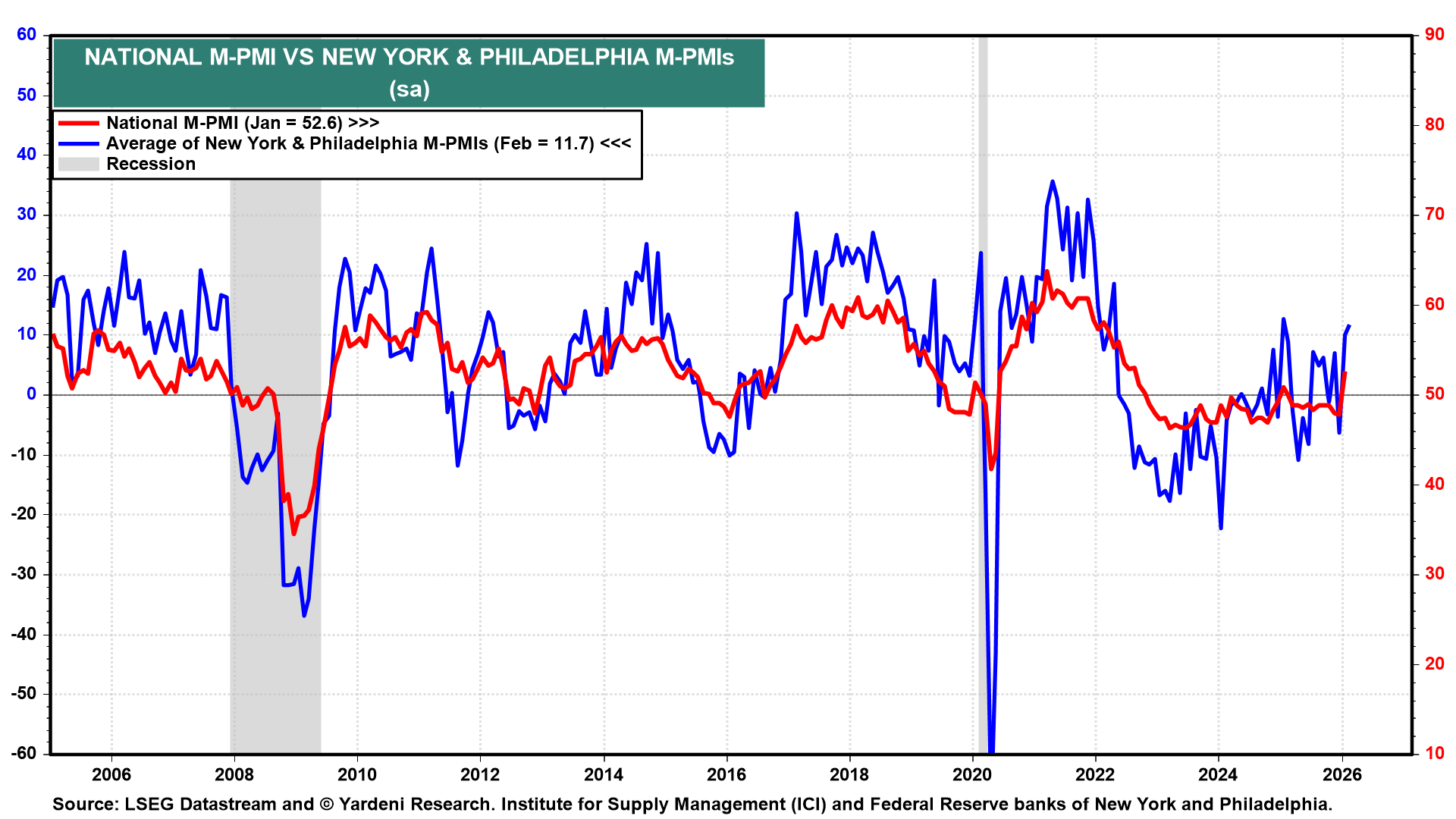

(3) Regional Fed surveys. As Fed Chair Jerome Powell and his fellow policymakers try to get a handle on growth dynamics, this week’s bevy of Fed business surveys could be illuminating. The Chicago Fed and Dallas Fed are out of the gate first (Mon), followed by the Richmond Fed (Tue) and Kansas City Fed (Thu). The New York and Philly surveys suggest business is improving (chart).

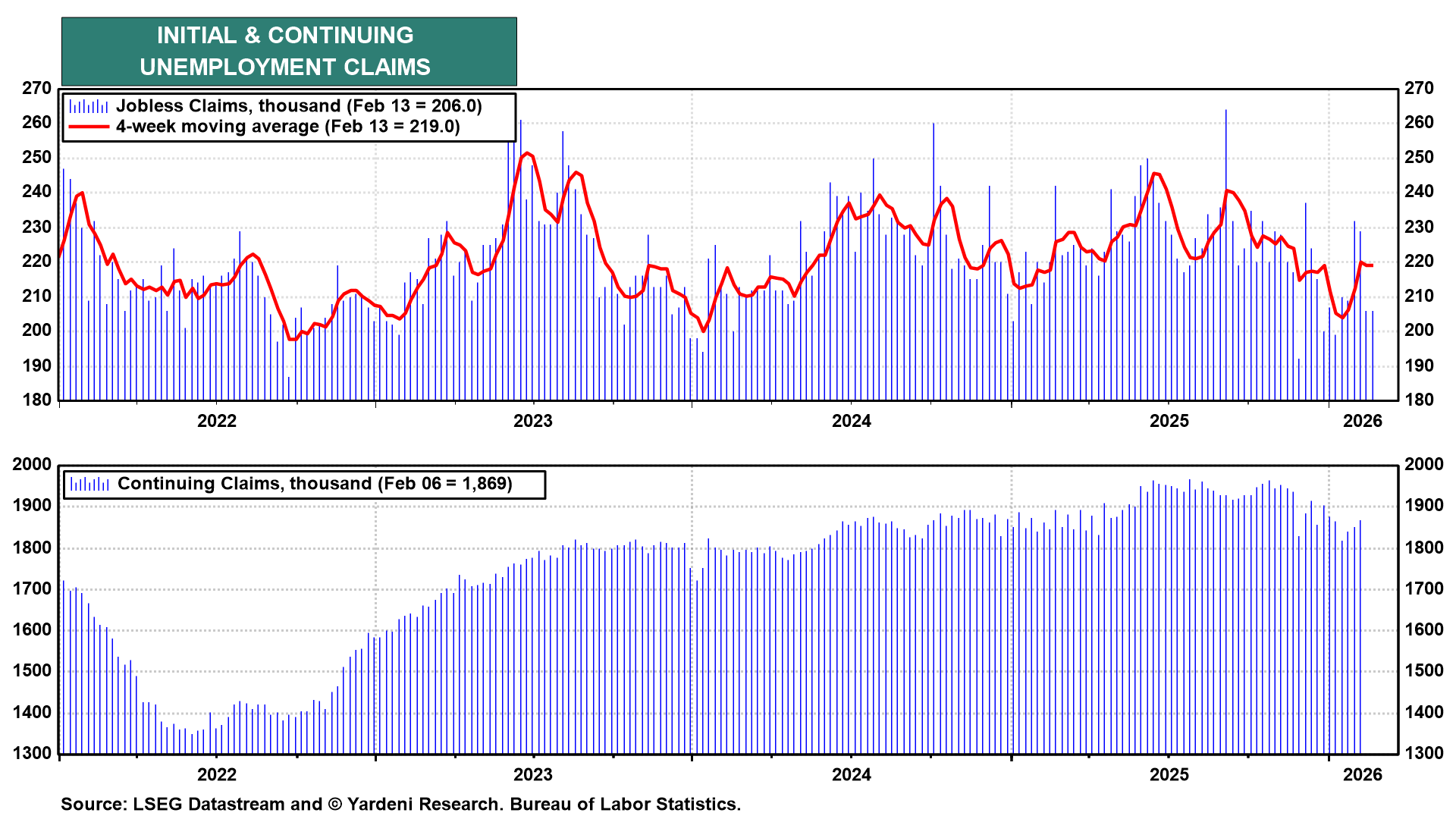

(4) Jobless claims. Last week’s larger-than-expected 23,000 drop in initial claims for state unemployment benefits fit with the view that the Fed should be in no hurry to ease again. This week’s data (Thu) could go a long way toward allaying fears that conditions might be weakening. That’s particularly so if claims come in at around the 206,000 level again (chart).