Layered on top of a still-developing trade war, President Donald Trump's attack on Iran puts markets in decidedly uncharted territory. Much will depend on how Iran responds to the attack. Trump said in Saturday's White House address, if Iran doesn’t "make peace" then "future attacks will be far greater and a lot easier."

In addition, Trump's "Big Beautiful Bill" could make fresh headlines this week as Senate Republicans gear up for a potential vote on their tax-cut tweaks to the House version. Also, Fed Chair Jerome Powell delivers his two-day semiannual monetary policy report to Congress on Tuesday and Wednesday.

Yet, despite the fog of wars (over US tariffs, Iranian nukes, and the US federal budget), the US economy continues to hum along. This week's data are likely to remind markets that, for all the uncertainties, the underlying economy is holding its own.

Here's a look at the upcoming US data releases with the greatest chance of influencing markets as well as the Fed's wait-and-see approach:

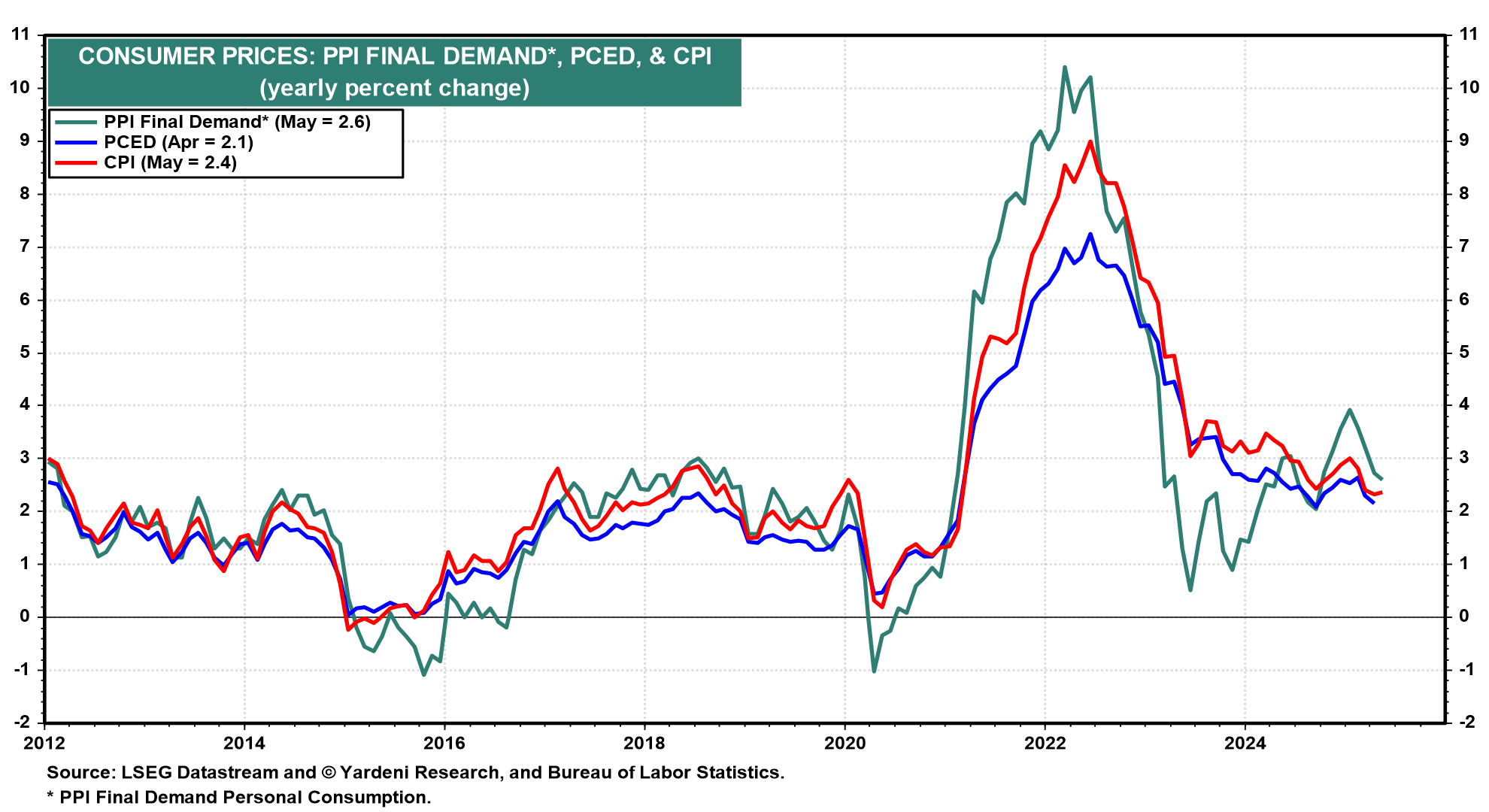

(1) Inflation. May's PCED inflation rate (Fri) might show a bit of acceleration. The Cleveland Fed's inflation Nowcasting tracking model is showing a 2.3% y/y increase for headline PCED up from 2.1% y/y in April (chart). If so, this inflation report will validate the Fed's reluctance to ease, especially since most Fed officials expect the fog of wars to put upward pressure on inflation, at least in the short run. June's Summary of Economic Projections (SEP), released by the FOMC last week, shows a median estimated 2025 PCED inflation rate of 3.0%, up from the March SEP median estimate of 2.7%.

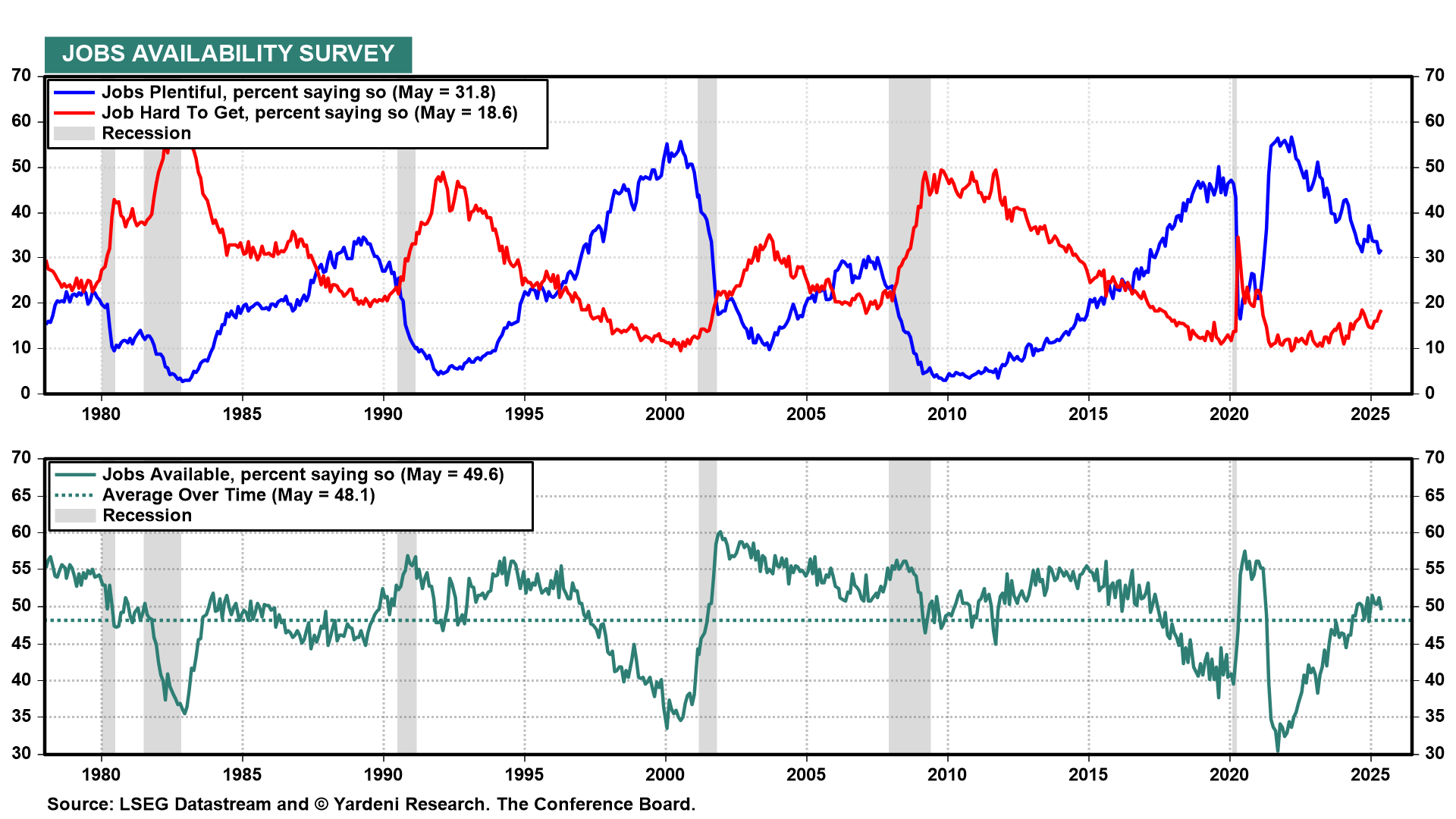

(2) Consumer confidence. We expect the labor market indicators in the Consumer Confidence Index (CCI) survey (Tue) to reflect solid underlying conditions. Recent readings on jobless claims confirm our view that the extreme economic uncertainty dominating news feeds matters less than perceptions about job security and future wage gains. As such, the CCI survey indicates how plentiful or hard to get jobs are in June and will be of great interest to Fed watchers (chart).

(3) Personal income. Following recent reported increases in payroll employment and average hourly earnings in May, personal income (Fri) probably rose solidly last month. It helps that hourly wages have been rising to record highs in real terms (chart). For low-wage workers, in fact, real average hourly earnings have been rising faster than their long-term uptrend for two years now.