Nothing upends the economic game board like a sudden war few had in their bingo cards a week ago. Granted, the coordinated US-Israel attack on Iran over the weekend wasn’t a complete surprise. But the scale of the bombardment that killed Supreme Leader Ayatollah Ali Khamenei was impressive. Tehran’s wave of retaliatory missile and drone attacks aimed at US bases and allies around the region, and threats to close the Strait of Hormuz, have economists scrambling to calculate the fallout.

As traders assess what all this means for energy and other commodity prices, this week features a couple of key data reports that could influence the timing of any future Federal Reserve rate cuts, namely, February employment (Fri) and January retail sales (Fri).

We’ll hear from Fed Governor Michelle Bowman (Thu) speaking on the economy and innovation. New York Fed President John Williams also speaks (Tues). Other voting Federal Open Market Committee members scheduled to make comments include Minneapolis Fed President Neel Kashkari (Tue) and Cleveland Fed President Beth Hammack (Fri).

This will be a busy week on the international front. China’s annual “Two Sessions” meeting begins (Wed) and will unveil its 2026 GDP target — likely abound 4.5%. We’ll get updates on Japanese unemployment (Tue) and Eurozone inflation (Tue). And, of course, global markets will be on the lookout for any news on the latest zigs and zags in the AI trade.

Here are the economic data releases most likely to affect Fed policymakers’ views on whether another rate cut is needed:

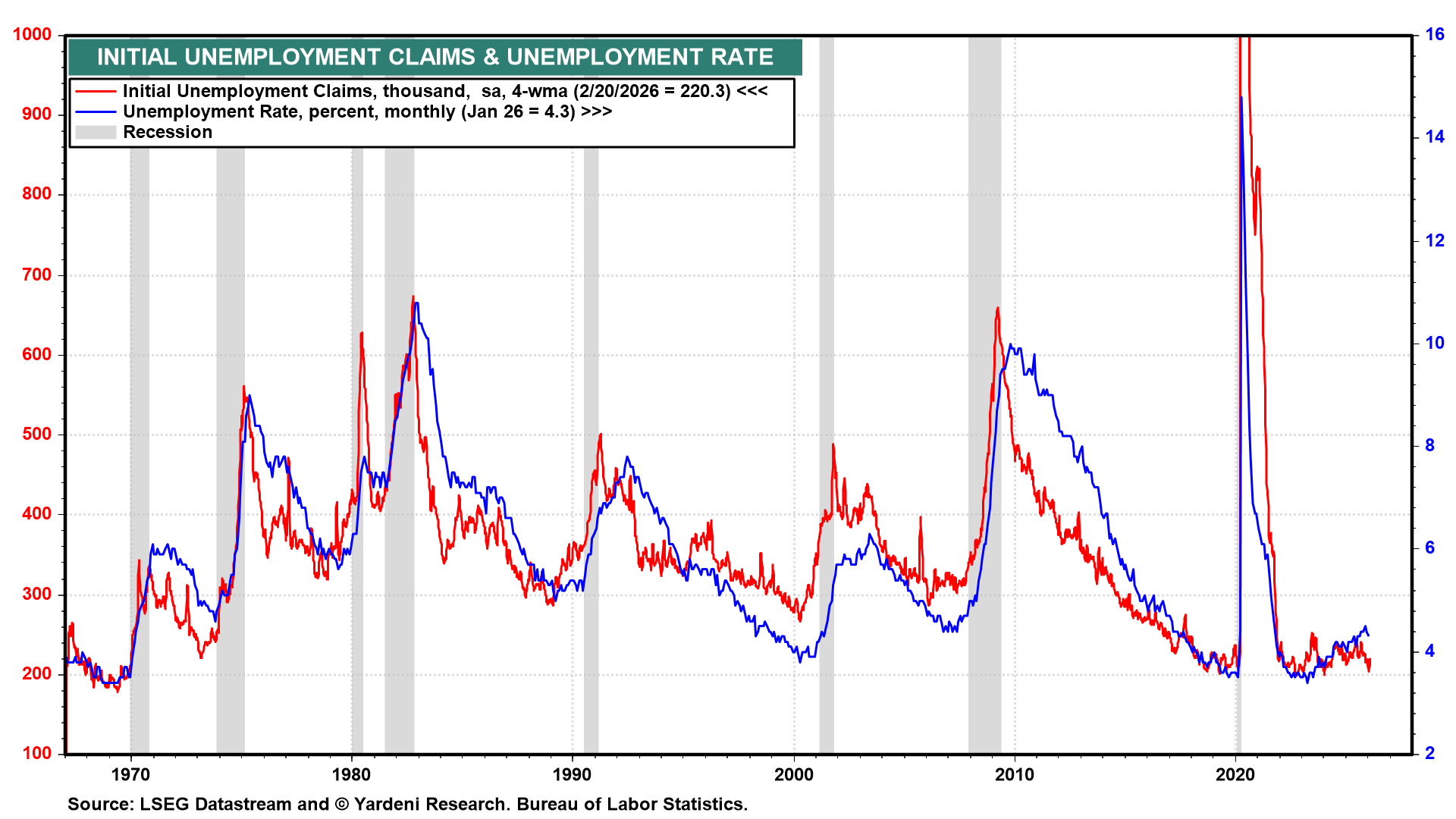

(1) Employment. We expect a 60,000 increase in February payrolls (Fri). The data takes on increasing significance since last month’s surprisingly robust increase of 130,000 and 4.3% jobless rate. Another healthy jobs report could close the door on Fed rate cuts for the foreseeable future. We’ll also get February employment data from ADP (Wed) and Challenger (Thu), as well as initial jobless claims (Thu), which suggests that the jobless rate probably fell again last month (chart).

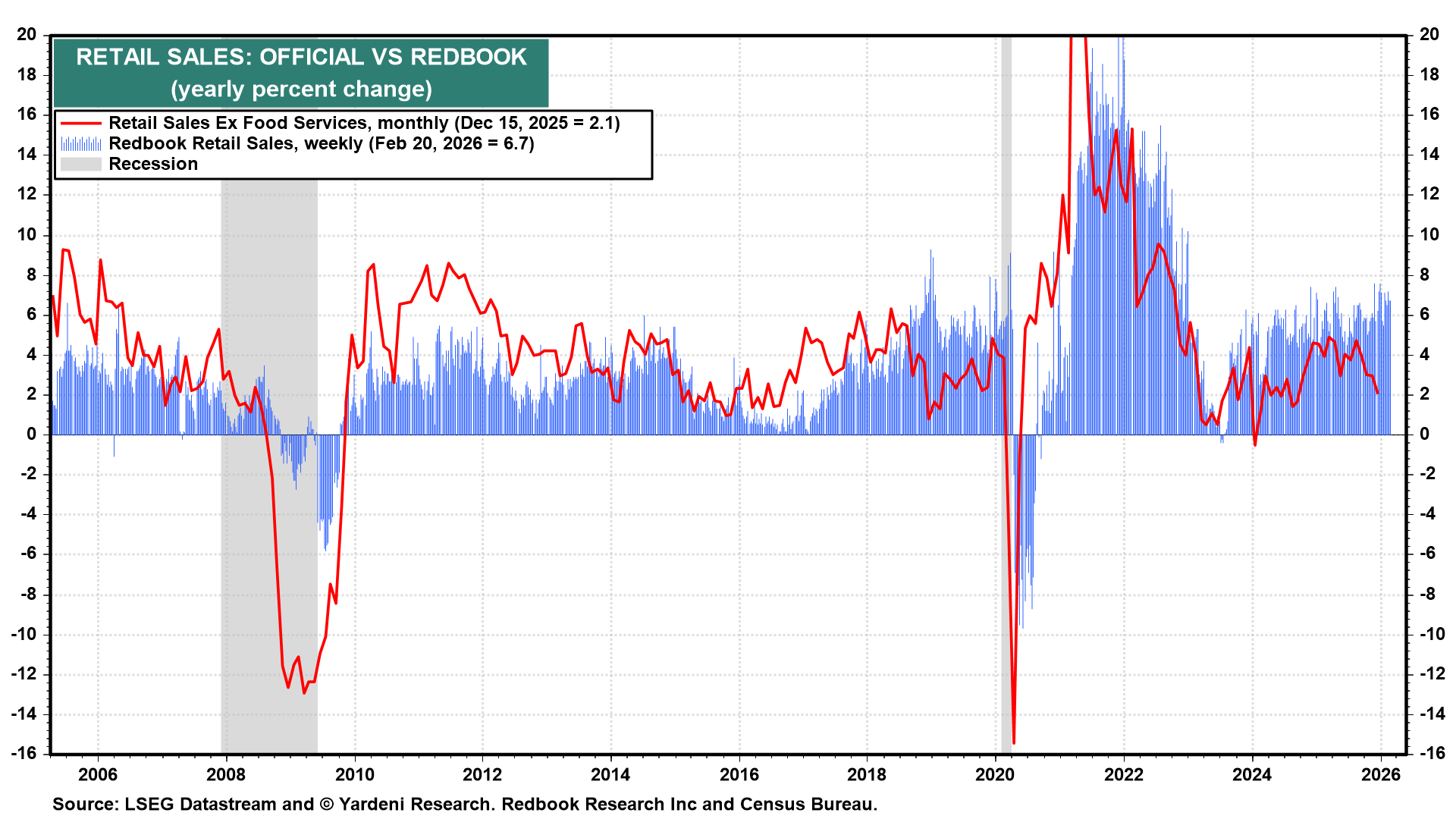

(2) Retail sales. The January retail sales report (Fri) will be an important reality check following a flat December reading. Most forecasts center on a roughly 0.2% m/m drop last month. Still, with employment holding its ground and the stock market near record highs, spending patterns should hold up as well, as confirmed by the weekly Redbook Retail Sales index (chart).

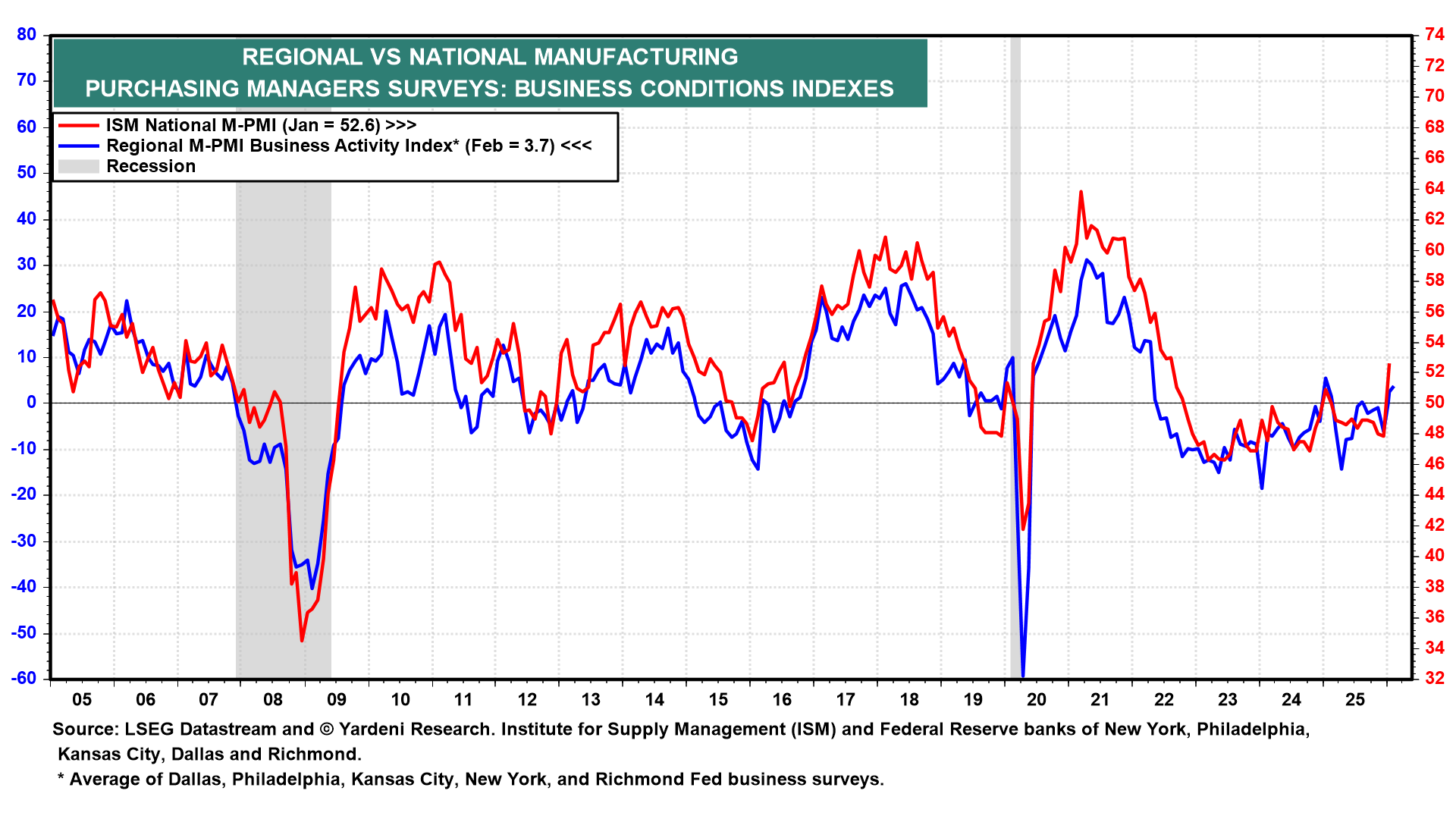

(3) PMIs. The Institute of Supply Management reports its February manufacturing purchasing managers' index (Mon), which expanded in January to 52.6. The non-manufacturing PMI (Wed) follows. It, too, came in well above 50.0 the previous month, at 53.8. The regional business surveys suggest that M-PMI remained above 50.0 last month (chart).