This promises to be a nerve-racking week of developments in the Middle East. In the nine days since the US and Israel launched attacks on Iran, the conflict has embroiled various neighboring countries. Tehran’s moves to effectively shut the Strait of Hormuz are causing sharp spikes in oil and gas prices – and sending economic forecasters back to the drawing board.

This evening, Brent crude topped $100 a barrel. As such, this week’s reports from OPEC and the International Energy Agency (IEA) on shocks to seaborne energy from the Persian Gulf could be major market movers. Especially after the United Arab Emirates and Kuwait reduced oil production because they've run out of storage.

Naturally, all eyes are on any signs of escalation and their potential impact on inflation expectations. Already, investors are scaling back expectations for interest-rate cuts this year. This includes the Federal Reserve, heading toward its March 17-18 policy meeting. Many Federal Open Market Committee members are unhappy with the gradual pace of returning inflation to its 2% comfort zone. Indeed, the minutes of the January FOMC revealed that "several" participants felt rate hikes could even be appropriate.

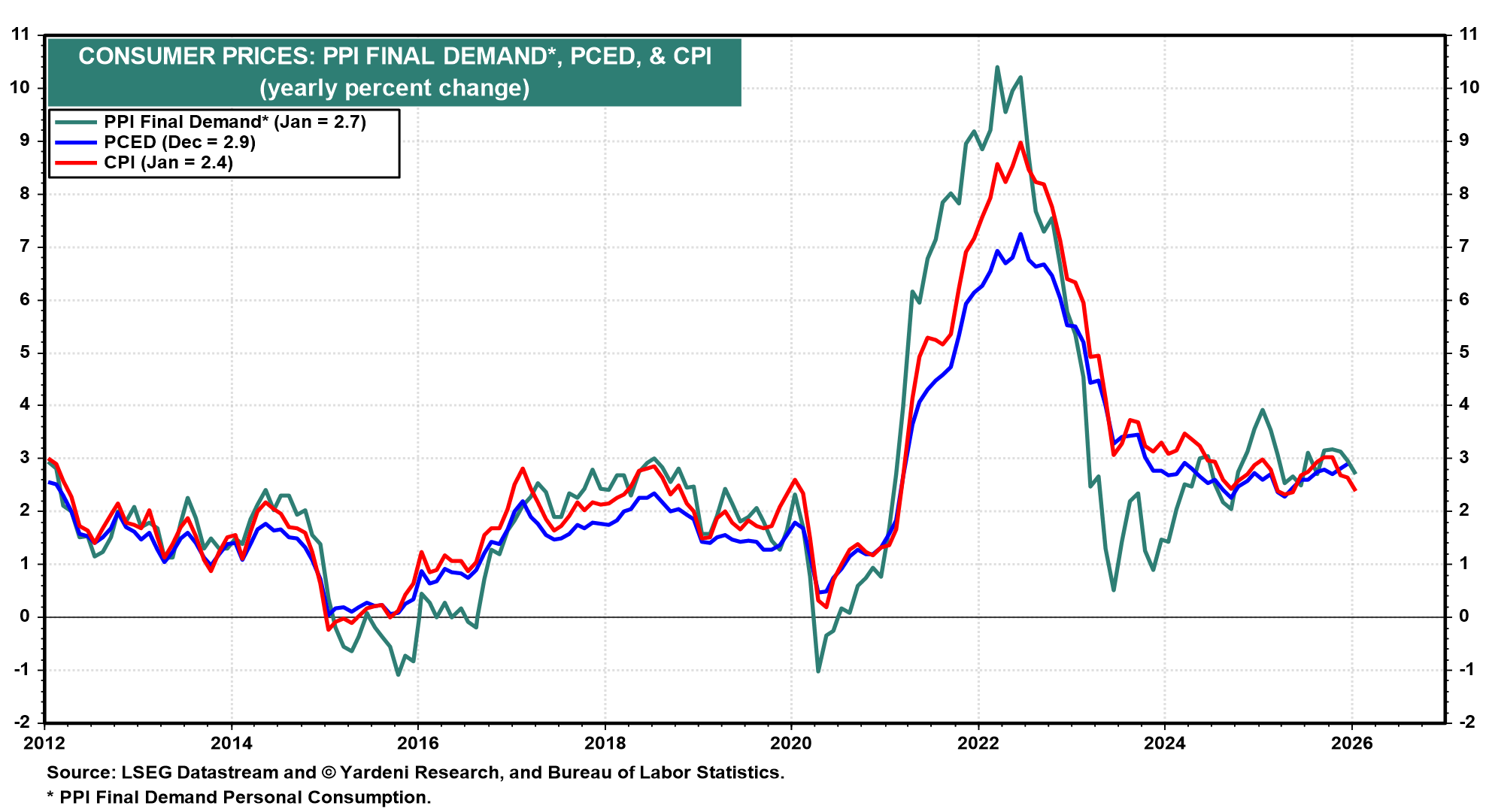

Hence, this week’s reports on consumer prices (Wed) in February and PCE inflation (Fri) in January could pack more punch than usual for bond markets already on edge. The PCE data – the Fed’s preferred price trend barometer — could be particularly market-moving. It’s remained stuck near 3%.

The days ahead will bring updates on global inflation dynamics from China, India, Brazil, and Mexico. We’ll also get reality checks on the effects of President Donald Trump’s tariffs from the Eurozone (industrial production), Japan (GDP), Canada (trade and employment), and the UK (monthly GDP).

Here are the US data releases most likely to influence the financial markets this week, though they are likely to be overshadowed by developments in the Middle East:

(1) PCE inflation. Following a 2.9% y/y reading in December, the Cleveland Fed’s Inflation Nowcasting model projects the headline PCE to ease to 2.8% y/y in January (chart). That might comfort the Fed doves. But given fast-changing inflation dynamics, most officials might look past any good news in the short run.

(2) CPI. After dipping to 2.4% y/y in January — and a 2.5% core rate — many expect consumer prices to hold largely steady in February (Wed). That includes the Cleveland Fed’s model, which forecasts a roughly 0.2% m/m increase for both headline and core CPI. Of course, this, too, could be the calm before the inflationary storm to come.

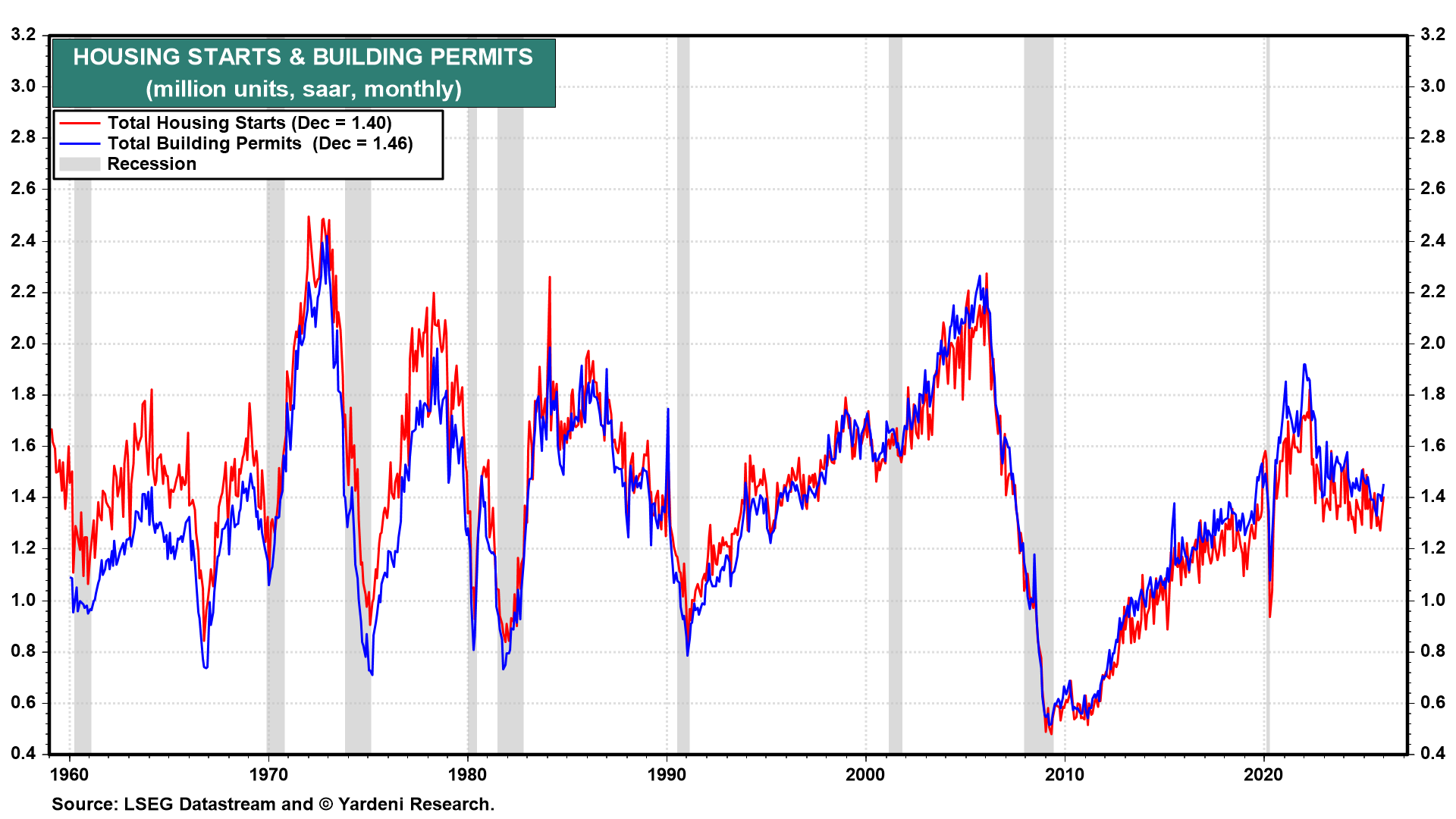

(3) Housing data. This week’s flurry of housing data and surveys could offer important insights into US confidence as both bond yields and the economic outlook gyrate. We’ll get news on February existing home sales and housing affordability (Tue) and January housing starts (Thu) (chart).

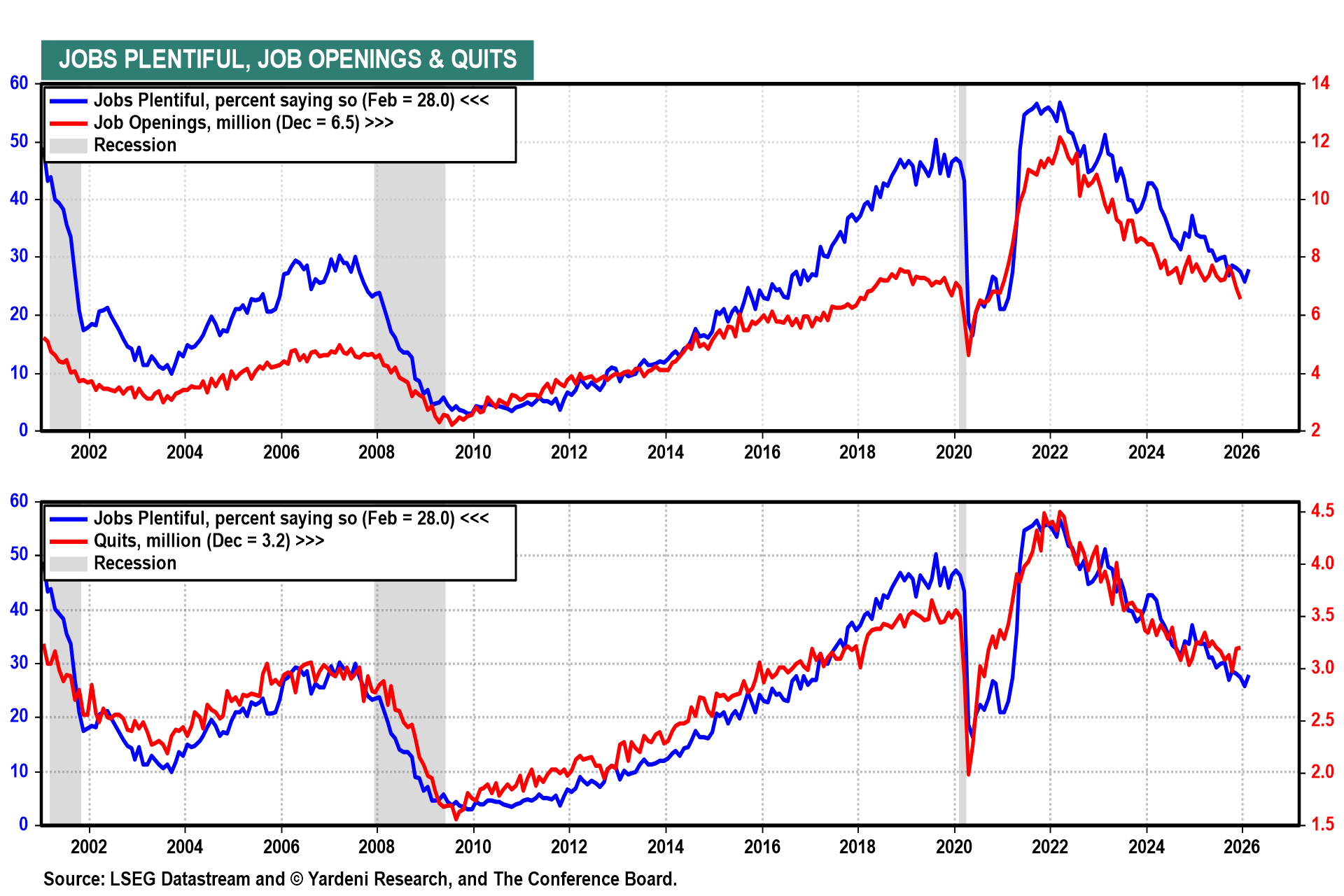

(4) JOLTS and claims. News that US job openings dropped to the lowest level in more than five years in December fits with more recent signs of slowing labor markets. Markets will pay close attention to January JOLTS data (Fri) for any hints of further deterioration (chart). Meanwhile, trends in initial weekly jobless claims (Thu) — coming in at 213,000 in the previous week — continue to indicate a stable labor market with low layoffs.