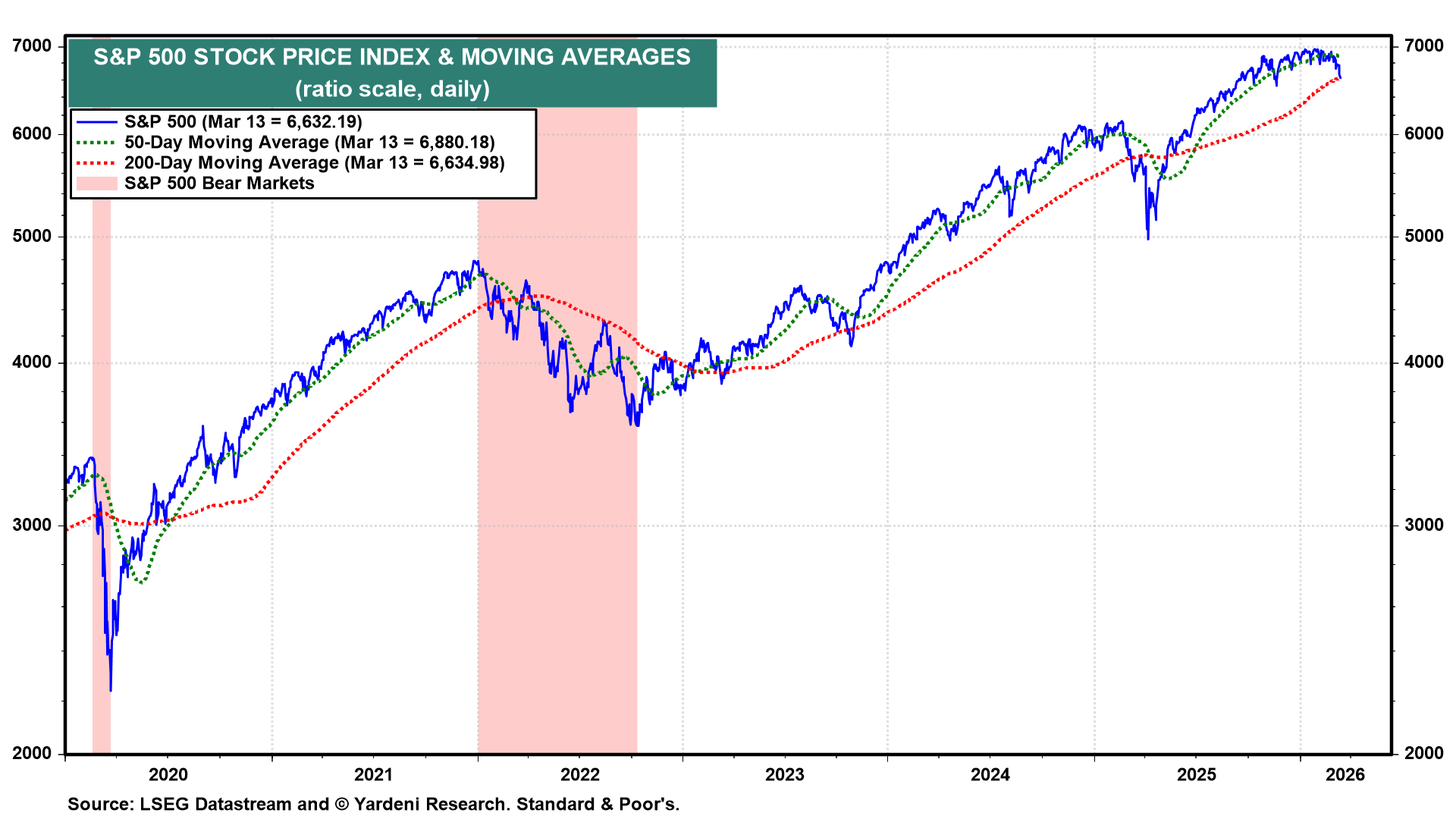

Why has the stock market held up so well since the start of the war? The S&P 500 is down only 4.96% from its record high on January 27 and 3.59% since the start of the war on February 28 (chart). It fell to its 200-day moving average on Friday and held it. The obvious explanation is that the market is discounting a short war. That was our initial assessment, but three days after the war began, we concluded it might last longer, leading to a 10%-15% correction, and warned that we could not rule out a bear market.

That's what happened in 2022 after Russia invaded Ukraine, sending oil, gas, and grain prices soaring. Back then, we bet on the economy's resilience and called the October bottom of the S&P 500 in early November. That all worked out well. The bear market was attributable to widespread fears of a recession, which we did not share.

Despite soaring oil prices and the closing of the Strait of Hormuz, recession fears seem more muted now than they were in 2022. We raised our odds of a recession from 20% to 35% a few days after the war started, when we concluded it might be longer than widely expected. More recently, we've become concerned that a weakening US economy might exacerbate the cracks in the US private credit market.

The apparent resilience in the S&P 500 is attributable to the increasing bullishness of industry analysts' consensus estimates for earnings per share in 2026 and 2027 (chart). Apparently, they did not get the memo about the possible negative consequences of a protracted war and closure of the Strait. So S&P 500 companies’ aggregate forward earnings rose to a record high last week of $328.80 per share. At Friday's close, that implied a forward P/E of 20.2, which is down from 22.0 on January 27. The 1.8% increase in forward earnings per share offset some of the 6.8% decline in the valuation multiple, resulting in the 5.0% decline in the S&P 500.