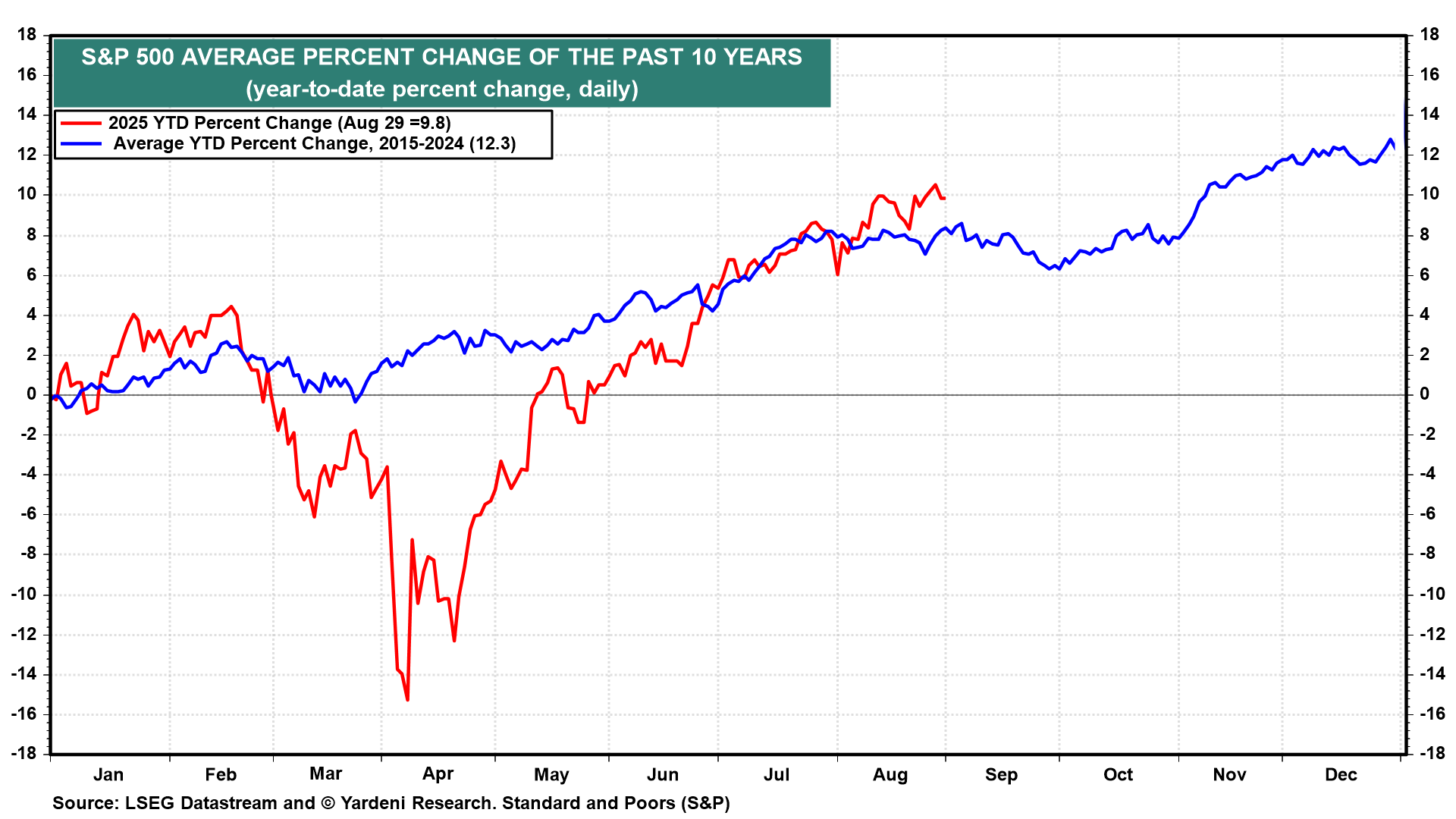

September has a long history of being a tough month for the stock market. This has been particularly true over the past decade, based on the average year-to-date percentage change in the S&P 500 during Septembers (chart). But when September was weak in the past, it often provided buying opportunities for year-end rallies.

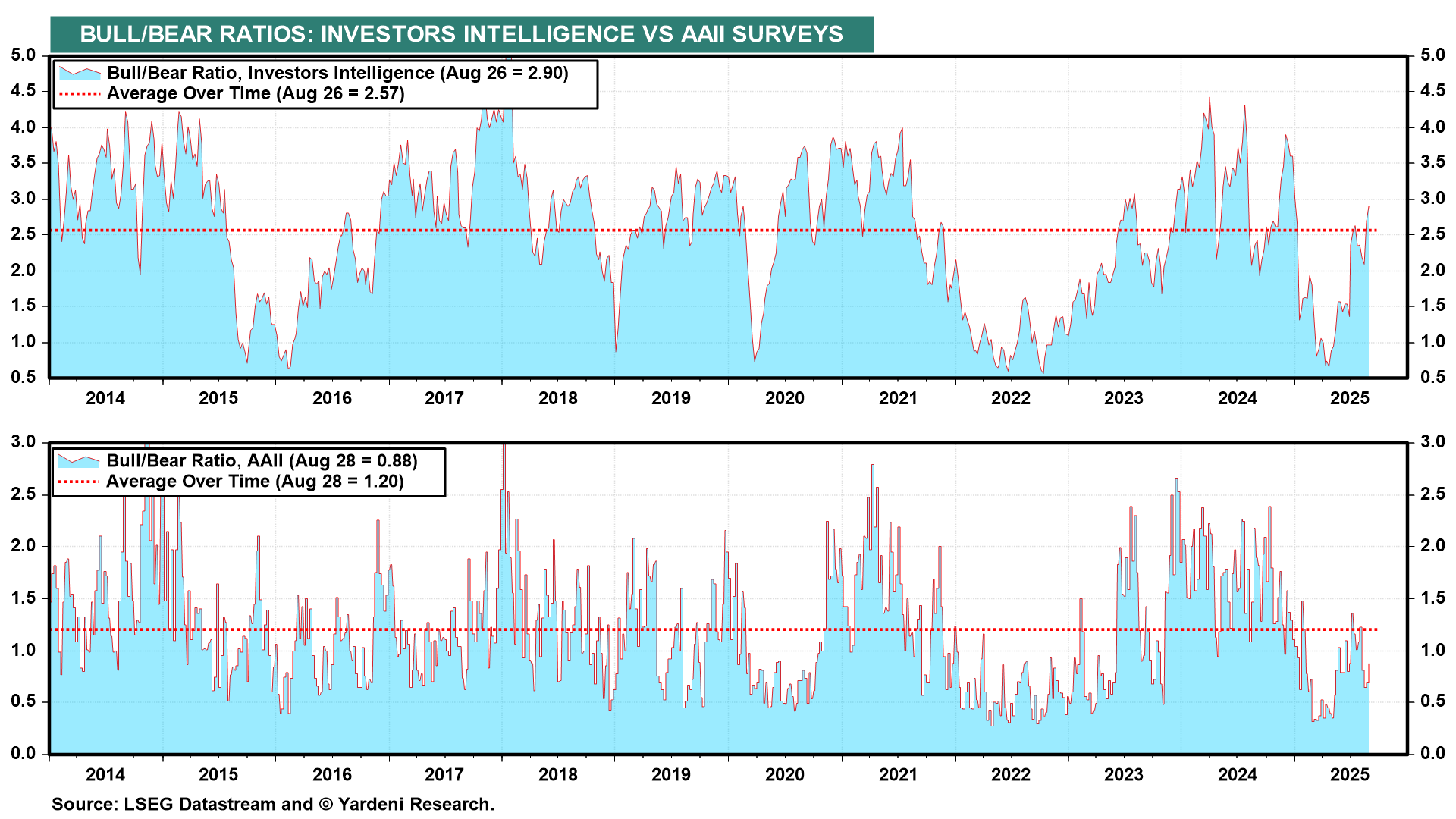

So, might the latest top in the S&P 500 have been hit on Thursday, August 28, at 6501.86? Probably. Notably, Nvidia reported great earnings on Wednesday, yet the market's AI bellwether stock sold off on Thursday and Friday. Then again, profit-taking before a long holiday weekend isn't unusual. Furthermore, the bull-bear ratios remain relatively subdued, suggesting that any pullback in September is unlikely to be a correction or the start of a bear market (chart).

However, the uncertain future of the Fed's monetary policy (and even the Fed itself!) and now Trump's tariffs are likely to weigh on the stock market over the next few weeks. Overseas, France appears to be on the verge of a debt crisis that could topple the government, while Germany's manufacturing sector may be falling into a recession. Japan's bond yields are soaring. Here is more:

(1) The Fed & the economy. The CME FedWatch Tool indicated that the latest probability of a 25-basis-point Fed rate cut at the September 17 meeting of the FOMC is 86.4%. Our subjective odds are 40%. Friday's data supported our none-and-done-in-2025 stance based on our view that the economy doesn't need a rate cut, especially with inflation closer to 3.0% y/y than the Fed’s 2.0% target.

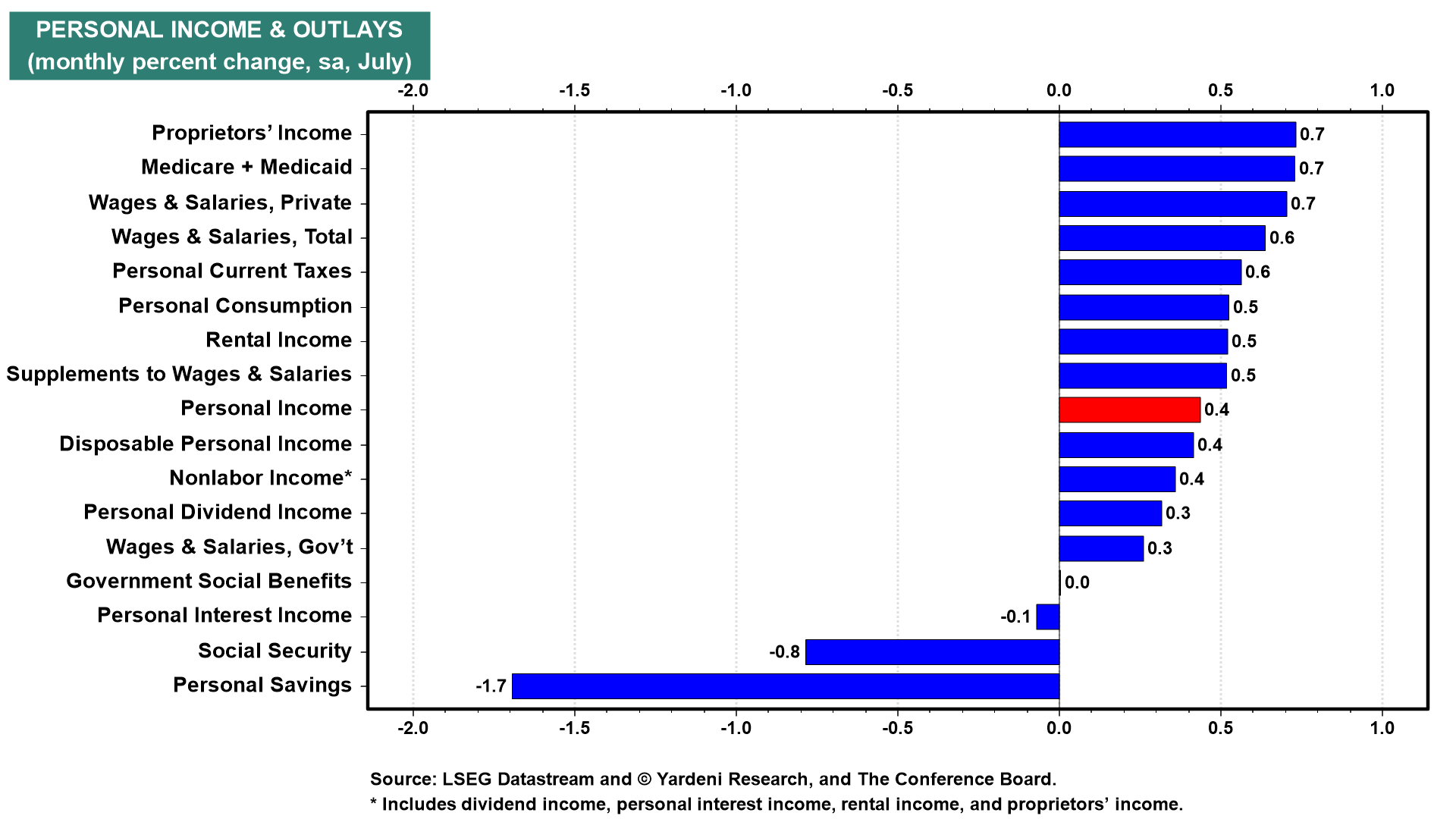

Friday's personal income report showed a robust gain in consumer spending (0.5%) and a solid increase in personal income (0.4%), led by a substantial gain in private wages and salaries (0.7%) (chart).

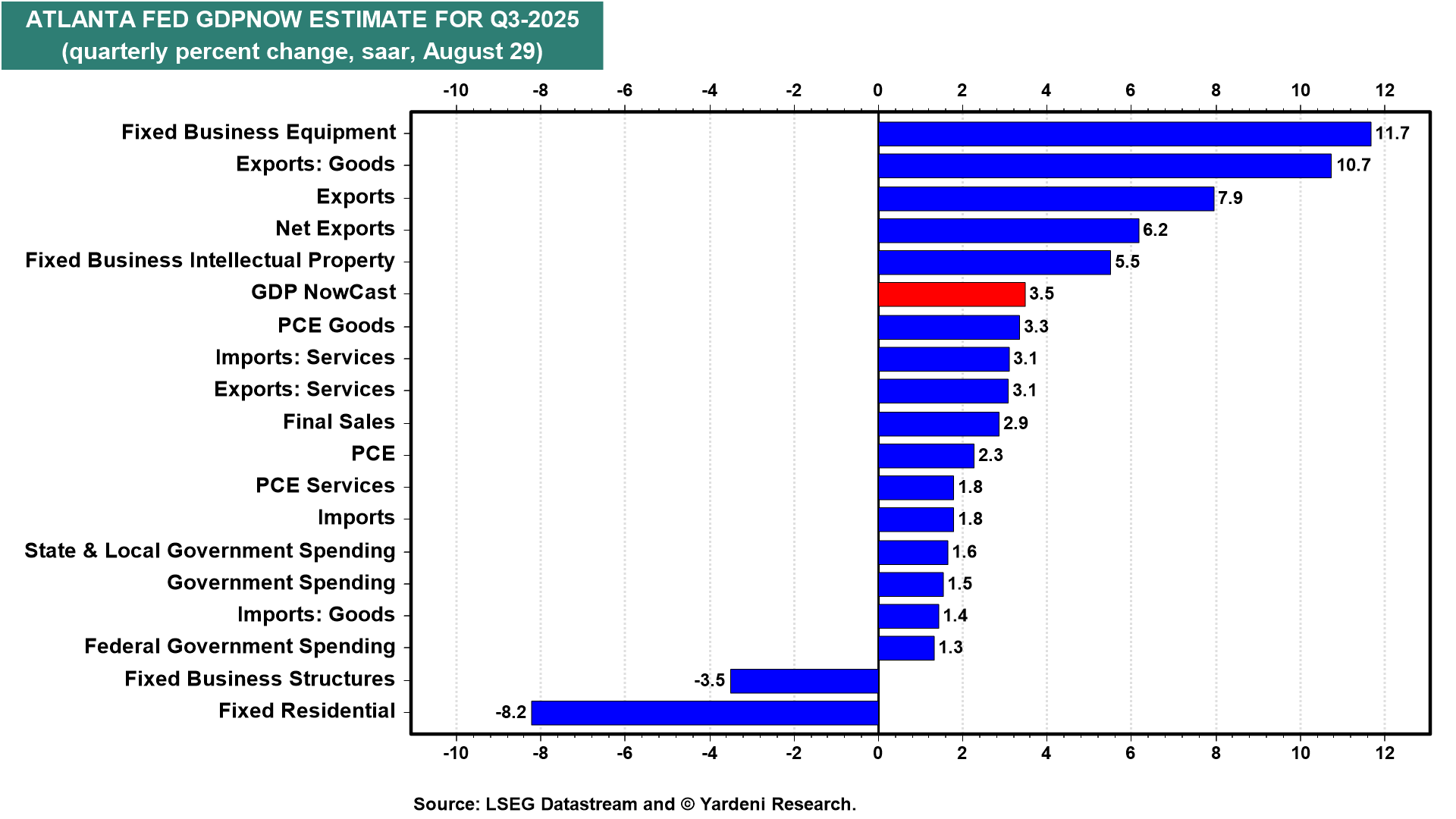

Also on Friday, the Atlanta Fed's GDPNow model tracked Q3's real GDP growth rate at 3.5%, up from 2.2% (chart)! It rose 3.3% during Q2.

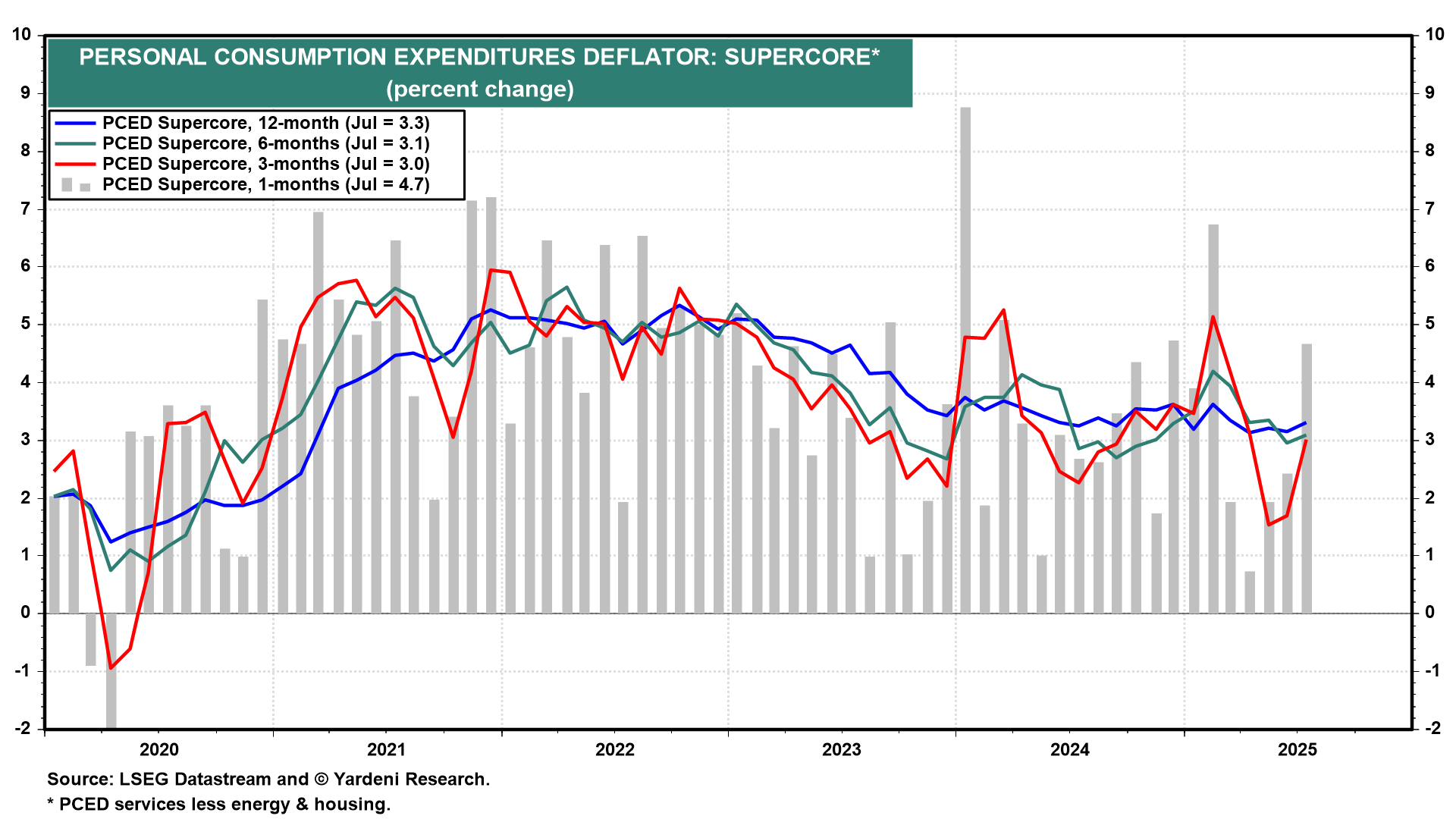

(2) The Fed & inflation. July's headline and core PCED inflation rates showed gains of 2.6% and 2.9% y/y in Friday's personal income report. The monthly increases in the core inflation rate have been rising for the past four months, led by the "supercore" inflation rate for PCED services less energy and housing (chart).

(3) The Fed's independence. Also unsettling the financial markets will be the ongoing attack on the Fed by the Trump administration. The September 17 meeting of the FOMC is likely to confirm that the attacks are cracking the foundation of the Fed. If the majority votes to cut the federal funds rate or to hold off on doing so, there will be at least two dissenters either way, if not more. If the Fed cuts the rate even though the data don't warrant such easing, the Bond Vigilantes are likely to protest.

(4) Trump's tariffs. As we anticipated, a US appeals court ruled on Friday that most of President Donald Trump's tariffs are illegal. The court allowed the tariffs to remain in place through October 14, giving the Trump administration a chance to file an appeal with the US Supreme Court. "If these Tariffs ever went away, it would be a total disaster for the Country," Trump wrote in a Truth Social post. "If allowed to stand, this Decision would literally destroy the United States of America." The Bond Vigilantes might start acting up again if they can no longer look forward to a significant reduction in the federal deficit attributable to tariff revenues.

(5) European turmoil. France appears to be on the edge of a political and debt crisis. French markets tumbled after Prime Minister Bayrou unexpectedly called for a confidence vote on September 8 to approve his debt-cutting plan. His proposal was roundly rejected by opposition parties, who said they would relish the opportunity to cut short his minority government's time in office.

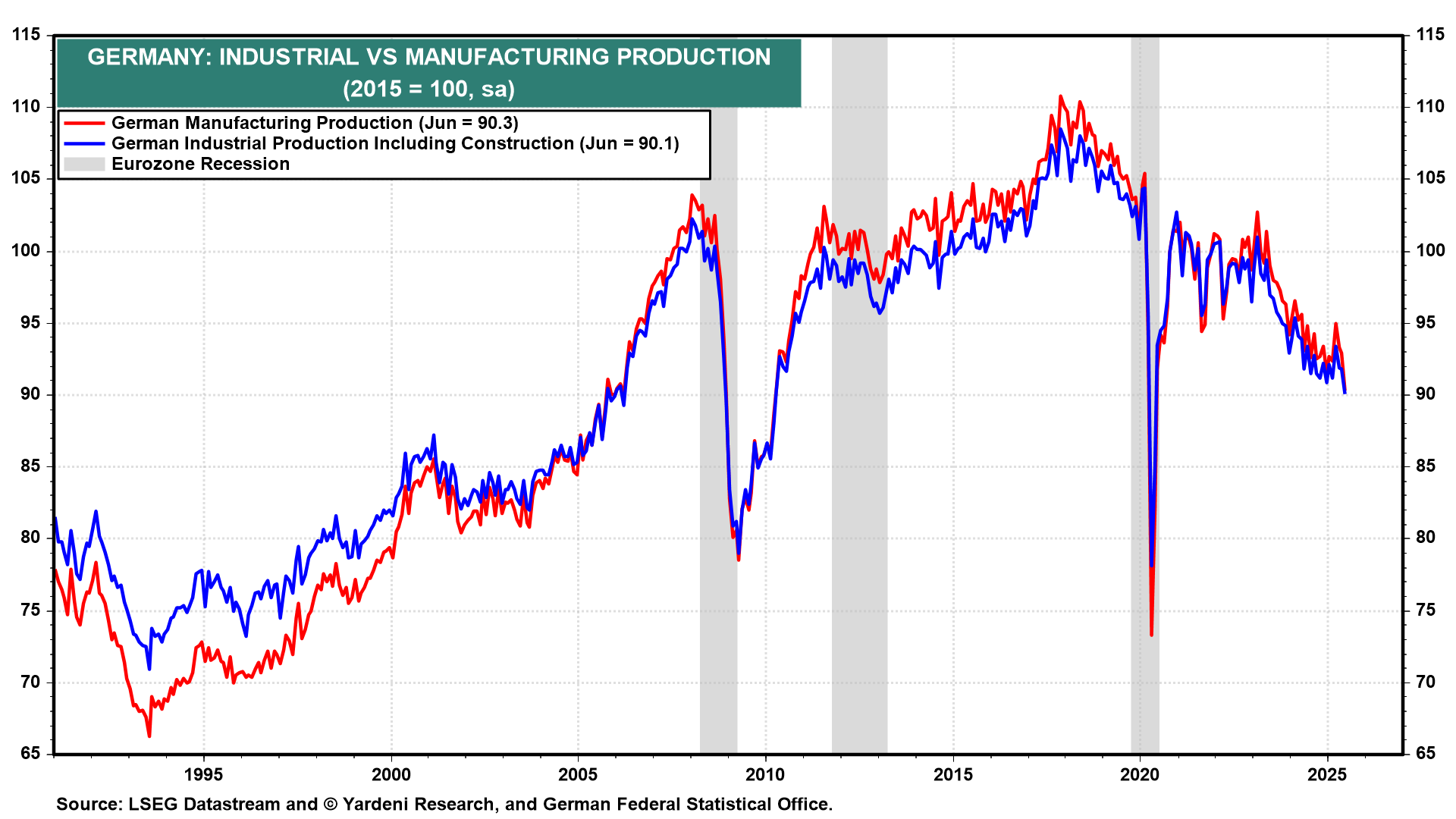

Germany's industrial output fell in June to its lowest level since the pandemic in 2020, extending last year's declines amid weakening foreign demand and increasing competition from China (chart).

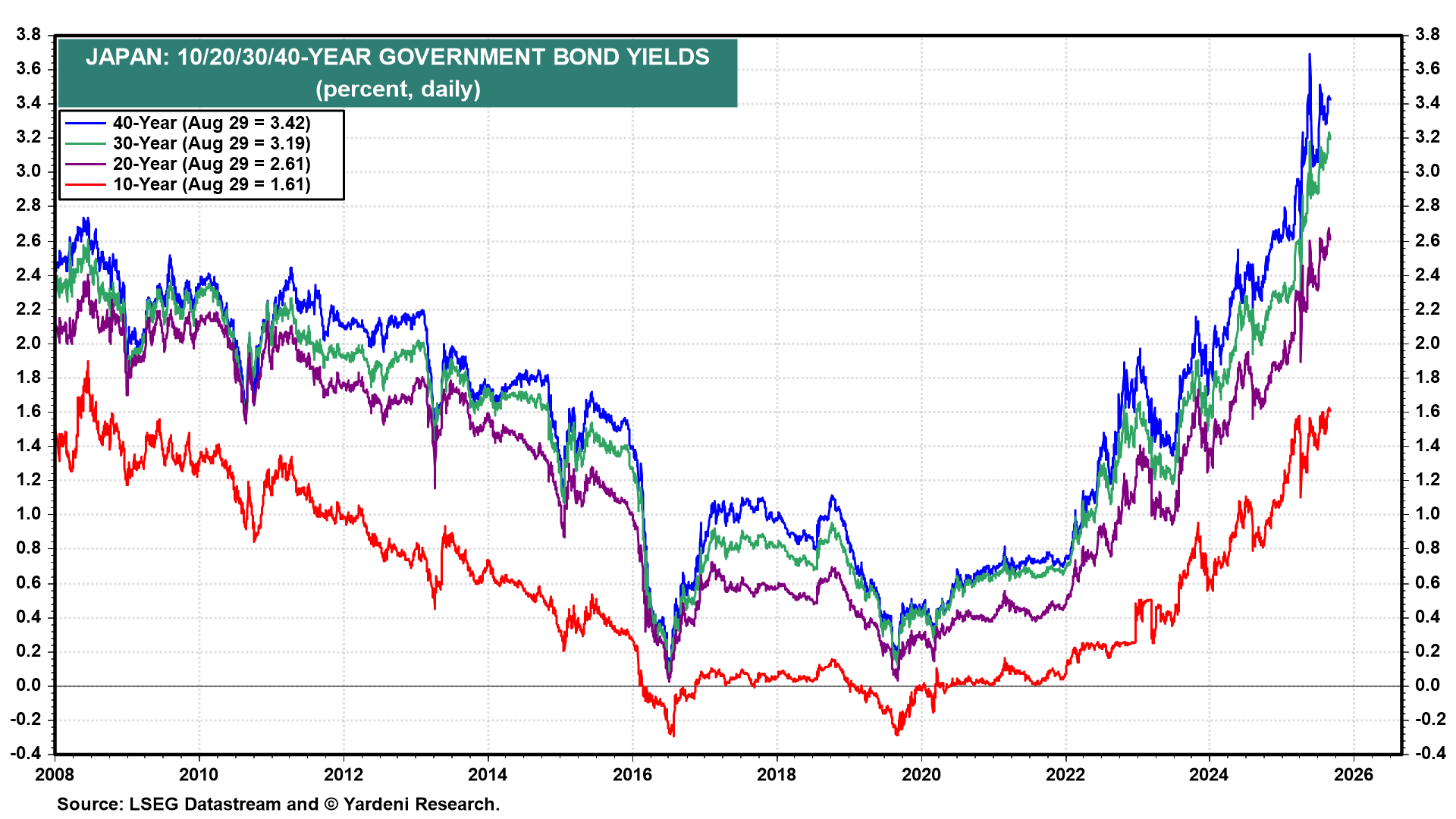

(6) Japan's debt crisis. The Bond Vigilantes have been pushing bond yields up rapidly in Japan (chart). Inflation is rising. The prospect of fresh fiscal stimulus following the ruling coalition's defeat in July's upper house election is raising concerns about increased debt issuance.

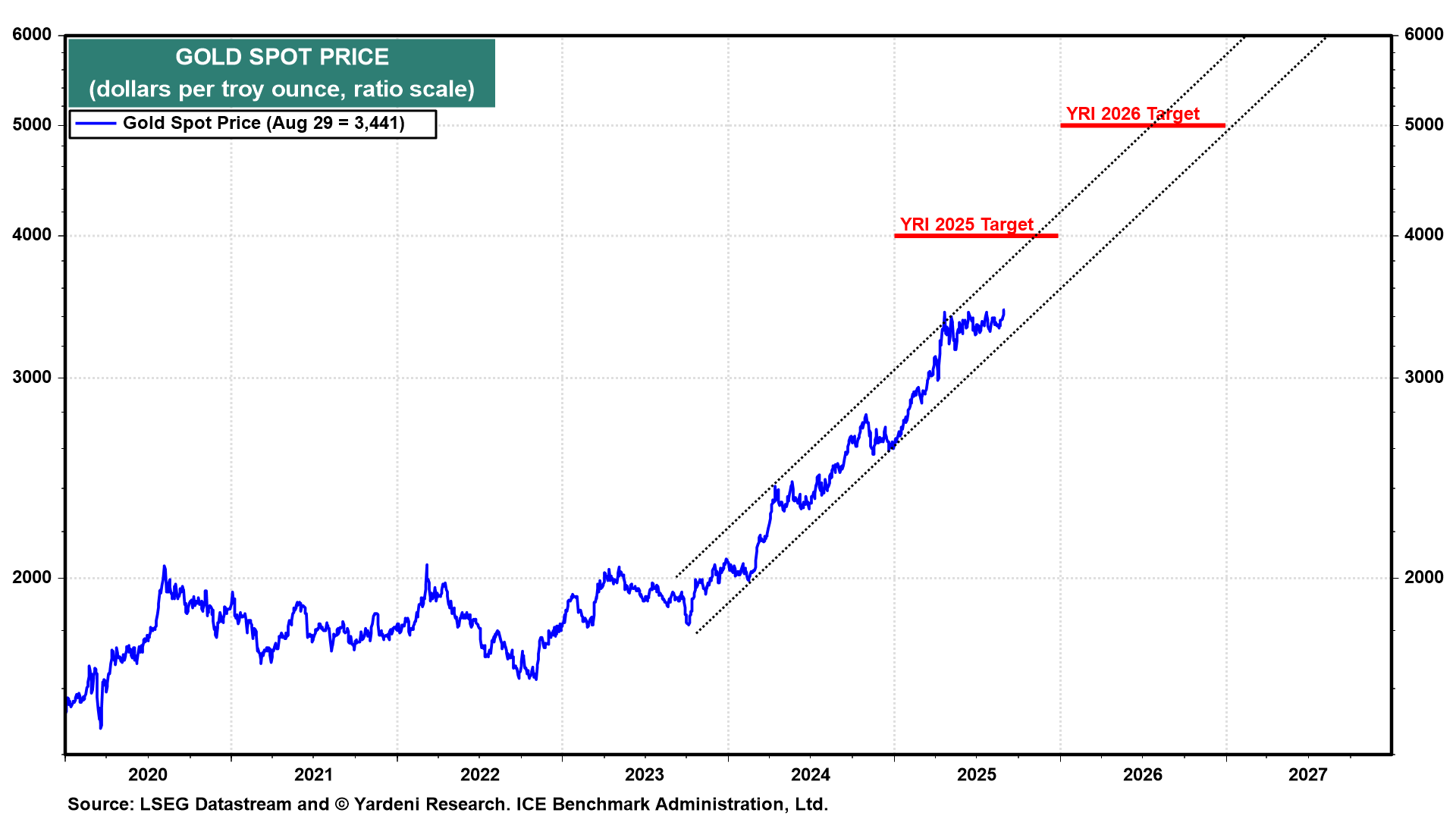

(7) Gold. No wonder that the price of gold seems set to climb to new record highs, perhaps reaching our year-end target of $4,000 an ounce (chart).