Our initial reaction to the latest war in the Middle East was that it isn't likely to last long. However, wars are hard to predict. The fog of war can be very disorienting. The US and Israel killed the top leaders of Iran's regime during the first day of their attacks on the country. So we thought that might set the stage for a short war. However, the regime's Islamic Revolutionary Guard Corps (IRGC) is still fighting to protect the Islamic Republic from both external threats and internal ones (including the regular army and a popular revolution). It is a branch of Iran's armed forces established shortly after the 1979 Islamic Revolution. It is one of the most powerful and influential institutions in Iran.

The United States designated the IRGC as a Foreign Terrorist Organization (FTO) in April 2019 — the first time the US had made such a designation against a government entity. These terrorists are likely to be hard to eradicate with just air power. Their threats to attack ships sailing through the Strait of Hormuz have effectively closed the sea lane through which vital oil and gas supplies are shipped around the world.

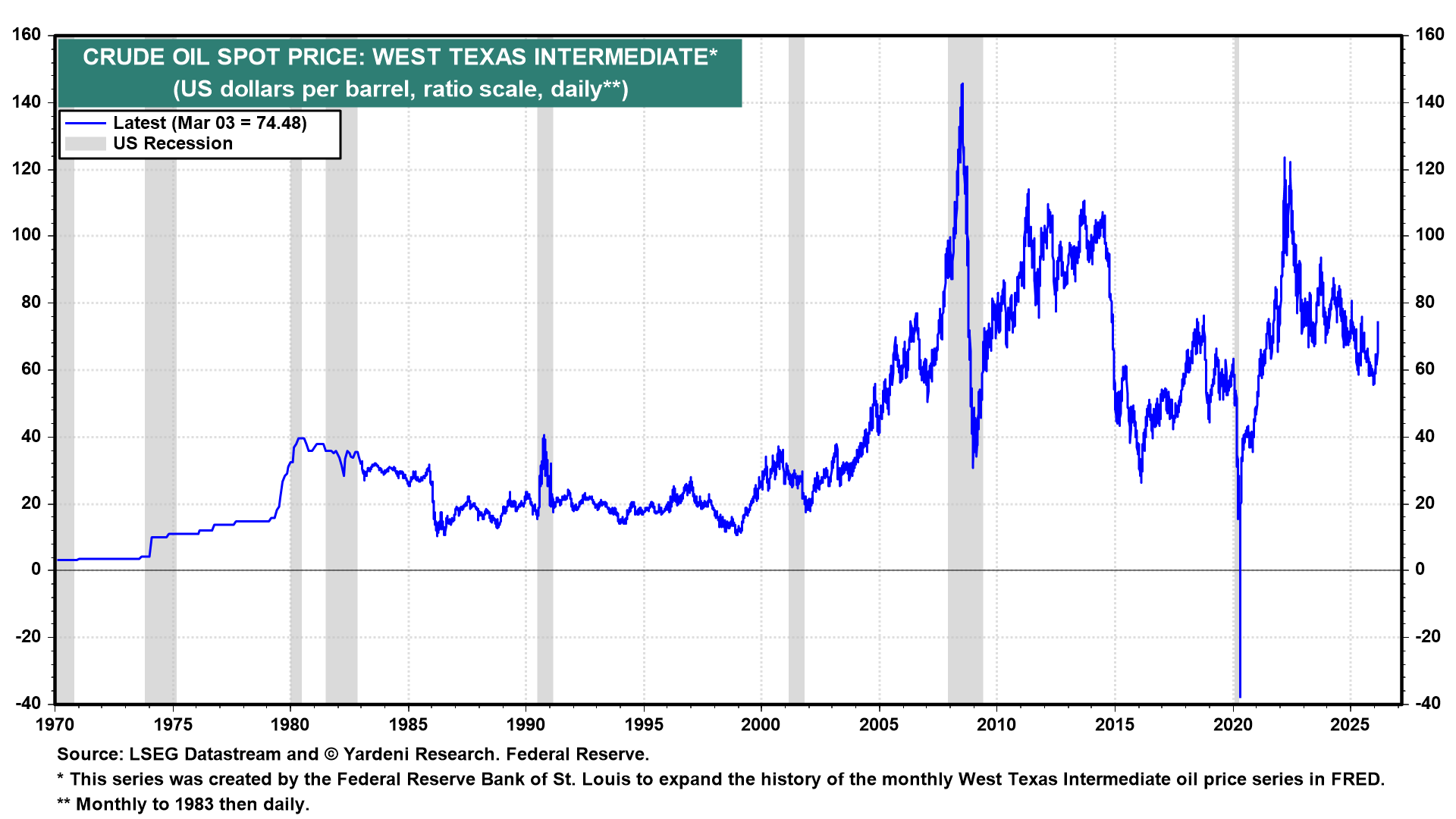

President Donald Trump today responded to soaring oil prices by ordering the United States Development Finance Corporation to provide maritime risk insurance and said that the US Navy will begin escorting tankers through the Strait "if necessary." Brent crude oil, which traded above $85 a barrel this morning, fell to $79 and closed above $81 (chart).

Rapidly rising oil prices have a history of causing recessions and bear markets in stocks (chart). That was not the case in 2022, when oil prices spiked, and the economy continued to grow, yet there was a bear market. The longer the war lasts, the more likely it is that the oil price shock results in stagflation. The Fed would be frozen as the risks of higher inflation and higher unemployment both increase.

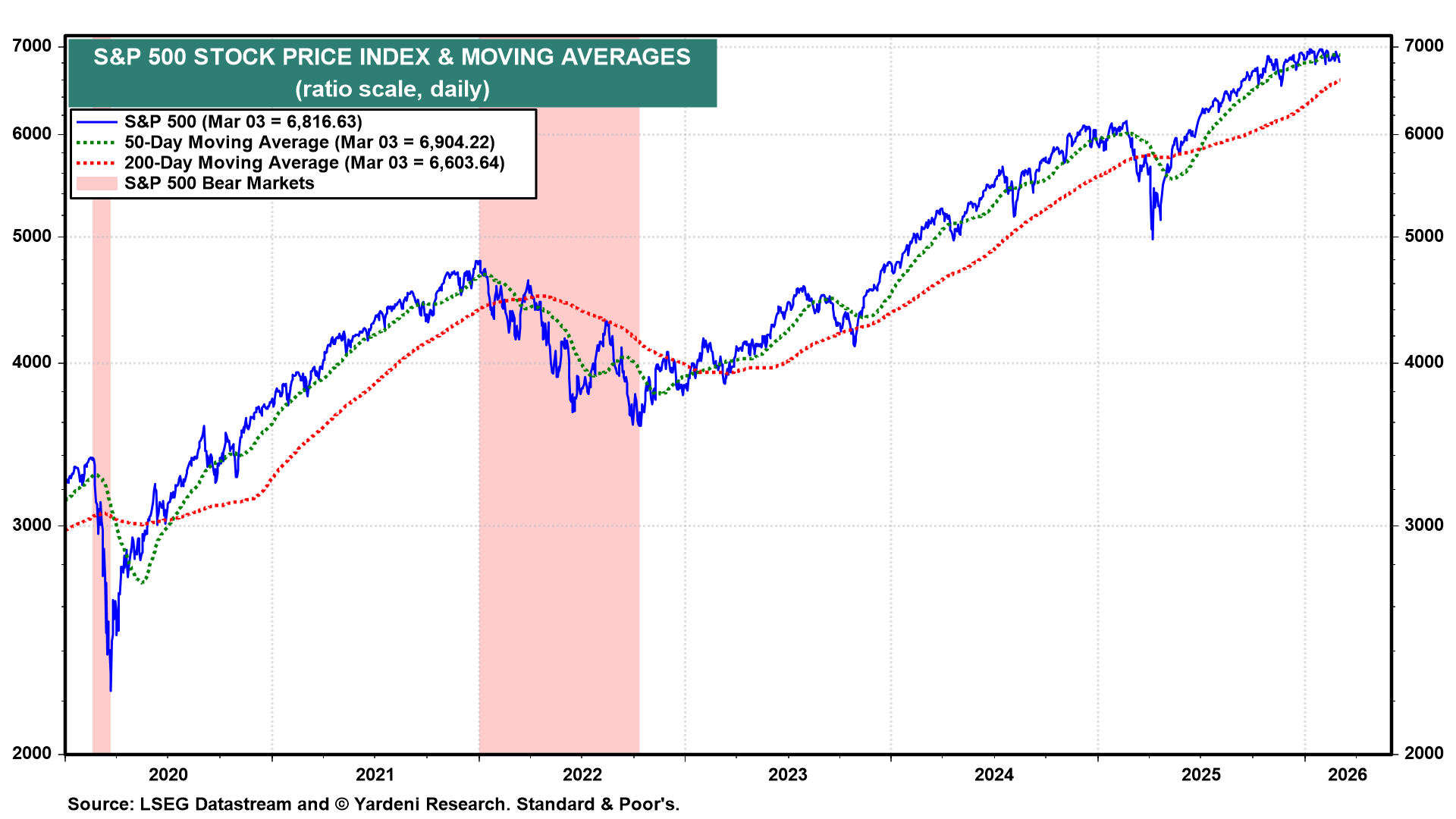

The S&P 500 fell sharply this morning and then rebounded, but still closed down by almost 1.0% and slightly below its 50-day moving average (chart). It is only 2.3% below its record high on January 27. We've been expecting a pullback due to excessive bullish sentiment, but now we expect a 10% correction from the high. It's hard to imagine that the IRGC won't use drones and speed boats to maintain their effective blockade of the Strait. If they are successful in doing so, the correction could be closer to 15%.

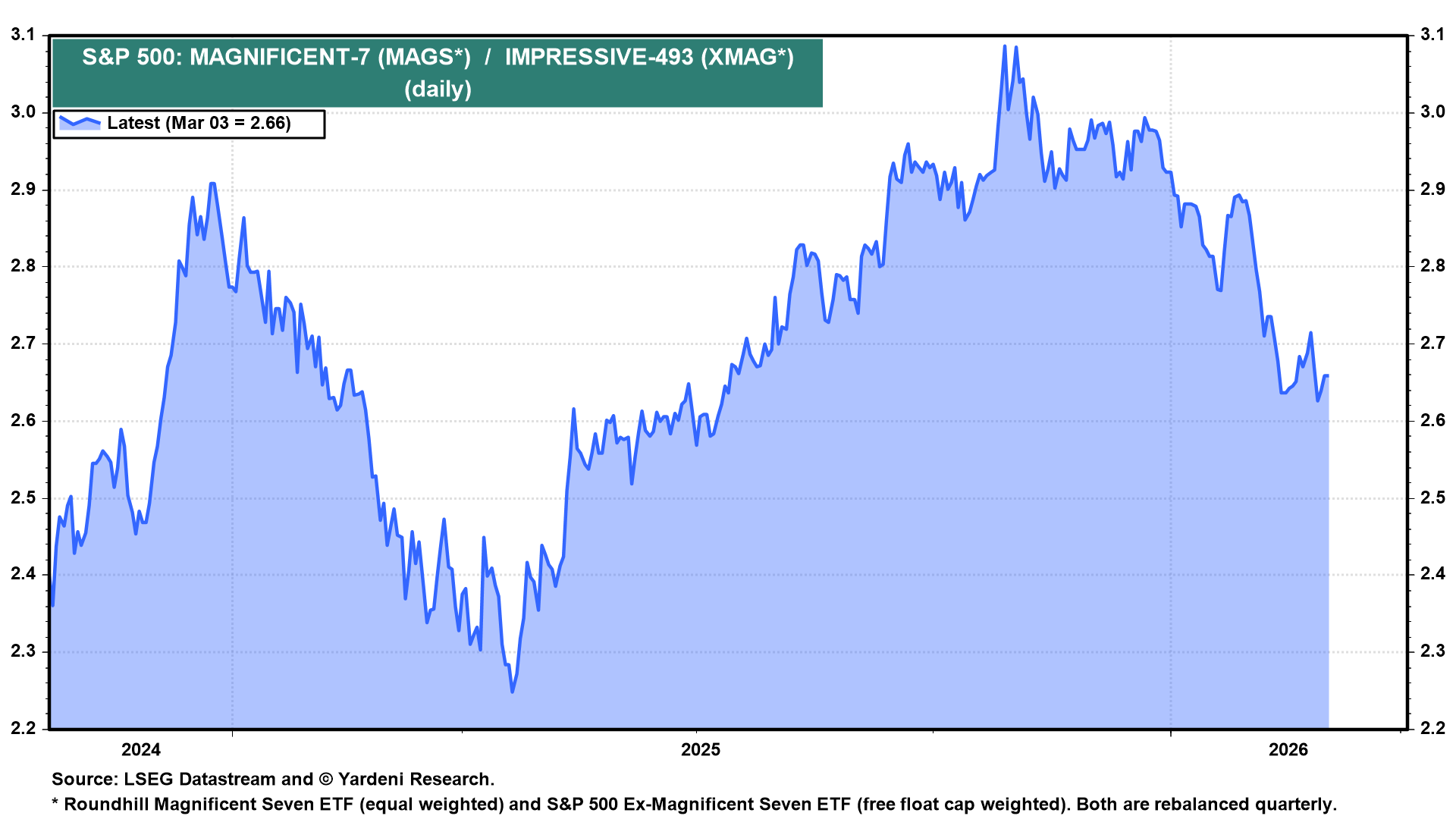

There may also be a short-term reversal in the domestic and global rebalancing trade that we predicted on December 7. It was working, but it is already being upended by the war. If recession fears start spreading, the Magnificent-7 could outperform the rest of the S&P 500, as they did today (chart).

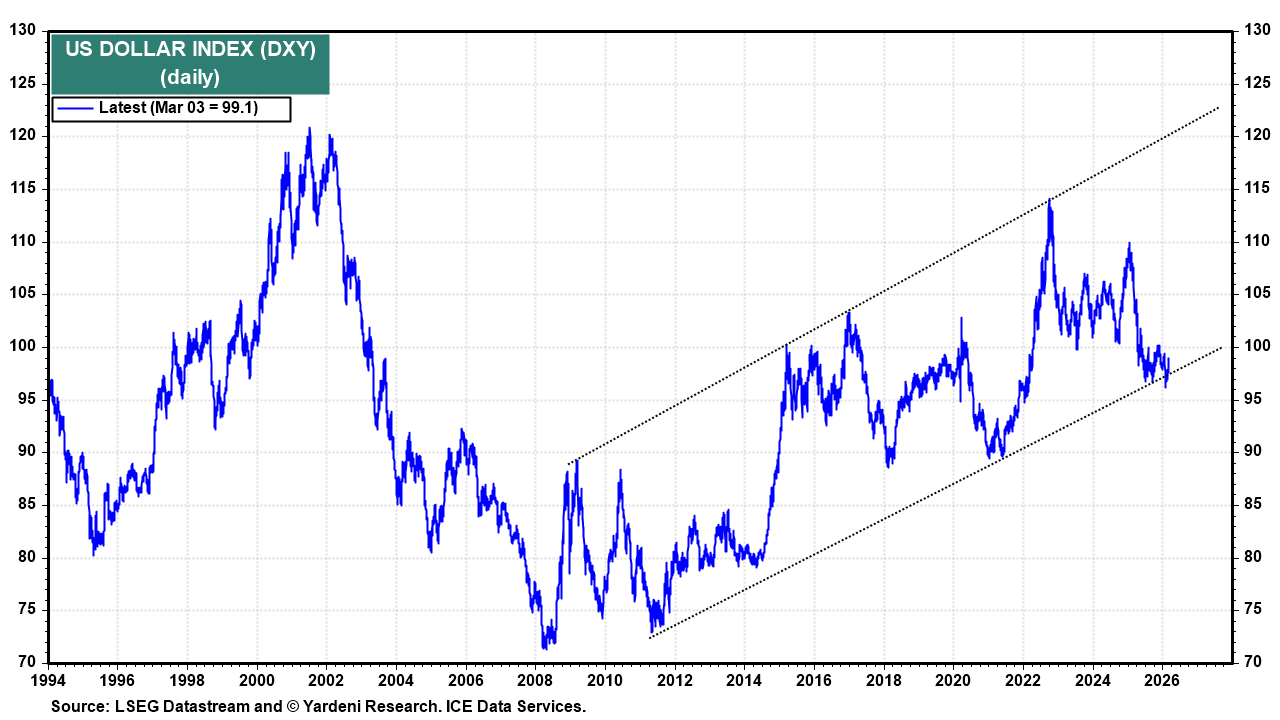

Also, our Go Global rebalancing act might be upended for a while until a credible ceasefire is reached. Overseas stock markets have been hard hit by the war. For starters, the war shows that the US dollar remains the safe-haven currency of choice (chart).

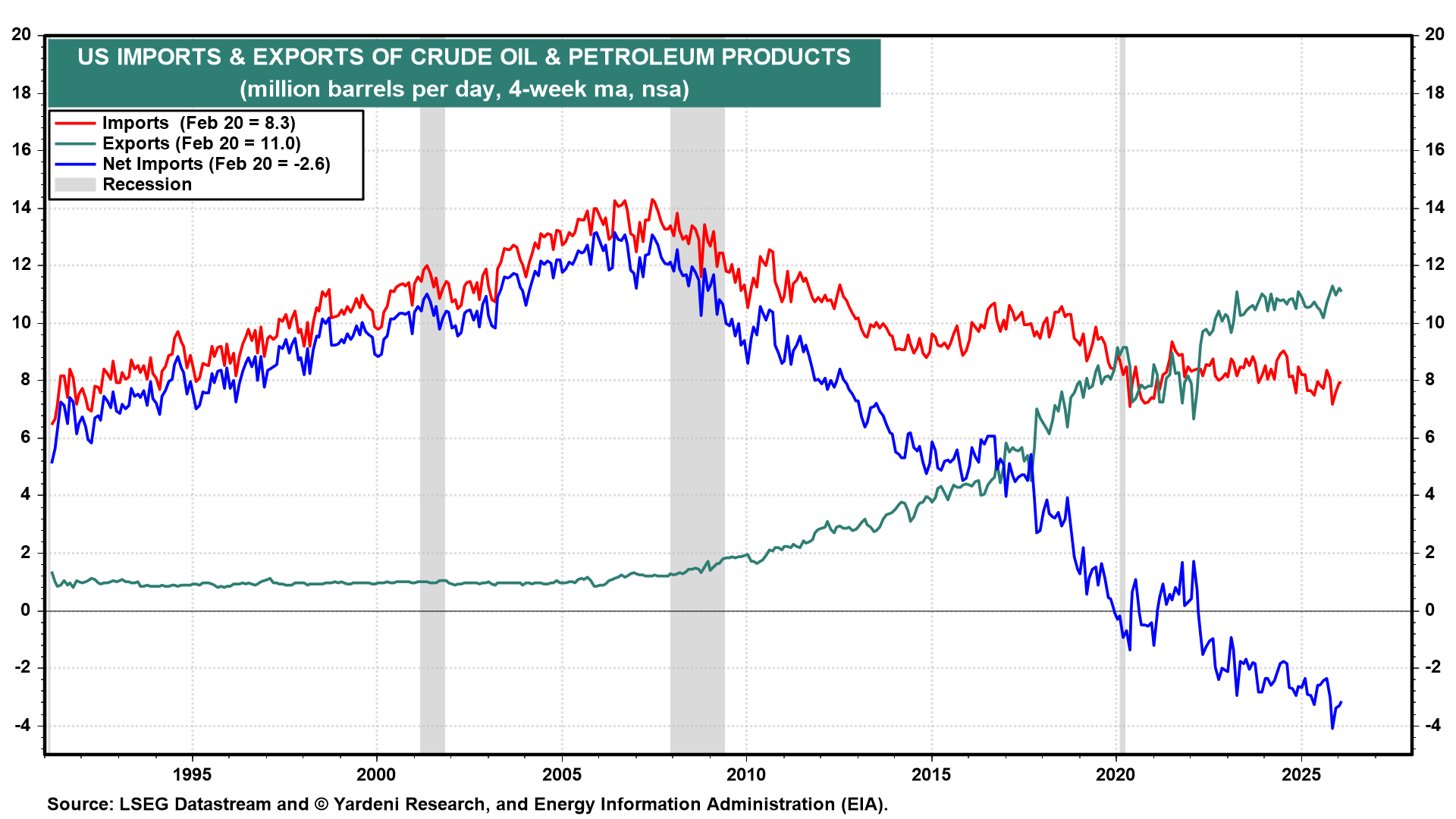

An energy crisis is likely to be less severe in the US than in many other countries that import oil and gas. The US is an exporter of both (chart). During the 1970s, high gasoline prices and shortages depressed consumer confidence and spending. This time, shortages are unlikely in the US.

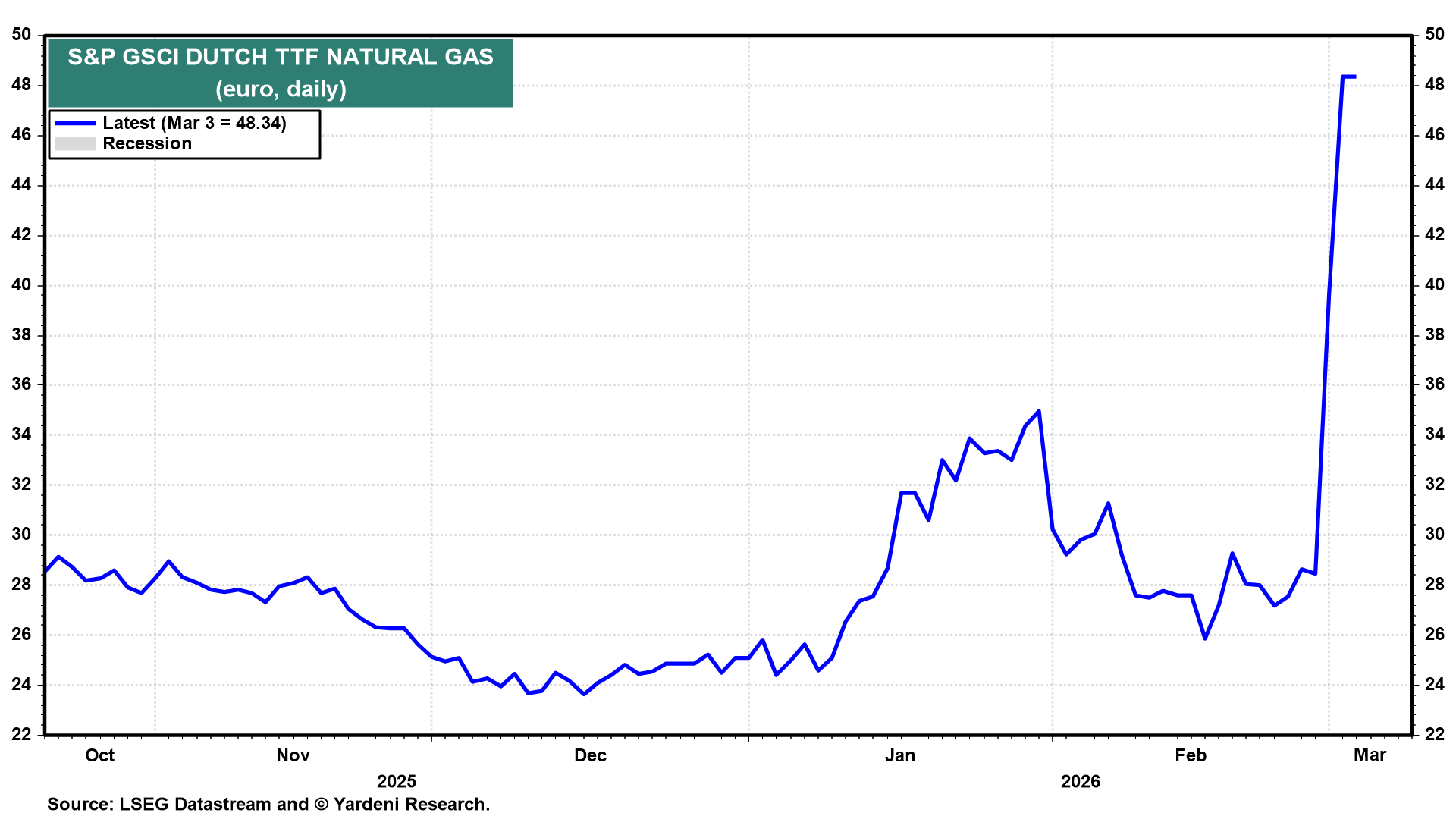

European consumers are already facing the prospect of soaring natural gas prices (chart). A similar situation, which depressed European economies, occurred after Russia invaded Ukraine in 2022.

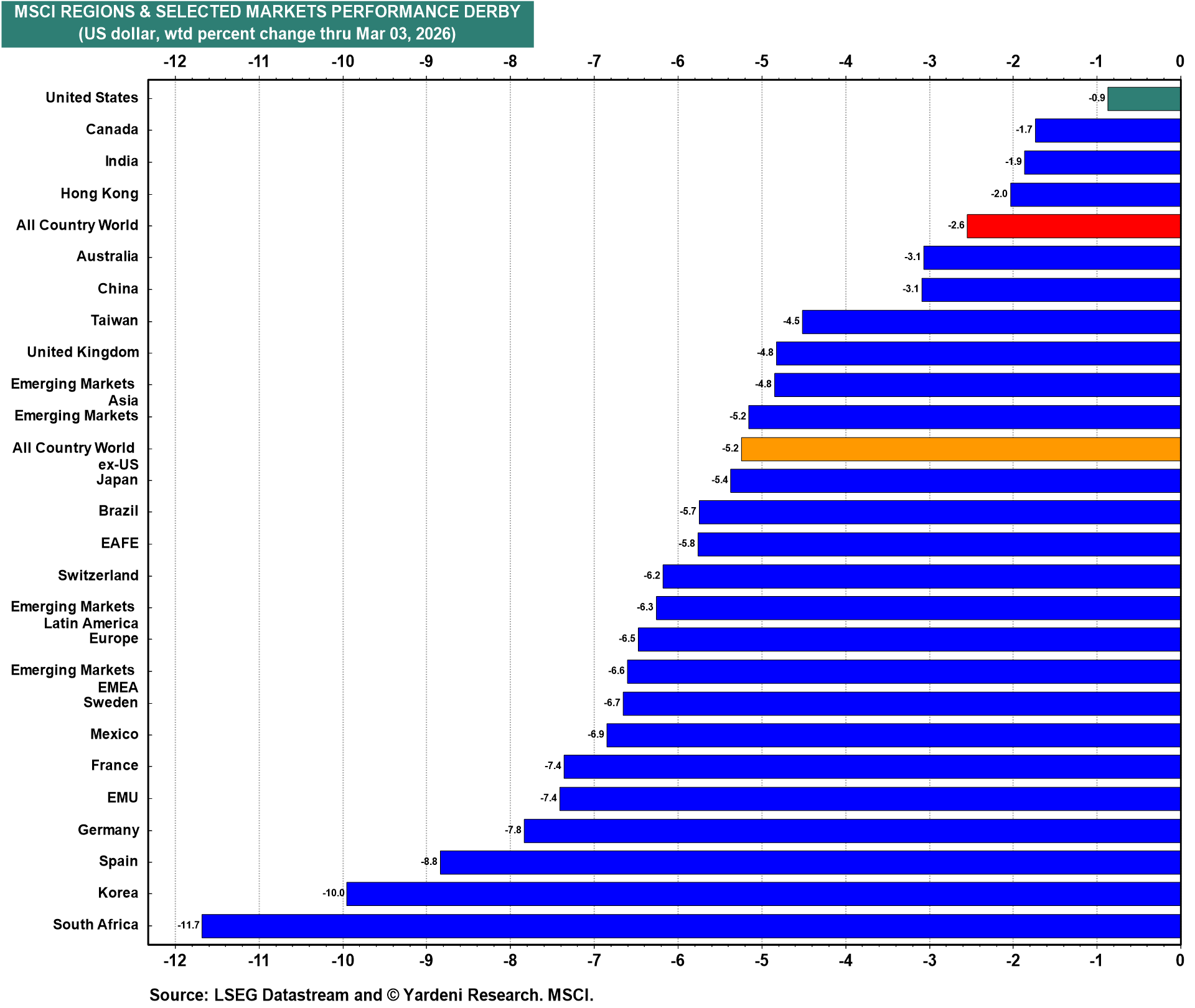

Many emerging economies are also importers of oil. So they are vulnerable to the latest oil shock. Since the war started, the US MSCI stock price index is down less than the MSCI indexes for all the other countries and regions we follow (chart).

Notwithstanding our increasing caution about the war's length and economic impact, we still expect it to last weeks rather than months. We are still targeting 7700 on the S&P 500 by the end of this year. We are sticking with our Roaring 2020s base case. We don't expect a rerun of the Depressing 1970s.

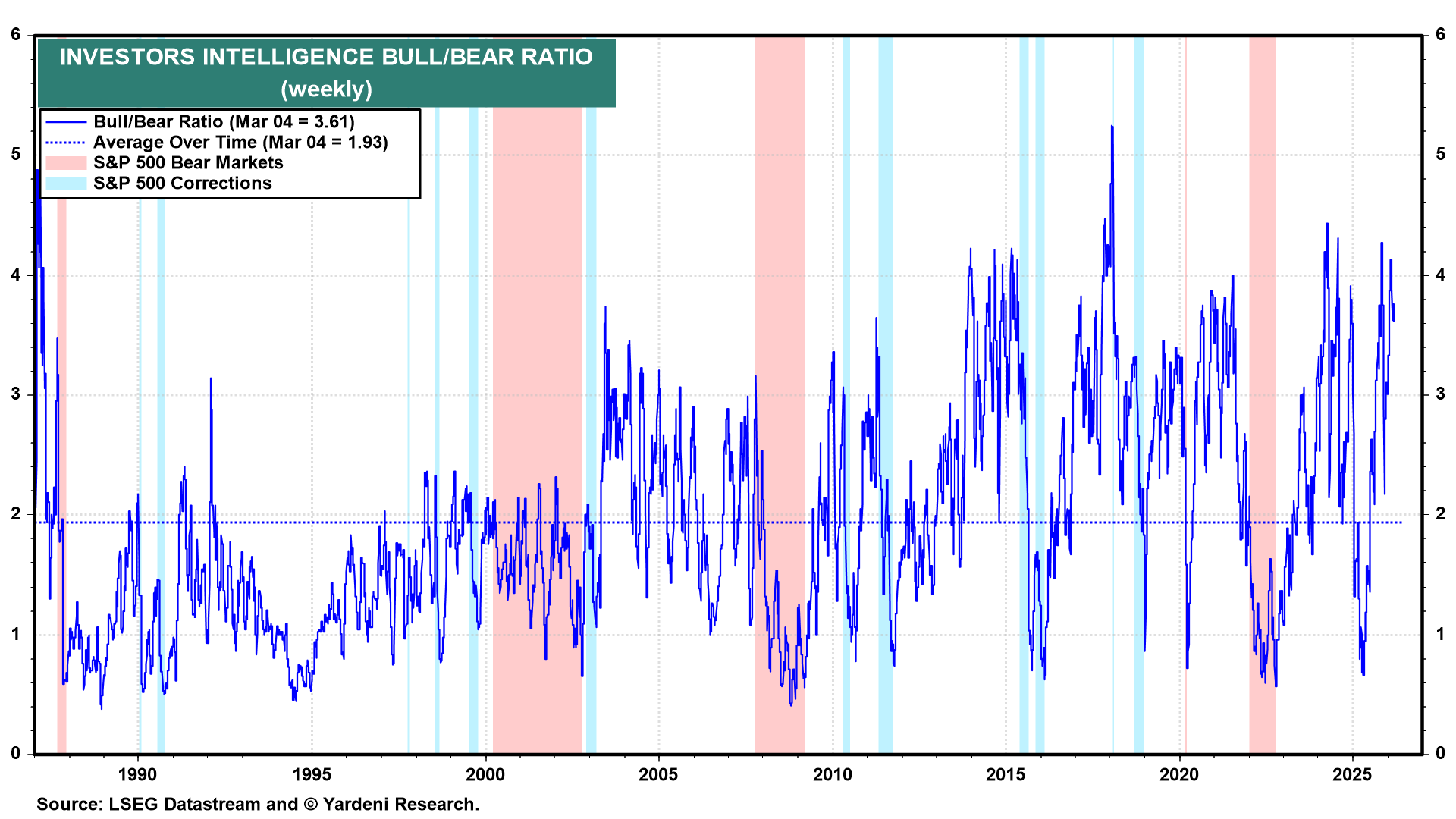

For now, we are also troubled by the latest high reading of our favorite Bull/Bear Ratio at 3.61 this week (chart). We will probably turn more bullish when investors turn more bearish.