On Tuesday, we warned: "We've been expecting a pullback due to excessive bullish sentiment, but now we expect a 10% correction from the high. It's hard to imagine that the IRGC won't use drones and speed boats to maintain their effective blockade of the Strait. If they are successful in doing so, the correction could be closer to 15%."

When the war started, our initial thought was that it might be a short one, given that Iran's government had been decapitated during the first hour of the war. On Tuesday, we had second thoughts about the length of the war. The Iranian regime had prepared for the war by adopting a chaos strategy, launching missiles and drones not just at US and Israeli targets, but at its neighbors as well. The strategy includes shutting down the Strait of Hormuz to all shipping. By causing all this pain, Iran's regime hopes that it will pressure its adversaries to negotiate a ceasefire that keeps the regime in power.

Today, we read a Bloomberg article by James Stavridis, a retired US Navy admiral, titled "Iran Can Turn the Persian Gulf Into a Minefield." The Admiral noted that Iran has hundreds, if not thousands, of the small "fast mover" speedboats that can harass civilian shipping. In addition, he stated that Iran "has been planning a Strait of Hormuz closure operation for decades and probably has more than 5,000 mines; just one hit can severely damage a thin-skinned tanker." The US and its allies have minesweepers, but not enough of them. Oil prices rose again this morning on a report that Iran had struck an oil tanker with a missile in Iraqi territorial waters.

Stock prices fell on this news. In addition, the Trump administration dropped a bombshell on the semiconductor industry today. According to a Bloomberg report released this afternoon, the administration has drafted sweeping new regulations that would give Washington unprecedented control over the global sales of AI chips from companies like Nvidia and AMD.

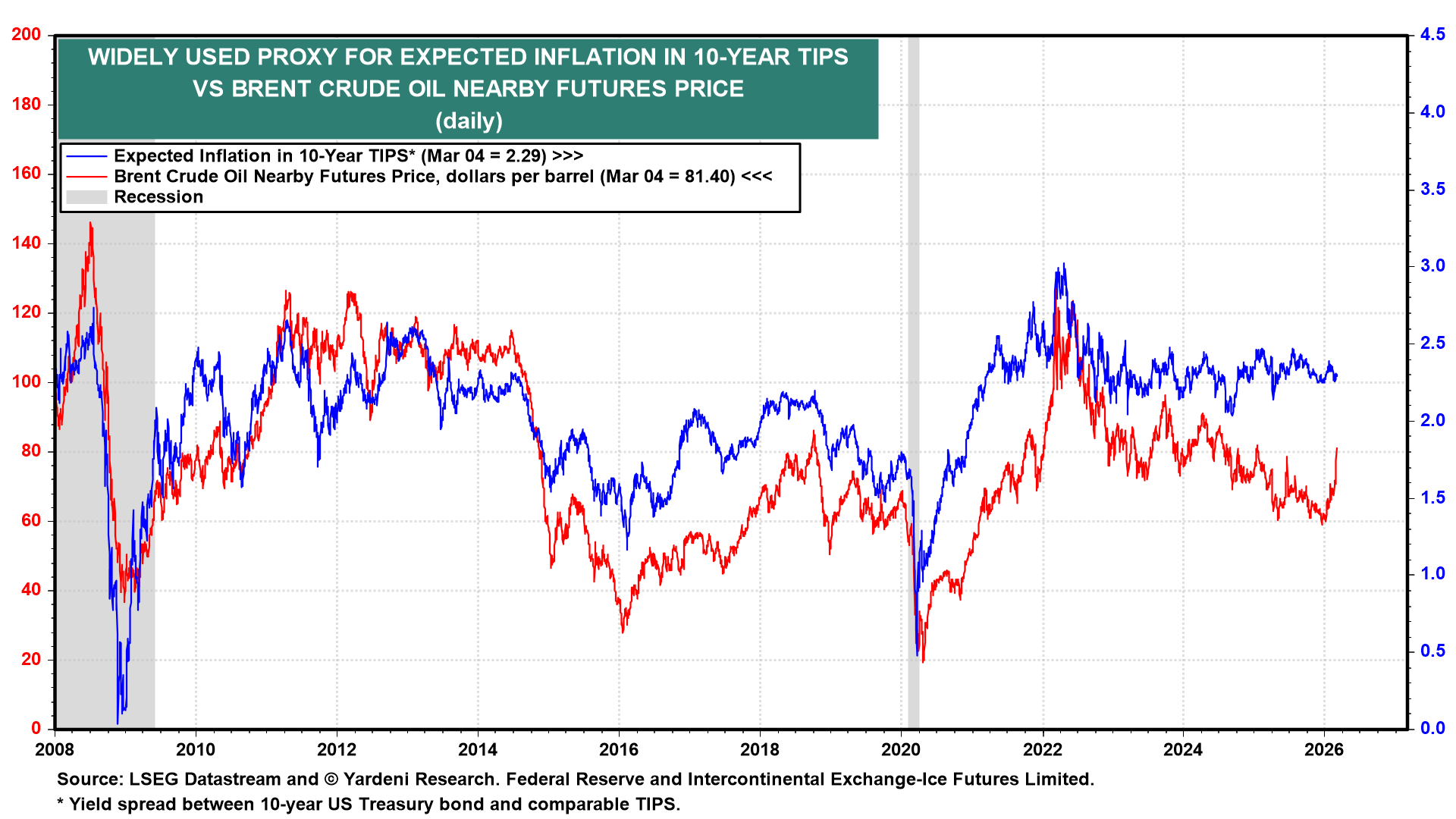

Soaring oil prices have driven up US bond yields since the war started (chart). The longer the war lasts, the more it will straitjacket the Strait of Hormuz, increasing the risk of stagflationary economic outcomes in the US and other countries. In this scenario, the Fed would be in a straitjacket too, unable to cut rates because of rising inflation, even if the economy weakens.

So far, the increase in the 10-year Treasury bond yield has been relatively small because the rise in oil prices hasn't boosted inflation expectations. However, in the past, there has been a strong correlation between the two variables (chart). If oil prices continue to rise, they are likely to boost inflationary expectations and the bond yield.

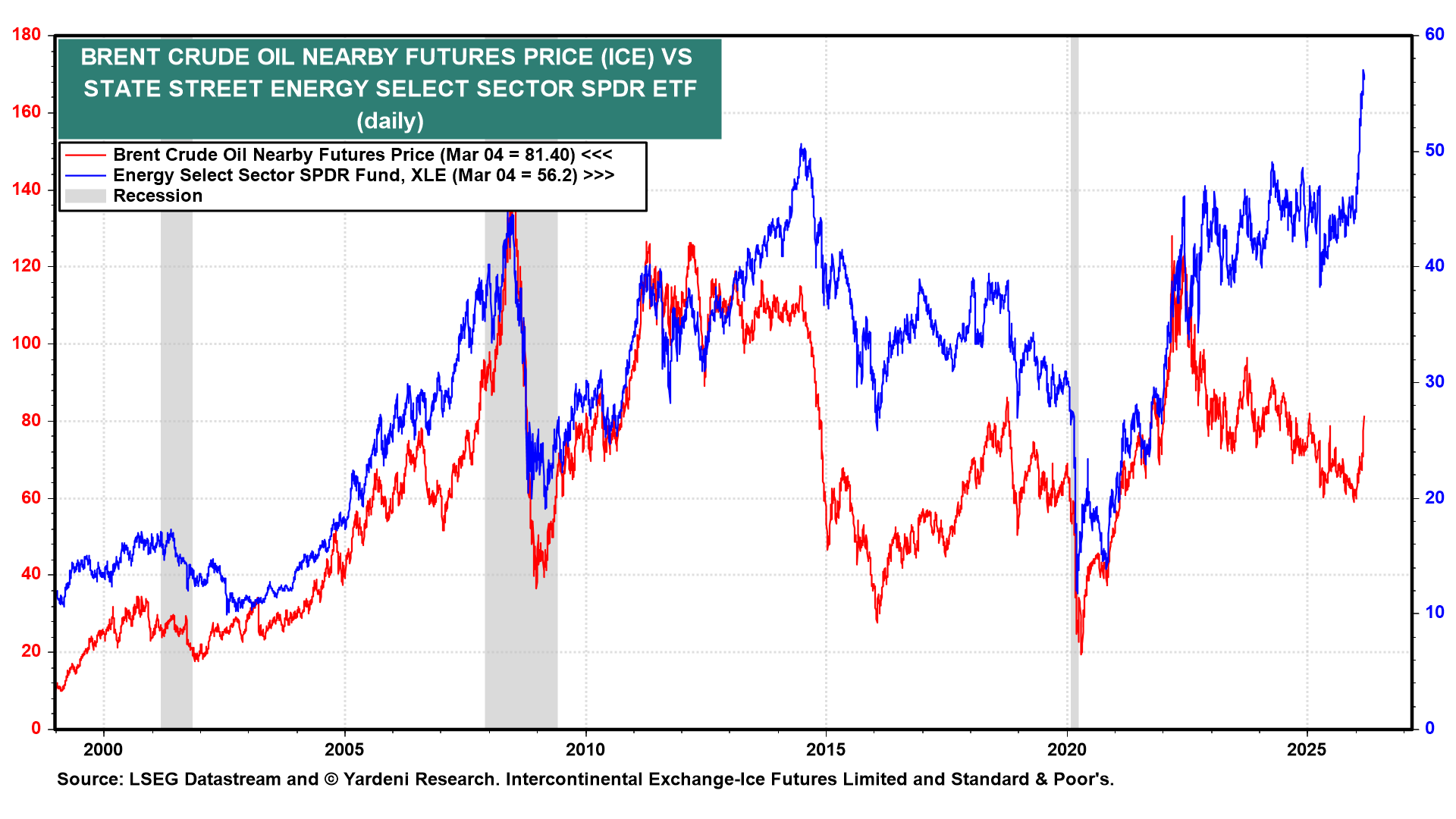

The only hedge against the war so far has been energy stocks and commodities (chart). Gold hasn't worked because the war has boosted the dollar's foreign exchange value, as the US economy is likely to be more resilient to rising energy prices than most other countries.

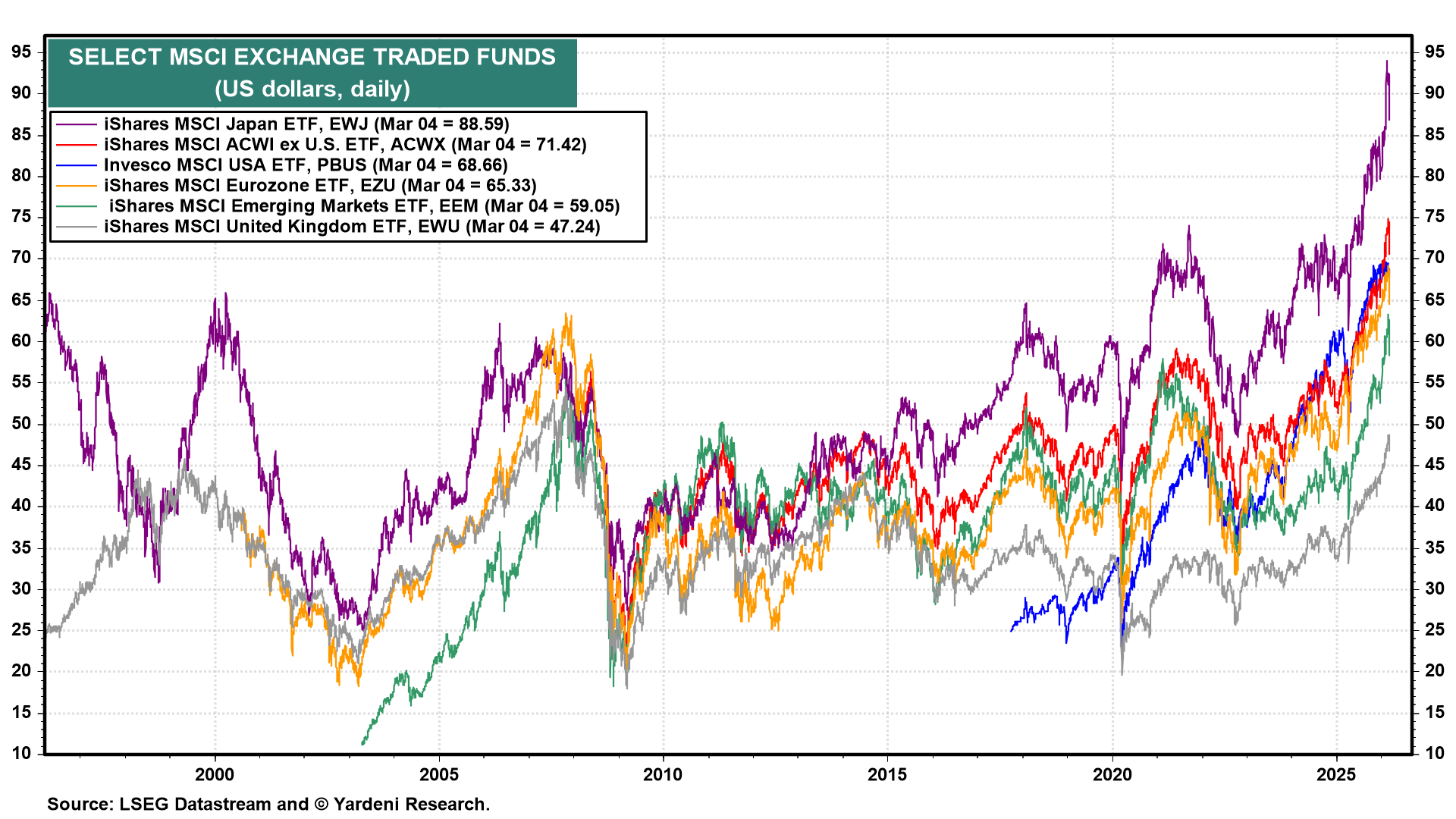

Foreign stock markets are down more than the US stock market since the start of the war (chart).

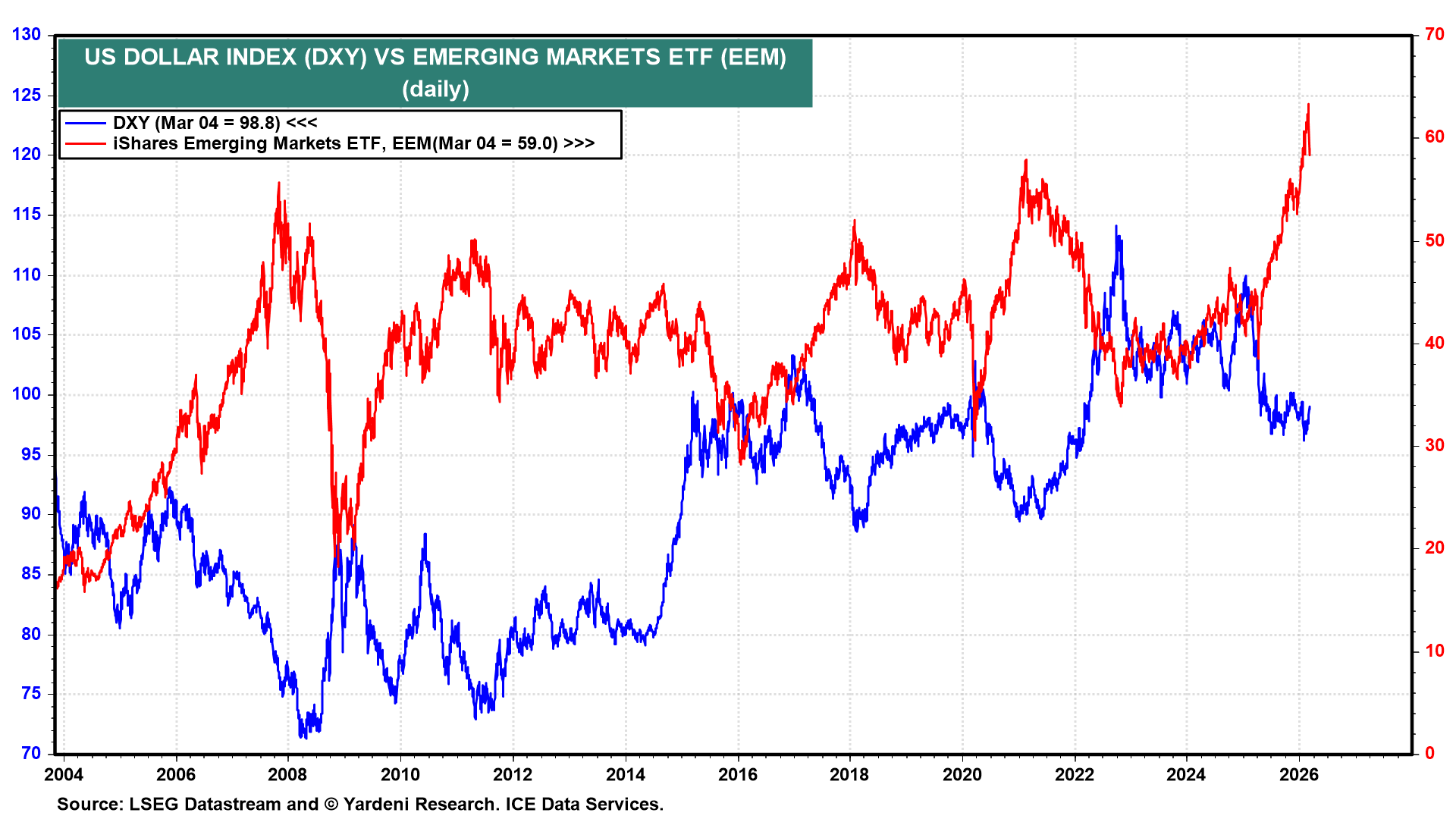

Rising oil prices are weighing on emerging market economies that import oil. The rising dollar is also weighing on the stock prices of emerging economies (chart). In our opinion, this should prove to be a buying opportunity if the war ends soon, with shipping returning to normal in the Strait of Hormuz. That's still a likely scenario given the damage that Iran is experiencing.

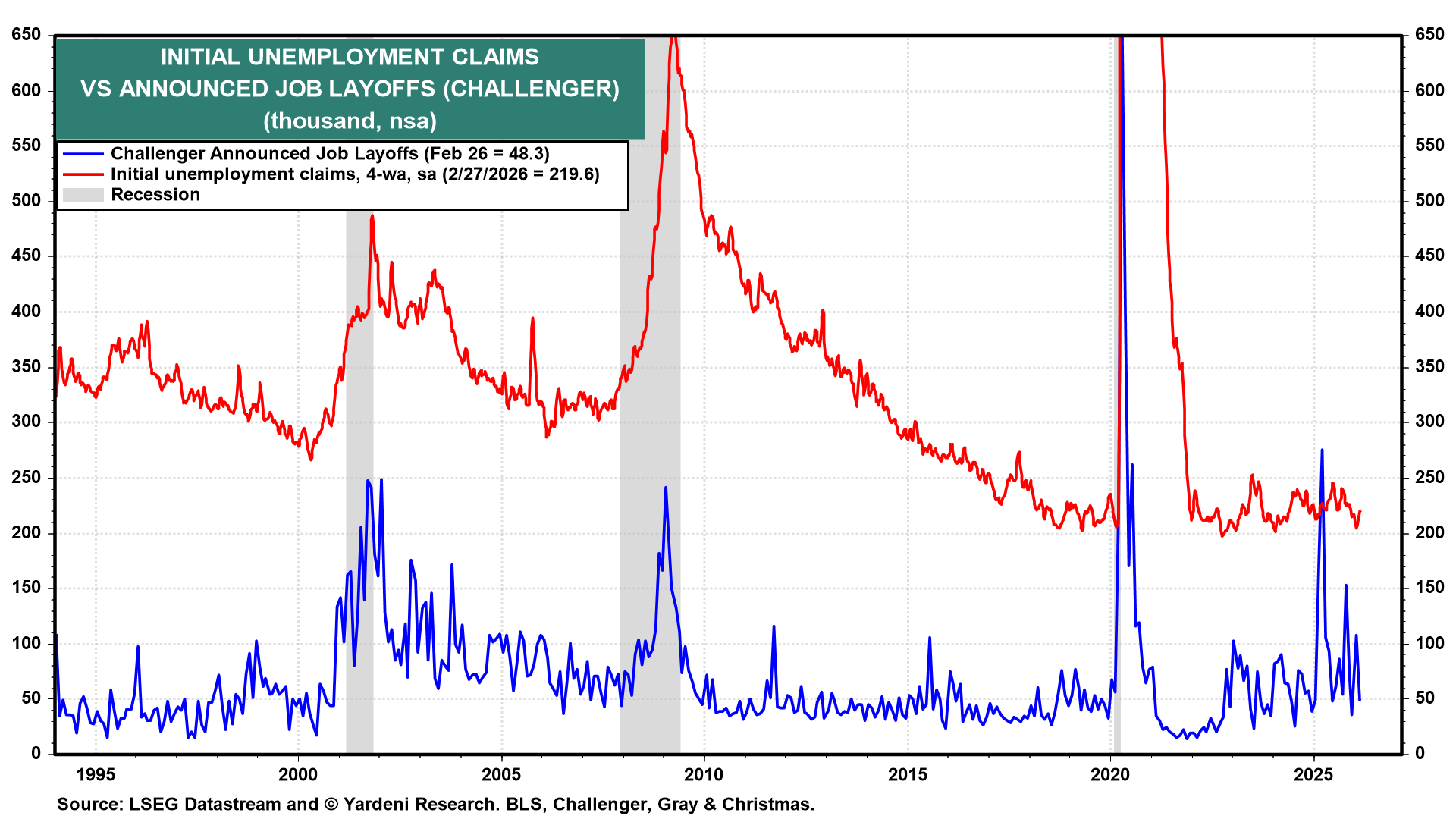

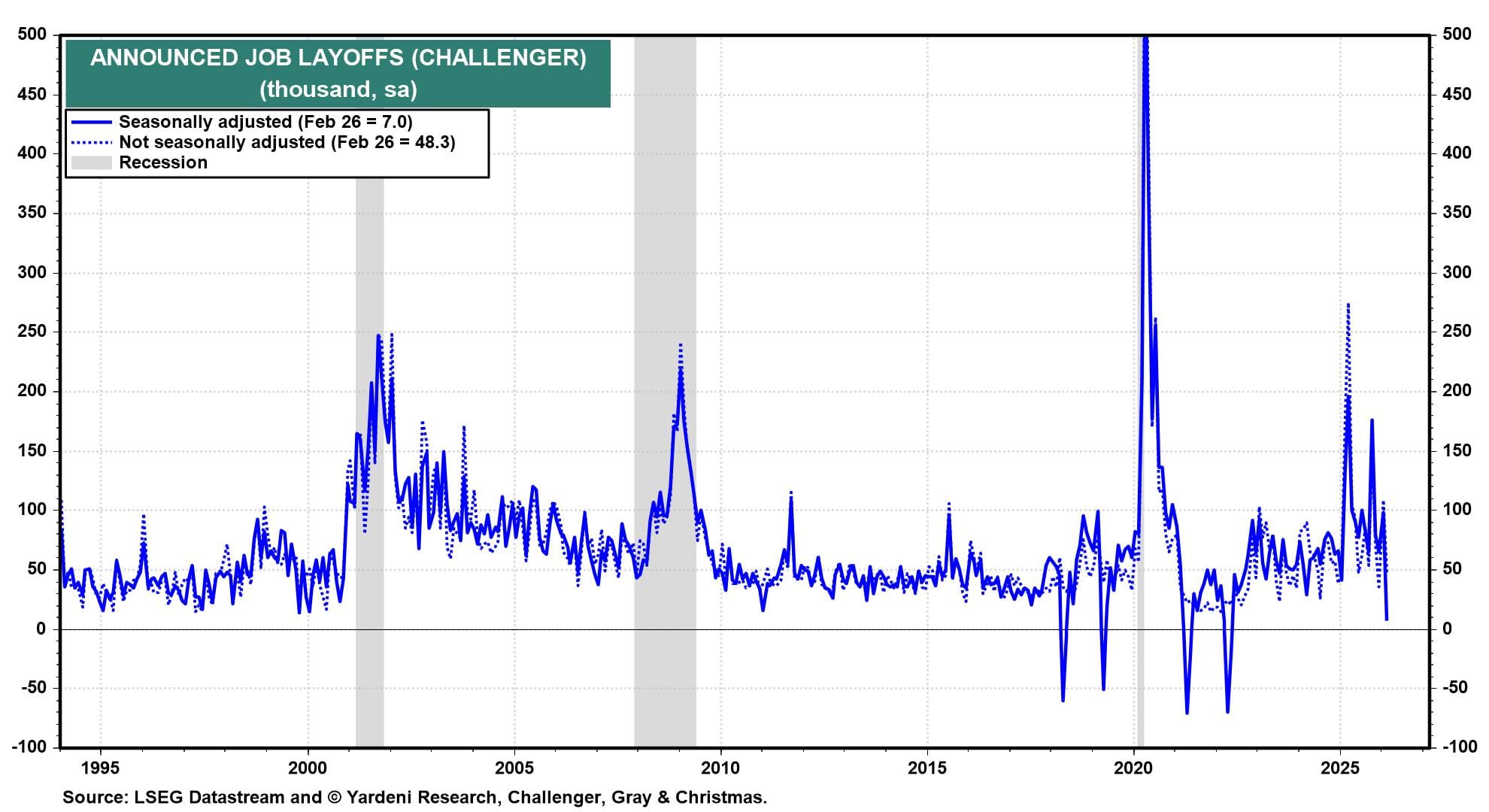

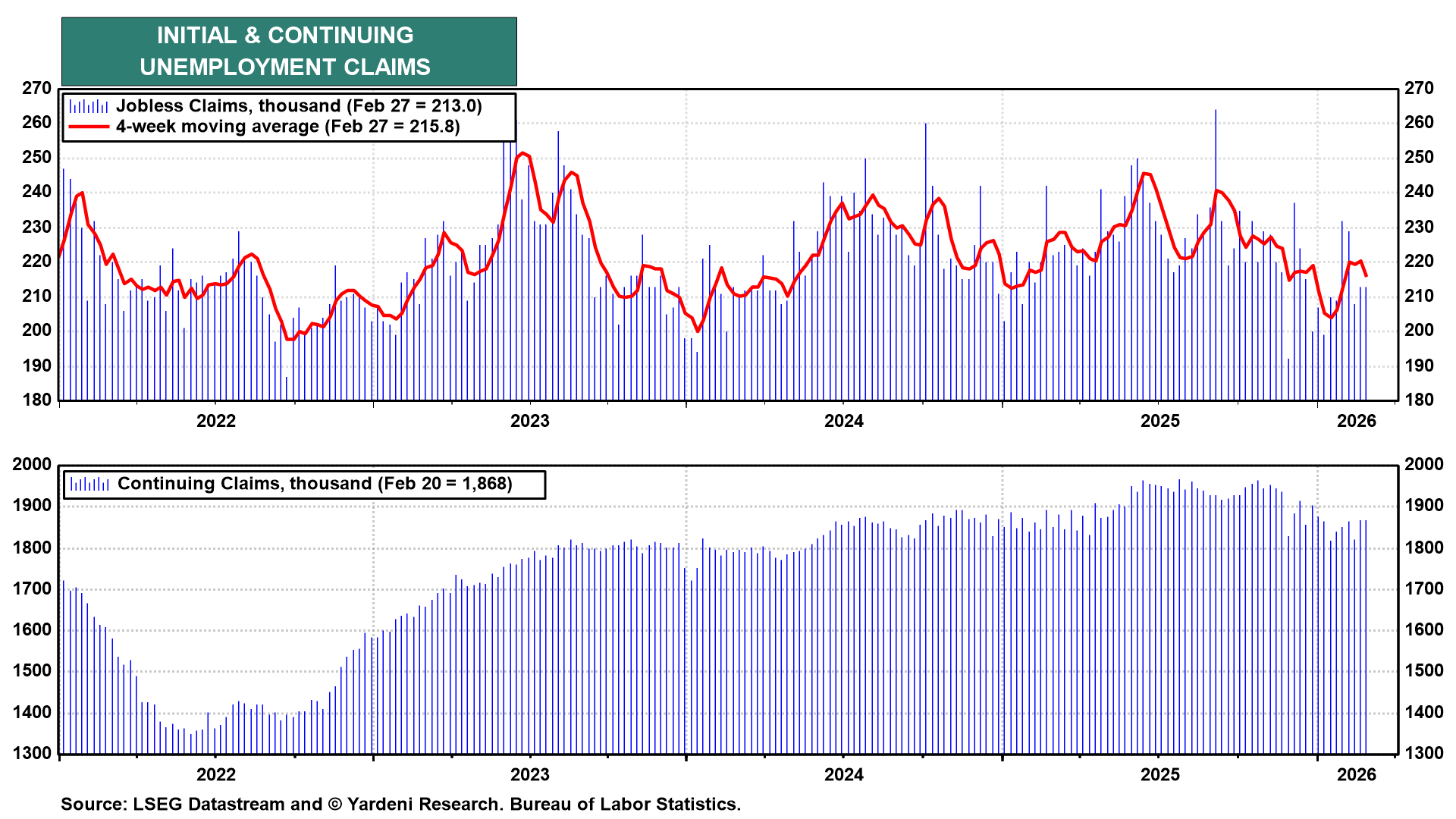

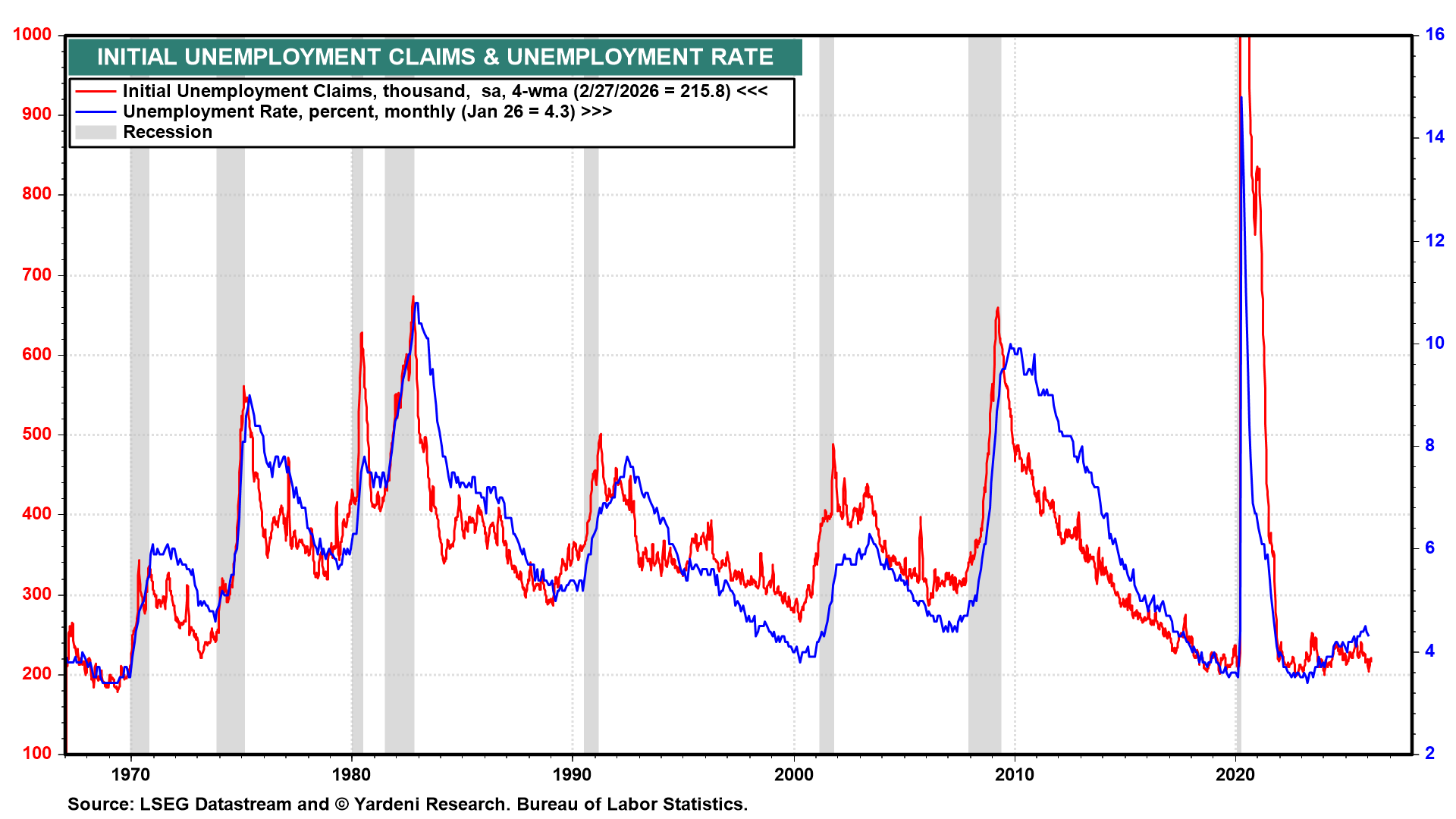

Meanwhile, back home in the US, today's initial and continuing unemployment claims, as well as February's layoff announcements, suggest that the labor market is at least stabilizing if not improving (charts). Tomorrow morning's February employment report could show a better-than-expected payroll employment gain and another drop in the unemployment rate, as in January's report.