Happy Lunar New Year! Last year was the Year of the Wood Snake, according to the Chinese Zodiac. In Chinese culture, the Snake is often seen as a symbol of wisdom, intuition, and transformation. The Horse is one of the most beloved zodiac signs. It is a powerful symbol of energy, freedom, and rapid success. Because the Horse is a social and high-spirited animal, its year is usually expected to be fast-paced and full of movement.

While the Chinese year 4724 has just started, 2026 has already been a wild ride in the stock market, with a dramatic rotation of market leadership from the Magnificent-7 to the Impressive-493. Despite the weakness in the Mag-7, the S&P 500 has held up remarkably well. It is continuing to do so despite the increasingly likely prospect that the US will attack Iran in a matter of days, which has raised the price of a barrel of Brent crude oil from around $60 at the start of the year to over $70 (chart).

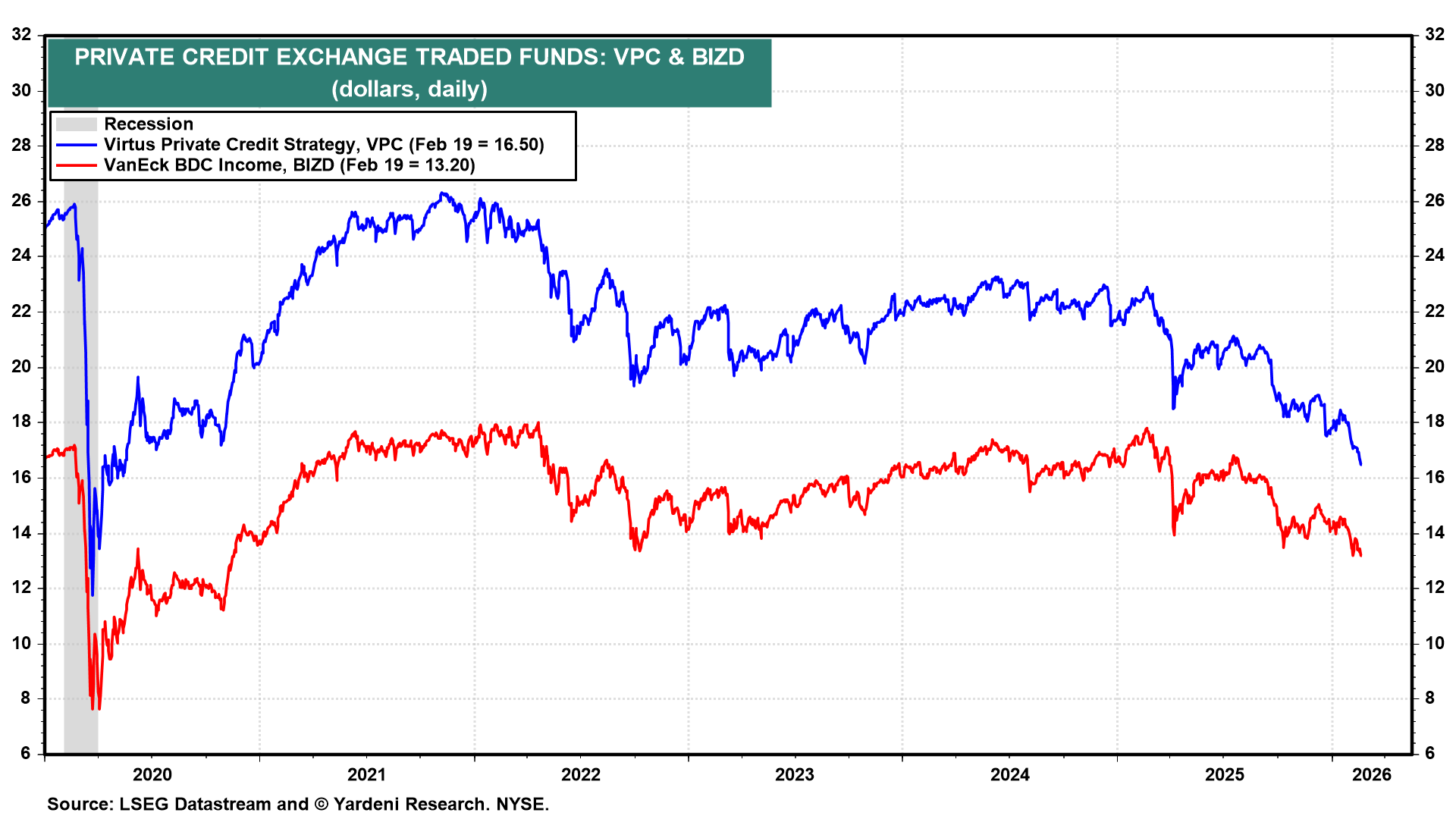

Concerns about private credit have also been increasing. Today, Blue Owl Capital shares tumbled after a decision to restrict withdrawals from one of its private credit funds raised fresh concern over the risks bubbling under the surface of the $1.8 trillion market. We've been monitoring the falling prices of ETFs that invest in the shares of private credit companies since late last year (chart). We don't expect a Lehman Moment in the private credit market, but it is included in our “what-could-go-wrong” scenario, to which we currently assign a 20% subjective probability. We include geopolitical risks in this bucket, too.

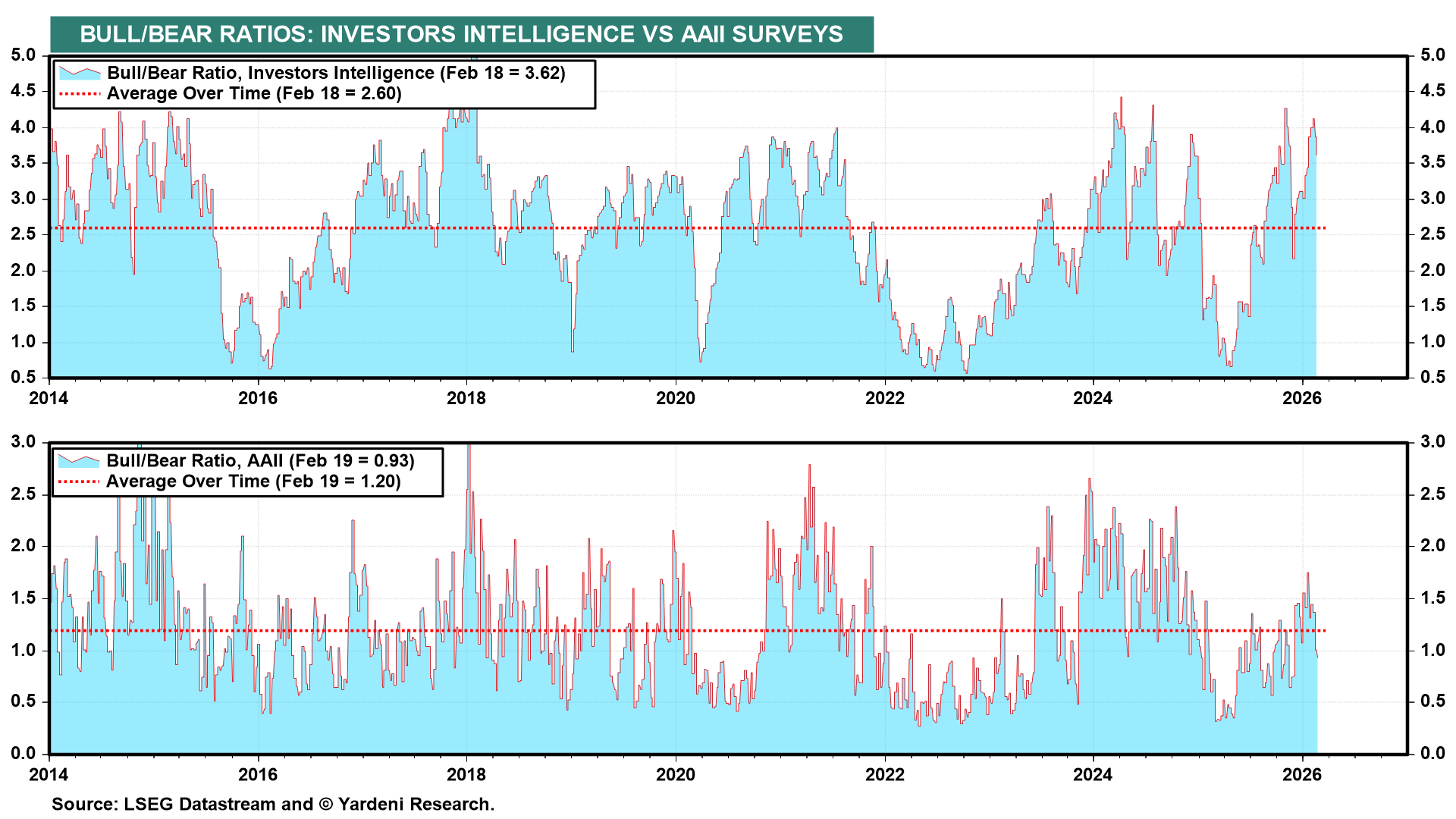

The complacency in the stock market so far this year, as evidenced by the high readings of the two Bull/Bear Ratios that we monitor, led us to conclude that a pullback was likely (chart). That's still a concern and consistent with our view that the first half of this year would be choppy. Nevertheless, for now, our base case is that the S&P 500 will rise to 7700 by the end of the year, and that the Great Rotation Trade (a.k.a. the “AI Immunity Trade”) remains the way to go.

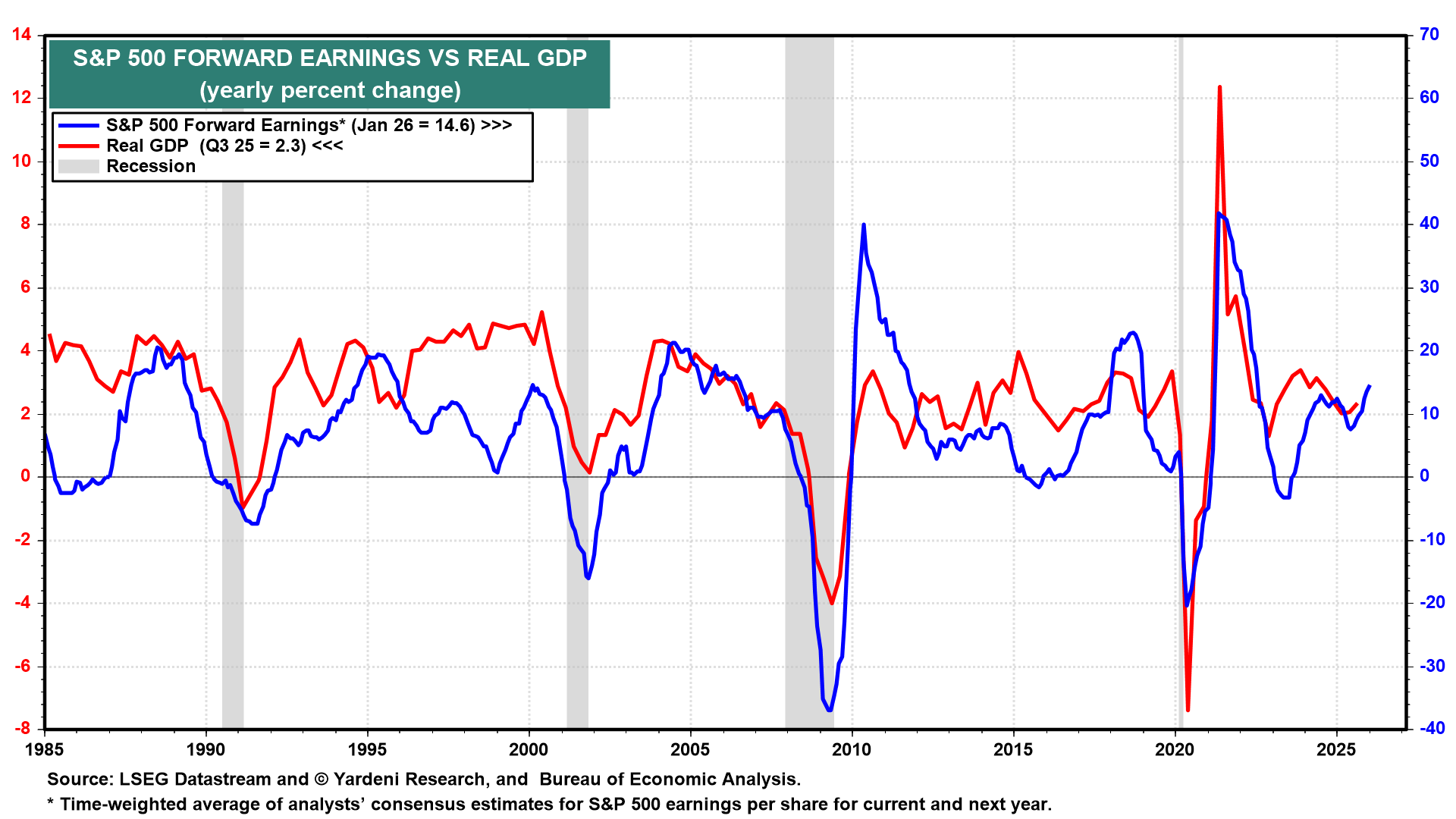

Our optimism is based on our view that corporate earnings will gallop along with the US economy this year, as they did during the last three quarters of 2025. Our favorite indicator suggests that we are off to a very good start. We are referring to S&P 500 forward earnings, which is highly correlated with real GDP on a y/y basis (chart). The former suggests that the latter has been picking up at the start of 2026. Forward earnings is available both weekly and monthly.

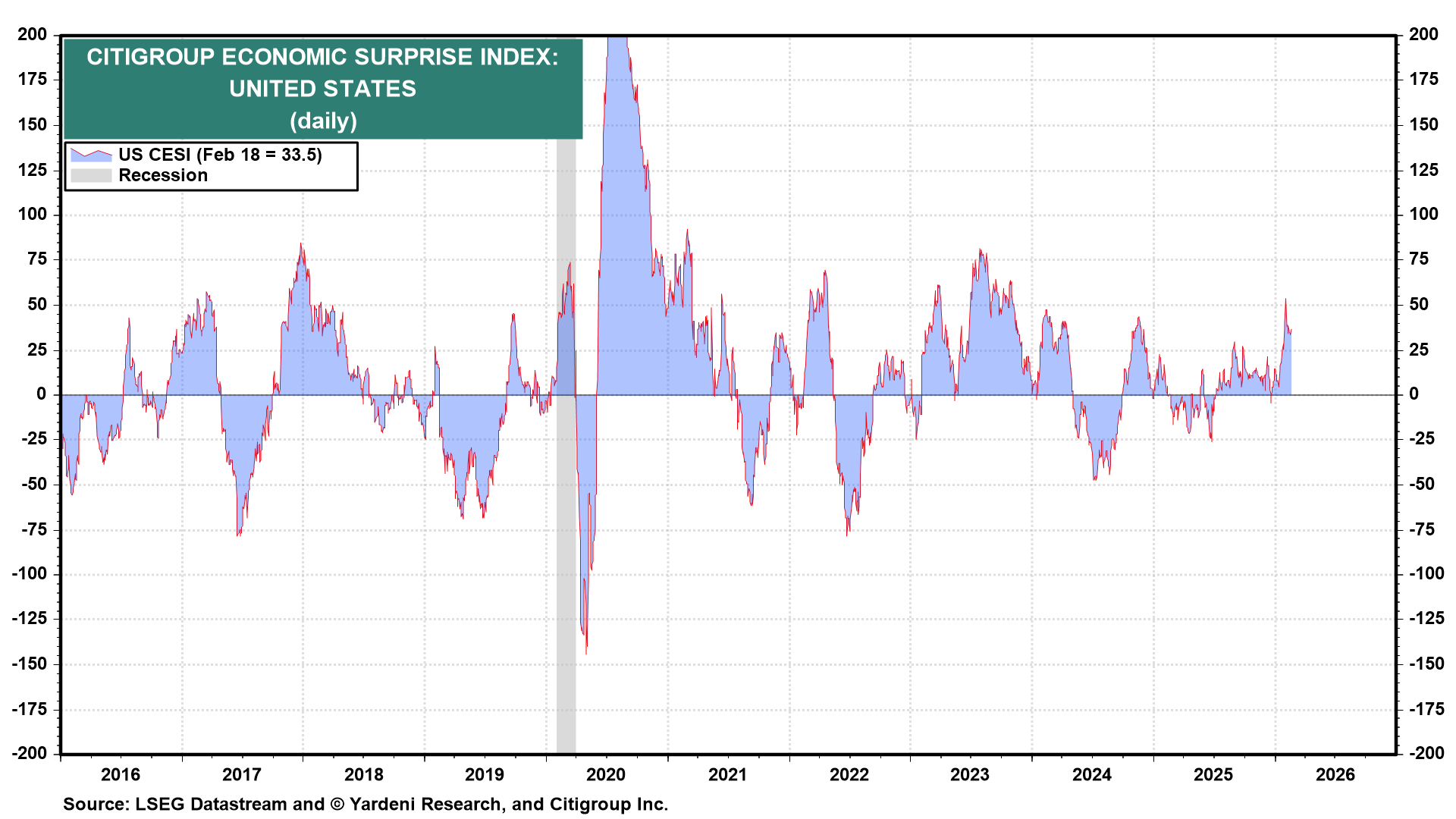

Another indicator that has started to gallop in recent weeks is the Citigroup Economic Surprise Index, which has exceeded last year's readings (chart).

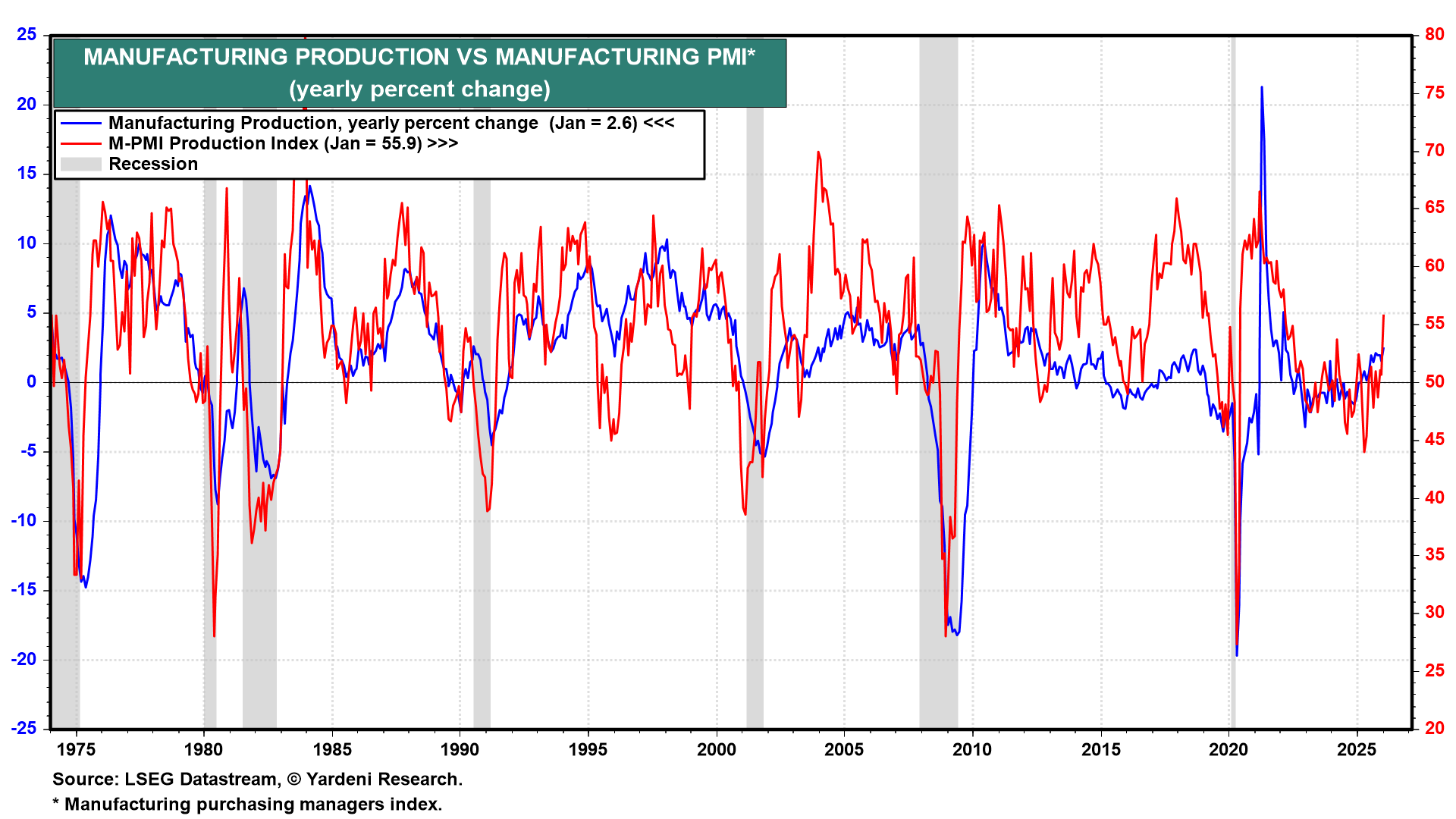

Even the manufacturing sector, which has been hobbling for the past few years, may be starting to gallop. The M-PMI Production Index jumped to 55.9 in January, its highest reading in years, while manufacturing production growth firmed to 2.6% y/y in January.

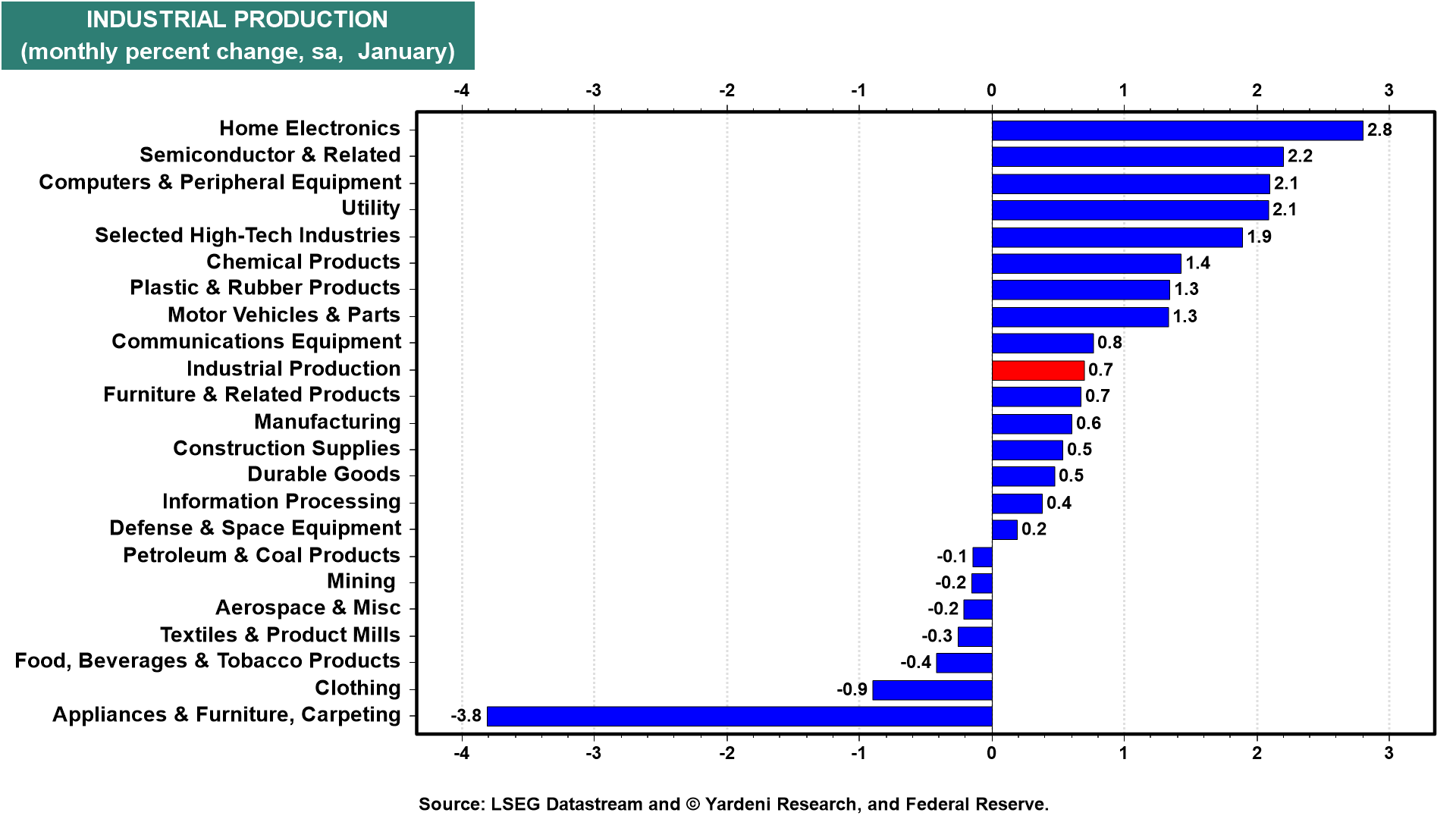

Industrial production rose by 0.7% m/m in January, exceeding estimates of 0.4% and accelerating from a downwardly revised 0.2% gain in December (chart). Strength was concentrated in high-tech industries, including home electronics, semiconductors, and computers.

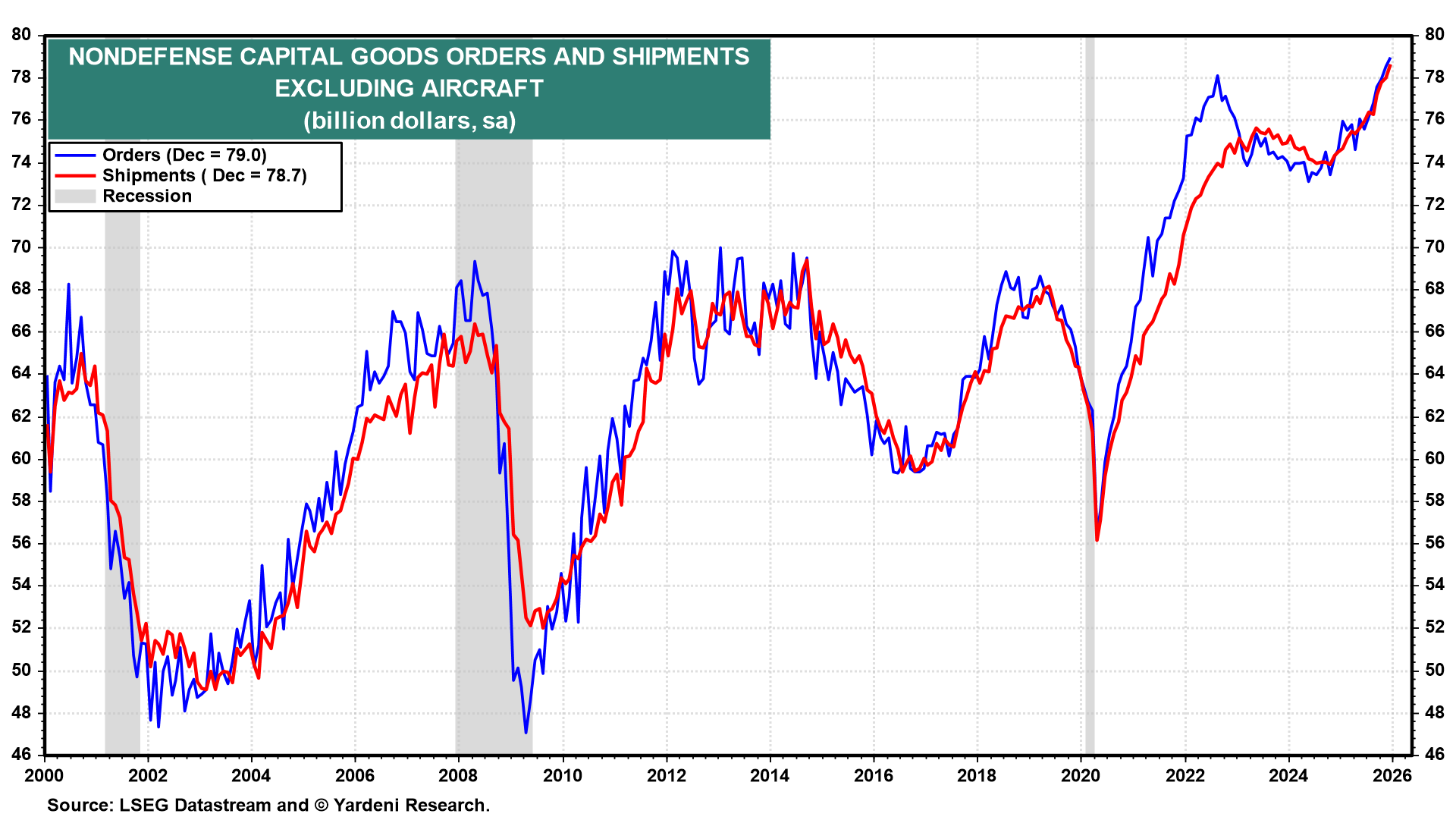

Nondefense capital goods orders and shipments excluding aircraft hit record highs in December (chart).

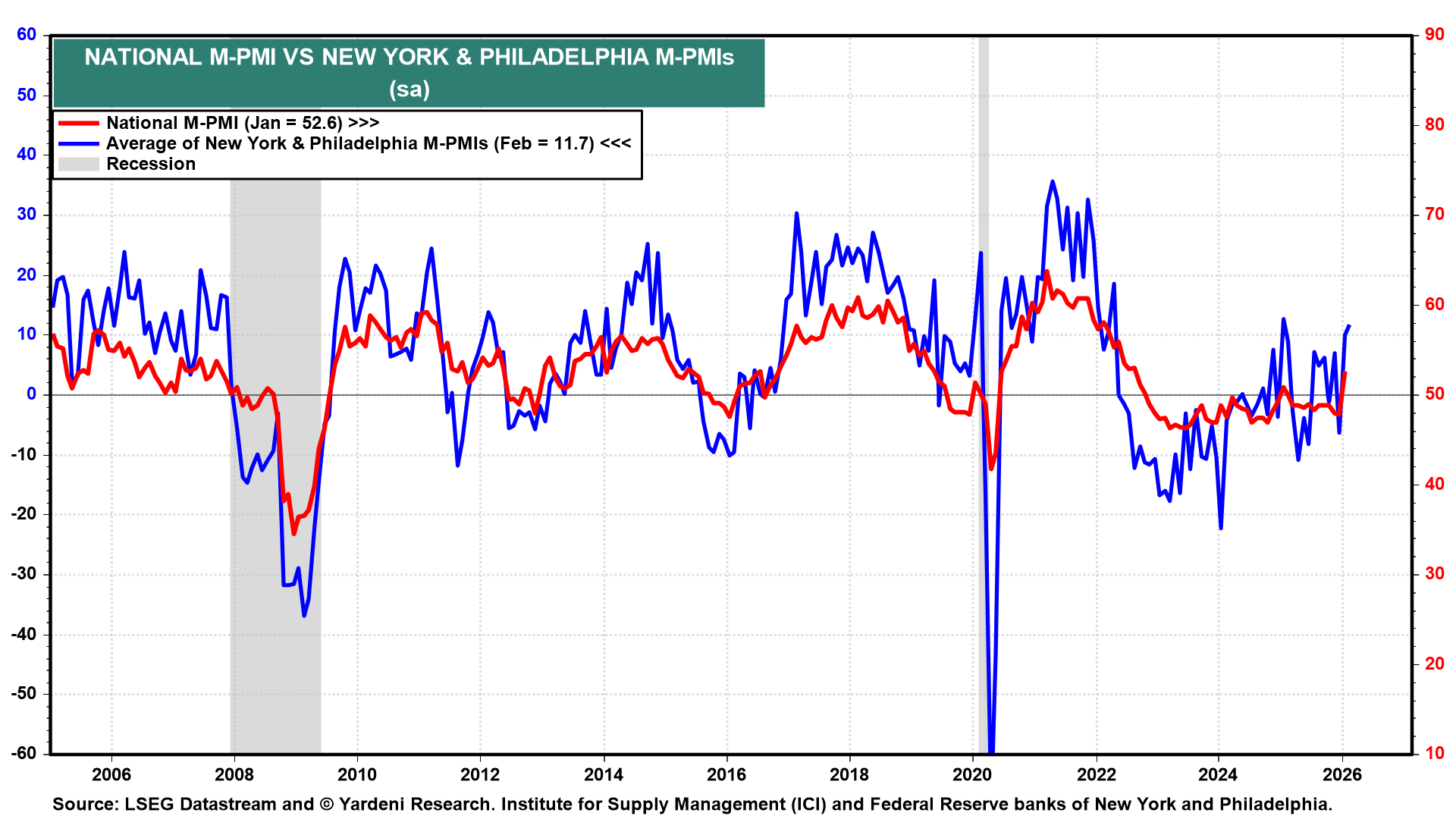

Regional business surveys from New York and Philadelphia continued to improve in February, reinforcing the fact that the manufacturing recovery is finally happening (chart).

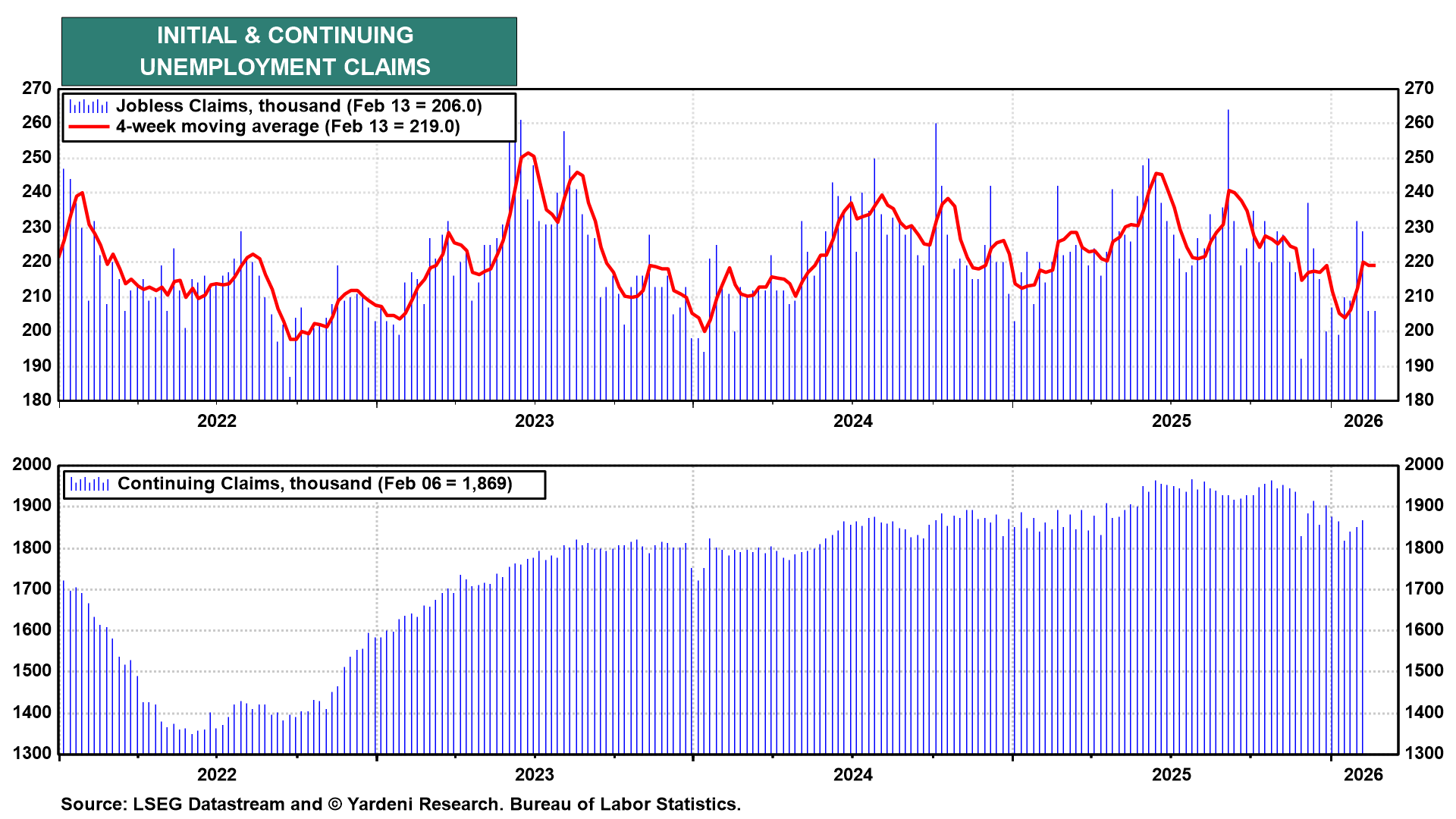

Initial unemployment claims fell to 206,000 for the week ended February 13, well below expectations. Continuing claims edged up slightly to 1.87 million but remain well below last year's highs. We wouldn’t be surprised by another upside surprise in payroll employment during February.

All indications are that 2026 and 4724 should be as interesting as 2025 and 4723.