We have nothing to fear but nothing to fear. Stock investors have been fearless since the S&P 500 fell to the year's low on March 30, when war-related fears peaked. The index has soared 16.1% since then to a new record high.

Yesterday, we explained our Buzz Lightyear Theory (BLT) of the stock market. Investors have concluded that, thanks to AI, demand for "compute" will increase to infinity and beyond, and so will the earnings of the S&P 500, including the hyperscalers and the semiconductor companies, particularly those that manufacture memory chips.

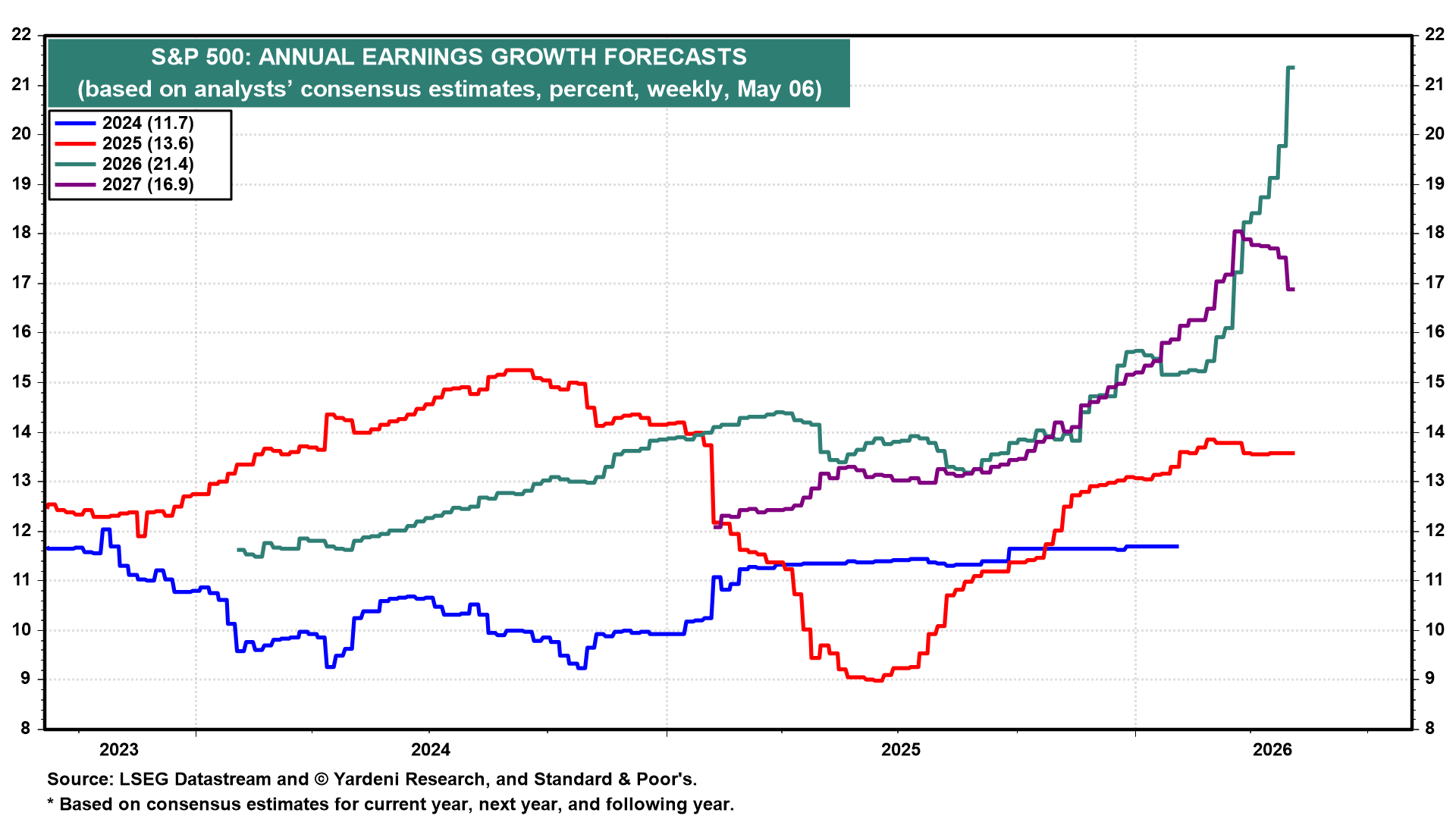

Even more fearless is the consensus of industry analysts. They didn't flinch during March when the war in the Middle East was raging. They raised their earnings growth expectations for 2026 that month and continued to do so, up to 21.4% currently (chart). They’ve also been raising their expectations for the level of 2027 earnings, but the growth rate for next year has declined in recent weeks to 16.9% simply because this year's upward estimate revisions have been so strong! That's mostly because companies have beat their estimates during Q4-2025 and now Q1-2026.

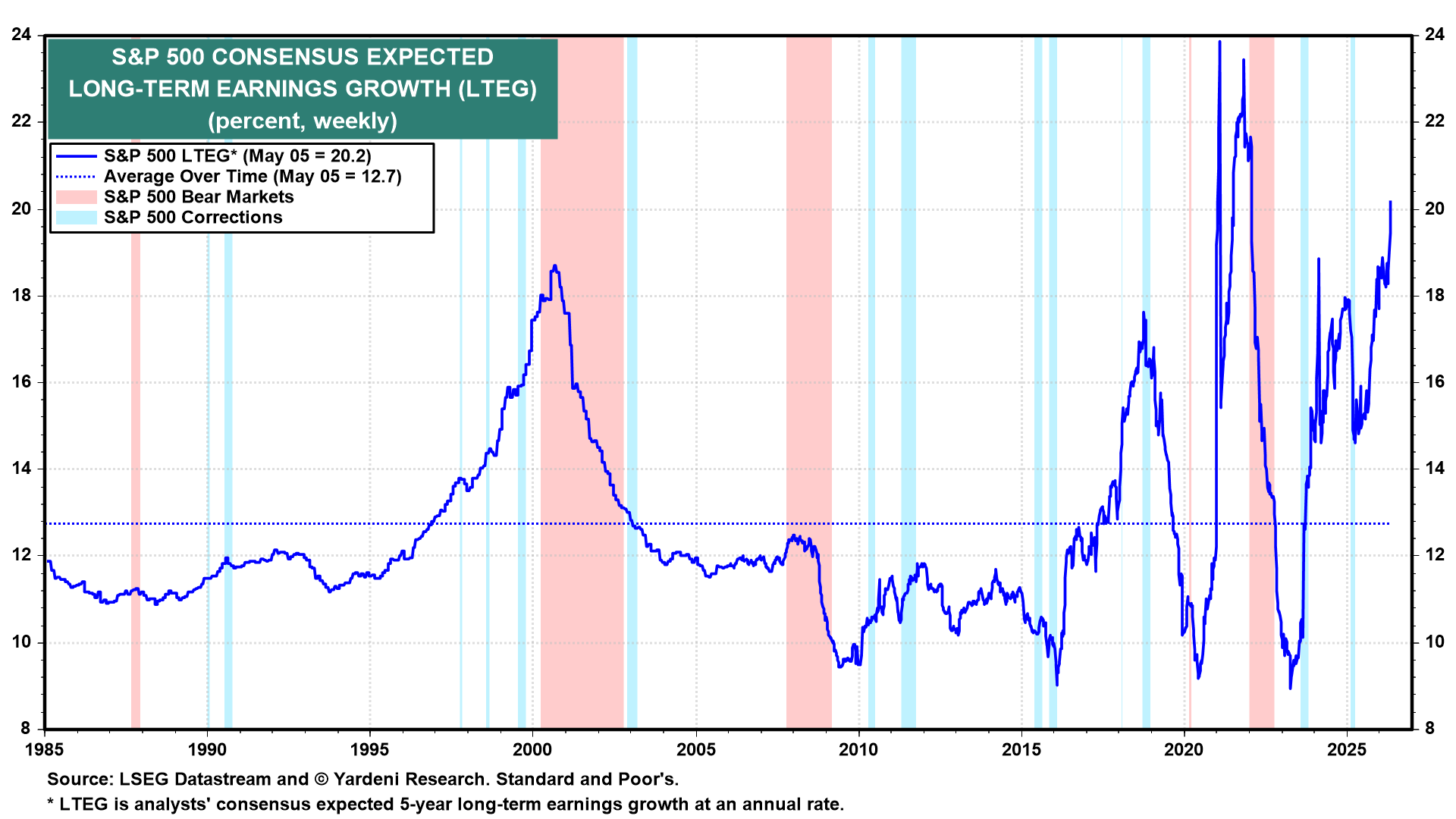

The analysts may be starting to get “Buzzed,” as their expected long-term earnings growth (LTEG) for the S&P 500 rose to 20.2% during the week of May 5 (chart). It rose even higher during the pandemic, when fiscal and monetary policymakers both were slamming on the accelerator. But LTEG now exceeds the 18.6% peak of the 2000 tech bubble.

So the recent melt-up in actual and expected S&P 500 earnings has weighed on the index's forward P/E. The PEG ratio, which is the forward P/E divided by LTEG, is down to 1.03 (charts). The market looks cheap unless earnings growth expectations for the rest of the Roaring 2020s and the early Roaring 2030s get bashed, as they did after the Tech Wreck of 2000.