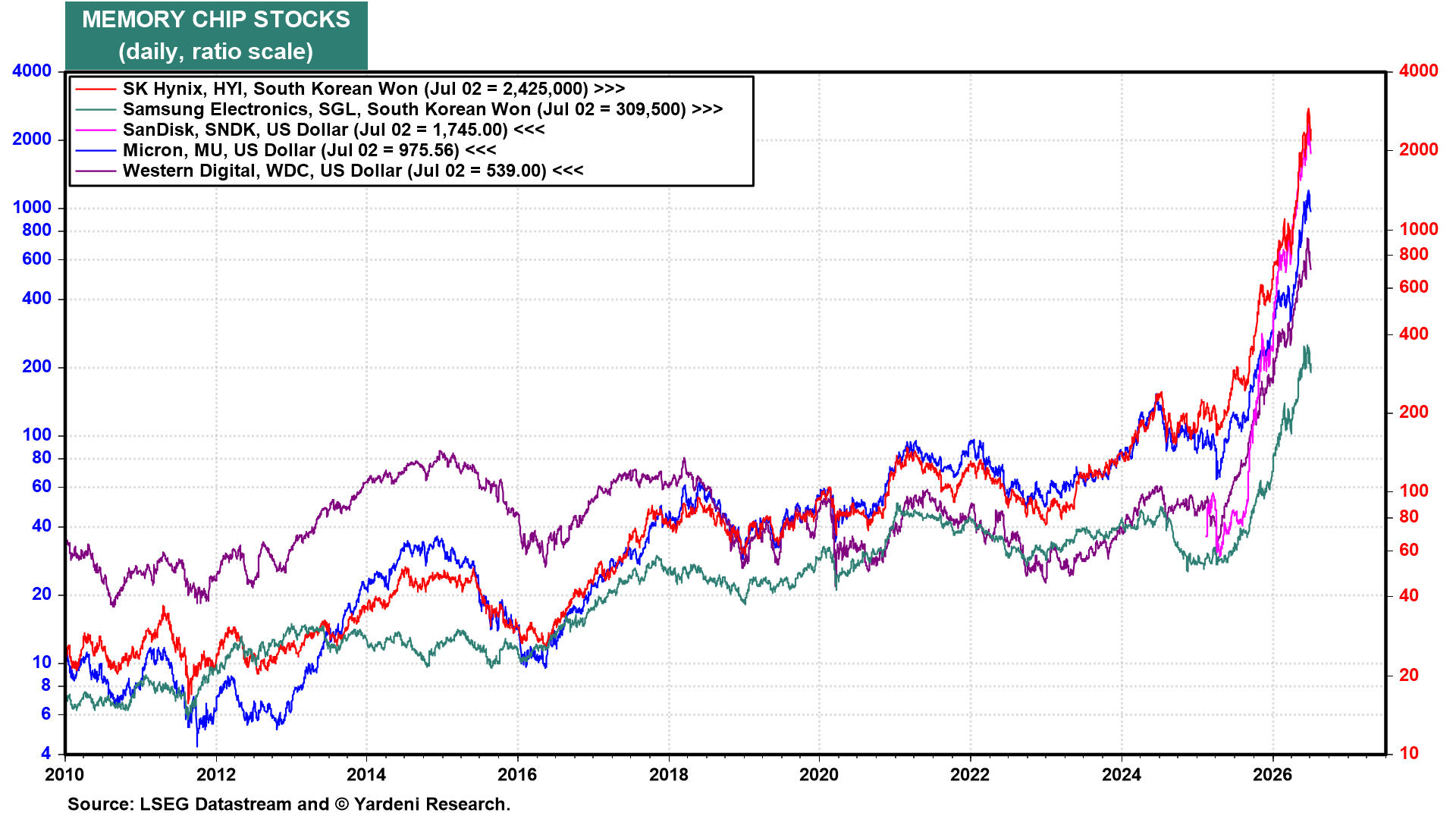

The S&P 500 closed Thursday at 7,483.23, up 1.8% on the week, while the Nasdaq rose 2.1%. Memory chip stocks pulled back sharply last week, cooling off the parabolic run that followed Micron's blowout June 24 earnings report (chart). Shares surged 17% the next day to a new all-time high of $1,255.00, then closed Thursday at $975.56, down 22.3% from the intra-day high. That is the same pattern as March, when a blowout earnings report also sent shares to a high before a sharp pullback.

June's jobs report on Friday adds to the uncertainty. Payrolls rose just 57,000, well below the 115,000 consensus, with April and May revised down a combined 74,000. The unemployment rate still fell to 4.2%, but only because labor market participation dropped to 61.5%, the lowest since March 2021.

Nothing on this week’s calendar rivals either of those stories for market impact. Earnings season doesn’t start in earnest until JPMorgan and Citigroup report on July 14. Here are the key economic releases most likely to shape investors' thinking this week:

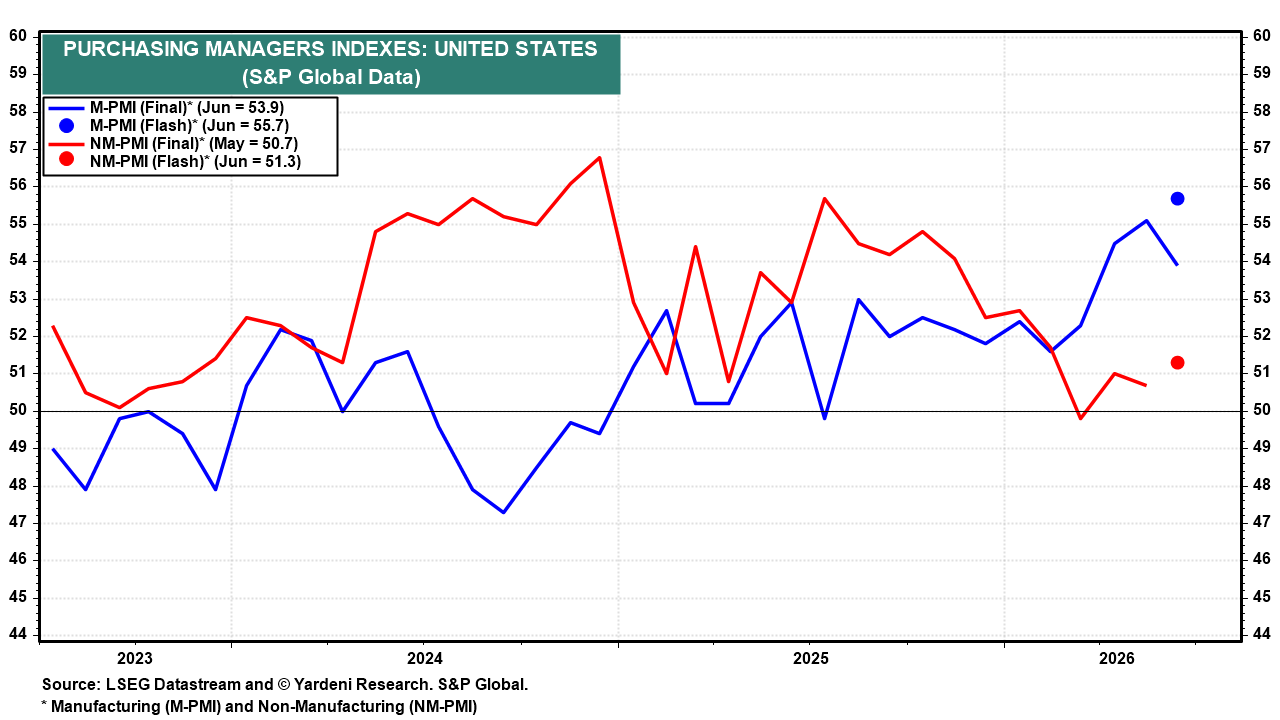

(1) PMI. June's ISM Services PMI (Mon) should remain in expansion territory, according to the comparable S&P Global index (chart).

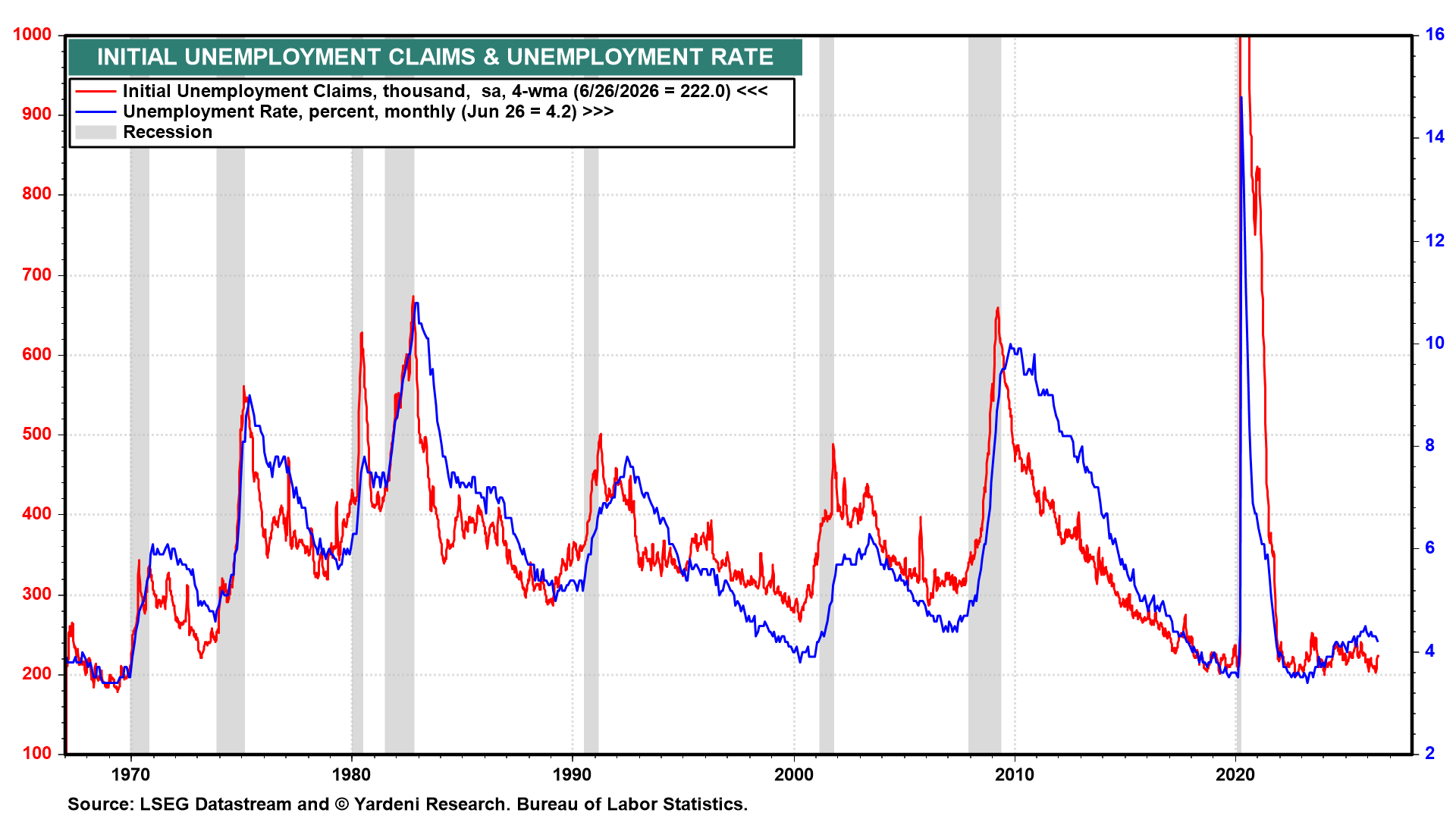

(2) Employment. Initial unemployment insurance claims for the week of June 26 held at 215,000, a 4-week average of 222,000, both within the range of the past two years (chart). Thursday’s report is the most current read on the labor market since the payrolls miss. It should confirm that layoffs remain low (chart).

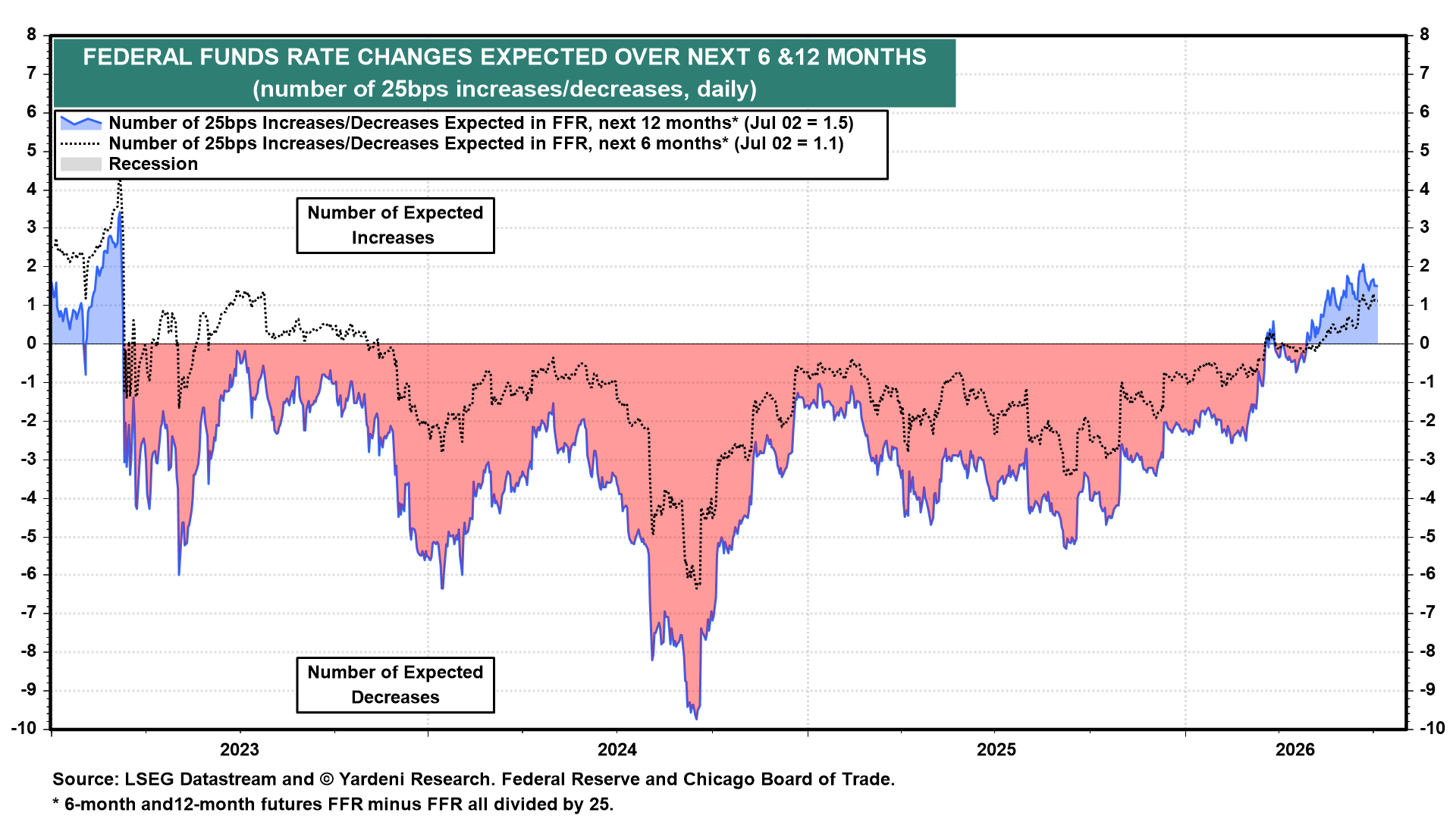

(3) FOMC Minutes. June‘s meeting minutes (Wed) is the first under new Fed Chair Kevin Warsh. He skipped the dot plot in June and has avoided forward guidance since taking over. Fed funds futures now imply 1.5 rate hikes over the next 12 months, a sharp reversal from the deep rate cut pricing that dominated the past three years (chart). The minutes should indicate how much of that repricing the committee actually endorses.

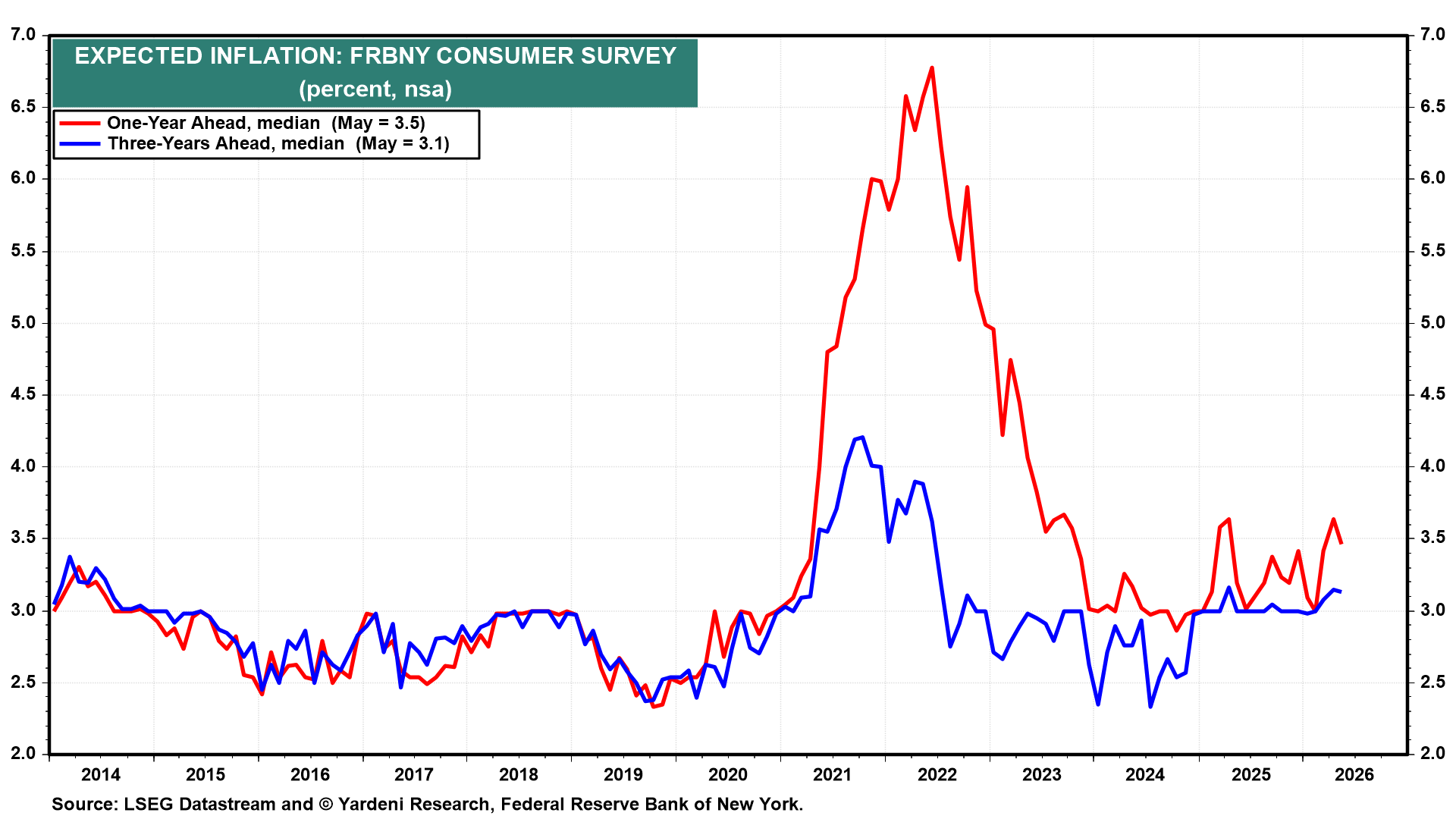

(4) Inflation Expectations. June's NY Fed survey of inflation expectations (Tue) is due this week. Its one-year-ahead measure was at 3.5% in May, with the three-year-ahead measure lower still at 3.1% (chart). The gap between the two suggests that consumers see current price pressures as more temporary than structural

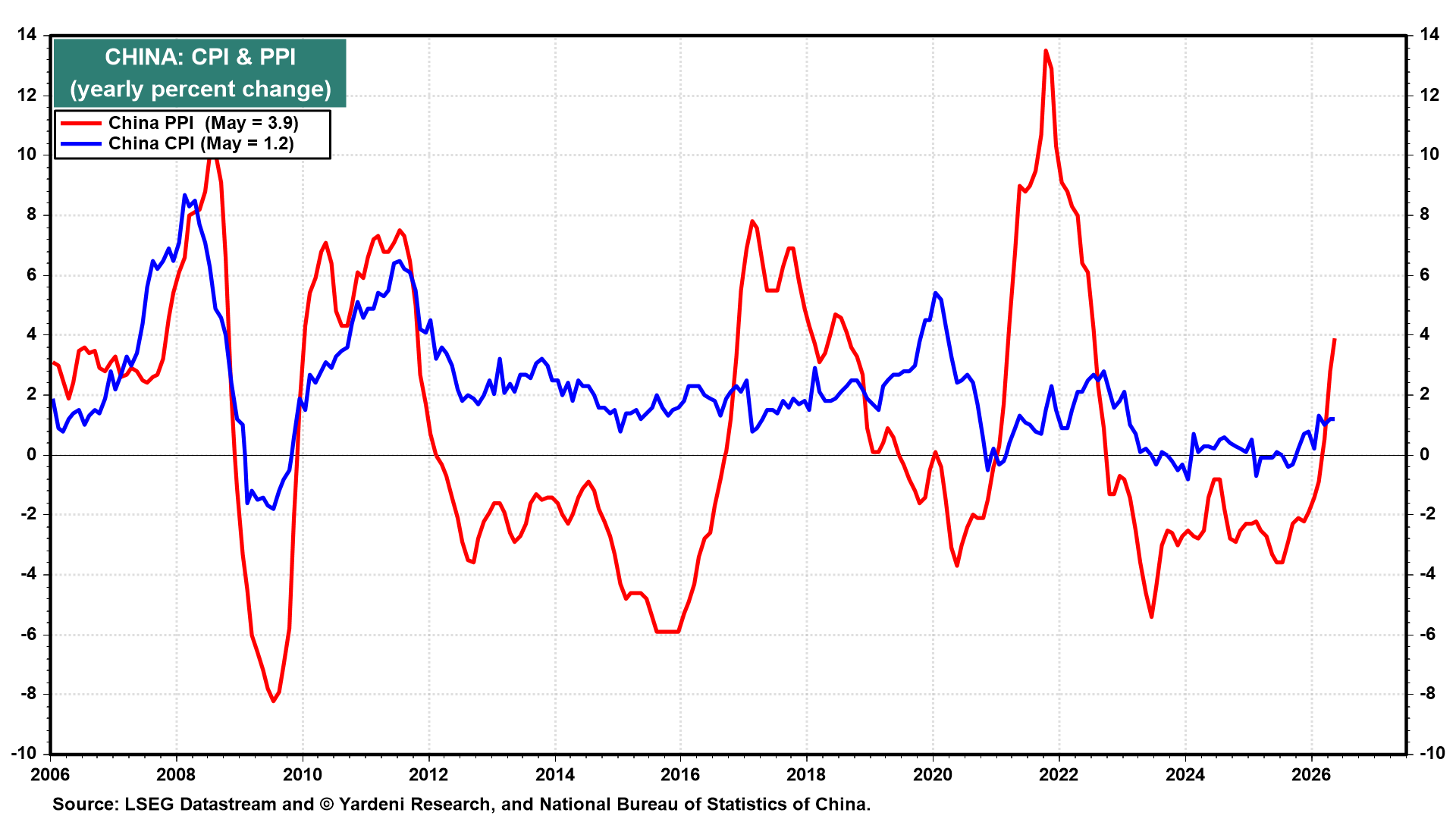

(5) Global Inflation. June's Eurozone PPI (Mon) is due to open the week’s international data. Japan’s PPI (Thu) accelerated to 6.3% y/y in May, the fastest pace since 2023 (chart). China’s PPI (Wed) rose to 3.9% in May from deeply negative readings a year ago, while the CPI stayed muted at 1.2%. Both probably moderated in June along with falling oil prices.