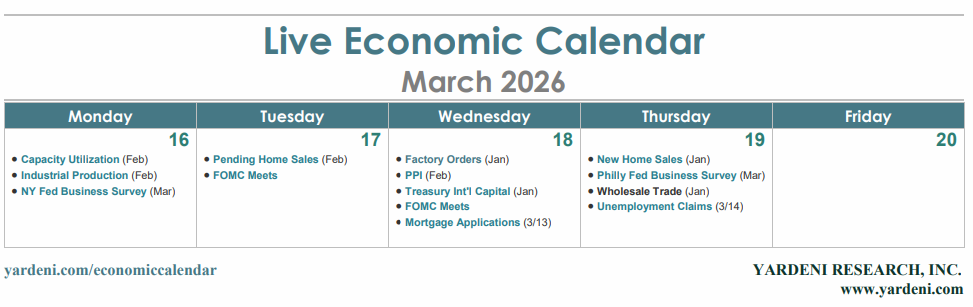

This week, many of the world’s top central banks have their first crack at responding to skyrocketing oil and gas prices driven by the war in the Middle East.

Along with hearing from the Fed (Wed), we’ll get rate decisions from the European Central Bank (Thu), the Bank of Japan (Thu), the Bank of England (Thu), the Bank of Canada (Wed), the Swiss National Bank (Thu), Sweden’s Sveriges Riksbank (Wed), and the Reserve Bank of Australia (Tue).

Though surprises are always possible, none of these monetary authorities is expected to adjust official rates. The preference is to wait and see how the war in Iran develops. Any signs that the conflict might drag on for some time, or that the resulting surge in oil prices is accelerating, could change the interest-rate calculus in the coming weeks and months.

News on Friday, for example, that US forces struck military targets on the vital Kharg Island and threatened to extend attacks to Tehran’s energy infrastructure might not sound promising to investors betting on a short conflict. With oil prices above $100 per barrel, any developments that affect transit through the Strait of Hormuz are likely to be big market movers.

In the interim, markets will pay closer attention to central bank statements and press conferences. Especially at the Fed, where Chair Jerome Powell will preside over his second-to-last Federal Open Market Committee (FOMC) meeting in his term. The Fed will release updated projections of FOMC participants' future expectations for rates, inflation, and the labor market.

Here are the economic releases most likely to affect the Fed’s next move — and when:

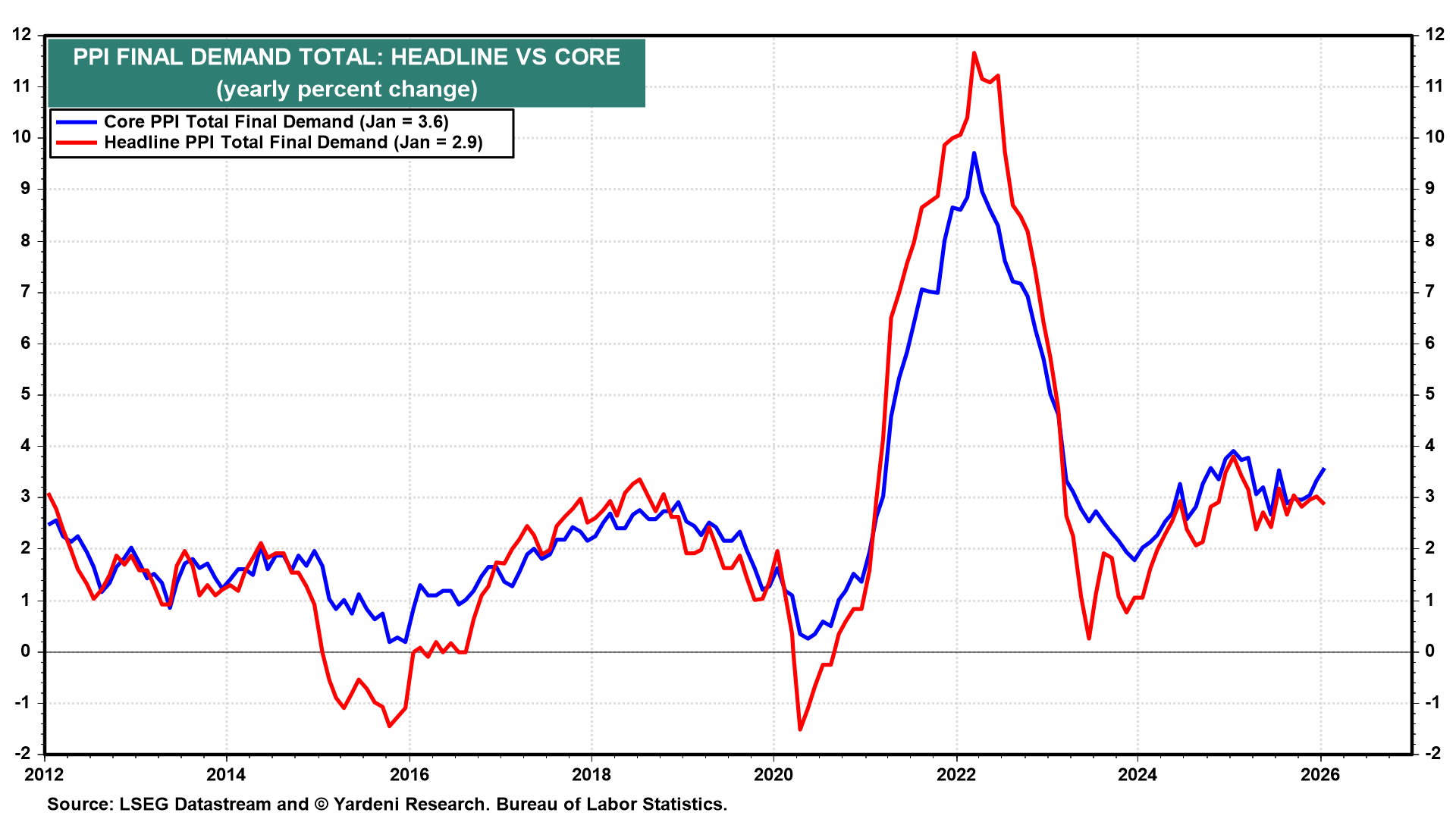

(1) PPI: January's hotter-than-expected producer price inflation rate (Wed) was a head-turner for Wall Street. Following that 0.5% m/m (3.6% y/y) jump amid higher service costs, economists expect a somewhat tamer 0.3% increase in February (chart).

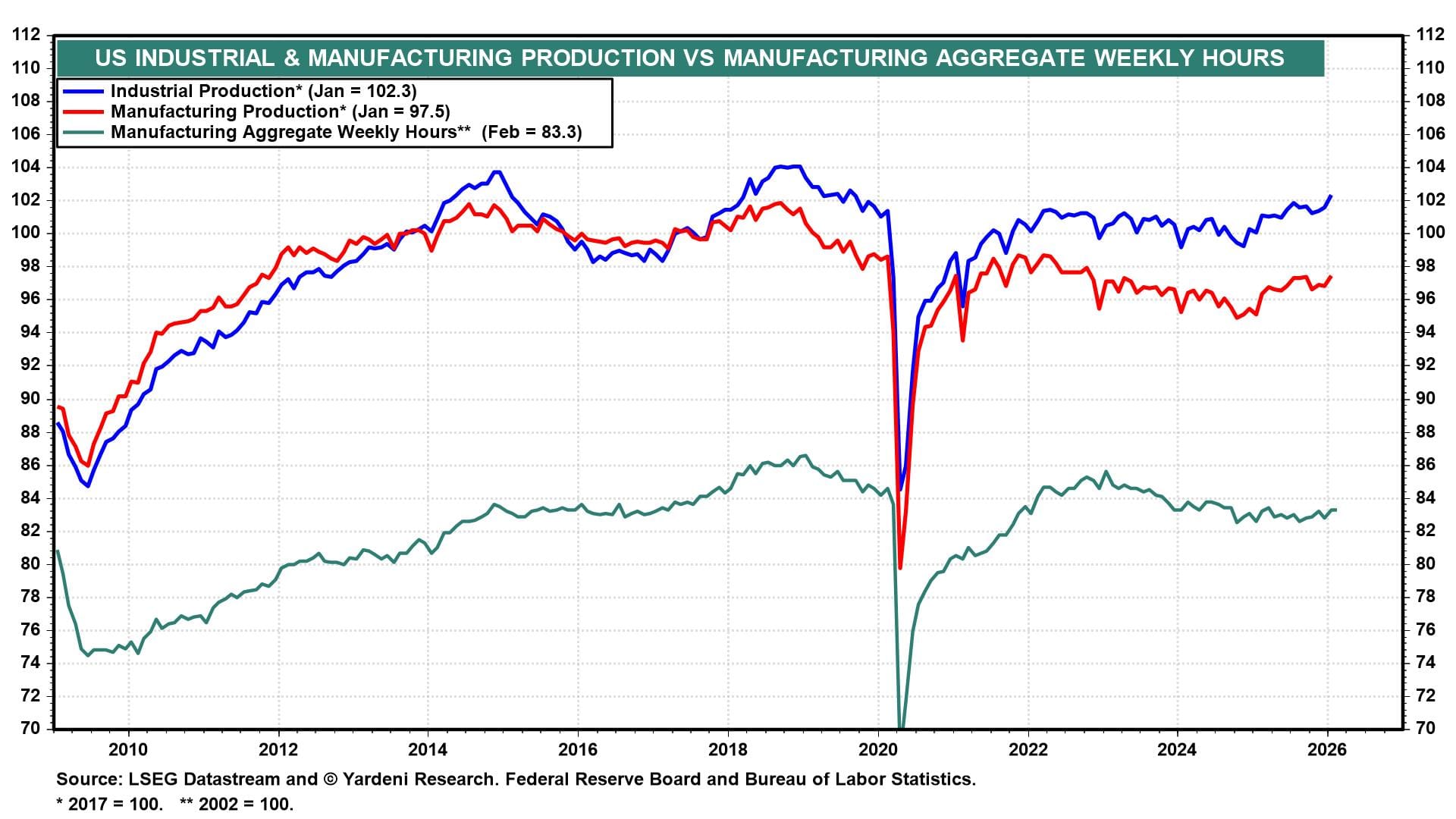

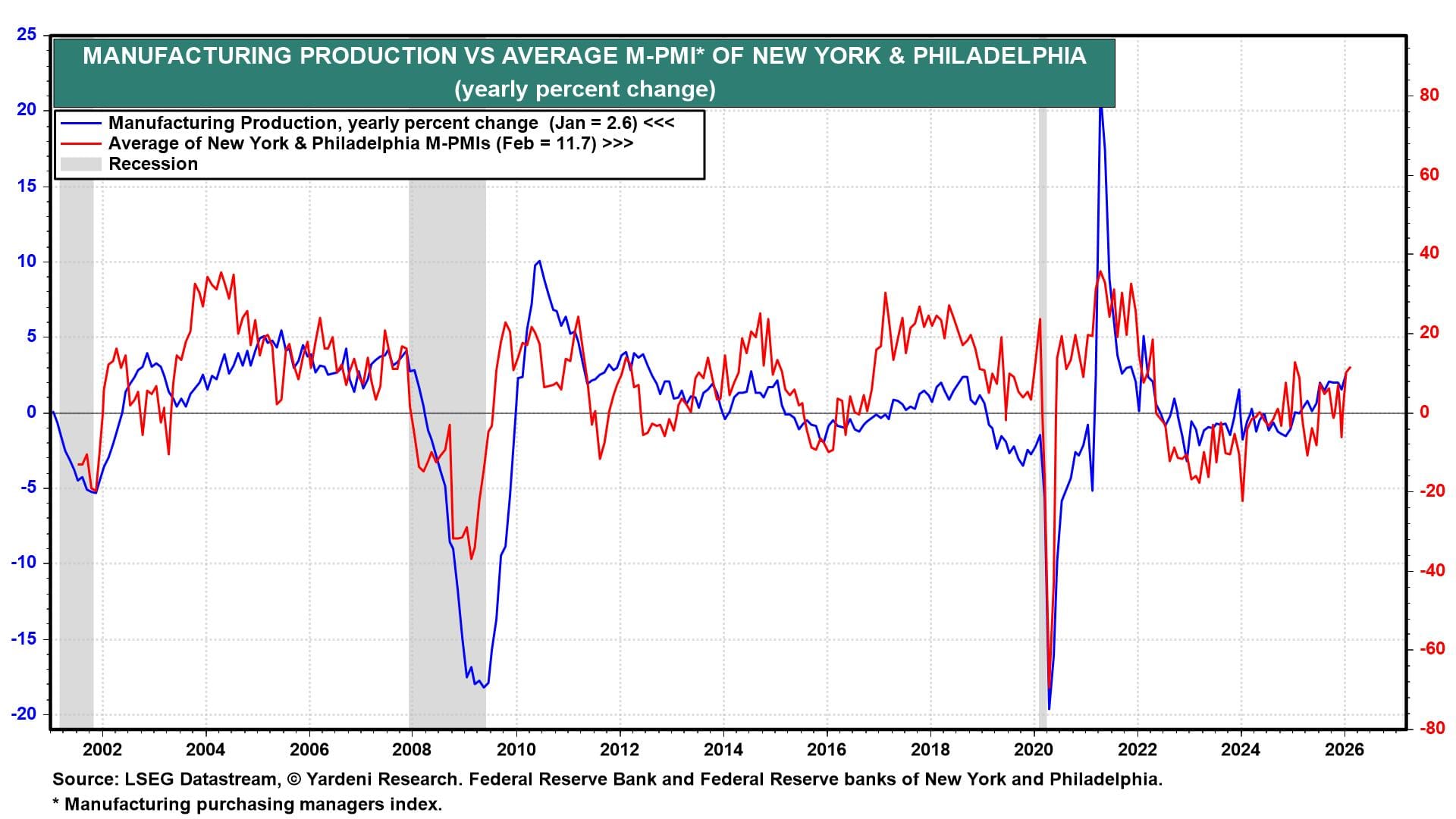

(2) Industrial production. Fed officials on the lookout for signs the economy is holding its own found them in January's industrial production (+0.7% m/m) and capacity utilization (76.2%, the highest since July) data. The February data (Mon) should confirm that industrial production remains on a modest uptrend (chart).

(3) Fed regional business surveys. The regional Fed business surveys could offer timely reality checks on where the economy stands. The New York Fed survey (Mon) starts the week, followed by the Philly Fed (Thu).

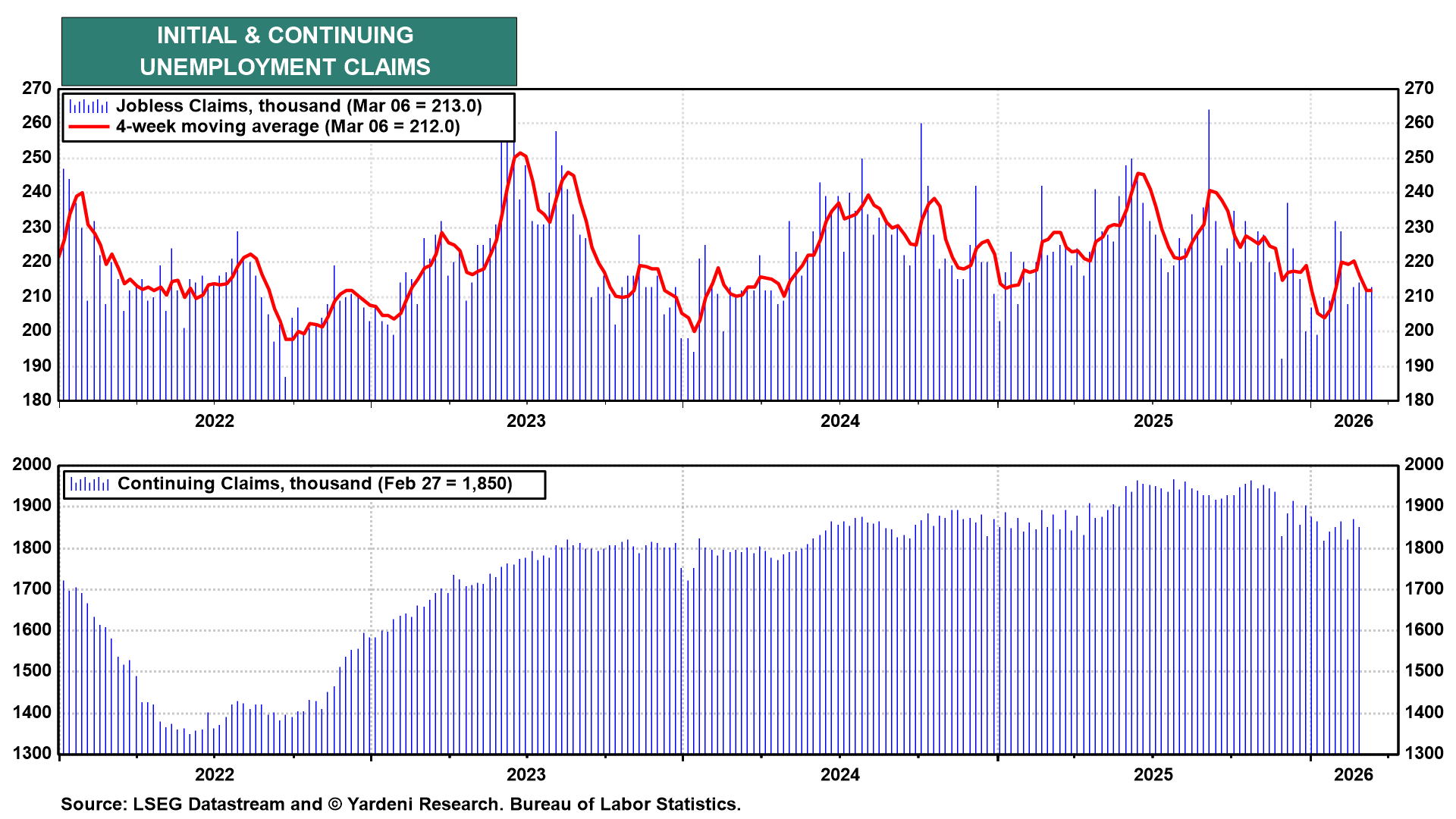

(4) Weekly claims. For all the handwringing about the slowing US labor market, the stability of weekly initial unemployment insurance claims (Thu) continues to show that layoffs aren’t surging as markets had feared. Should the latest data, for the week ended March 13, stay near last week’s 213,000 level, it would bolster the argument for steady Fed policy.