The week ahead is all about oil prices. As the Iran war enters its fourth week, the soaring price of crude has rapidly upended economic forecasts and shifted expectations for central bank policy.

Nowhere more so than at the Fed. In barely a week, bond traders have swung from expecting rate cuts to pricing in roughly a 50% probability of a tightening move by October. In Europe, the financial markets are now pricing in as many as three ECB rate hikes by year-end. The growing risk of a protracted Middle East conflict has put global monetary policy hawks firmly back in the ascendancy.

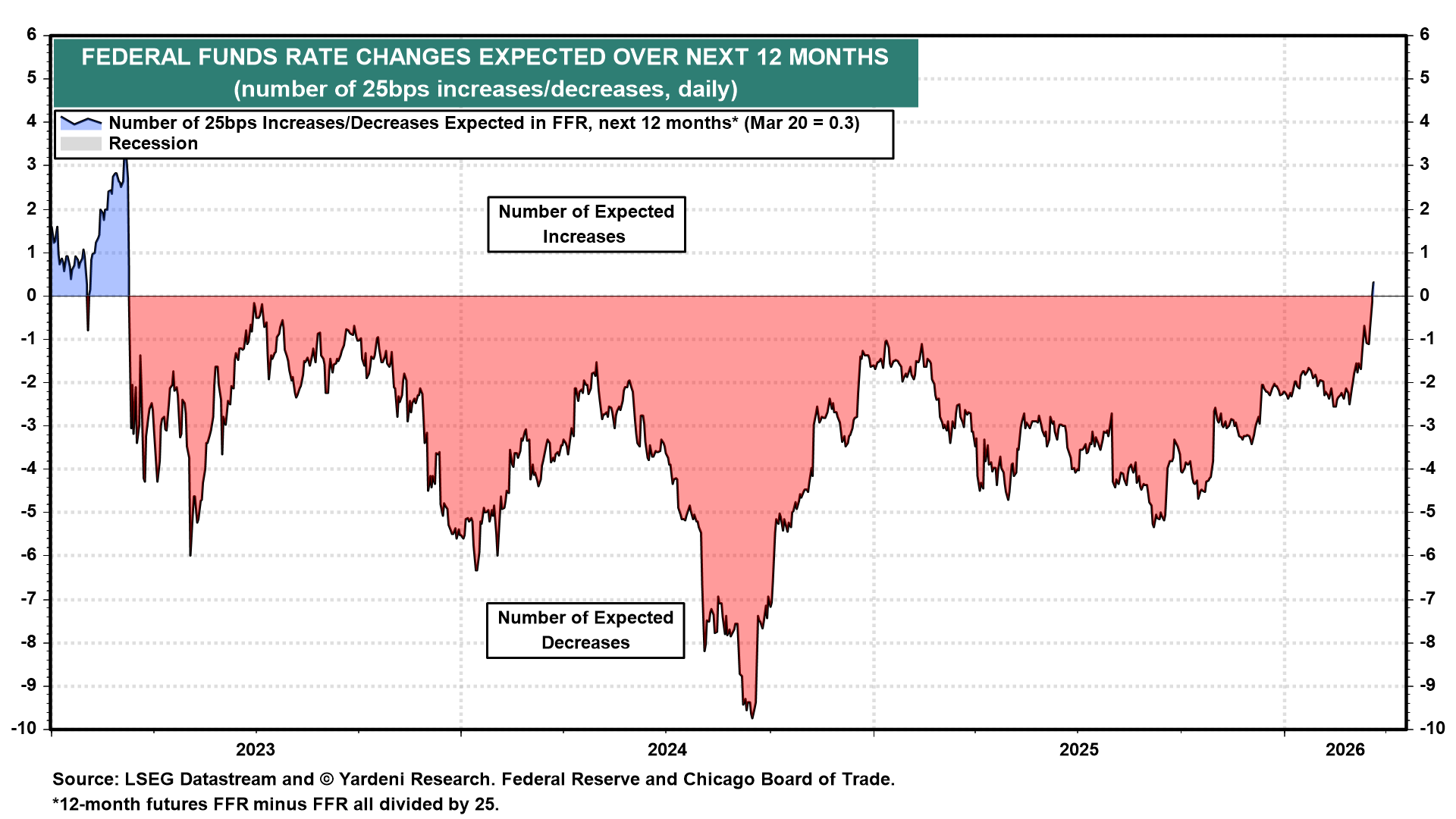

Following last week's Federal Open Market Committee meeting, Fed Chair Jerome Powell reiterated that further evidence of easing inflation is required before the Fed considers injecting liquidity into the economy. "If we don’t see that progress, then you won’t see the rate cut," he said. The federal funds futures market now implies no rate cuts over the next 12 months (chart).

In a relatively light week for major data, the financial markets will pay close attention to comments from Fed officials hitting the podium. Scheduled speakers include Governor Michael Barr (Tue, Thu) on the economic outlook, Stephen Miran (Wed, Thu) on digital assets and the Fed’s balance sheet, and Lisa Cook (Thu) on financial stability. They are joined by Governor Philip Jefferson (Thu), with San Francisco Fed President Mary Daly (Fri) and Philadelphia Fed President Anna Paulson (Fri) rounding out an already crowded slate of Fed commentary.

The war will remain front and center. Any further escalation involving the Strait of Hormuz, Iranian attacks, potential US boots on the ground, and attacks on energy and water infrastructure could drive significant market volatility. Over the weekend, tensions escalated further after US President Donald Trump, posting at 7:44 pm EST on Saturday, issued a 48-hour ultimatum for Iran to reopen the Strait of Hormuz, warning that the US would "obliterate" Iranian power plants if it failed to comply. So Apocalypse Now might or might not happen at 7:44 pm EST on Monday.

The price of Brent is relatively flat this evening, around $111 per barrel. The price of gold continued to decline to $4,325 per ounce at 8:52 pm, more than $200 below Friday's close.

Here are the US economic releases most likely to influence Fed thinking on the fallout from the war and the rate outlook this week:

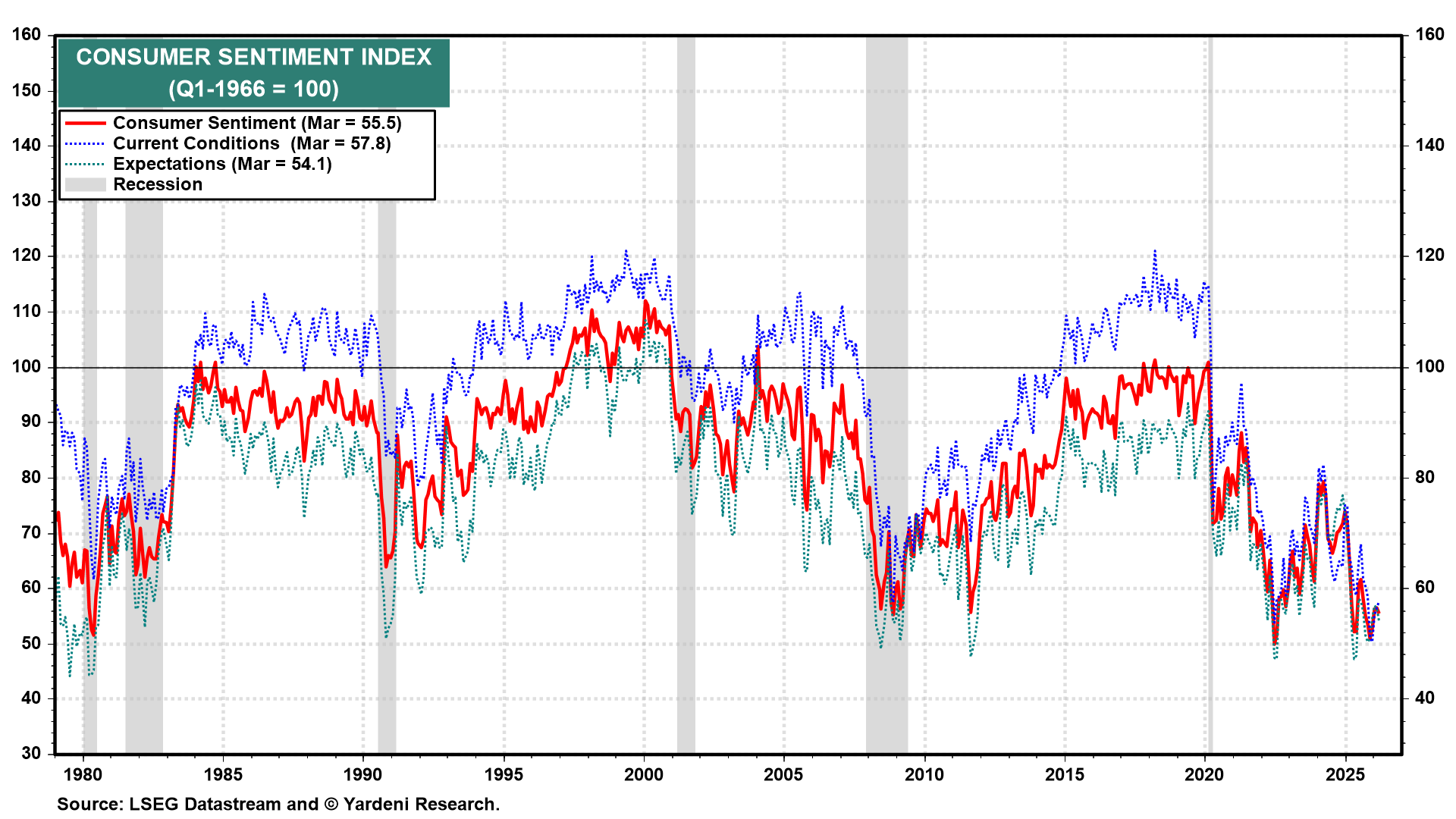

(1) Consumer sentiment. The University of Michigan will report its final March consumer sentiment index (Fri). The previous reading showed sentiment falling to 55.5 from 56.6 (chart). This week's update should show that surging gas prices are unnerving households around the country.

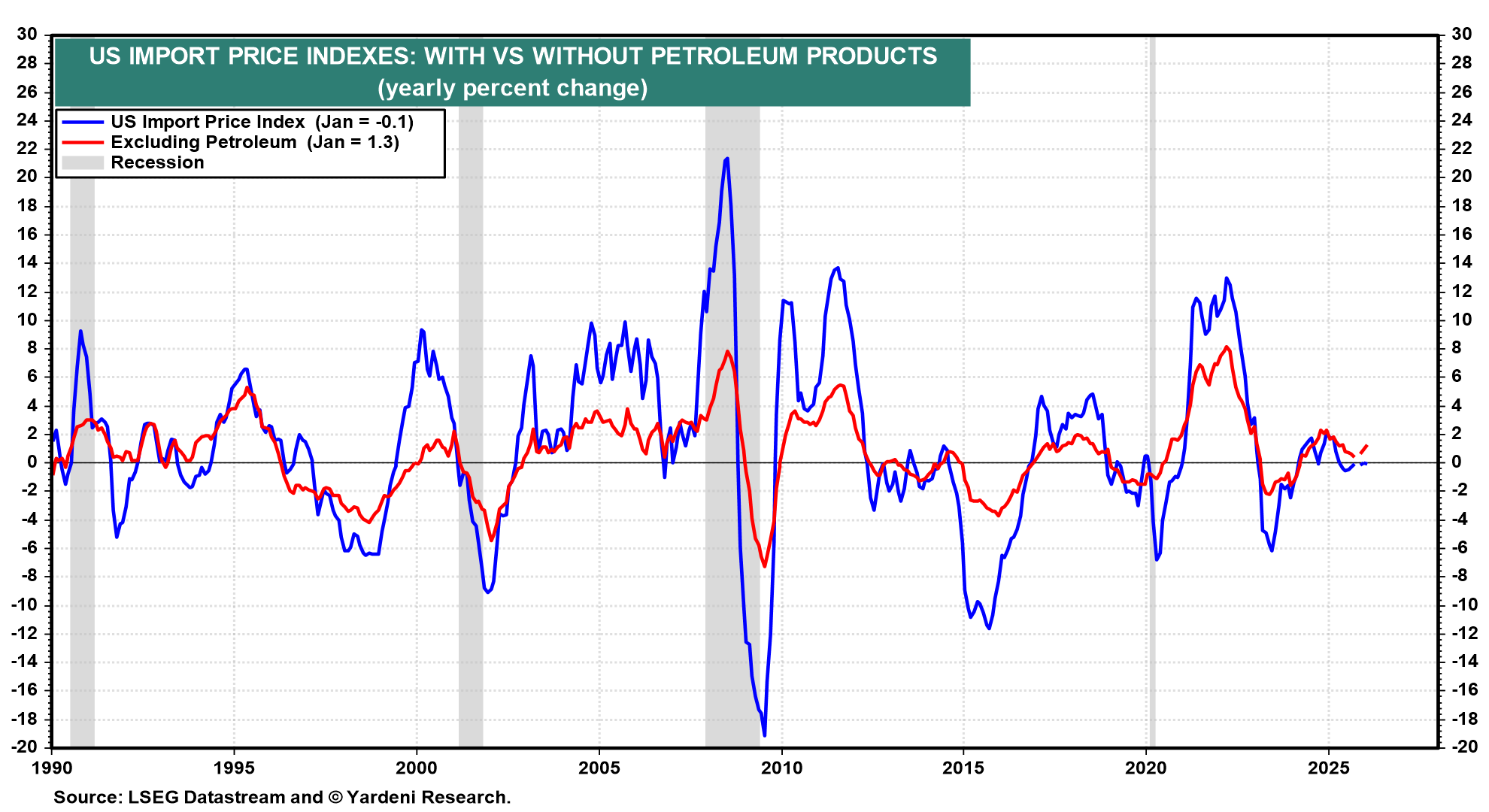

(2) Import/export prices. The February import price data (Wed) follows January's 0.1% m/m decline (chart). This is a pre-war report, so it won't reflect the jump in commodity prices during March. Q4 productivity and labor cost data (Tue) should confirm that both were disinflationary last year. We expect to see more of that in 2026.

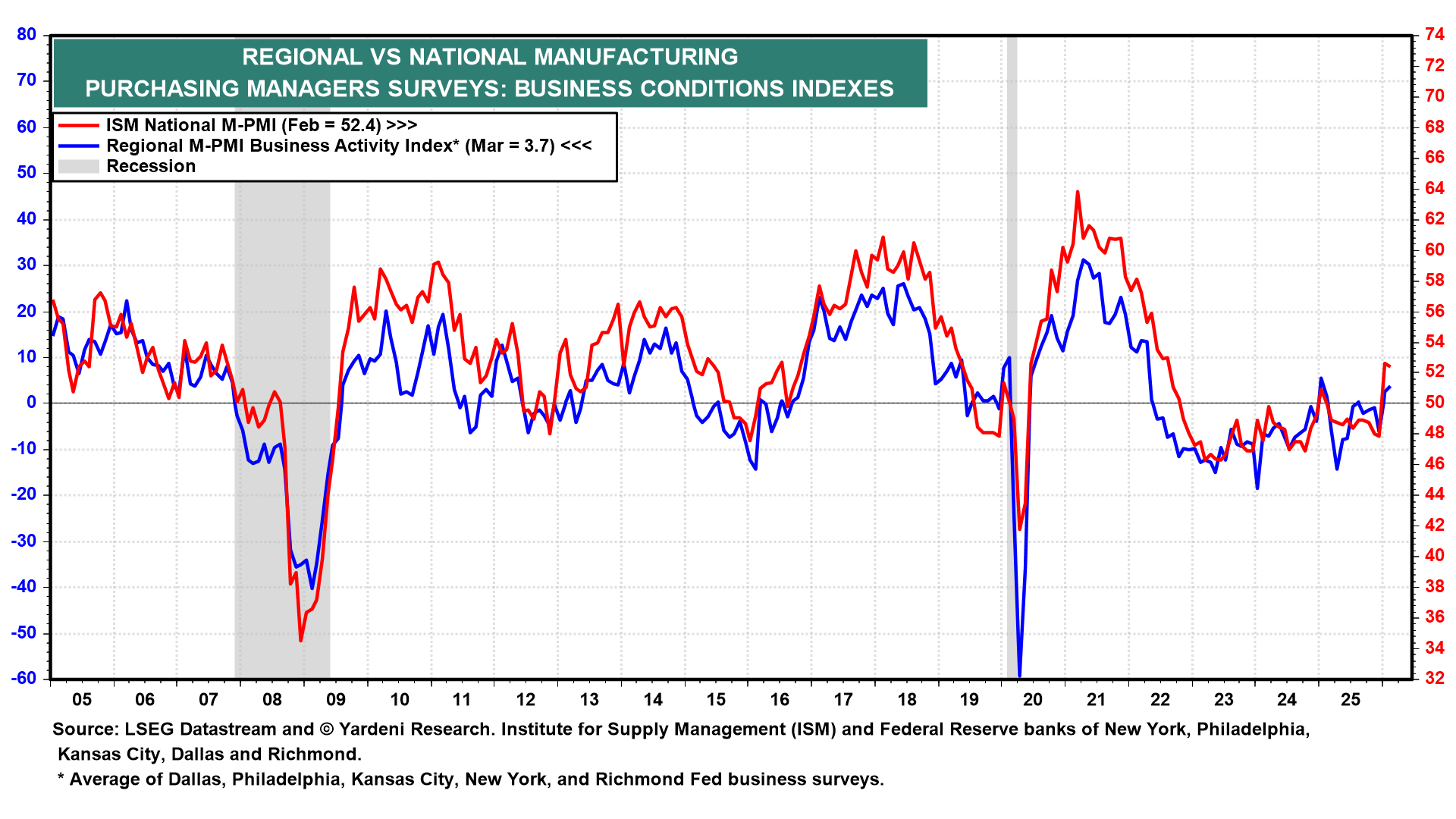

(3) Business surveys. At a moment when Fed officials are scrambling to keep up with economic zigs and zags, regional surveys should garner extra attention (chart). We'll hear from the Chicago Fed (Mon), the Richmond Fed (Tue), and the Kansas City Fed (Thu). Also, S&P Global releases its March purchasing managers' indexes (Tue) for both manufacturing and services. The impact of the war on the economy may become observable.

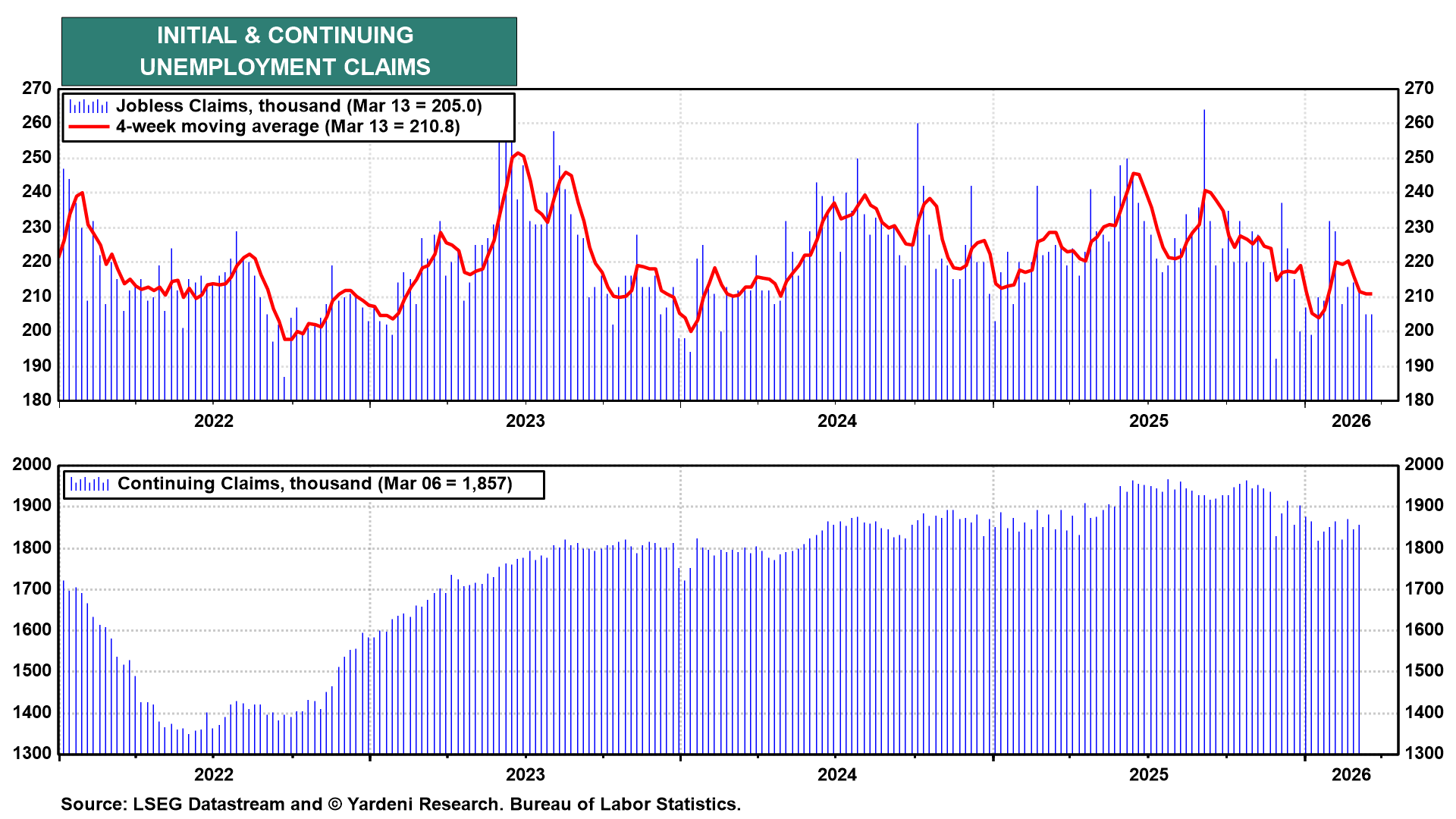

(4) Jobless claims. Weekly unemployment insurance claims remain upbeat, as claims continue to moderate (chart). Any reading in the neighborhood of last week's 205,000 level would confirm that layoffs remain low.