NEWS FLASH: President Donald Trump postponed Obliteration Day again today, until Monday, April 6 at 8:00 pm EST. He said he is granting a request from the Iranian government to extend the pause on potential airstrikes on Iran's power plants by an additional 10 days. That will prolong uncertainty and volatility in the financial markets.

It also means oil prices will remain elevated for at least another 10 days, unless there is a deal, exacerbating stagflationary pressures worldwide. Today, let's review developments in the Eurozone:

The latest energy crisis is hitting the countries of the European Monetary Union (EMU, or the Eurozone). In 2025, roughly 12% and 8% of the European Union's petroleum and gas imports originated in the Persian Gulf. Unlike the United States, which is an oil and gas exporter, the countries of the EMU are major energy importers. So a spike in energy prices hits the region harder, with higher inflation and weaker growth.

Now, the Eurozone economy is likely to experience a stagflationary bout similar to what happened in 2022 after Russia invaded Ukraine in February of that year, causing energy prices to soar back then too.

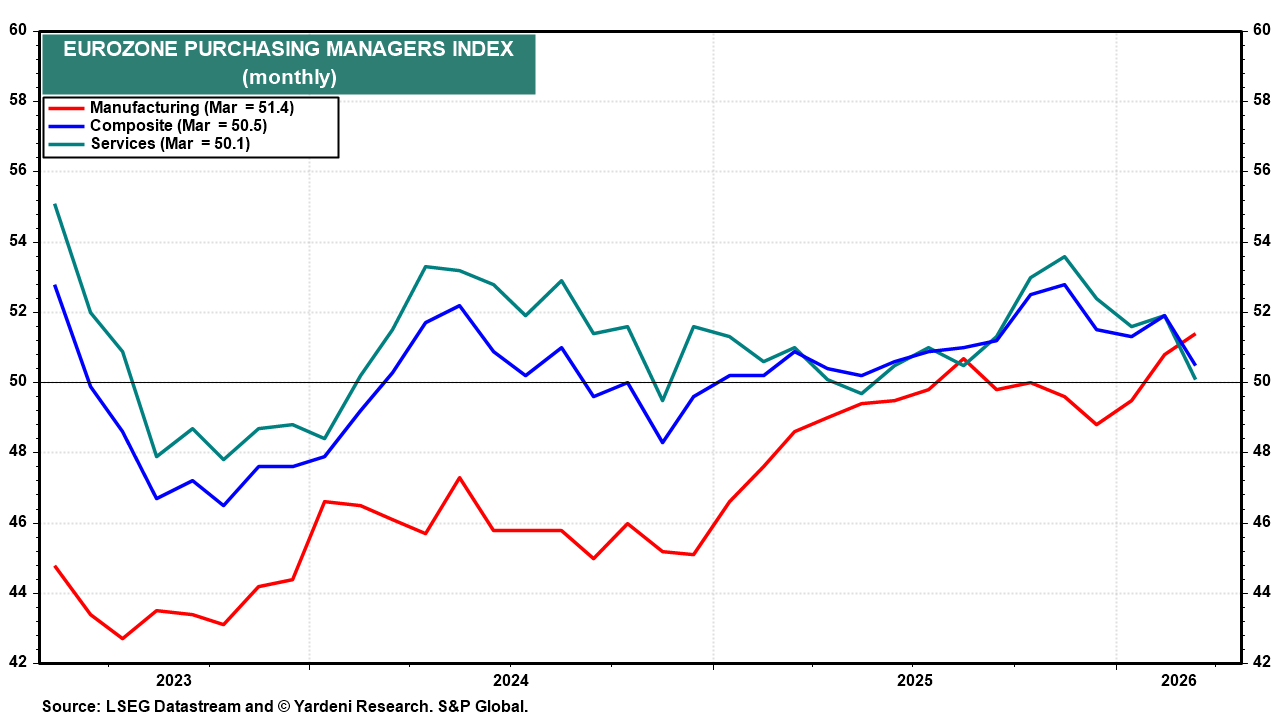

Before the war, which began at the end of February, the Composite PMI was 51.9 (chart). It fell to 50.5 in March, according to S&P Global. The Services PMI accounted for the decline, while the Manufacturing PMI continued to rise. Supply delays were reported by manufacturers more widely than at any time since October 2022. Average input costs rose at the fastest rate for 10 months. Higher costs were passed on to customers, resulting in the largest rise in selling prices in over three and a half years.

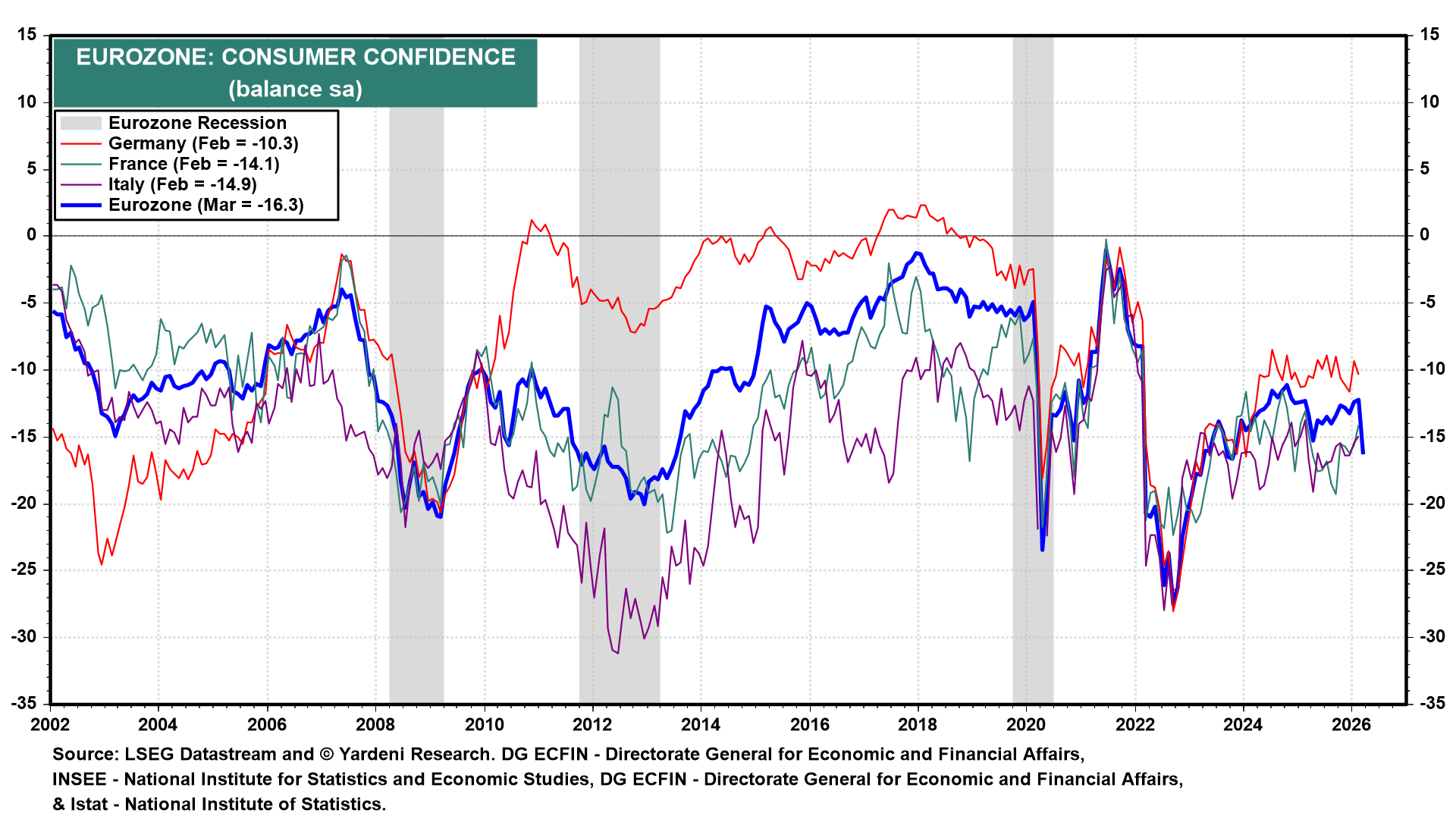

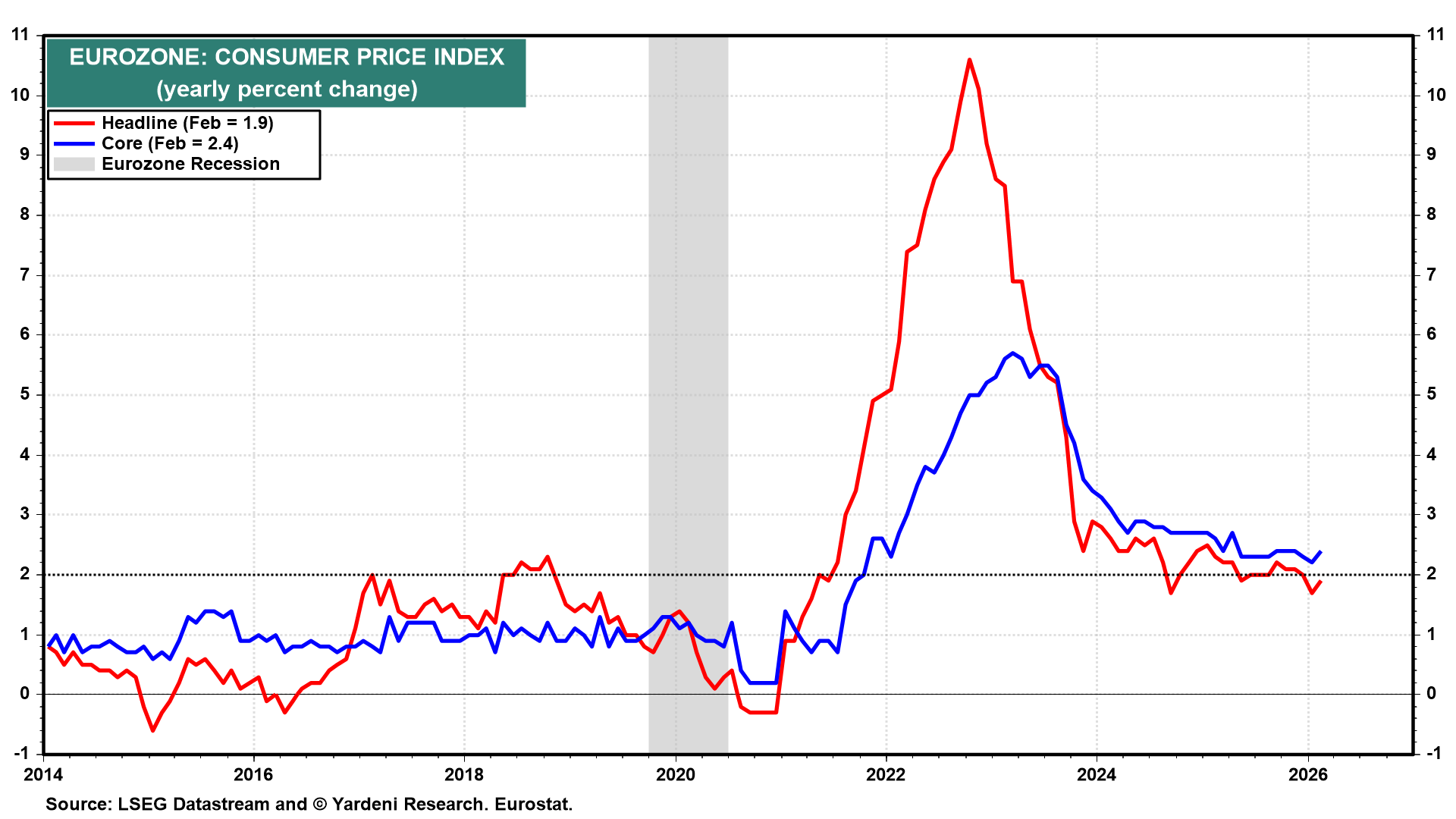

Eurozone consumer confidence dropped sharply in March (chart). An index of German consumer sentiment fell to its lowest in two years this month, and similar surveys in France and Italy also show growing unease. At the petrol stations, where the oil shock is felt most immediately by consumers, the cost of a 50-litre tank of diesel in Germany has risen by over €21 compared to the week before the war.

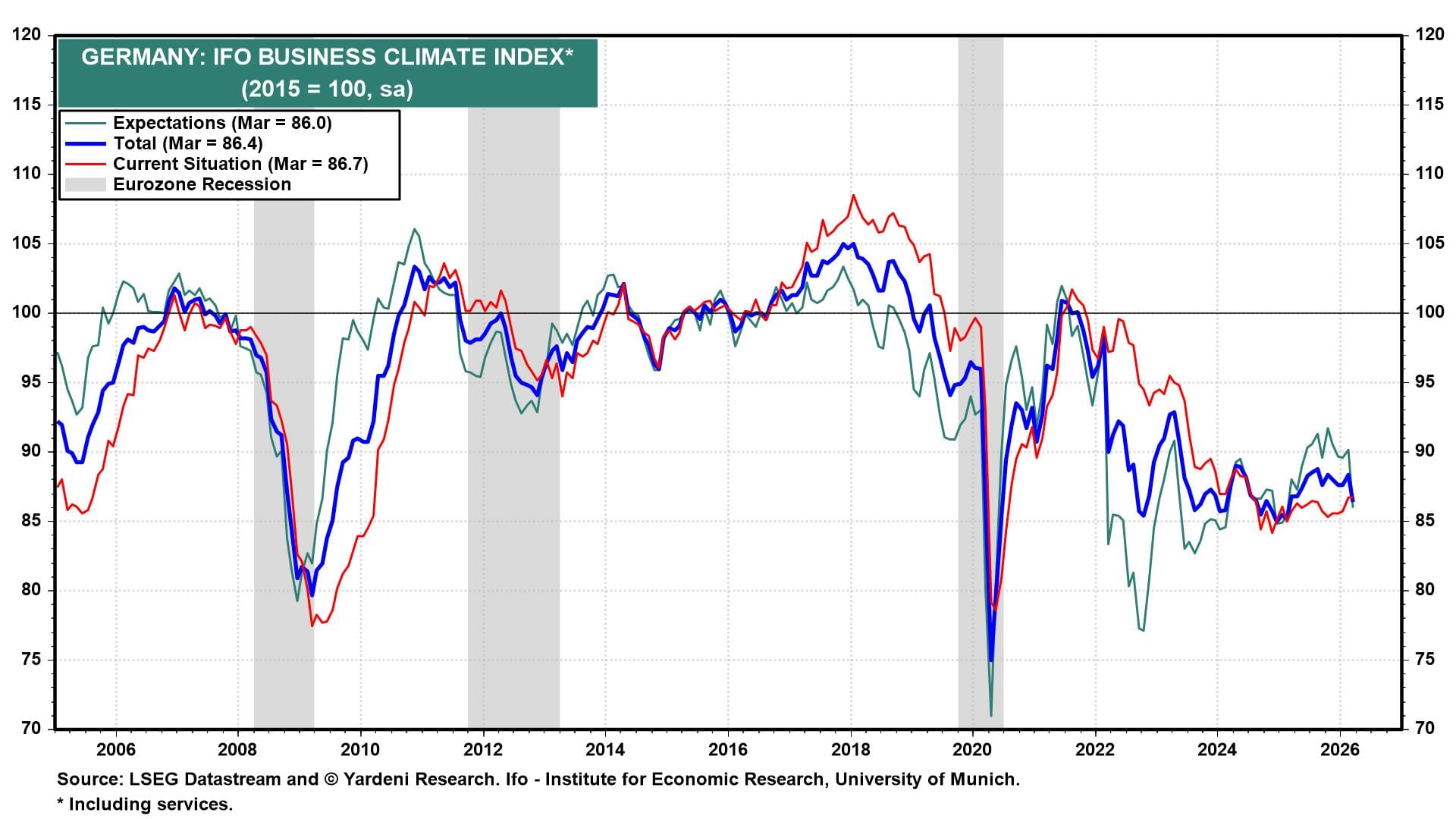

The March reading of Germany's Ifo Business Climate Index fell, led by a sharp drop in expectations (chart). Deutsche Bank has cut its German growth forecast for 2026 from 1.5% to 1.0%, warning that surging energy prices will weigh on the trade balance, dampen consumer spending, and exacerbate existing competitiveness challenges for the German industry, which already faced structurally uncompetitive energy costs before the oil-price shock.

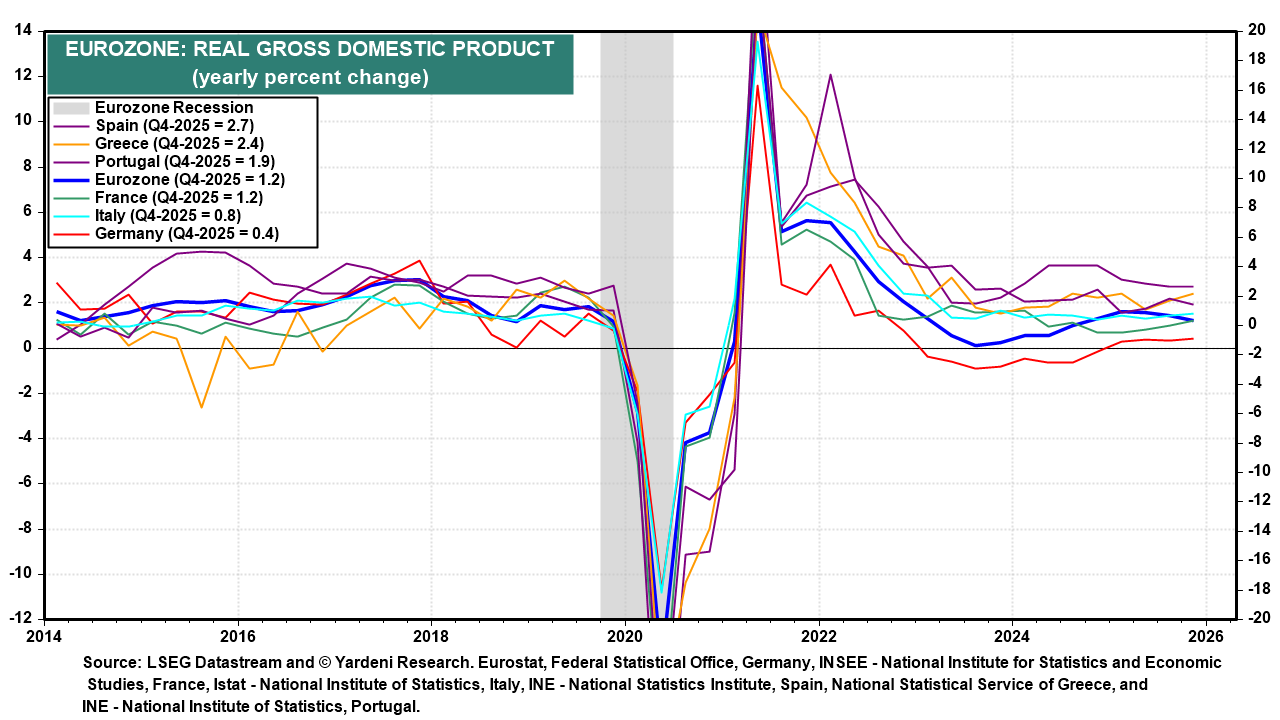

Other available economic indicators are pre-war. The Eurozone's real GDP rose 1.3% y/y through Q4-2025 (chart).

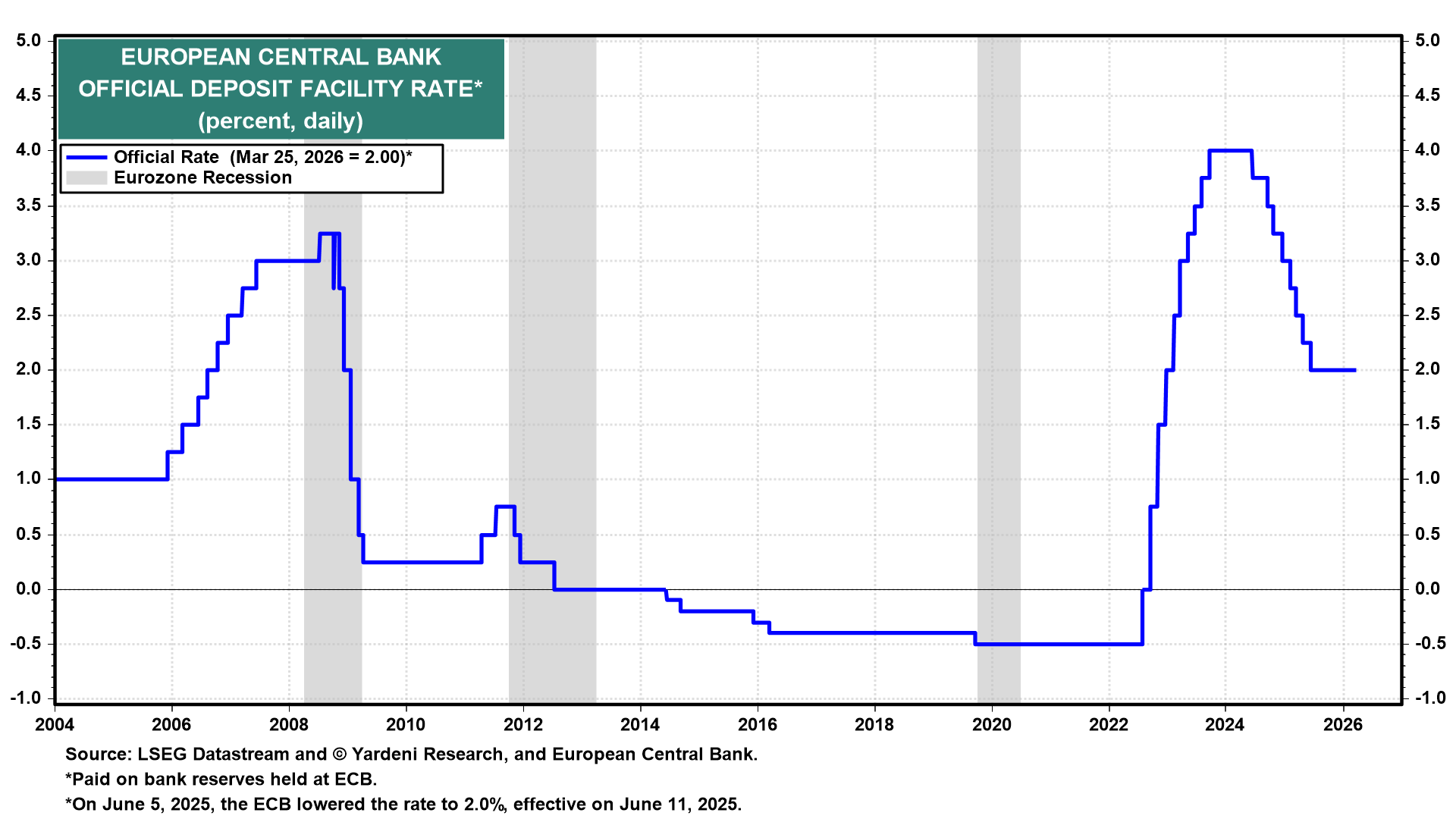

The European Central Bank (ECB) had cut its official deposit rate eight times since June 2024, bringing it to 2.00%, and further easing was likely this year (chart). The ECB has made clear that it won't let a new energy-led spike in inflation take root in the Eurozone, strongly hinting at interest-rate hikes in the coming months.

Now the ECB—which has only one mandate, i.e., to stabilize inflation around 2.0%—is expected to raise interest rates to subdue the inflationary energy price shocks resulting from the war. The ECB probably intends to mitigate the severe inflationary consequences of the current energy price shocks, as occurred during 2022 and 2023 following Russia's invasion of Ukraine (chart).

The ECB's new staff projections see headline CPI inflation averaging 2.6% in 2026, revised up 0.7ppt from December. Real GDP growth has been cut to just 0.9%, down from 1.2% in 2025, reflecting stagflation's drag on real incomes, investment, and confidence.

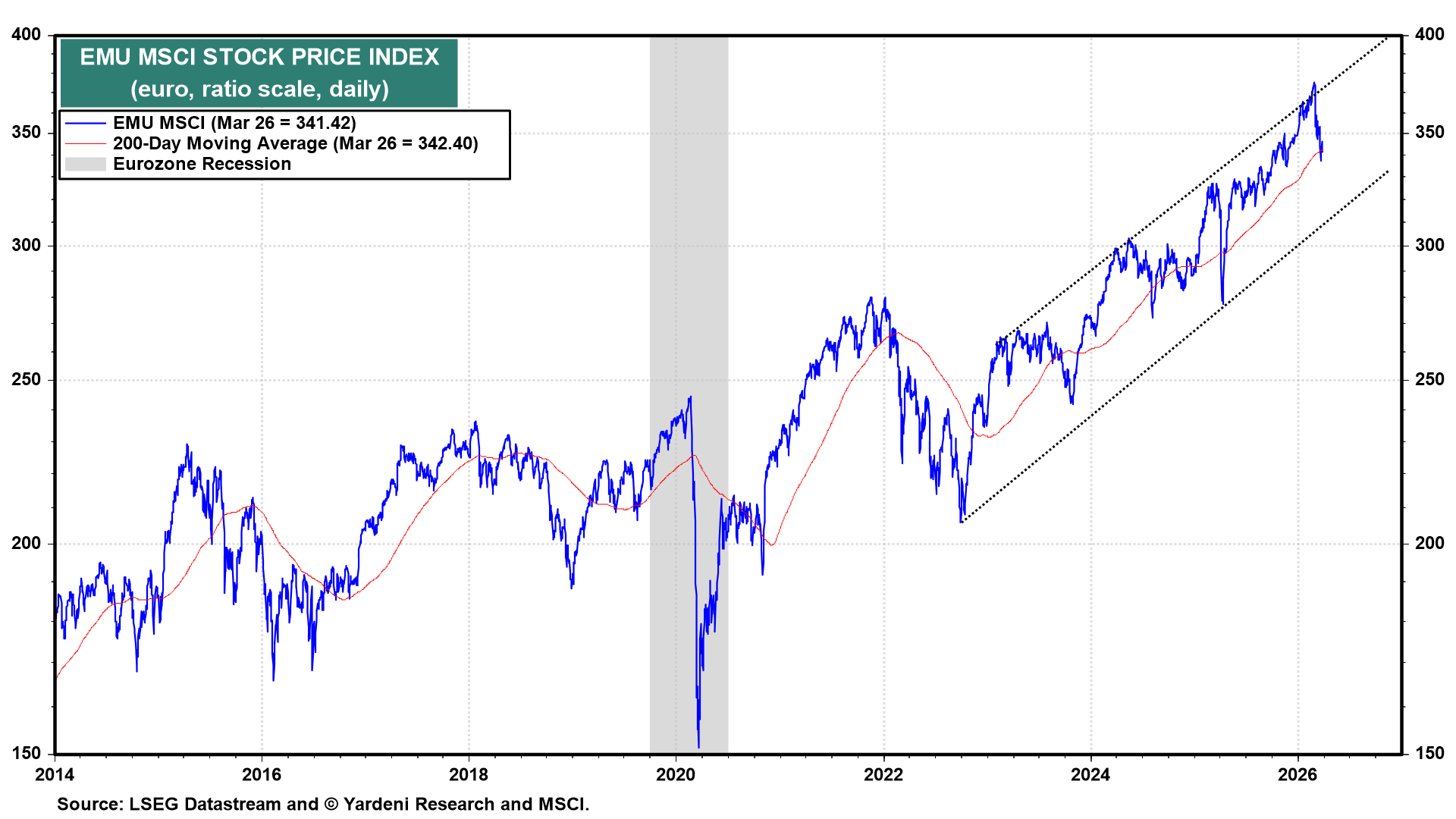

Financial markets now are pricing in one to two 25bps ECB rate hikes through the remainder of 2026, a significant reversal from expectations of further easing just a few weeks ago. As a result, the EMU MSCI stock price index in euros is down 8.7% from its record high on February 25, but may find support at its 200-day moving average (chart).

The share of investors overweighting European stocks dropped sharply from 35% to 21%, according to Bank of America's latest European fund manager survey. Stagflation is now "the consensus expectation" for the macro regime in the coming months, with the percentage of respondents expecting stagflation surging from 15% to 50% m/m, and expectations for European core inflation at their highest since 2022. The sectoral rotation shows that fund managers are rotating out of industrial stocks, previously seen as a key winner from Europe's reindustrialization ambitions, and into the more defensive basic materials and healthcare stocks.

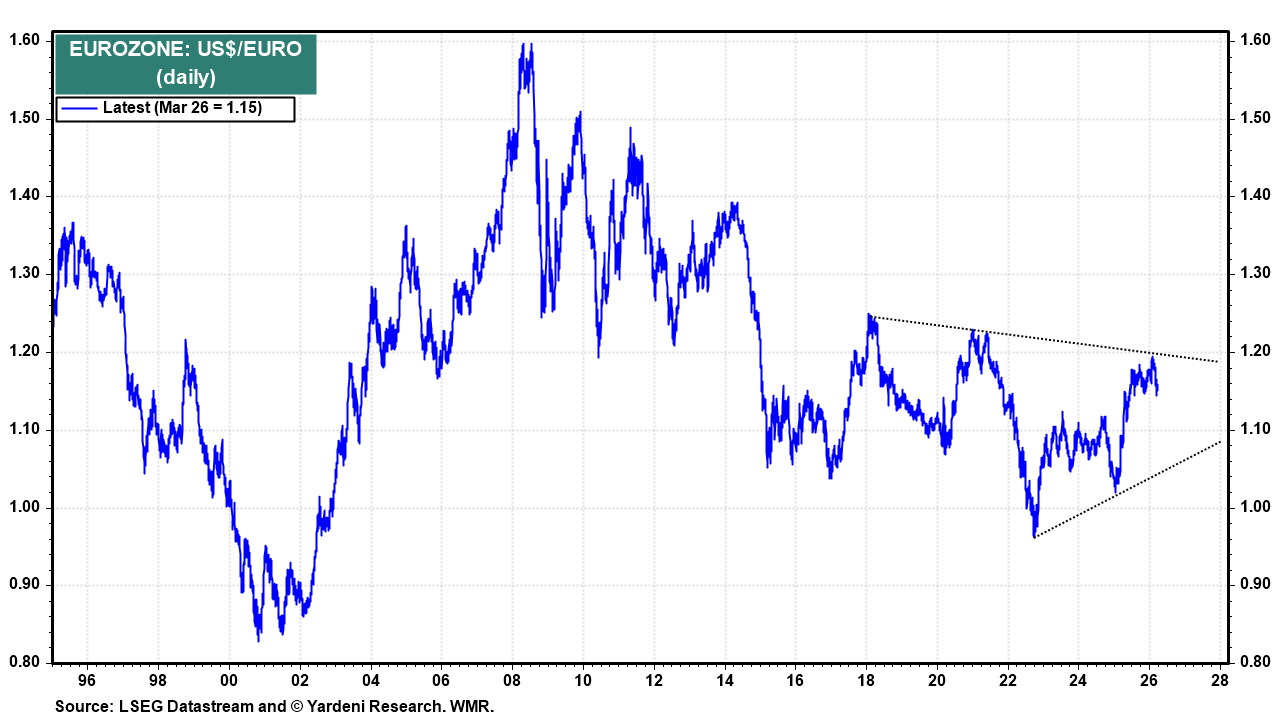

The euro has dropped from 1.1778 to 1.1457 against the dollar, making energy imports even more expensive for eurozone buyers (chart). An MSCI scenario analysis estimates that European equities could fall by as much as 16% in a sustained stagflationary shock. That would be a steeper drop than for US equities, reflecting Europe's structurally greater reliance on imported energy.

The key variable now is time. If the disruption in the Strait of Hormuz proves short-lived, the ECB can hold off on raising interest rates. If trouble persists, the ECB faces its most difficult policy dilemma since the 2022 energy crisis, this time with far less fiscal and monetary room to respond.