We've acknowledged that the odds of a Fed rate cut have increased since the release of July's cold employment report and July's lukewarm CPI report so far this month. But we've also noted that more economic indicators will be released before the next FOMC meeting in mid-September. So we haven't abandoned our increasingly contrary view that "none-and-done in 2025" is still a likely outcome for the Fed's rate cuts. That's because we haven't lost our confidence in the resilience of the economy nor in the FOMC's commitment to lower the inflation rate to 2.0% y/y.

Today's PPI and unemployment claims reports confirmed our position. Consider the following:

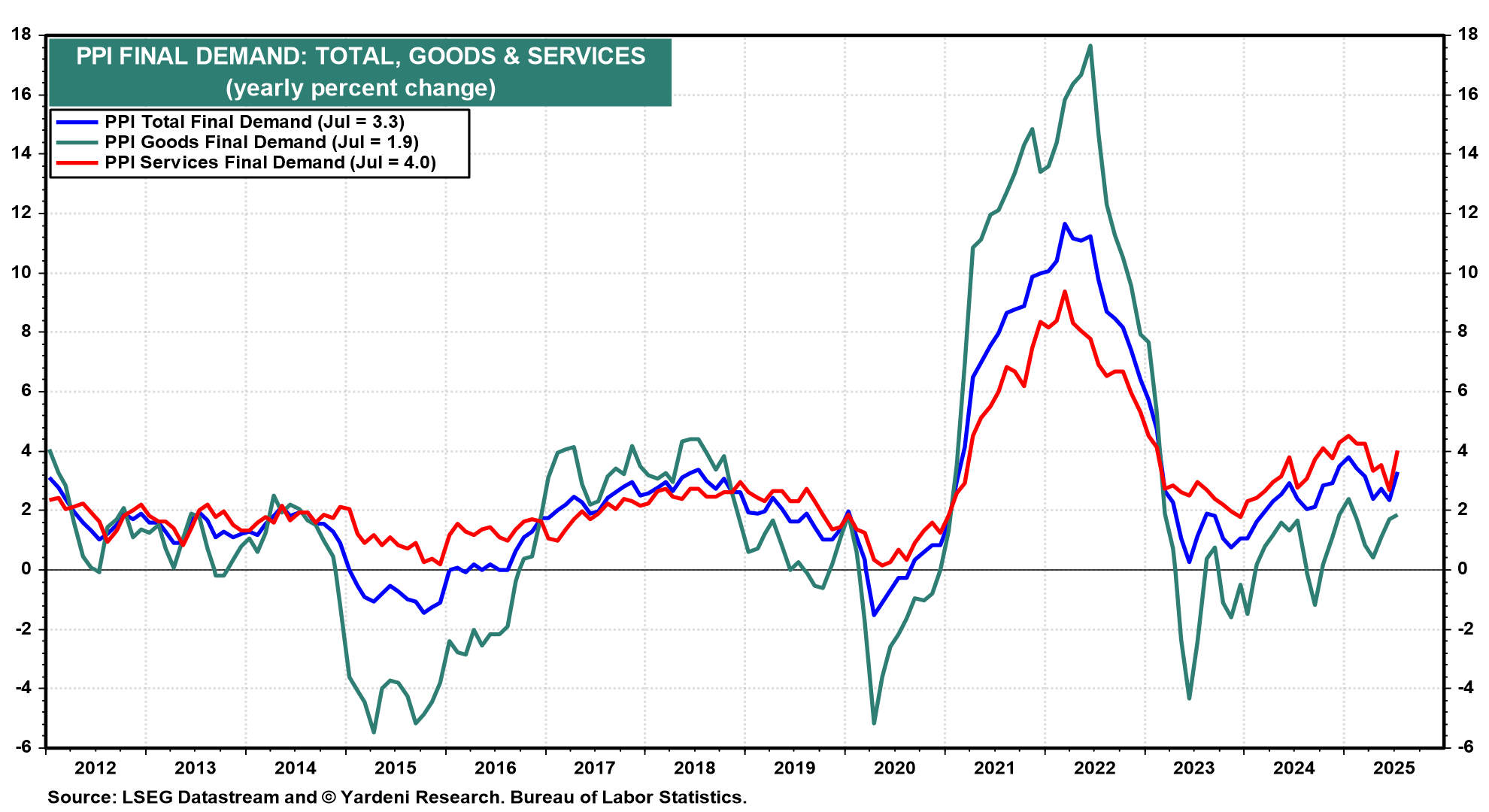

(1) PPI for final demand. The Producer Price Index for final demand rose 0.9% m/m in July. It advanced 3.3% y/y, the most significant 12-month increase since rising 3.4% in February 2025 (chart). This greater-than-expected increase was not directly attributable to tariffs because, unlike the CPI, the PPI does not include imports! But rising costs attributable to intermediate goods purchased by domestic producers (such as steel and aluminum) might have boosted the PPI. Then again, most of the rebound in PPI inflation during July was attributable to services (up 4.0%), not to goods (1.9%).