The US economy remains resilient, and so do corporate earnings. The US economy has passed several stress tests in recent years. The war in the Middle East is proving to be the latest stress test for the US economy, which seems to be passing it, so far. The macroeconomic data released in recent weeks confirms this resilience. The pre-war growth trajectory was solid enough that we were on the verge of raising our already bullish earnings estimates for 2026 and 2027. The war stopped us from doing that.

It seems Wall Street analysts haven't received the memo about the war. Their consensus estimates for S&P 500 revenues and earnings for this year and next year have been rising noticeably in recent weeks. We thought our pre-war estimates were bullish. The analysts are even more bullish. For now, we are sticking with our pre-war earnings forecasts, which support our 7,700 forecast for the S&P 500 by the end of this year. It could be higher if the analysts' estimates hold.

Consider the following:

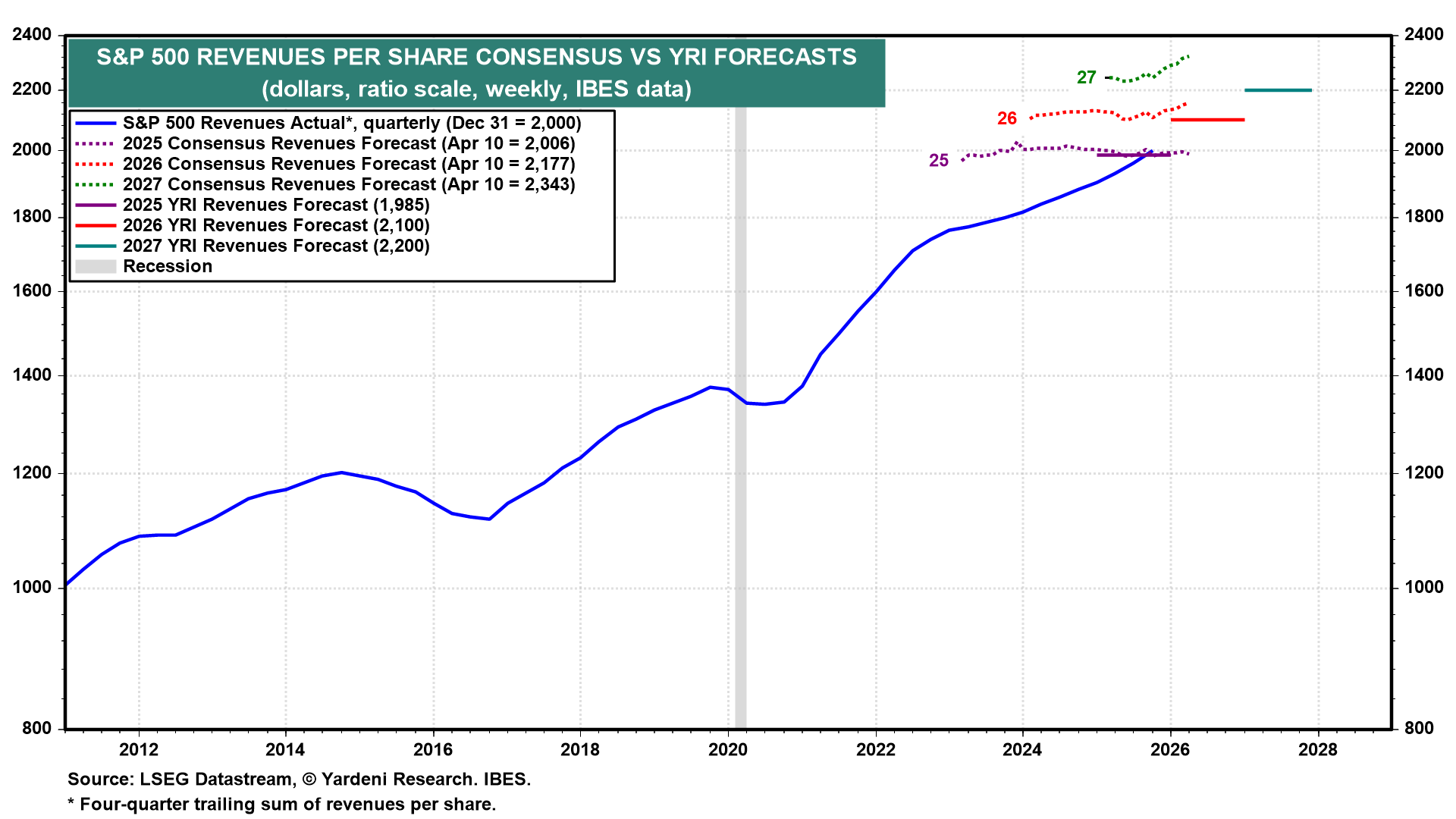

(1) RPS. The analysts' consensus estimates for 2026 and 2027 revenues per share (RPS) are very optimistic, with gains of 8.5% and 7.6% projected (chart). The average annual growth rate of RPS since 1993 is 4.3%, though that includes expansions and recessions.

(2) EPS. The analysts are similarly bullish about S&P 500 operating earnings per share (EPS). The consensus currently has 2026 EPS at $323.73 versus our estimate of $310. For 2027, the analysts’ current estimate is $377.94 versus our estimate of $350 (chart). They expect EPS to increase by 19.3% this year and 16.7% next year. The average annual growth rate of actual EPS since 1993 is 8.8%, including booms and busts.