I. Hot war with Iran and cold war with China

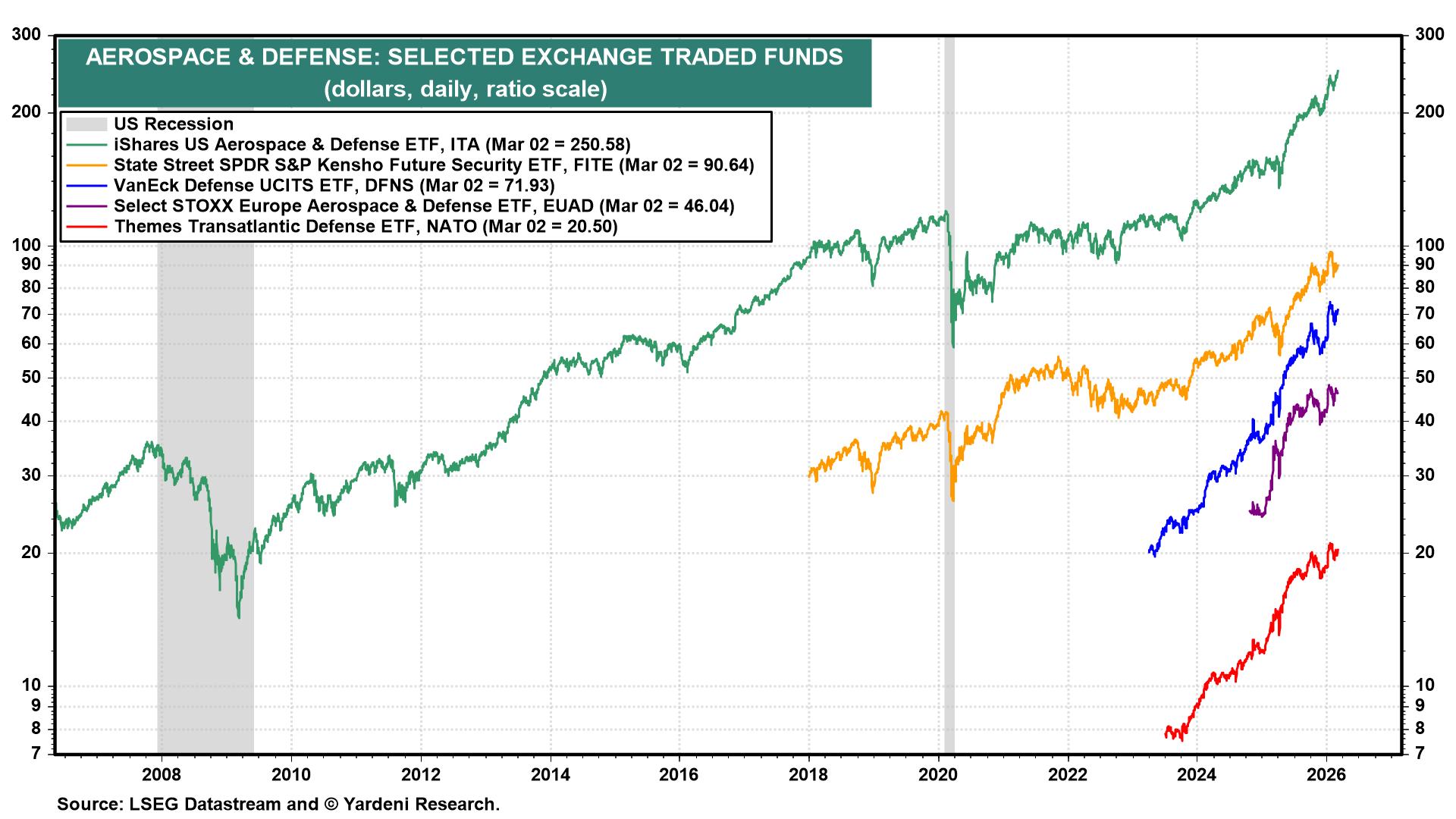

We remain in the short-war camp on the outlook for the current conflict in the Middle East. The stock market seems to agree, since it barely budged today, though defense stocks rose significantly (chart).

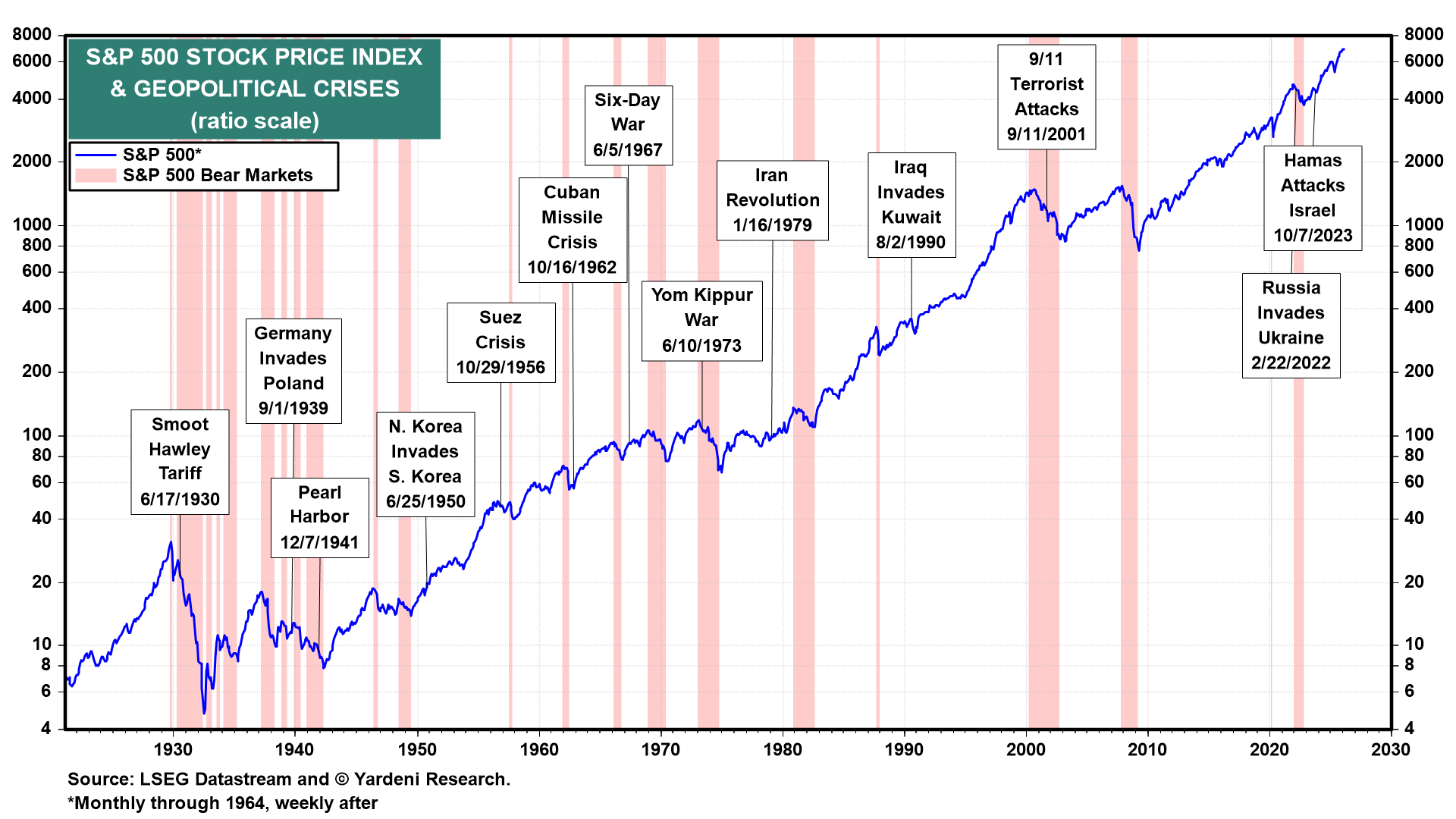

Geopolitical crises tend to create buying opportunities in the stock market (chart). The problem is that everyone knows that, which diminishes the magnitude of opportunities!

Following the assassination of Supreme Leader Ali Khamenei on February 28, Iran has activated a constitutional transition mechanism known as the “Interim Leadership Council” (or “Council of Three”). They represent the political, judicial, and clerical power centers and must nominate a new Supreme Leader. The new chosen one had better be ready to follow the commands of the White House or meet the same fate as his predecessor. Iran's foreign minister admitted that the country's attacks on neighboring countries are literally out of control: Soldiers in the field have no command structure and are just following the last orders they received before their top commanders died.

America's recent military actions in Latin America and Iran are designed to check China's ambitions to dominate these regions. China imports lots of oil from Venezuela and Iran and has invested significantly in both countries. A stable Middle East would allow the US to position more of its military might in the Pacific and frustrate China's plans to invade Taiwan.

II. US manufacturing showing more signs of life

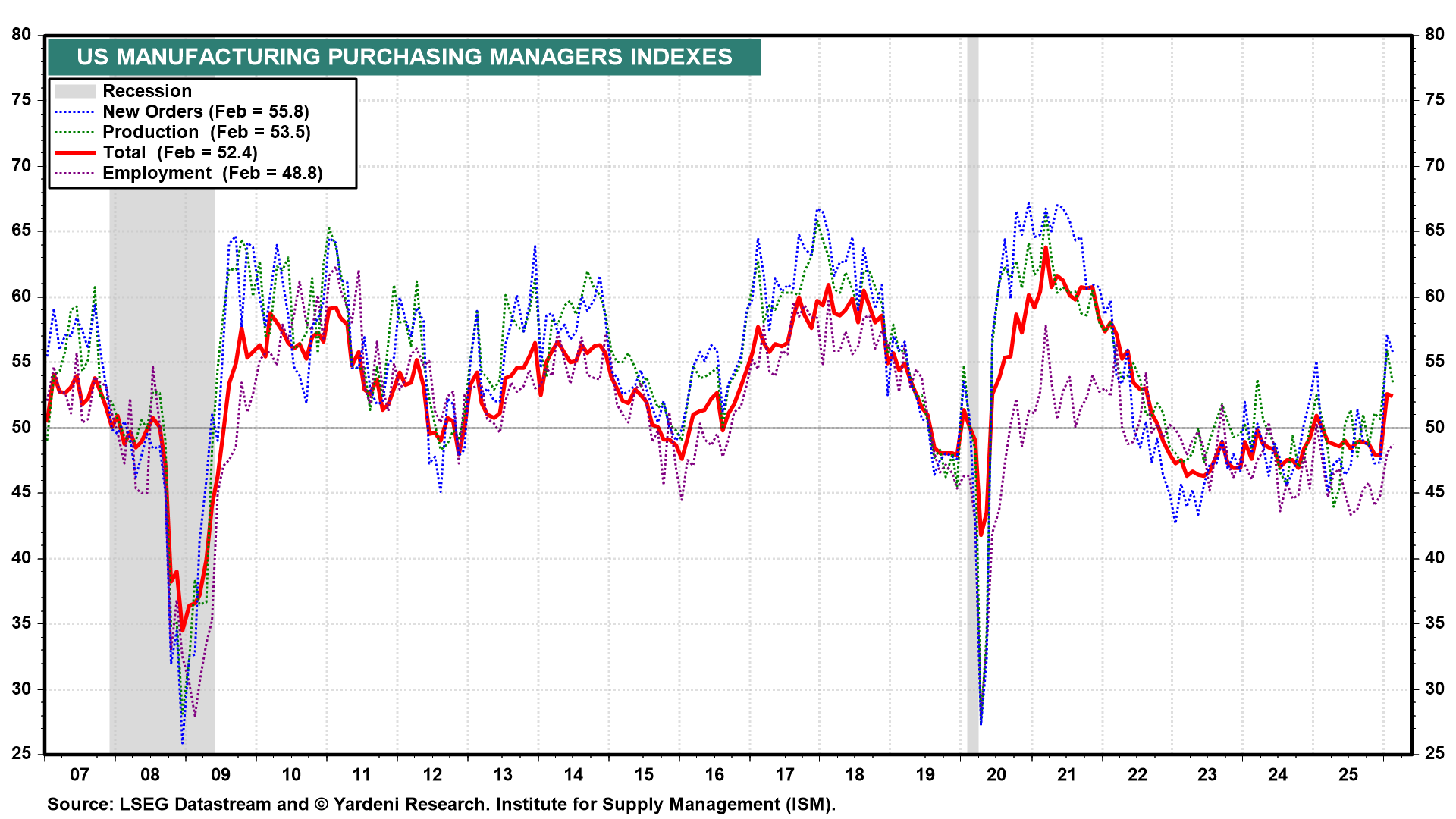

Here at home, the US economy has been remarkably resilient in recent years despite weakness in manufacturing, which is finally showing signs of revival. The ISM Manufacturing PMI (M-PMI) has found its footing after a long stretch of sluggishness. The most recent reading for February 2026 came in at 52.4%, following a very strong January reading of 52.6% (chart).

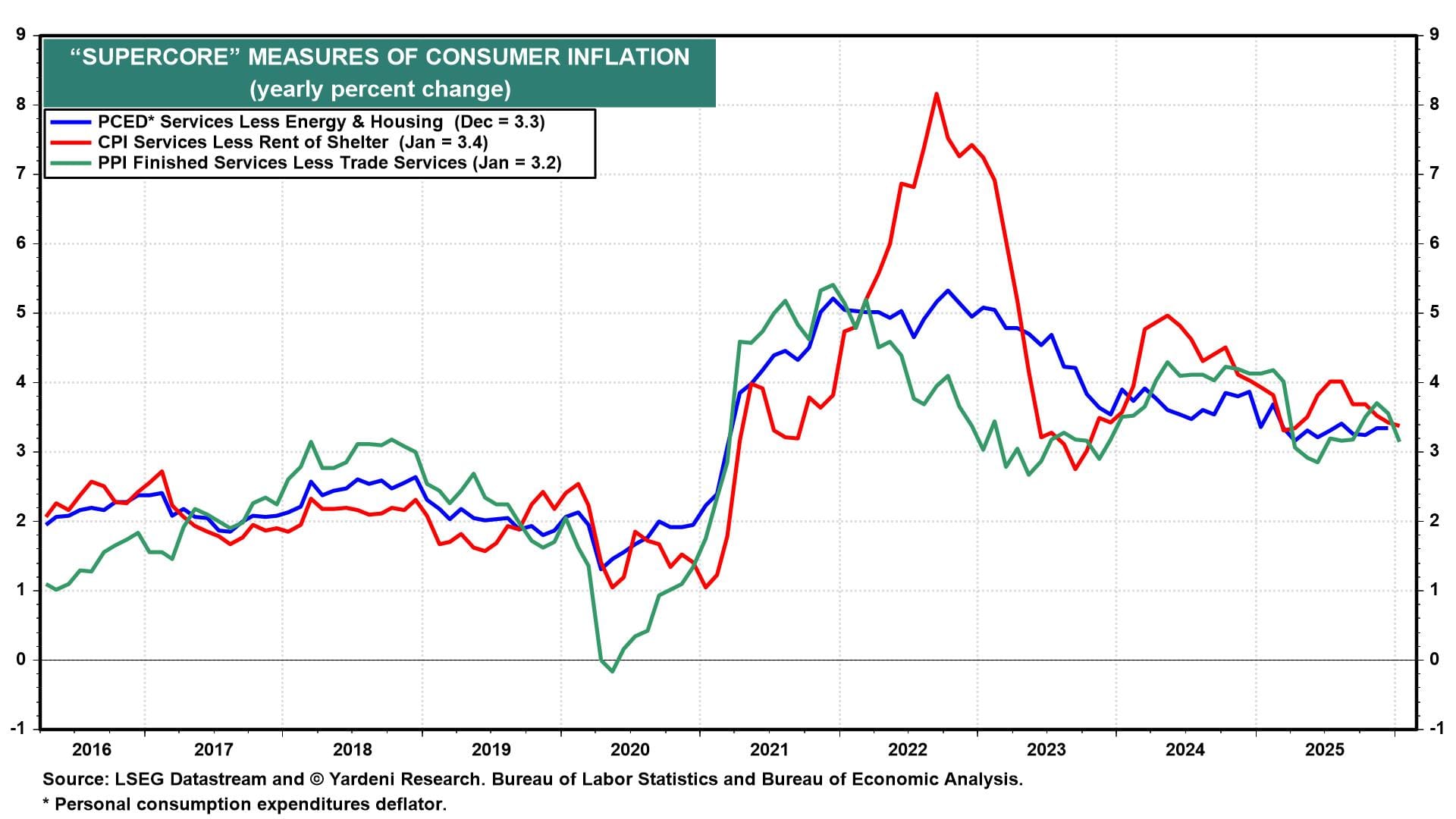

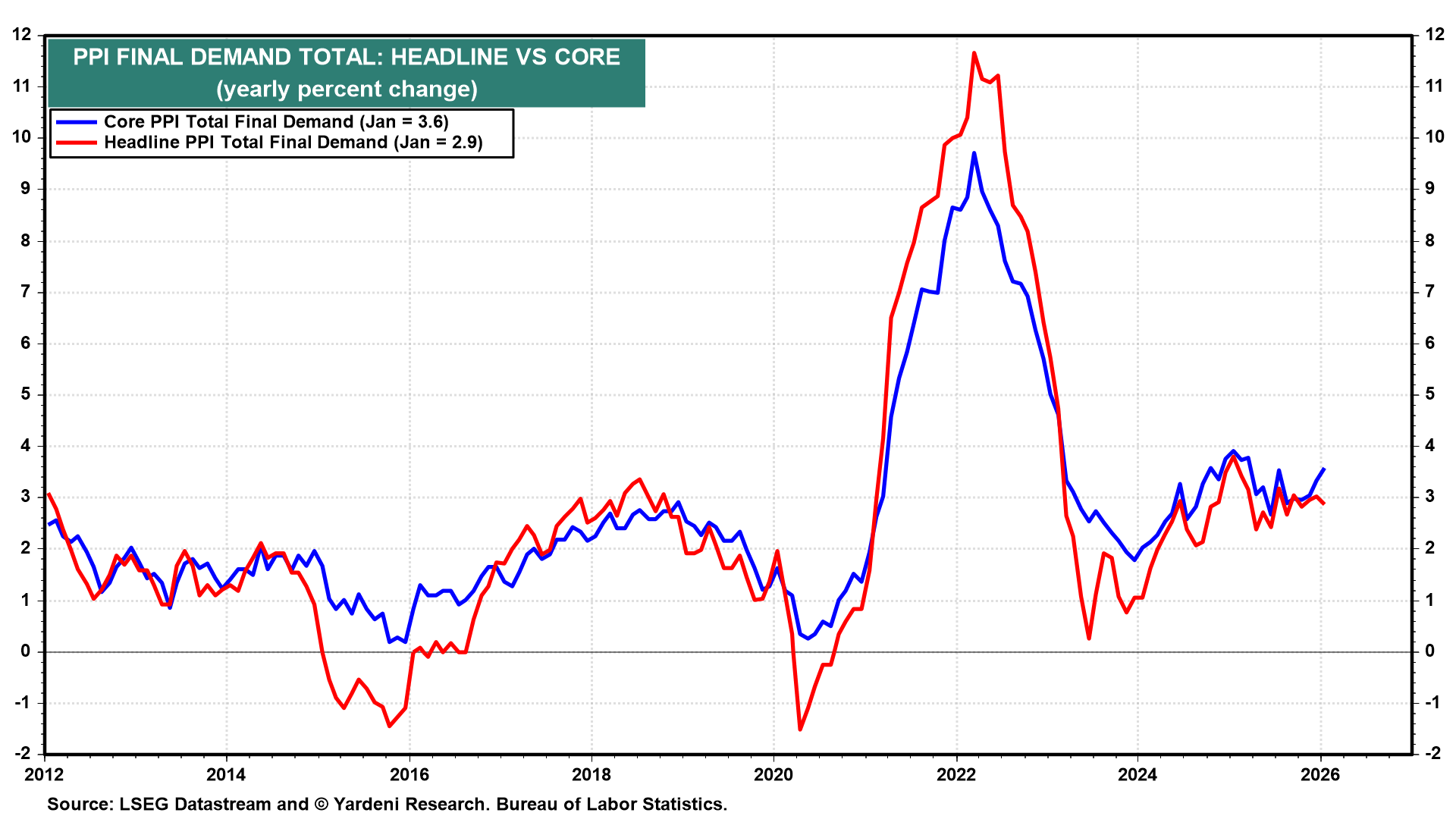

III. US PPI inflation hotter than expected

January's PPI report showed core inflation at 3.6% y/y (chart), up 0.8% m/m, compared to the expected 0.3%. The headline inflation rate was 2.9%. Both PPI inflation rates have moved sideways in recent months rather than continuing to decline, suggesting that the disinflation trend has stalled.

Much of the stickiness is concentrated in services inflation. Supercore readings remain in the low-to-mid-3% range (chart). We expect strong productivity gains to keep unit labor costs subdued this year, gradually easing services inflation. Furthermore, once the war in Iran ends, we expect oil prices to fall.