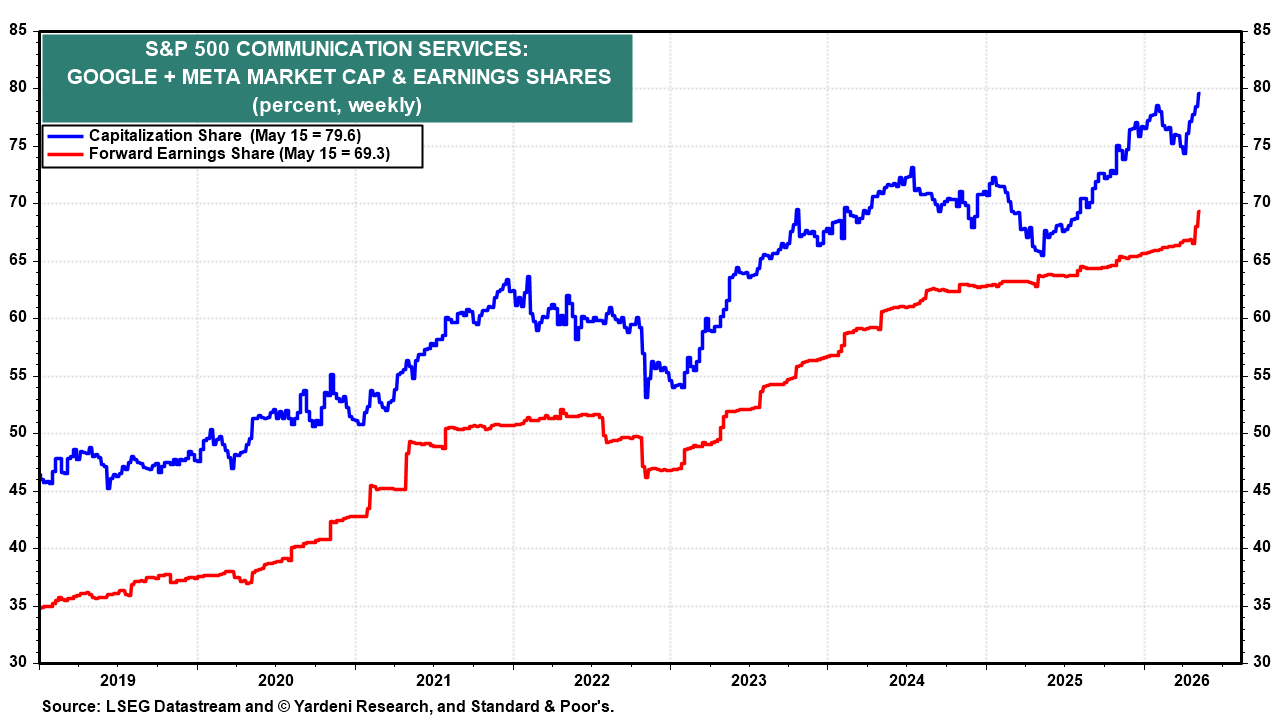

We continue to recommend a market-weight position in S&P 500 Communication Services, alongside our market-weight call on Information Technology, which we reiterated on April 25. The sector is a lopsided barbell. Alphabet and Meta together are the only two components of the sector's Interactive Media Services industry. Together, they account for almost 80% of the industry's market capitalization and 69% of its earnings (chart). The other 20% of the industry's market-cap share is a long list of advertising, broadcasting, cable, and telecom names that have largely underperformed. Any sector-level call is really a call on Alphabet and Meta.

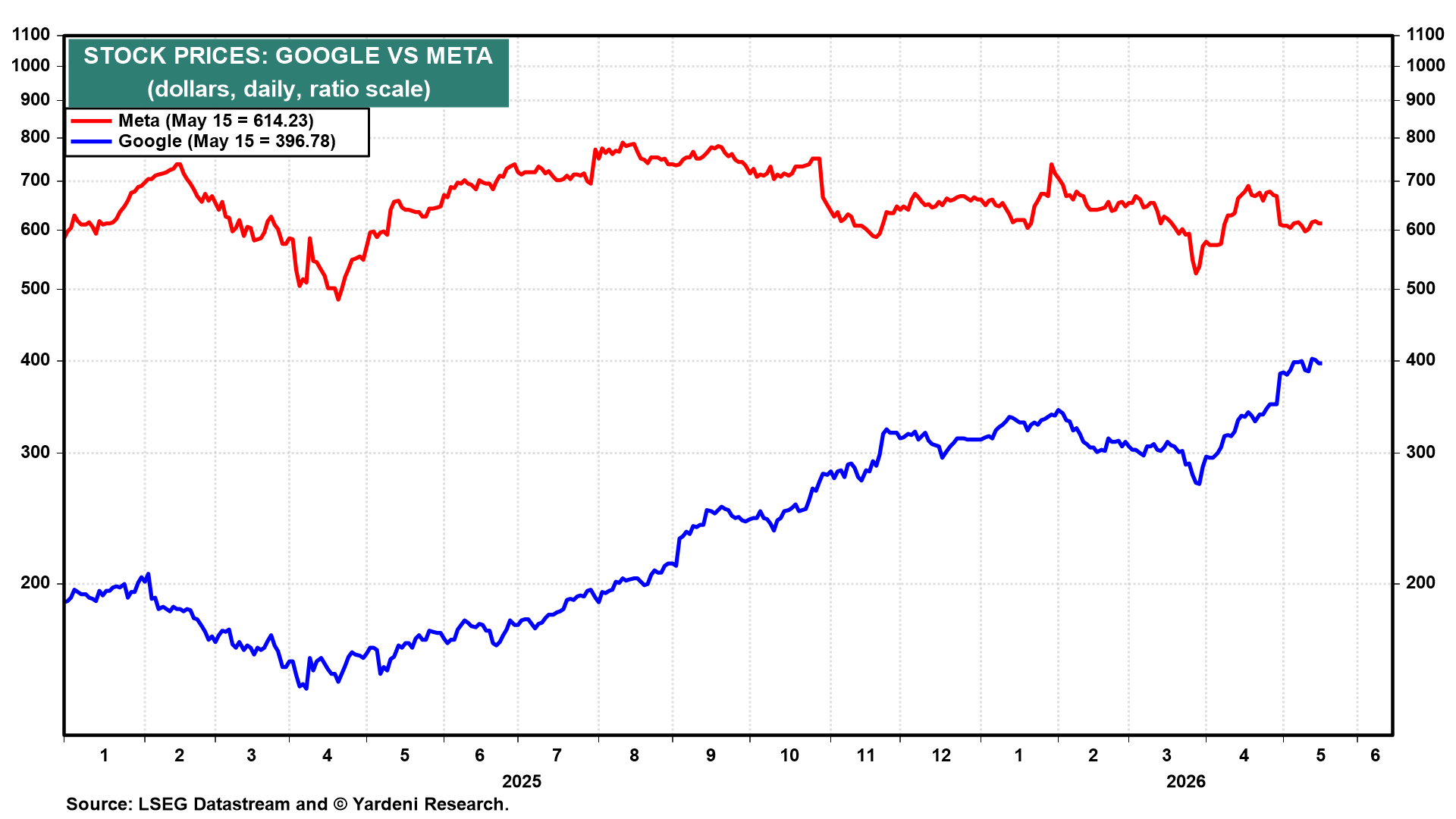

So far this year, Alphabet is up, while Meta is flat (chart). The divergence sharpened during the Q1 earnings season. Both beat on the top and bottom lines. Alphabet rose 10.0% after reporting a big increase in cloud revenue. Meta fell 8.6% after raising capex guidance. As a result, JPMorgan downgraded the name to "rising AI spend without a clear monetization path." Same sector, same capex story, opposite reactions. The market is rewarding companies that are clearly already monetizing their AI investments.

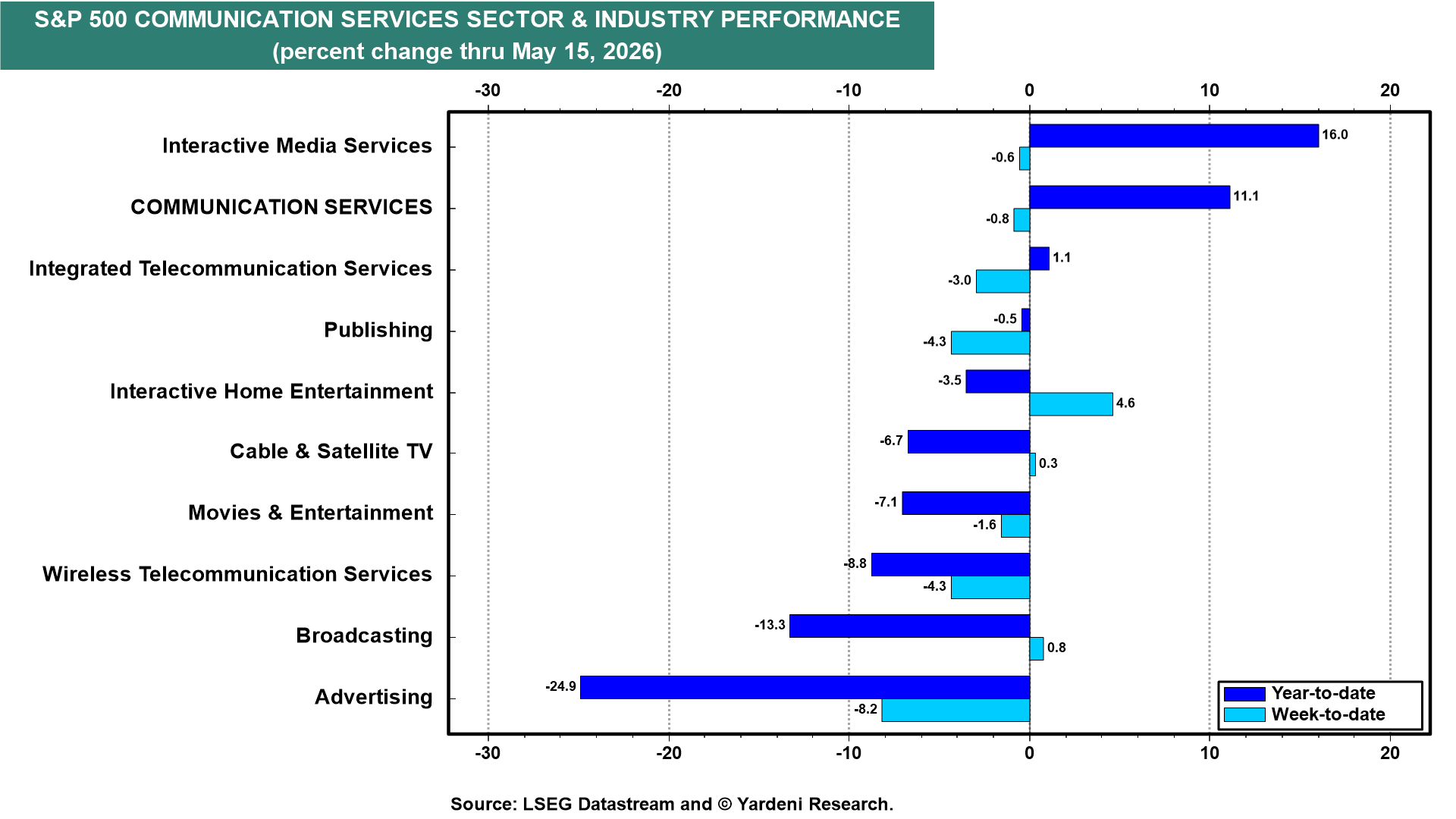

The Communication Services sector is up 11.1% ytd, beating the S&P 500's 8.2% gain (chart), but the headline flatters the breadth. Seven of the sector's nine main industries are still down so far this year (chart). Interactive Media Services (16.0%) and Integrated Telecom Services (1.1%) are the only positive readings.

Let's have a closer look at the sector's latest forward dynamics:

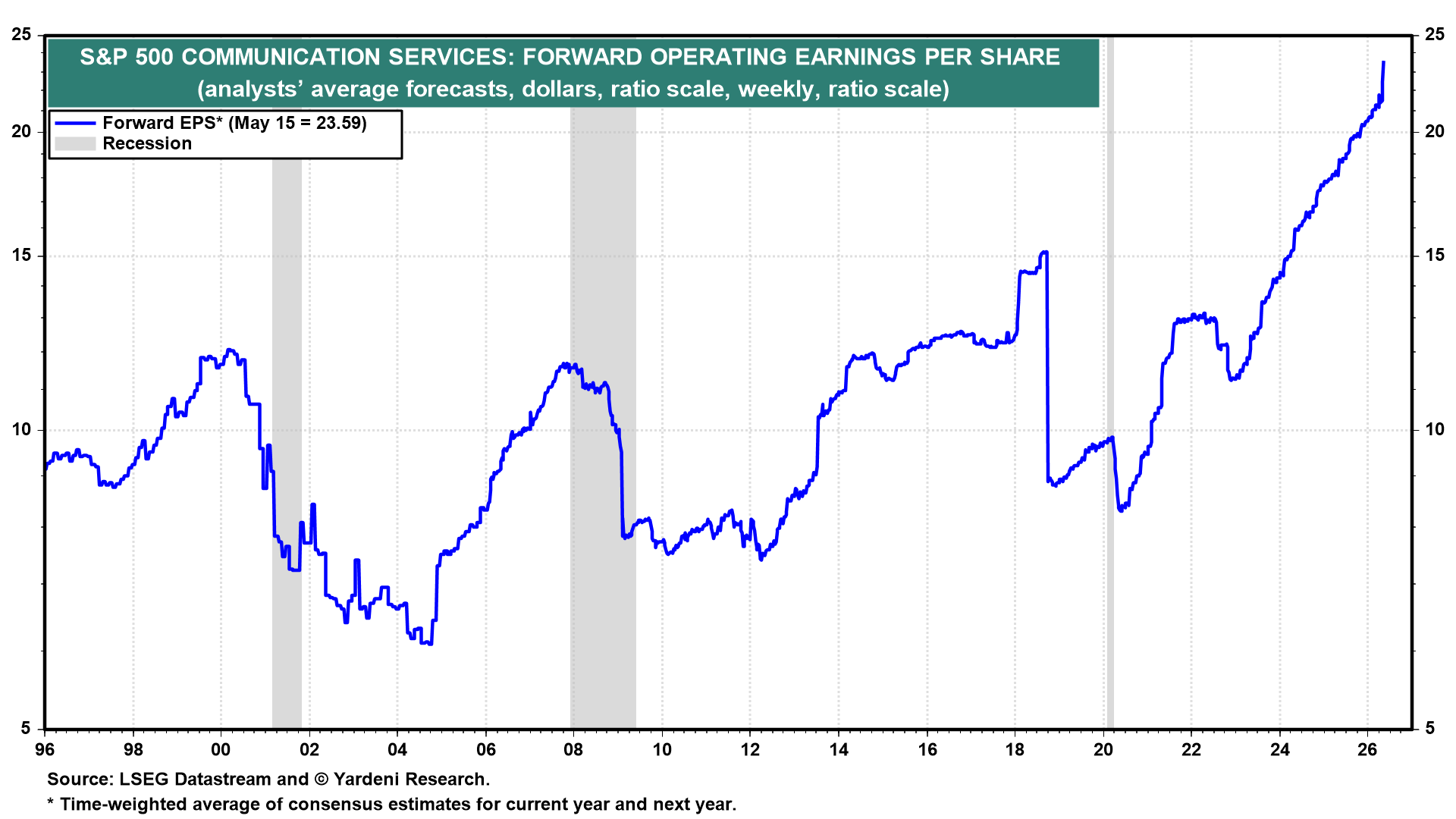

(1) Forward Earnings. The sector's forward earnings has soared to record highs since 2023 (chart). Q1 earnings growth is tracking at 54.8% y/y, the highest among all S&P 500 sectors. Annual earnings growth forecasts have also swung higher, with 2026 expectations now at 28.2%, firmly above the 18.3% recorded in 2025.

(2) Forward Revenues & Profit Margin. Q1 revenue growth is tracking at 13.6% y/y, the second-highest among all S&P 500 sectors. Annual revenue growth forecasts have been steadily revised higher, with 2026 now at 12.6%, up from 9.0% for 2025.

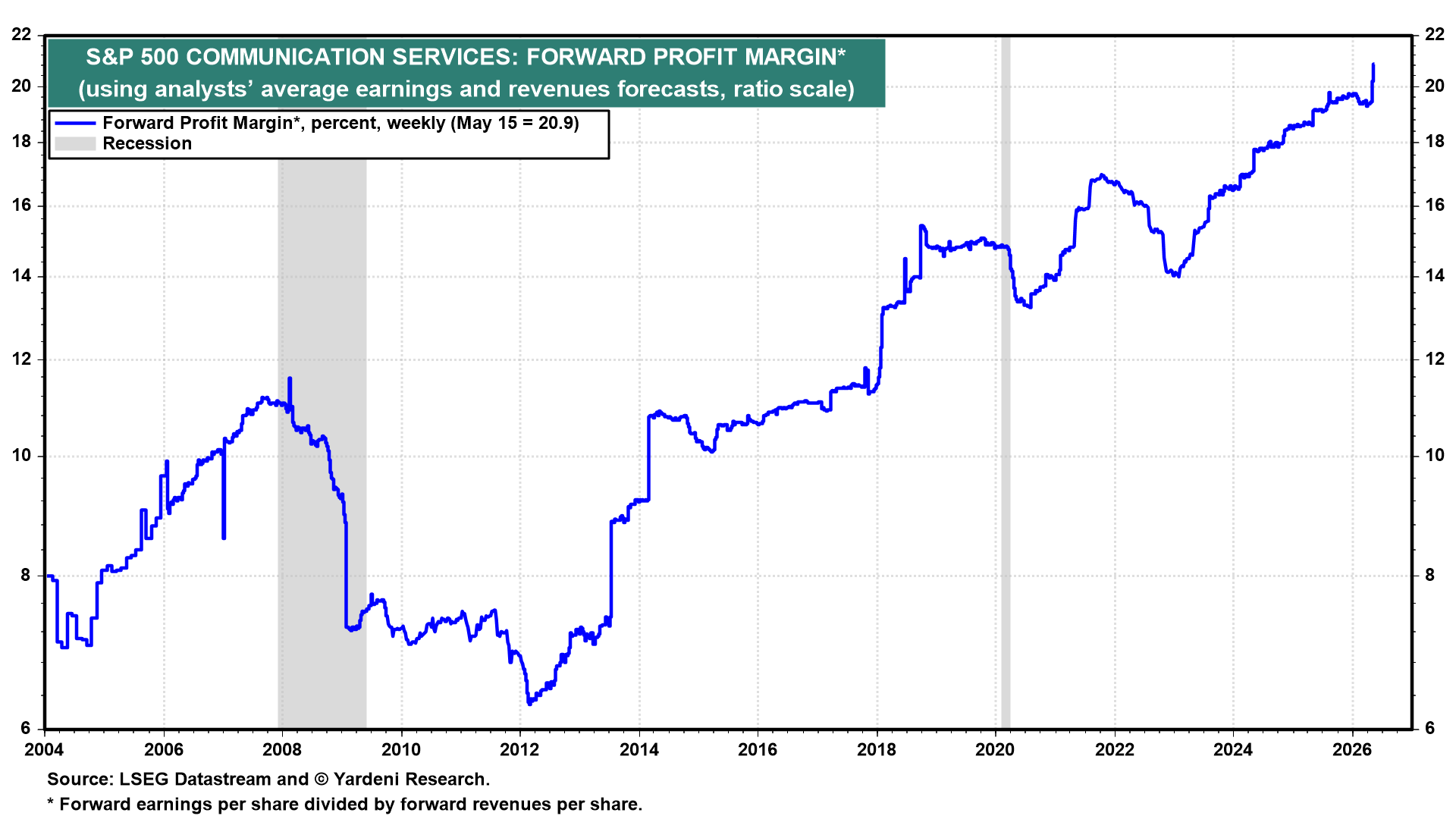

The sector's forward profit margin is 20.9%, the third-highest among the S&P 500 sectors, behind only Information Technology and Financials (chart). The sector's forward profit margin has steadily climbed from below 10% in the mid-2000s to record levels today.

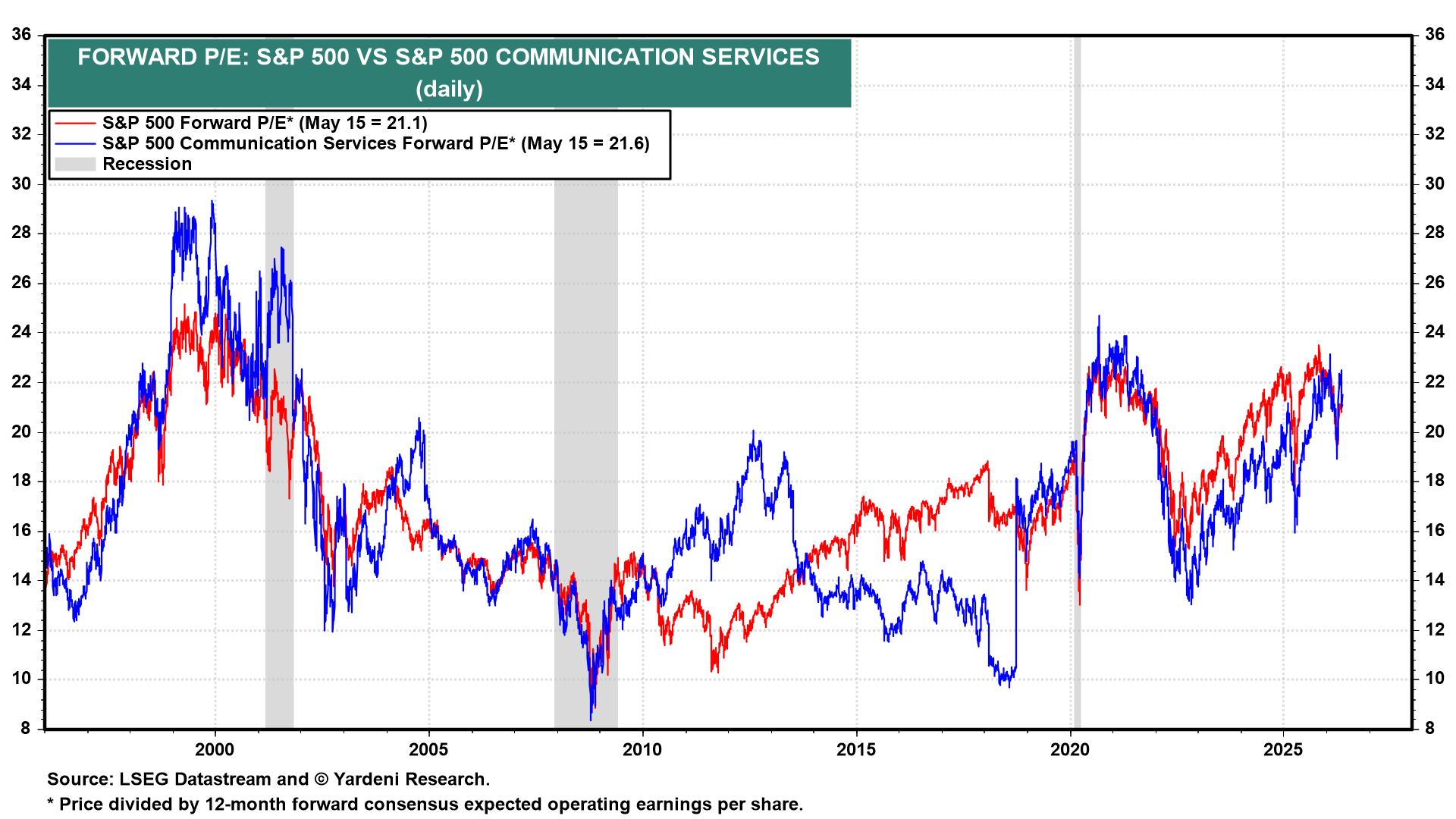

(3) Valuation. The sector's 21.6 forward P/E is only marginally above the S&P 500's 21.1, suggesting that its valuation is attractive given its high earnings growth rate.

(4) Bottom line. S&P 500 Communication Services is a concentrated bet on AI monetization. Strong earnings growth, healthy margins, and attractive valuation underpin our market-weight call.