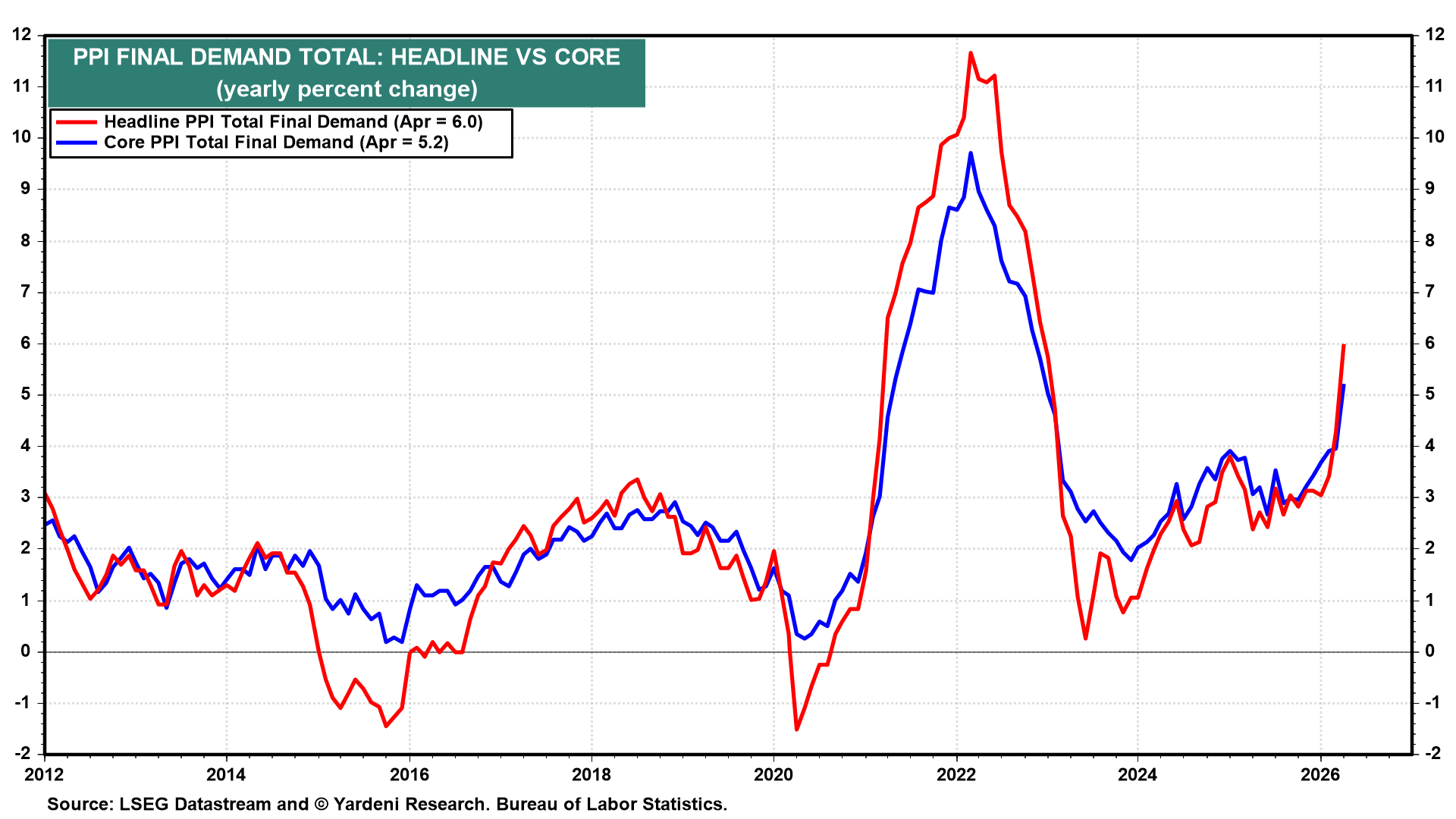

On Friday, the S&P 500 fell 1.2% from its record high of 7501.24 on Thursday. A run of hot inflation data and a spike in bond yields did the damage on Friday. April headline CPI hit 3.8% y/y, the highest since May 2023, while core CPI was 2.8%. The big shocker was last Wednesday's April PPI for final demand, which rose 6.0% y/y, the biggest increase since December 2022 (chart).

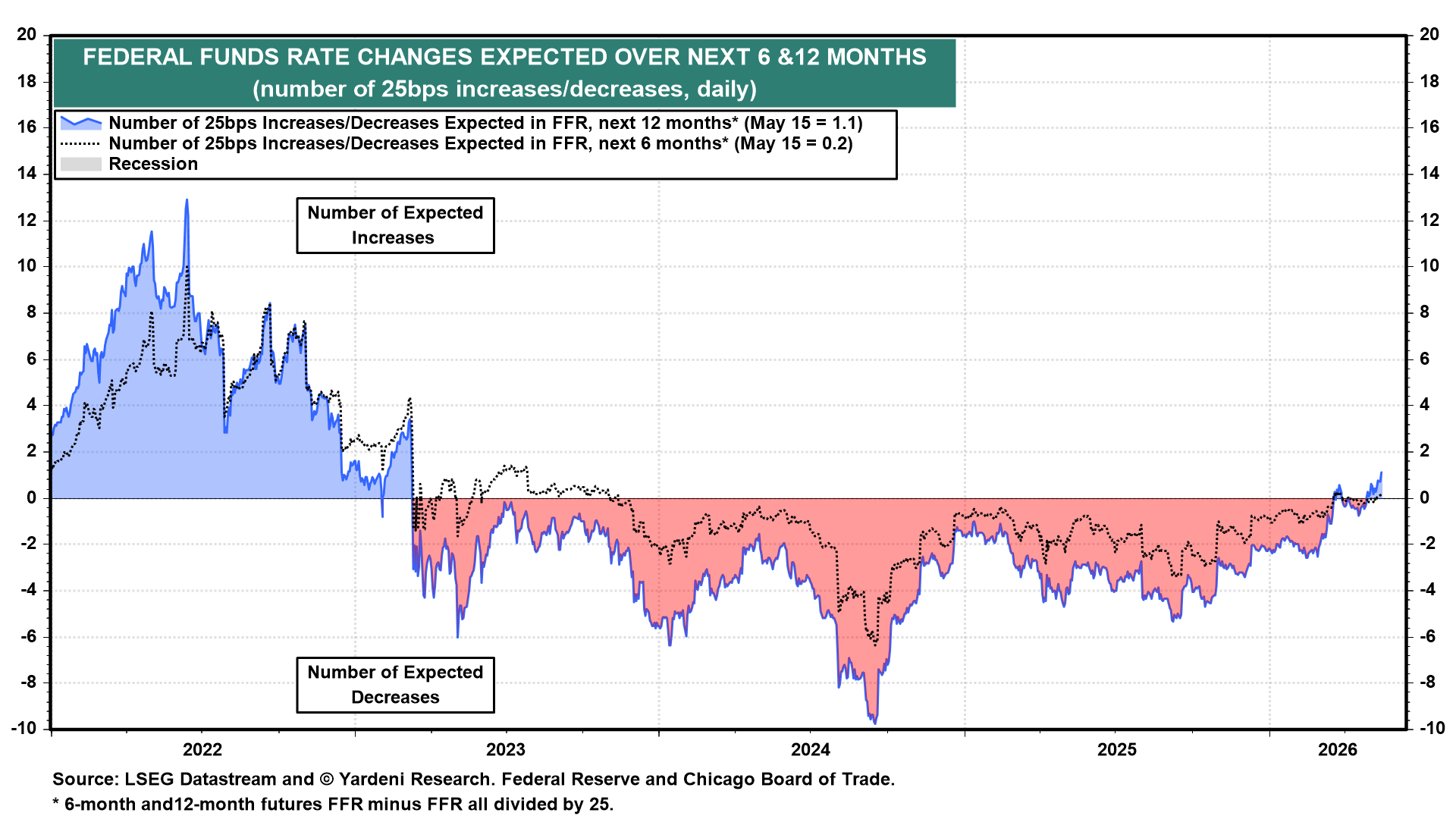

Federal funds futures have fully reversed the Fed's easing path priced just three months ago, with the next move now expected to be a hike. The 2-year Treasury yield rose to 4.08% on Friday, confirming that the current federal funds rate (FFR) range of 3.50%-3.75% is too low. The 10-year Treasury yield jumped to 4.60%, and the 30-year topped 5.10%, the highest since May 2025.

As we signaled last week, we expect the FOMC to signal a tightening bias at the June meeting of the monetary policy-setting committee, followed by a 25bps FFR hike at the July meeting. We can't rule out more rate hikes over the rest of this year.

The Trump-Xi summit in Beijing produced verbal alignment on keeping the Strait of Hormuz open and barring Iran from nuclear weapons, but no comprehensive tariff deal emerged. We expect that Trump might signal his next move in the Gulf War in the coming days. Odds are he will maintain the blockade of Iran's ports.

The week ahead is very light on US data. April's FOMC minutes will be released on Wednesday, with a couple of regional business surveys on Thursday. NVIDIA will report on Wednesday. The UK and Eurozone CPI will be reported on Wednesday.

With that said, here are the key releases most likely to shape investors' thinking this week:

(1) FOMC minutes. Wednesday brings the minutes from the April FOMC meeting, when the Fed kept rates on hold for the third consecutive meeting. The headline was the dissent: As usual, Stephen Miran voted for a cut; but three officials objected to including an easing bias in the policy statement, arguing that the data no longer justify signaling that the next move would be a cut. The minutes will indicate how many other participants might have also leaned toward either a neutral or hawkish bias.

In the past few weeks, Fed funds futures have flipped from pricing in cuts to pricing in one hike over the next 12 months (chart). With inflation now running too hot, the easing-bias language is the most dovish element of current Fed communication. It is unlikely to survive June’s FOMC meeting. The bias is likely to flip straight from dovish to hawkish.

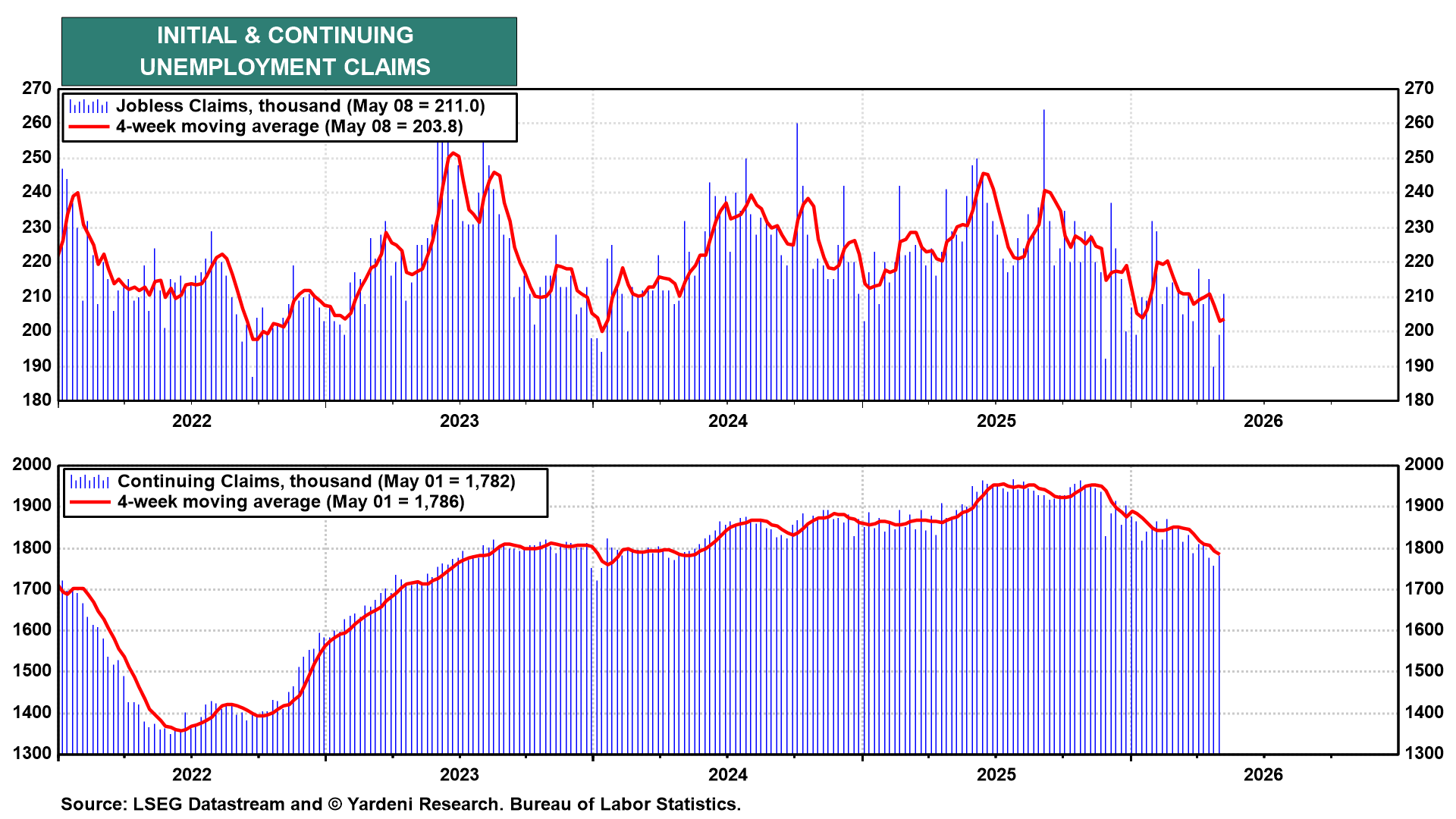

(2) Unemployment. Initial jobless claims (Thu) rose to 211,000, with the four-week moving average at 203,800 (chart). Continuing claims came in at 1,782,000, with the four-week moving average at 1,786,000. Until claims break decisively higher, the case for Fed rate hikes should build.

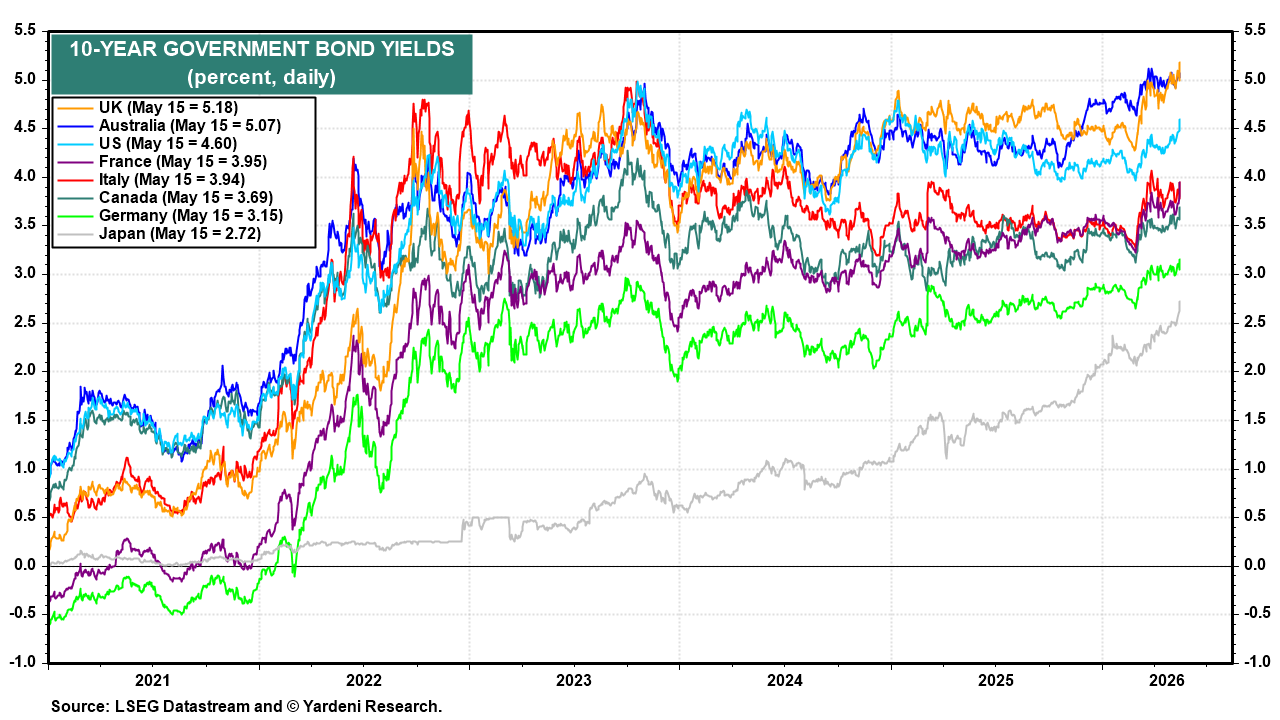

(3) Global yields. Yields have surged across developed markets in recent weeks (chart). UK 10-year gilts at 5.18% lead the G7, with Australia at 5.07% and the US at 4.60% (chart). Japan, at 2.72%, has climbed from essentially zero in 2021. Monday brings Japan's Q1-2025 GDP, and Thursday brings Japan's core CPI.

Wednesday is jam-packed with bond-moving data. April's UK CPI lands in the morning, followed by the German 10-year bund auction and the US 20-year Treasury auction in the afternoon. A weaker UK CPI would take pressure off the entire complex. A hot print would extend the move higher. BoE members Mann and Greene speak on Monday, with Mann the most hawkish dissenter on the MPC.

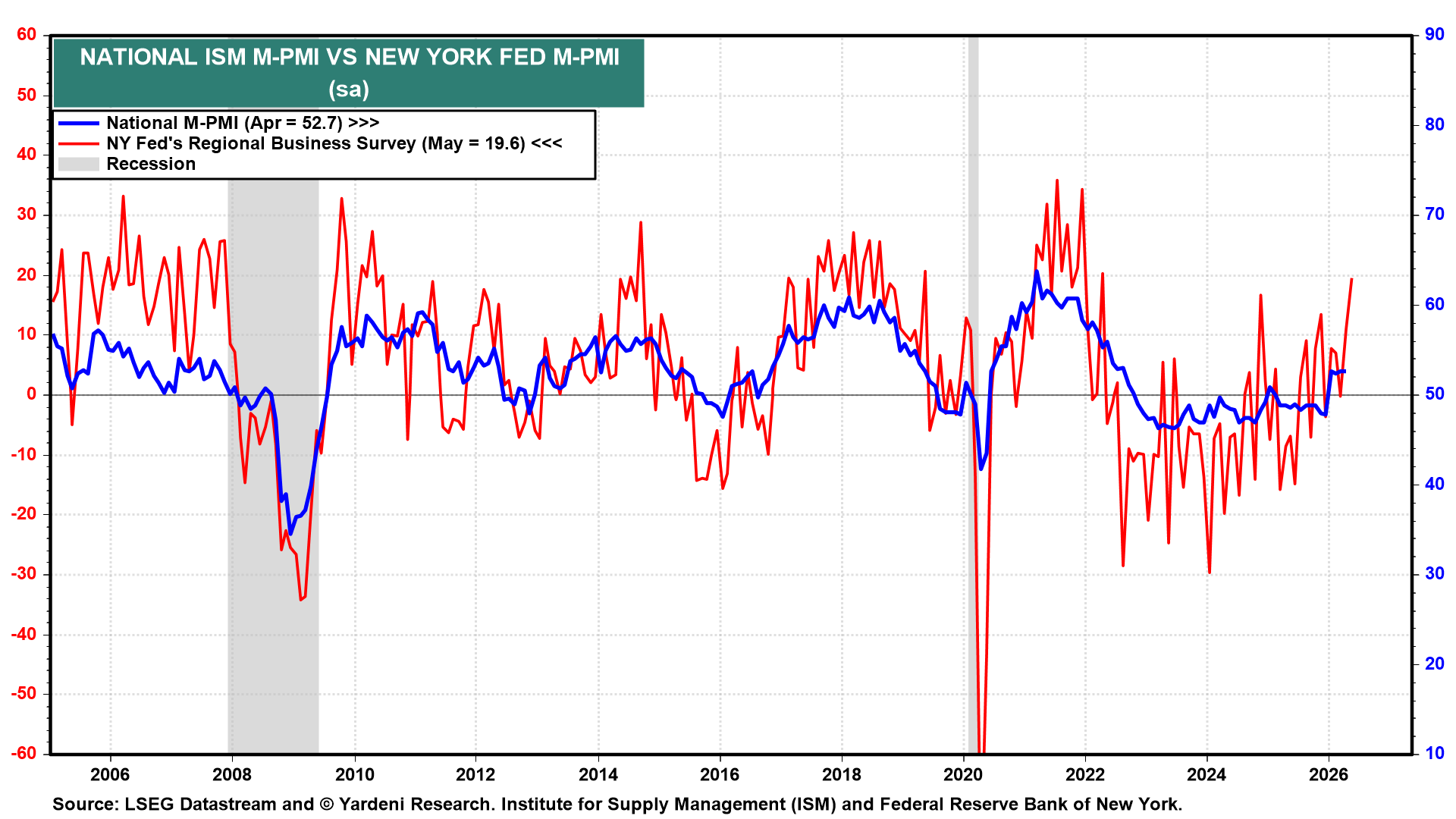

(4) Business Surveys. Thursday's S&P Global flash PMIs for May are the first hard read on the month's economic activity. According to the ISM surveys, April manufacturing came in at 54.5, the strongest in over a year, while non-manufacturing slipped to 51.0. May's Philadelphia and Kansas City Fed regional business surveys will also be released on Thursday. The NY Fed survey was very strong for May (chart).