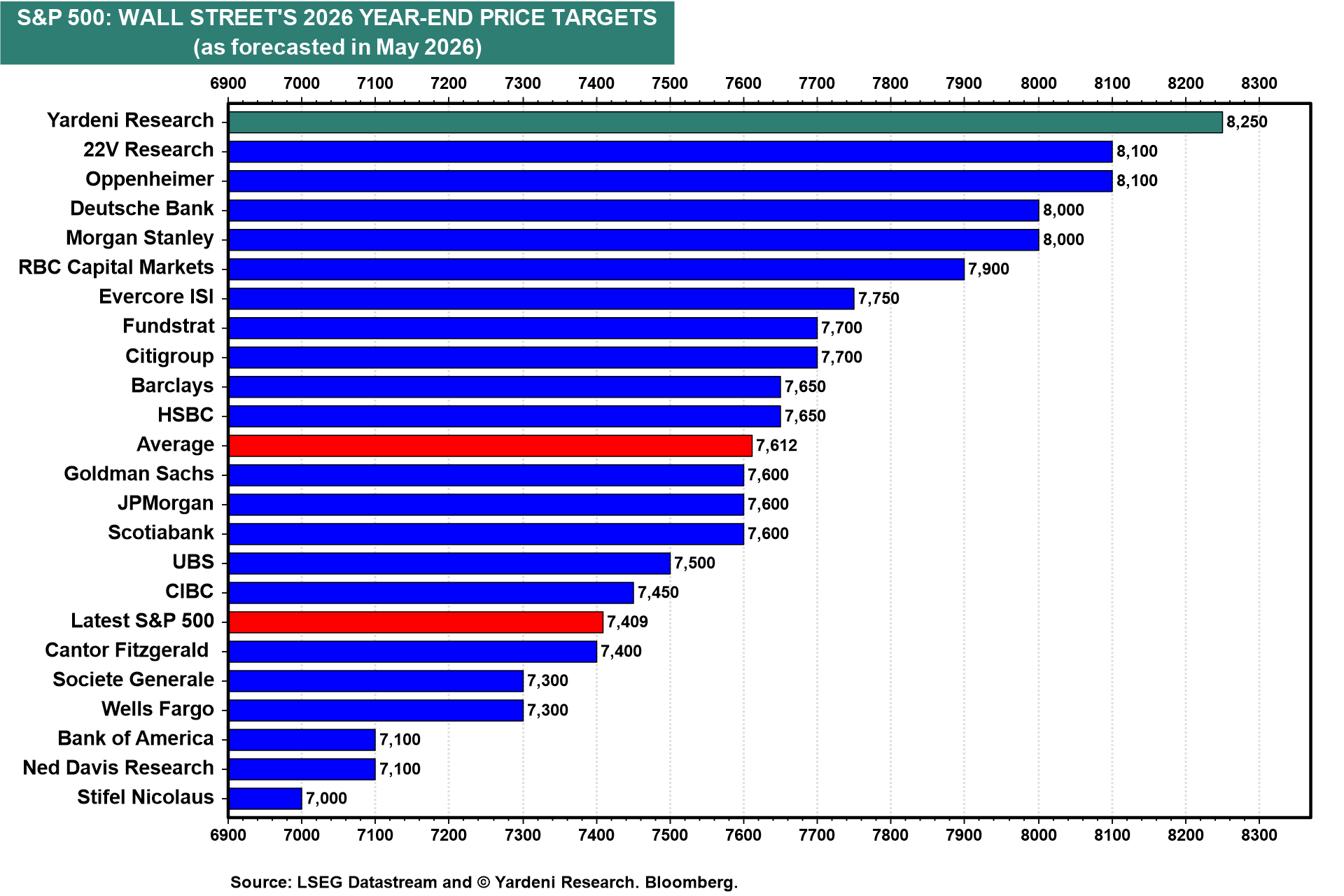

The S&P 500 sold off by 1.2% on Friday after hitting a record high of 7501.24 on Thursday. We are sticking with our 8250 year-end target for the S&P 500 (chart). However, the index might have peaked for a while. That's because bond yields spiked on Friday, which just happened to be Kevin Warsh's first day at the office as the new Fed chair. The bond market fears that he will tolerate inflation rather than hike the federal funds rate (FFR). He will likely have to cave and join the tightening camp sooner rather than later. The Bond Vigilantes will force him to pivot. So will his colleagues on the FOMC.

The Strait of Hormuz remains closed. In a post on Truth Social, President Donald Trump warned: "For Iran, the Clock is Ticking, and they better get moving, FAST, or there won’t be anything left of them. TIME IS OF THE ESSENCE!" A drone strike caused a fire at a nuclear power plant in the United Arab Emirates, officials there said on Sunday, while Saudi Arabia reported intercepting three drones.

Brent crude is up $2 to $111 per barrel this evening (chart). The longer it remains here or higher, the greater is the likelihood that the Fed will have to pivot from its easing bias in April to a tightening bias in June and an actual rate hike in July. We wouldn't rule out a June rate hike.

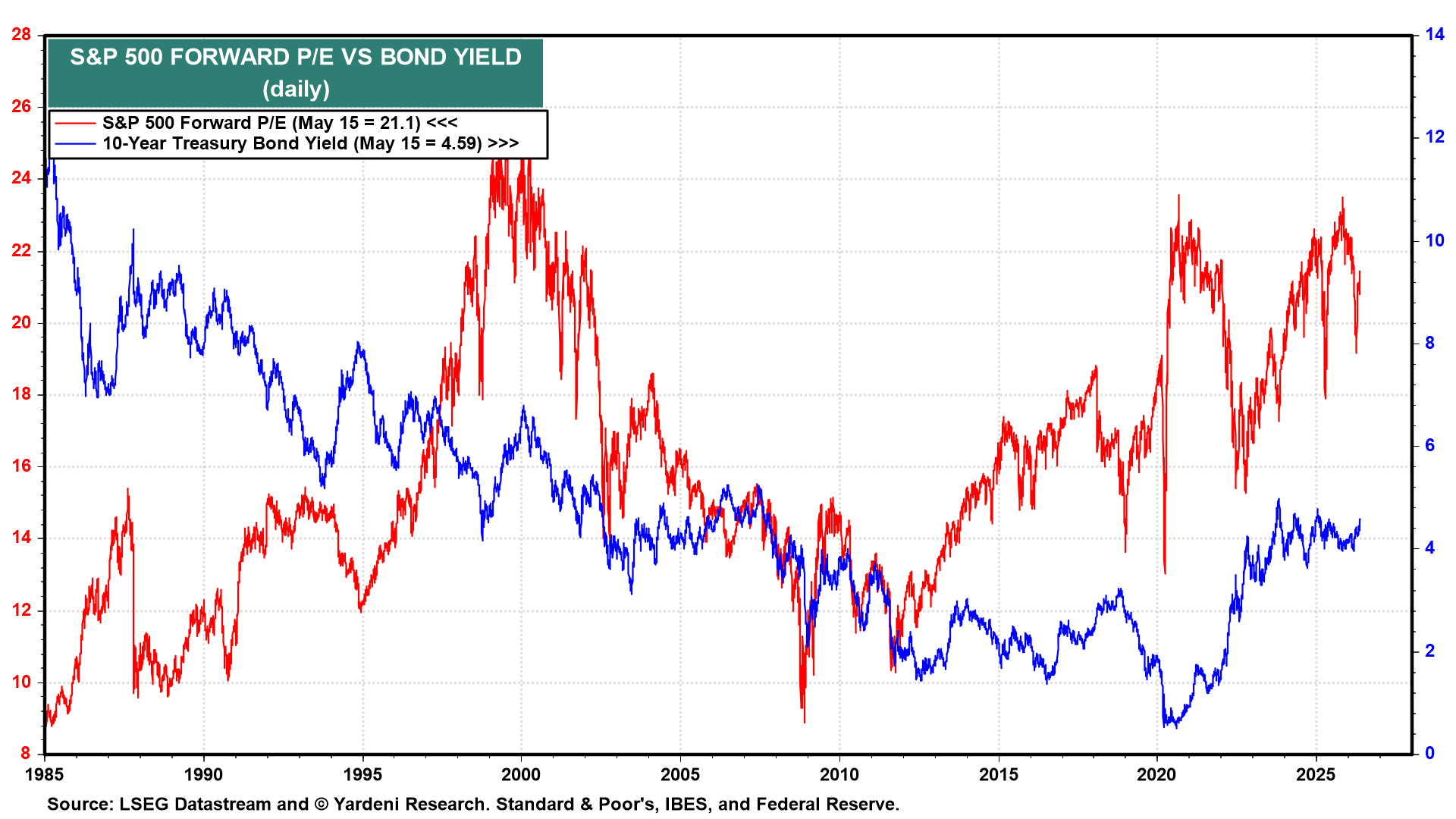

Last Wednesday, when the 10-year US Treasury yield was 4.46%, we predicted it was "likely to move up to 4.60% in the coming days." It got there on Friday (chart). This evening, it is at 4.63%. If it moves higher from here, then we would expect it to peak between 4.75% and 5.00% in the coming weeks. That would be a good buying opportunity for both bonds and stocks.

The S&P 500 forward P/E has risen 10% from its recent low of 19.1 to 21.1 on Friday, while the 10-year yield has climbed 63 bps from its low of 3.96% earlier this year (chart). If yields continue climbing, stocks will likely experience another P/E-led pullback. We would view it as another buying opportunity.