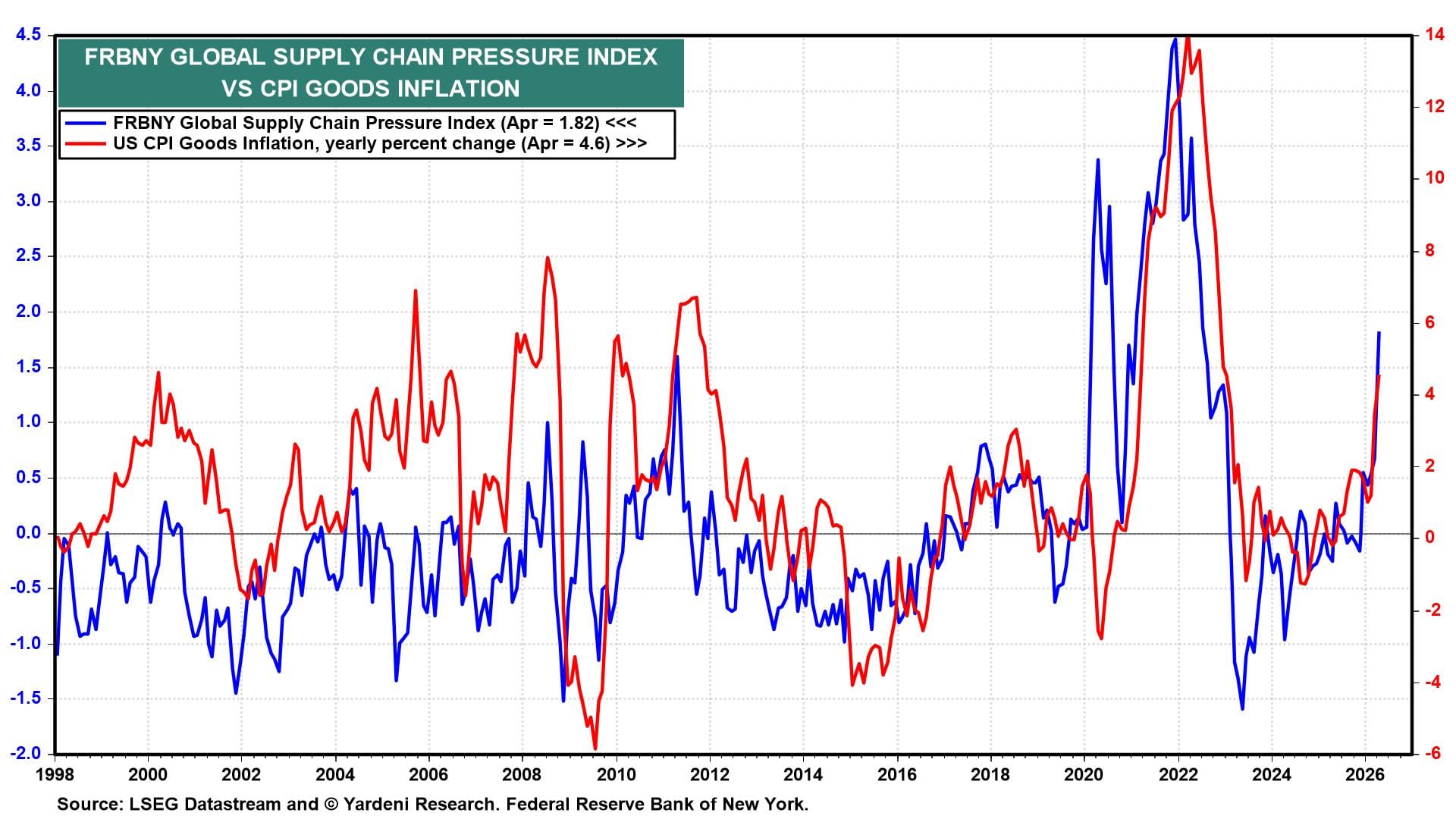

During 2021 and 2022, a wage-price spiral was exacerbated by widespread global supply chain disruptions and a spike in oil prices following Russia's invasion of Ukraine (charts). This time, the war in the Middle East has caused oil prices to spike. Some supply chains have been disrupted. But a wage-price spiral is less likely.

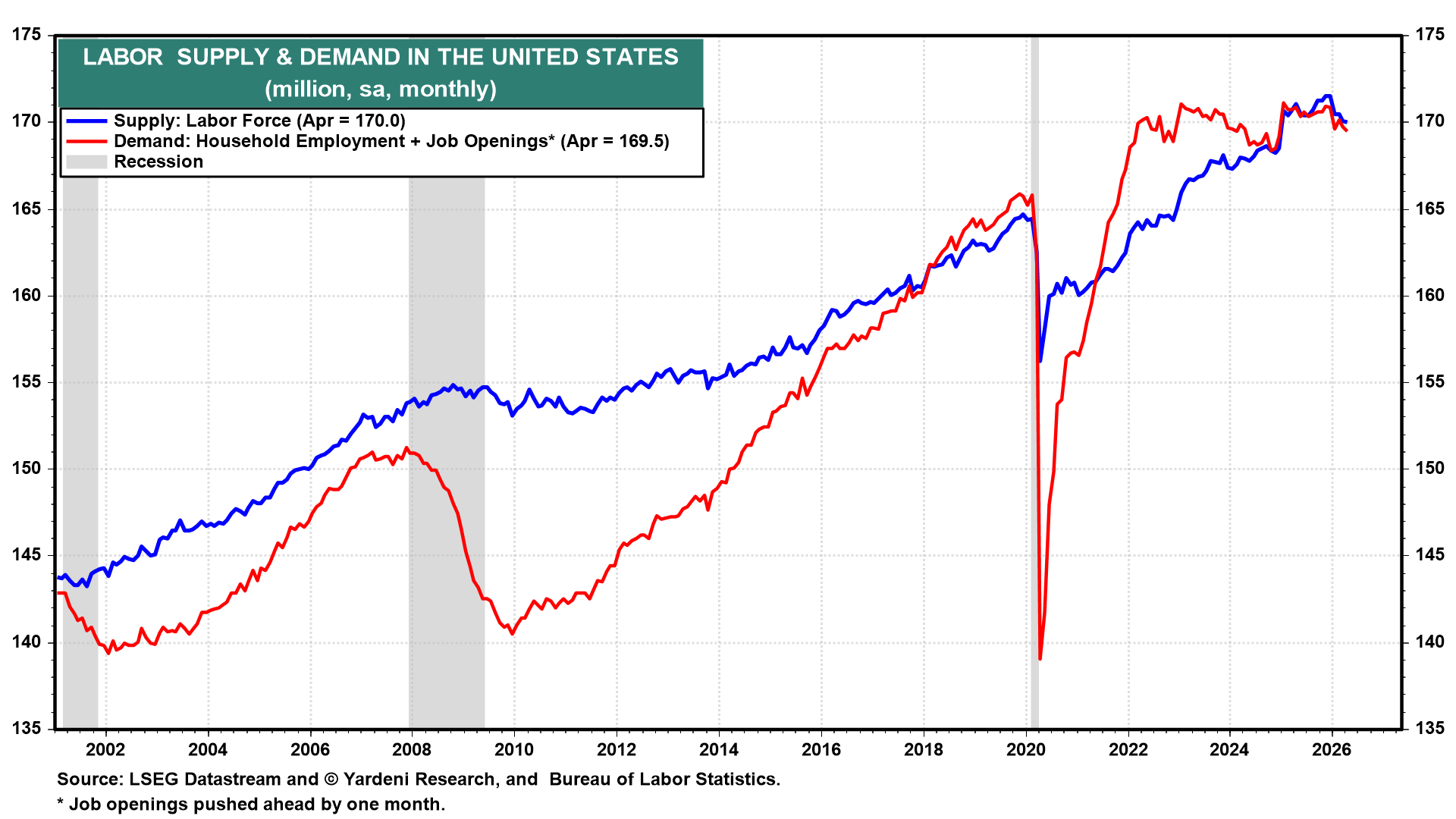

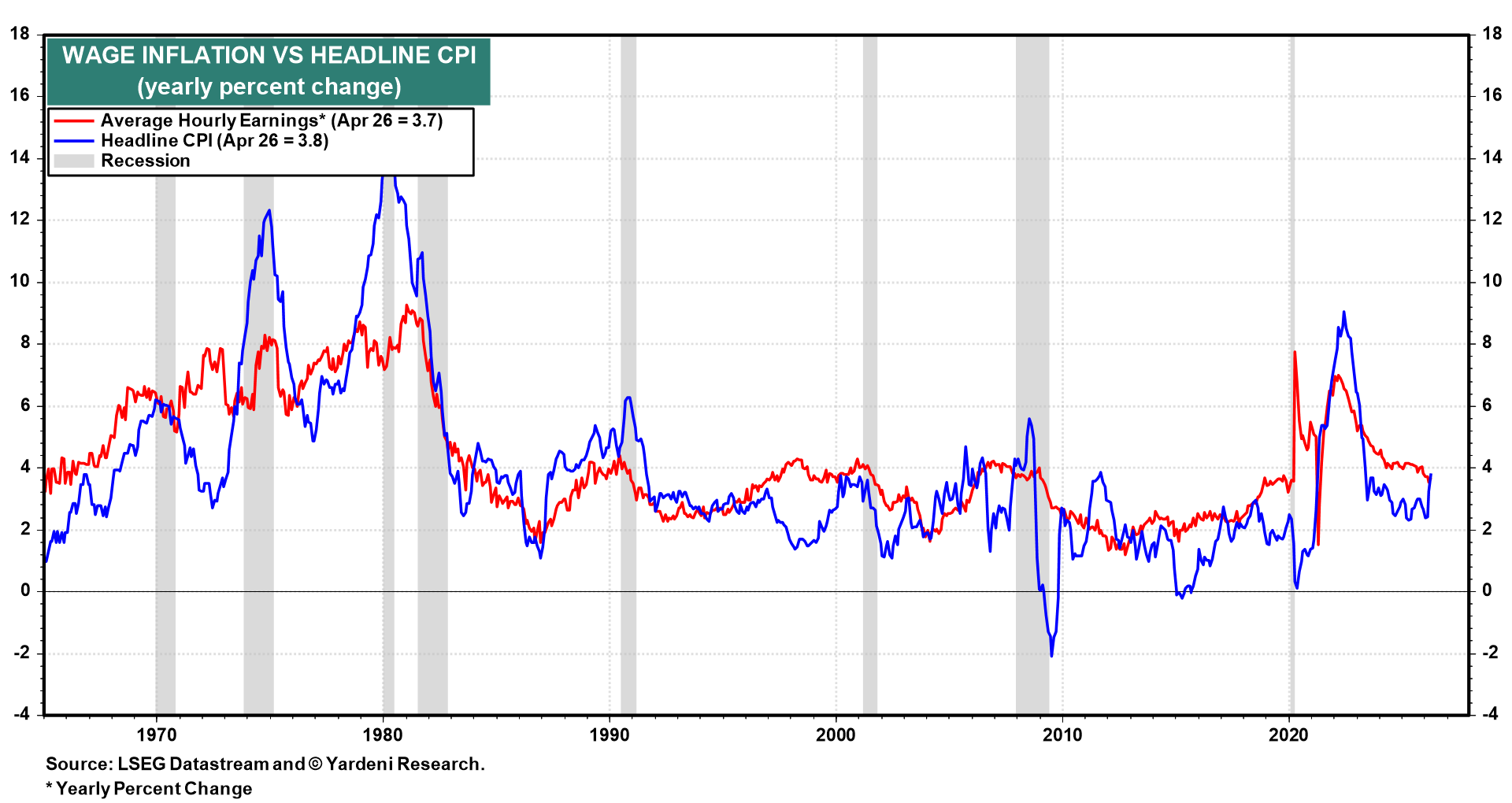

The labor market is in equilibrium this time (chart). In 2021-22, demand for labor significantly exceeded the supply of labor. So, wage inflation should remain much more moderate this time than it was back then (chart).

If so, then a wage-price spiral is unlikely to amplify the inflationary consequences of the supply shock attributable to the Strait of Hormuz blockade (chart).

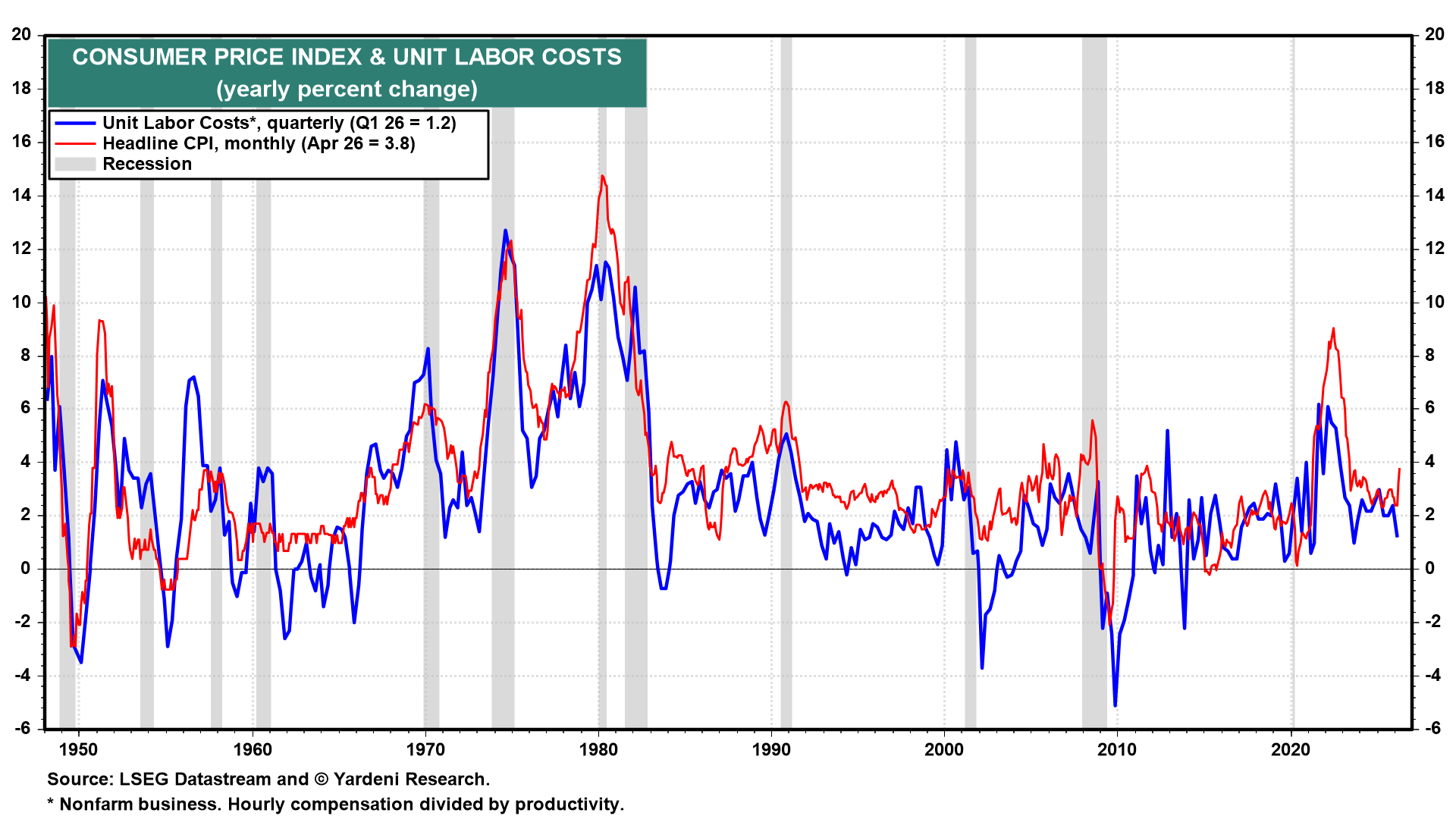

Unit labor cost inflation fell to 1.2% y/y during Q1 as productivity gains offset increases in hourly compensation (chart). In our Roaring 2020s scenario, productivity should remain a powerful disinflationary force, while wage inflation remains moderate.

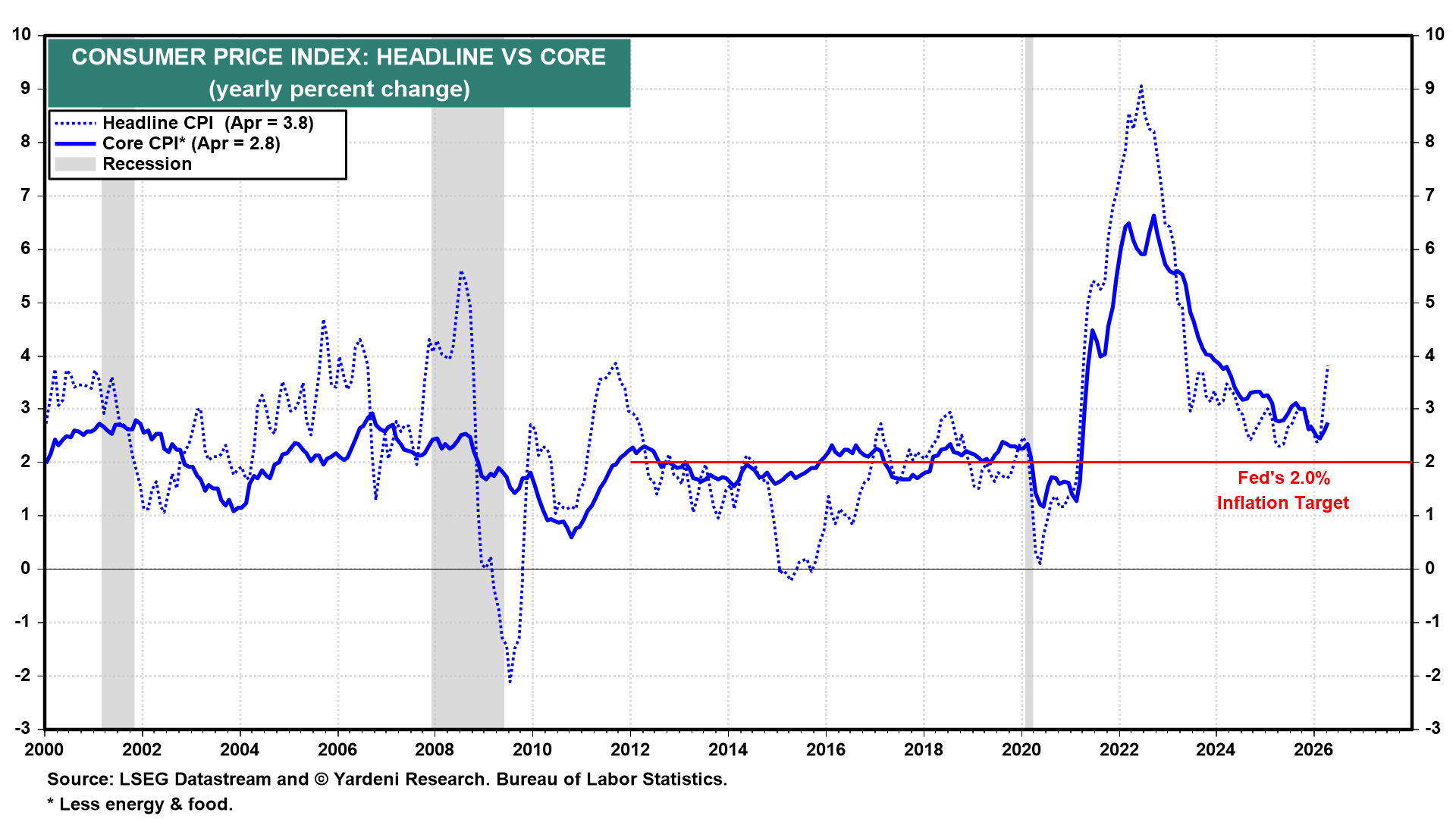

As a result of the latest energy shock, the headline and core CPI inflation rates rose to 3.8% and 2.8% y/y during April (chart). The headline inflation rate was the highest since May 2023, and up half a percentage point from March.

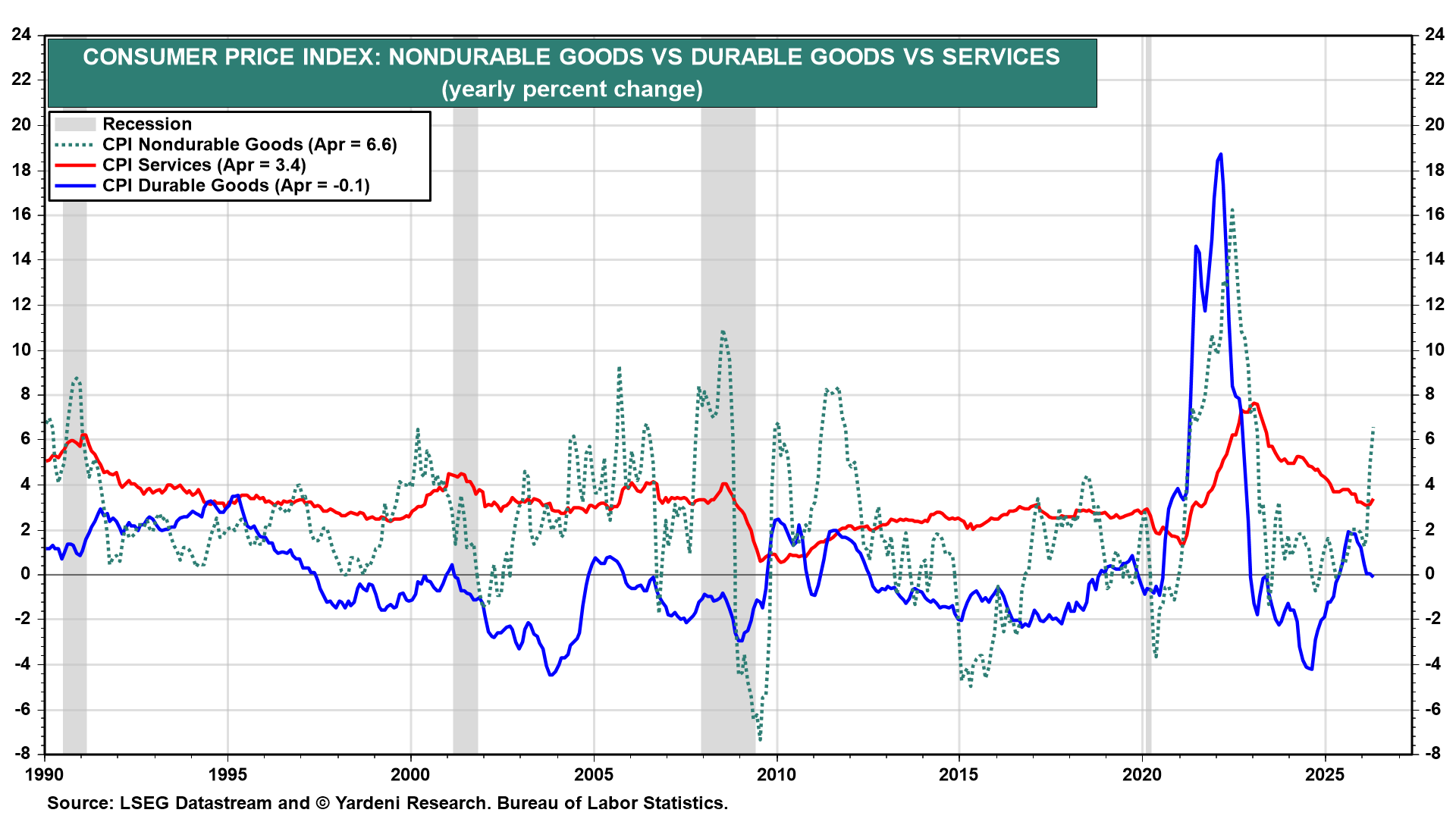

The CPI inflation rate was driven higher by a 6.6% y/y increase in nondurable goods prices, as energy prices rose 17.9% y/y (chart). Durable goods inflation continued to moderate to -0.1% y/y, indicating that the impact of tariffs is diminishing. The services inflation rate edged higher to 3.4%.

Let's have a closer look at the CPI data: