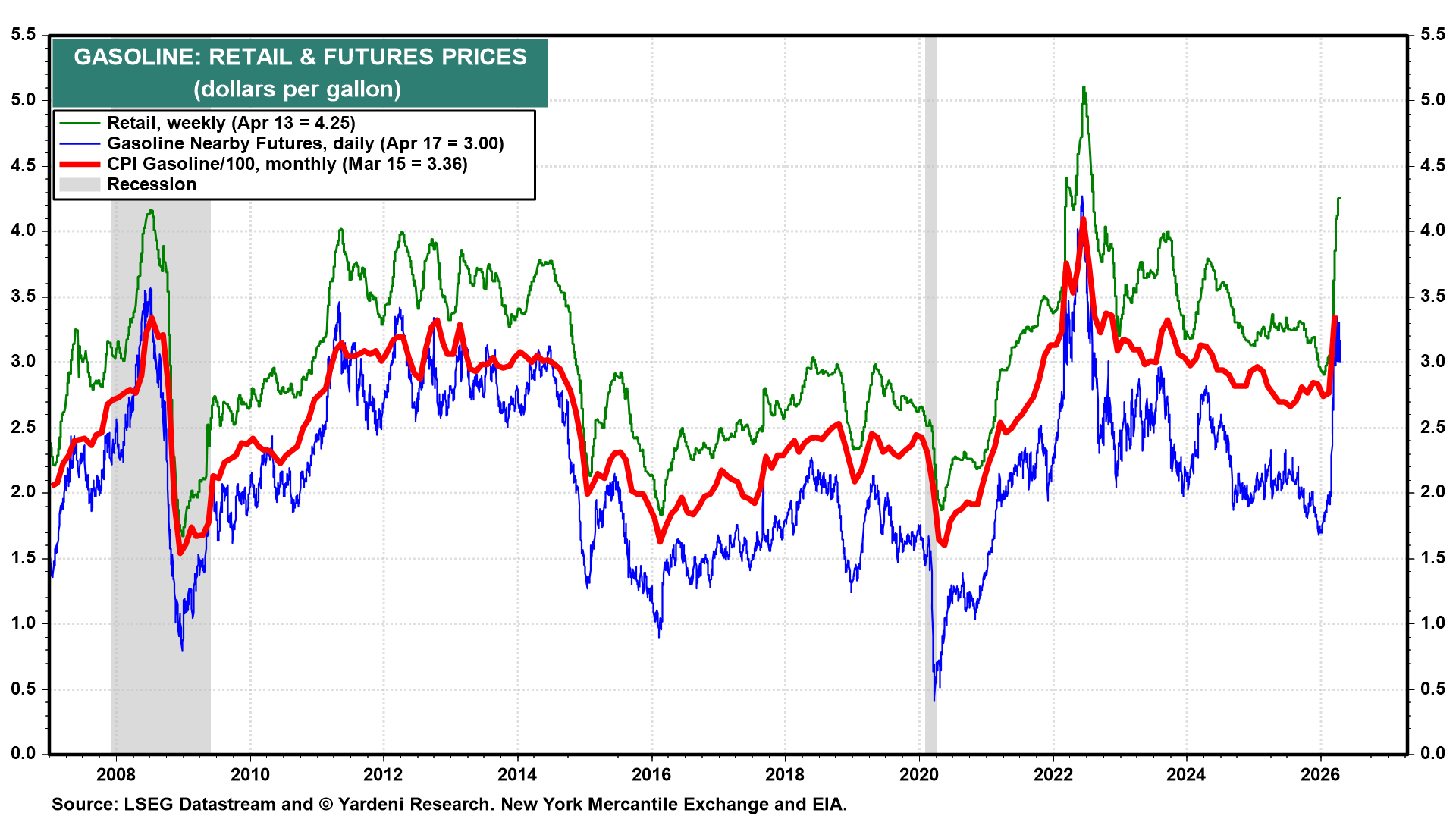

The week starts with the Strait of Hormuz still the key risk for financial markets. Today, Iranian state media said the Strait has been closed again because the US “did not fulfill their obligations.” Iran had declared it was open on Friday. A renewed US diplomatic push could send senior officials back to talks as early as Monday, but no date has been finalized, and the situation remains fluid. In the US, the average pump price remained above $4.00 during the week of April 13 (chart).

Adding to the week’s suspense, the probable next chief of the Federal Reserve, Kevin Warsh, testifies before the Senate at his confirmation hearing on Wednesday. The markets will be listening to how he views the Fed’s independence, the Fed's dual mandate, and the Fed's sequencing of rate decisions given the current economic backdrop.

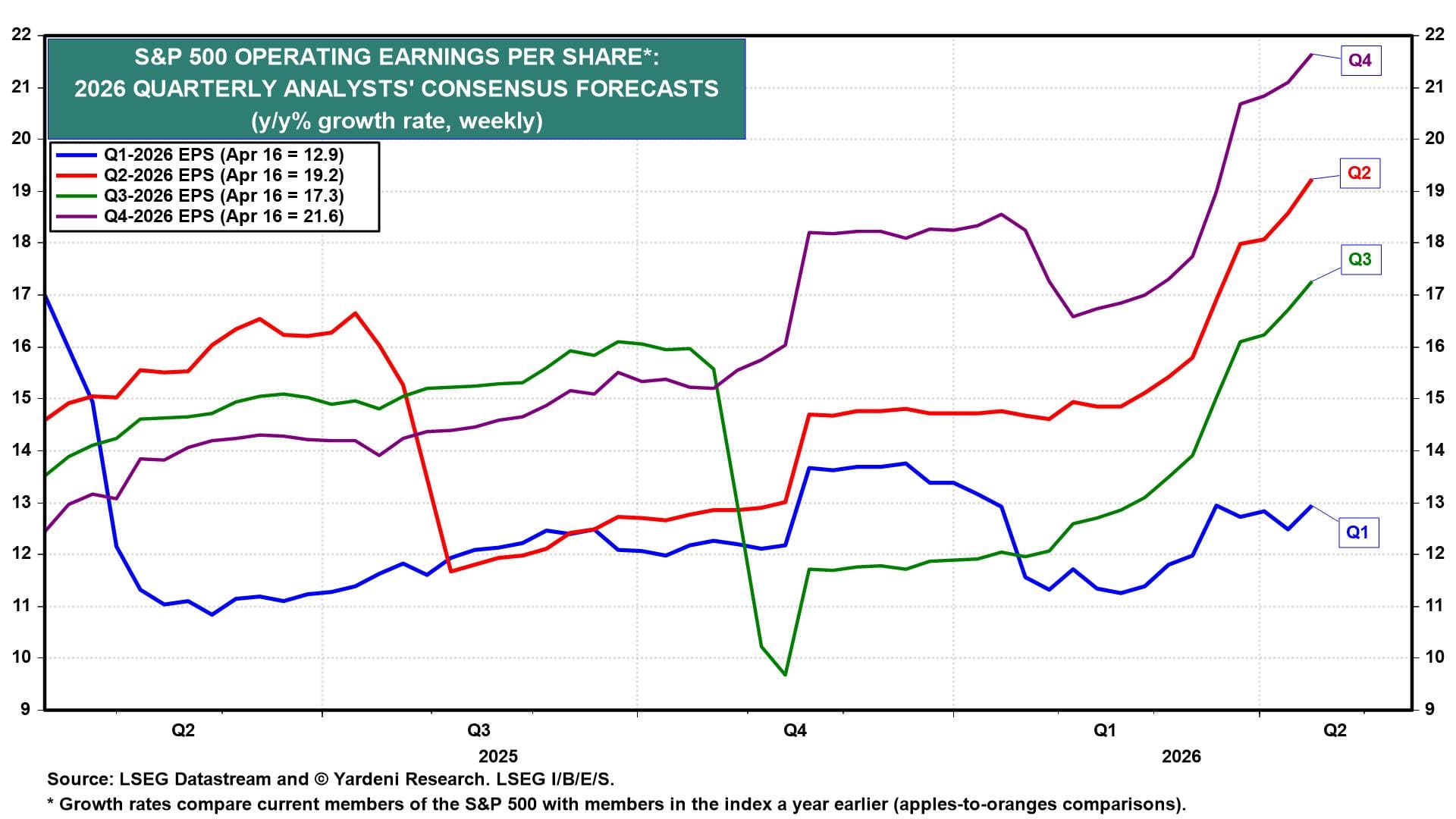

Earnings season adds another layer of complexity, with expectations remaining remarkably resilient despite the war in the Middle East (chart). Guidance is likely to be focused on geopolitical uncertainty. This week’s economic data and the corporate tape arrive simultaneously, and together they will do more to set the near-term vibe for equities than any Fed speaker except perhaps Warsh himself.

With that said, let’s take a look at the key US economic releases most likely to shape investors' thinking on the labor market, business activity, and sentiment this week:

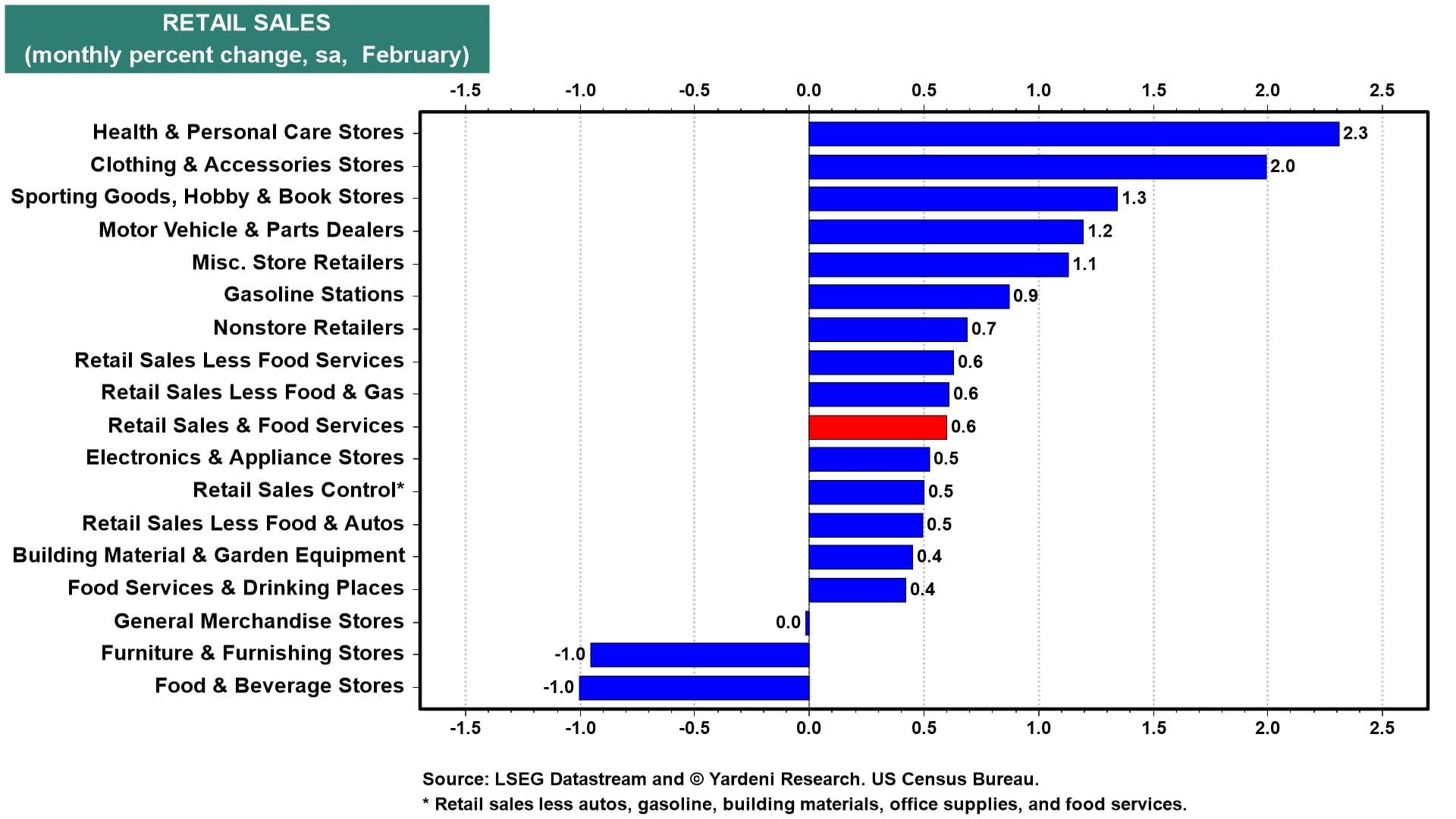

(1) Retail sales. March retail sales (Tue) will be the first hard data on consumers since the war started. Despite winter storms, February's category breakdown was unambiguously strong with health & personal care up 2.3%, clothing up 2.0%, and motor vehicles up 1.2%. Only furniture & furnishing stores and food & beverage stores were down that month (chart). The latter's weakness was probably weather related.

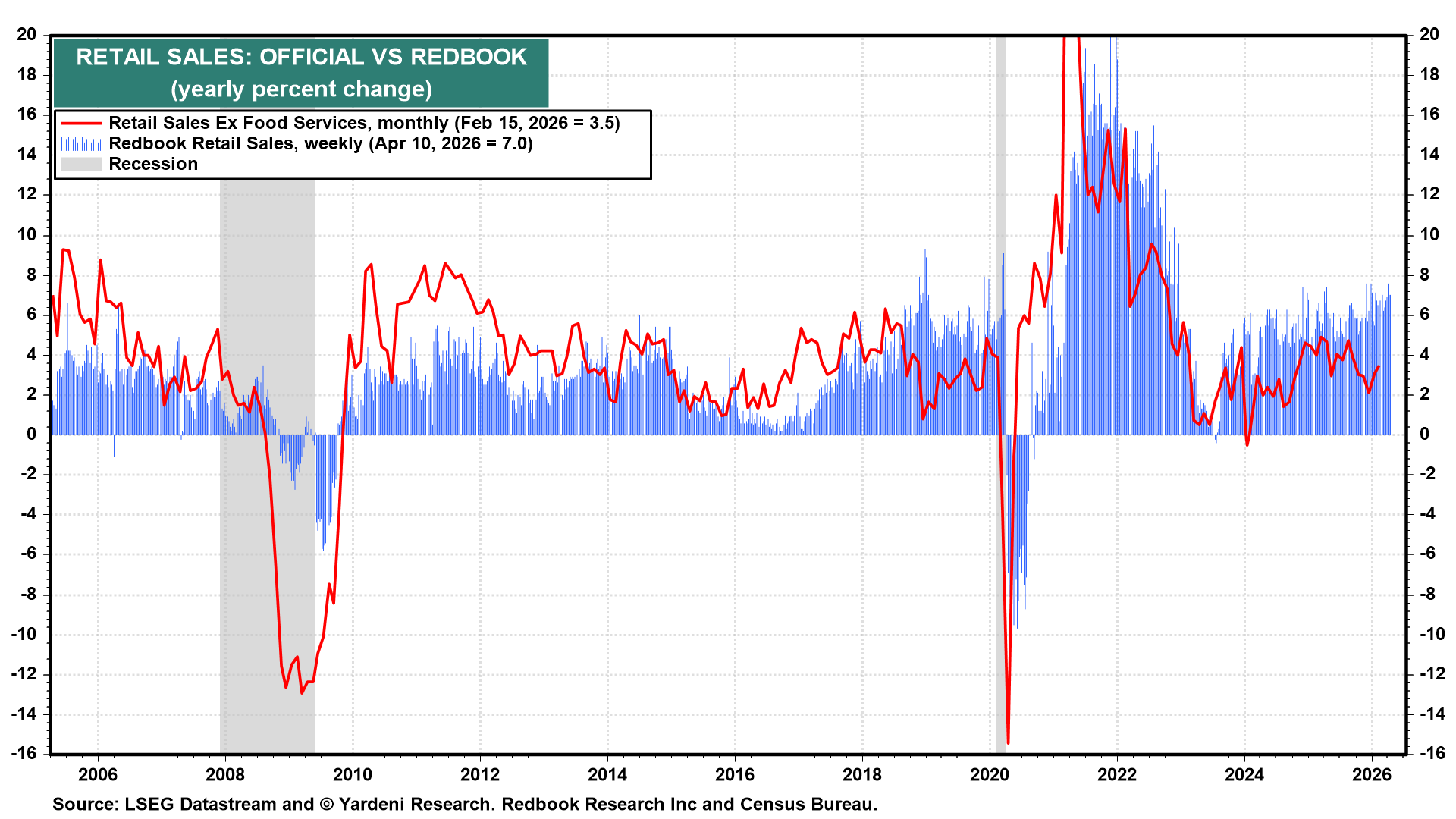

The weekly Redbook Retail Sales index suggests that the pace of consumer spending at retail stores remained solid during March and April (chart).

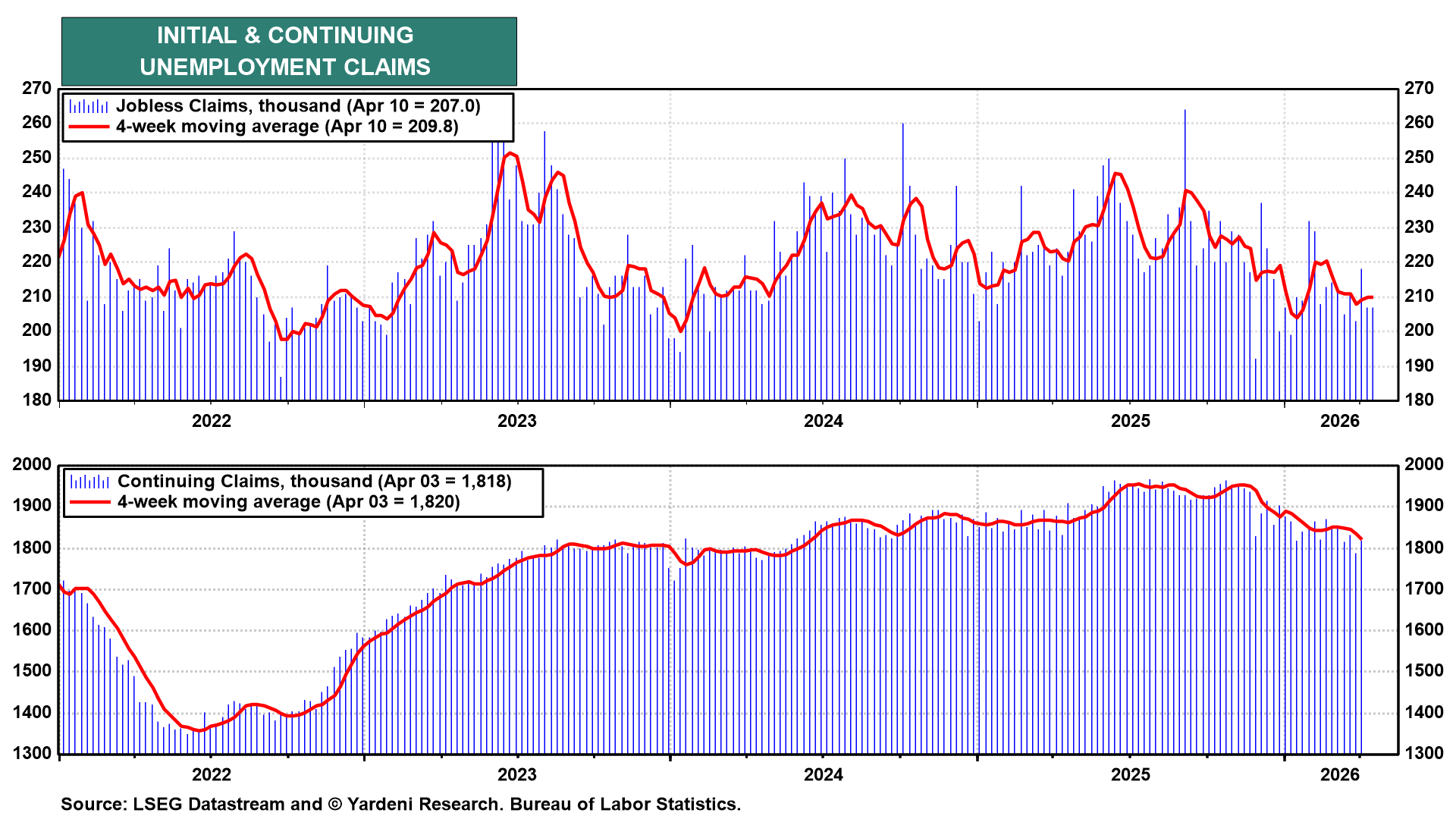

(2) Unemployment. Initial jobless claims fell to 207,000 for the week of April 10, with the four-week moving average edging up slightly to 209,800 (chart). Continuing claims ticked up to 1,818,000, though the trajectory still suggests that the duration of unemployment is shortening. Despite geopolitical uncertainties, most employers are not cutting their headcounts.

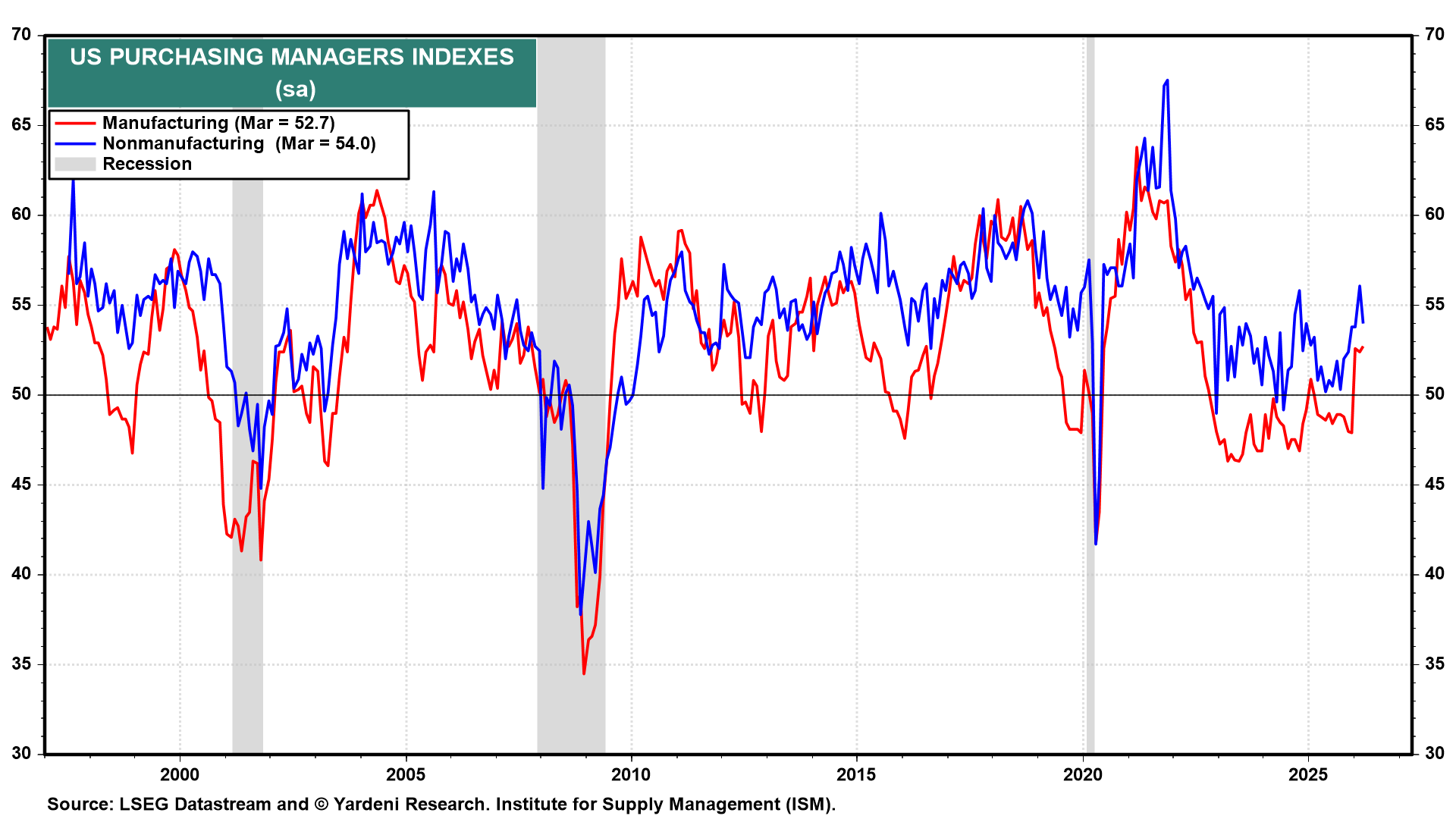

(3) Flash PMIs. The April flash PMIs (Thu) might hint at some war-related effects. March's final readings showed that manufacturing and non-manufacturing PMIs held comfortably above 50.0 at 52.7 and 54.0, respectively, and Thursday's flash will be the first April read on whether that resilience is holding (chart).

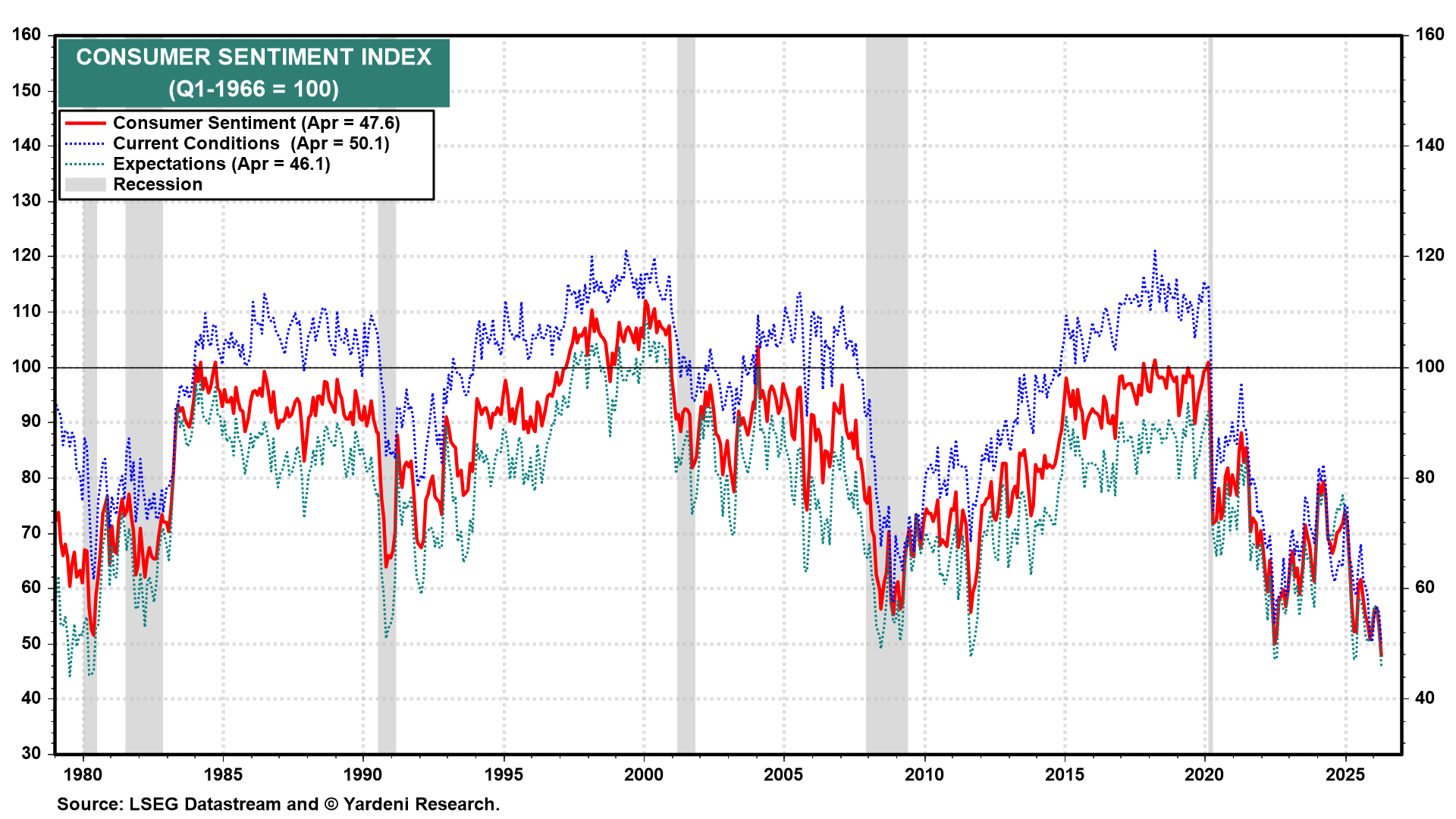

(4) Consumer sentiment. The University of Michigan will report its final April Consumer Sentiment Index reading on Friday. The preliminary print came in at 47.6, with current conditions at 50.1 and expectations collapsing to 46.1—levels last seen during the Great Financial Crisis (chart). Soaring gasoline prices are doing the damage. The revisions will tell us whether the preliminary read was peak anxiety or the beginning of a more persistent deterioration in sentiment. Given recent events, we wouldn't be surprised to see an uptick in sentiment.