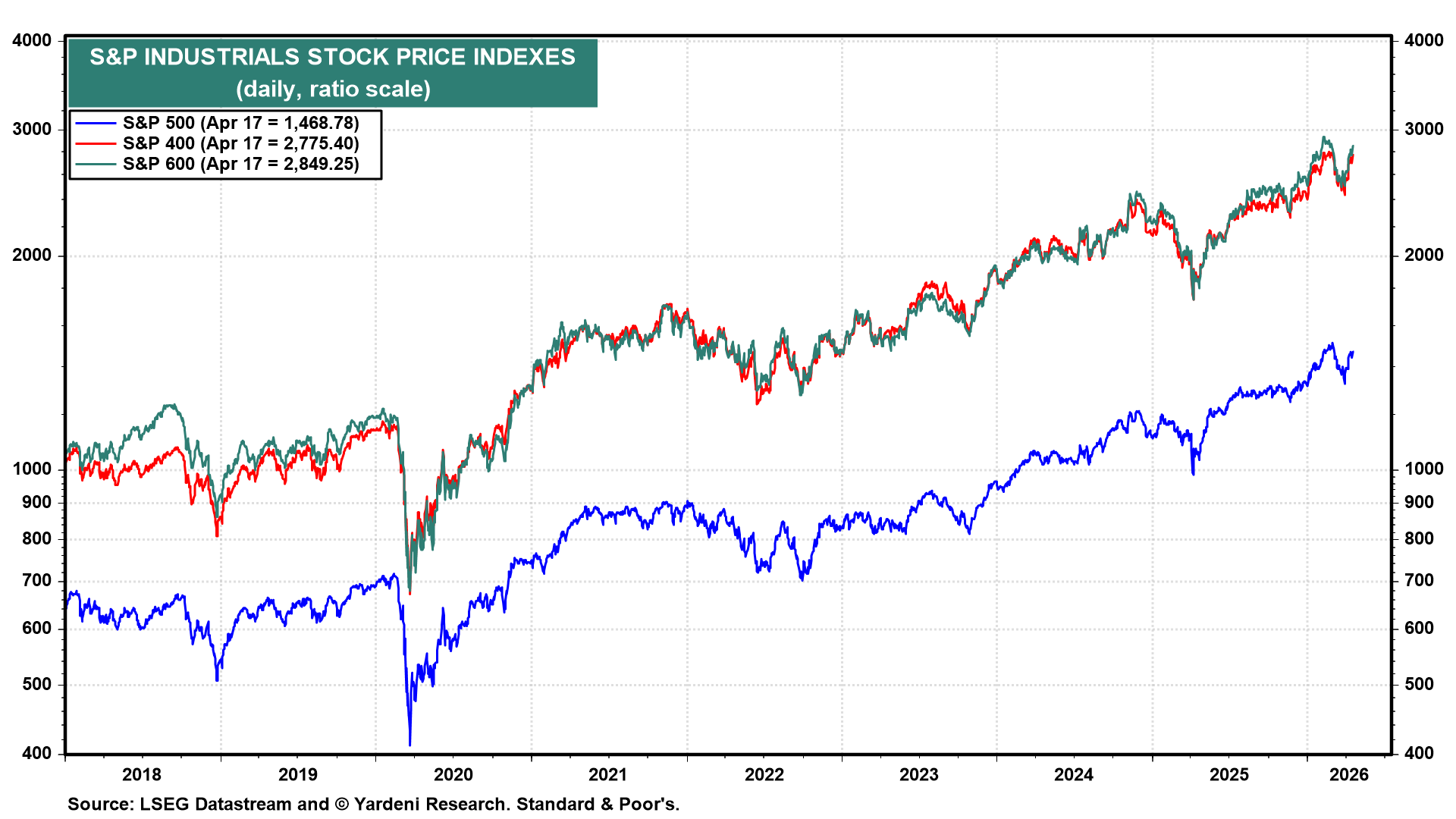

We continue to recommend overweighting the Industrials sectors in the S&P 500, the S&P 400, and the S&P 600. Granted, their valuation multiples are high, but so are their earnings growth rates. The sector's three major indexes all remain on solid uptrends that started in 2022 (chart).

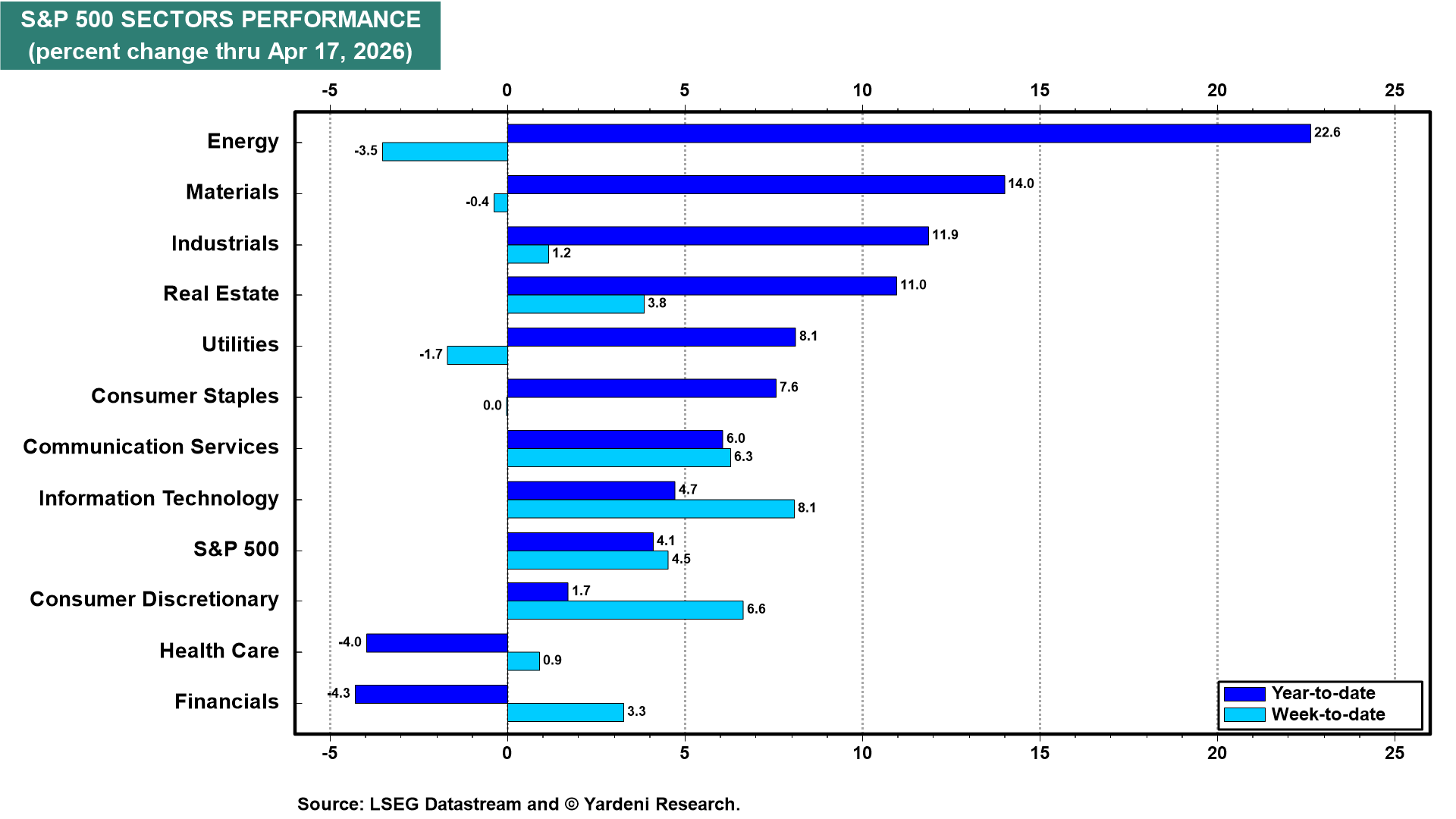

The S&P 500 Industrials sector is up 11.9% ytd, the third-best performing sector behind Energy and Materials (chart). Thursday's March industrial production report showed a 0.5% m/m decline. However, the decline was driven by weather-related utility output and a drop in motor vehicle production, which should rebound in April since auto sales were strong in March. The index remains near its all-time high and is up 0.7% y/y.

Onshoring, supply-chain diversification, defense rearmament, and the energy infrastructure demands of AI are creating a multi-year capex boom that the sector hasn't seen in decades. It's no coincidence that the S&P 500’s three best-performing sectors so far this year are Energy, Materials, and Industrials. The structural story is compelling.

Consider the following:

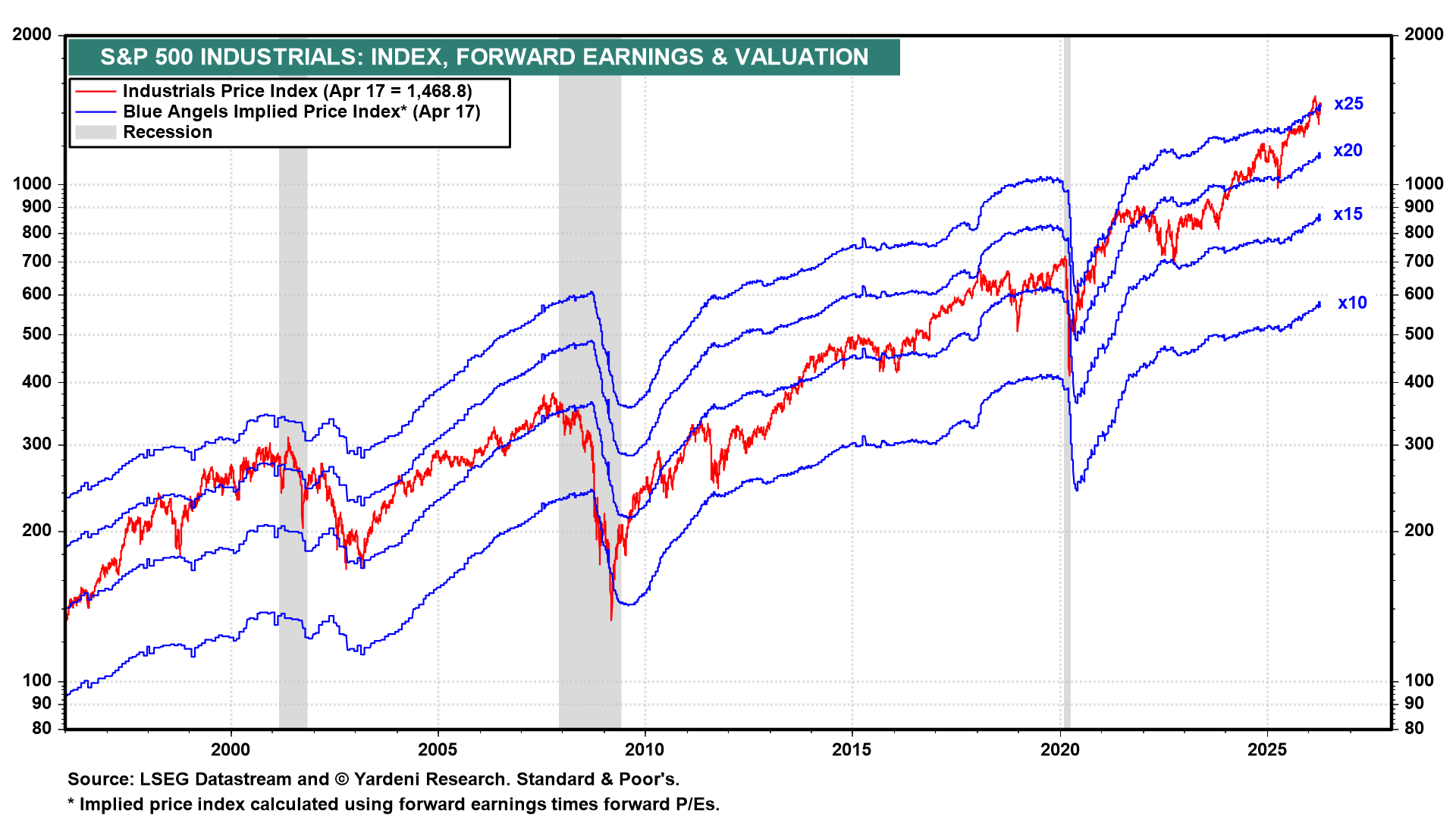

(1) The forward earnings per share of the S&P 500 Industrials sector has been rising at a faster pace since the beginning of the year to fresh record highs (chart). No wonder that the sector's forward P/E has been doing the same.

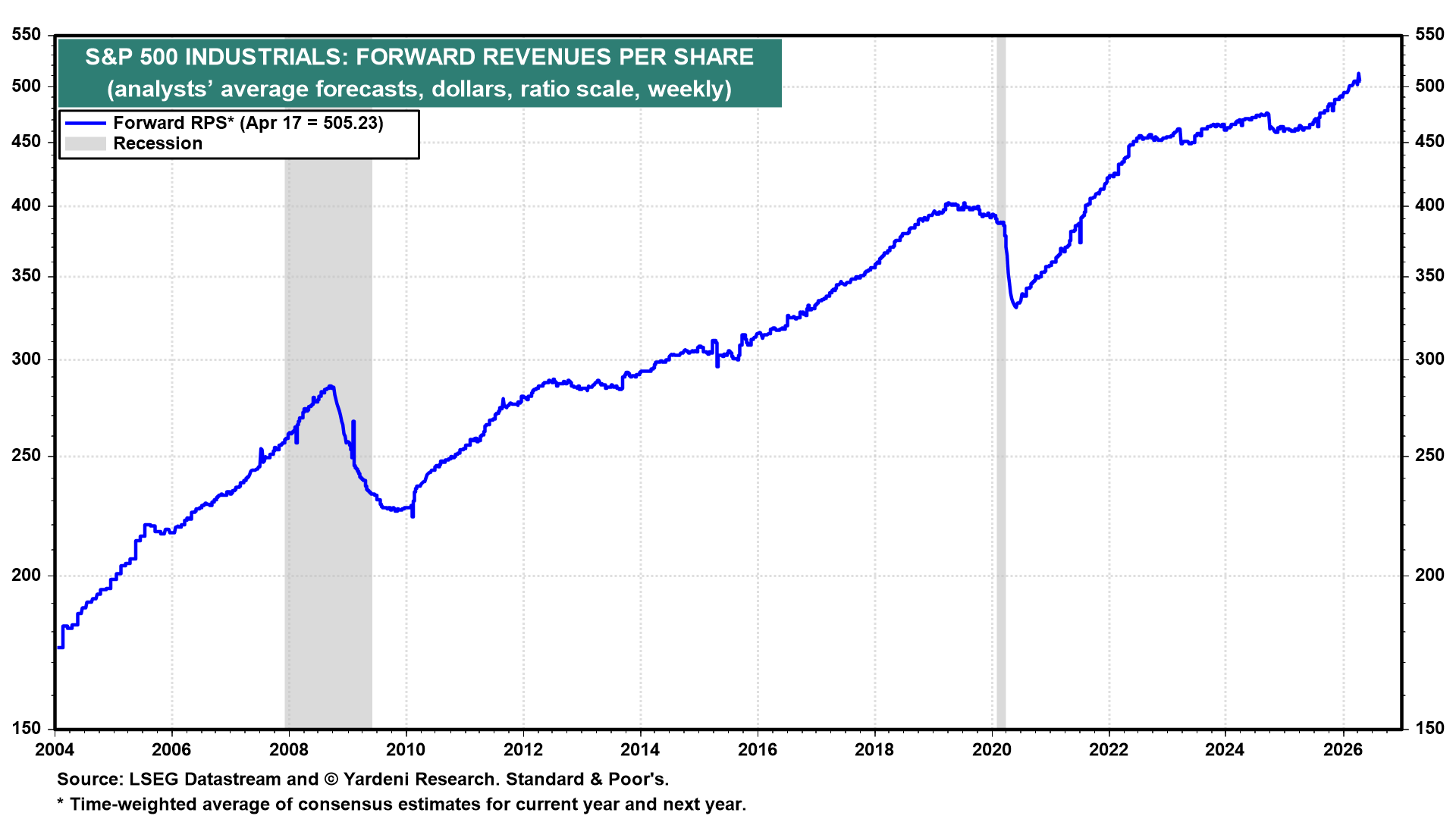

The sector's forward revenues per share has been rising to record highs since last year (chart).

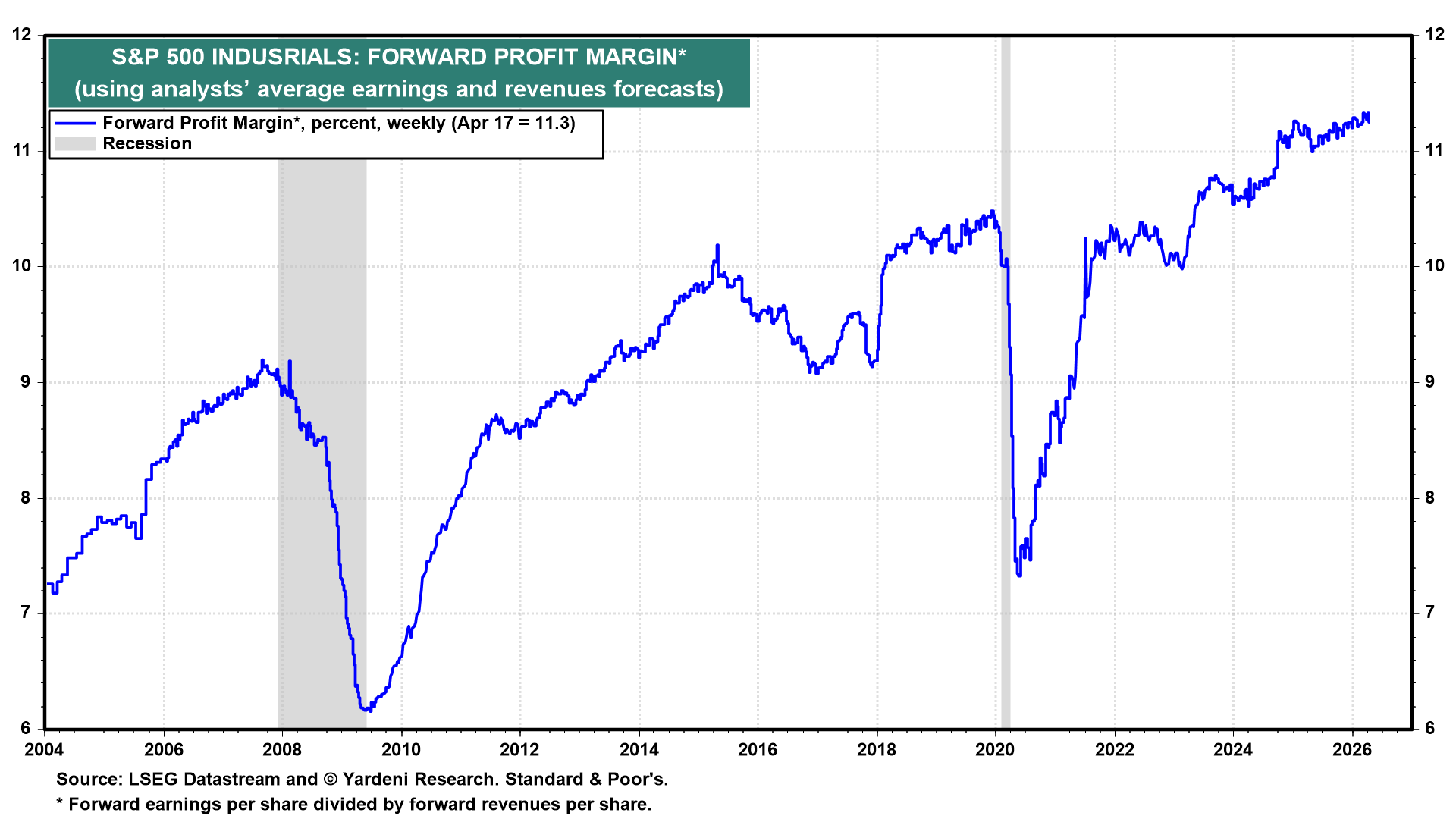

Furthermore, the forward profit margin of the sector has also been making new highs since late last year (chart).

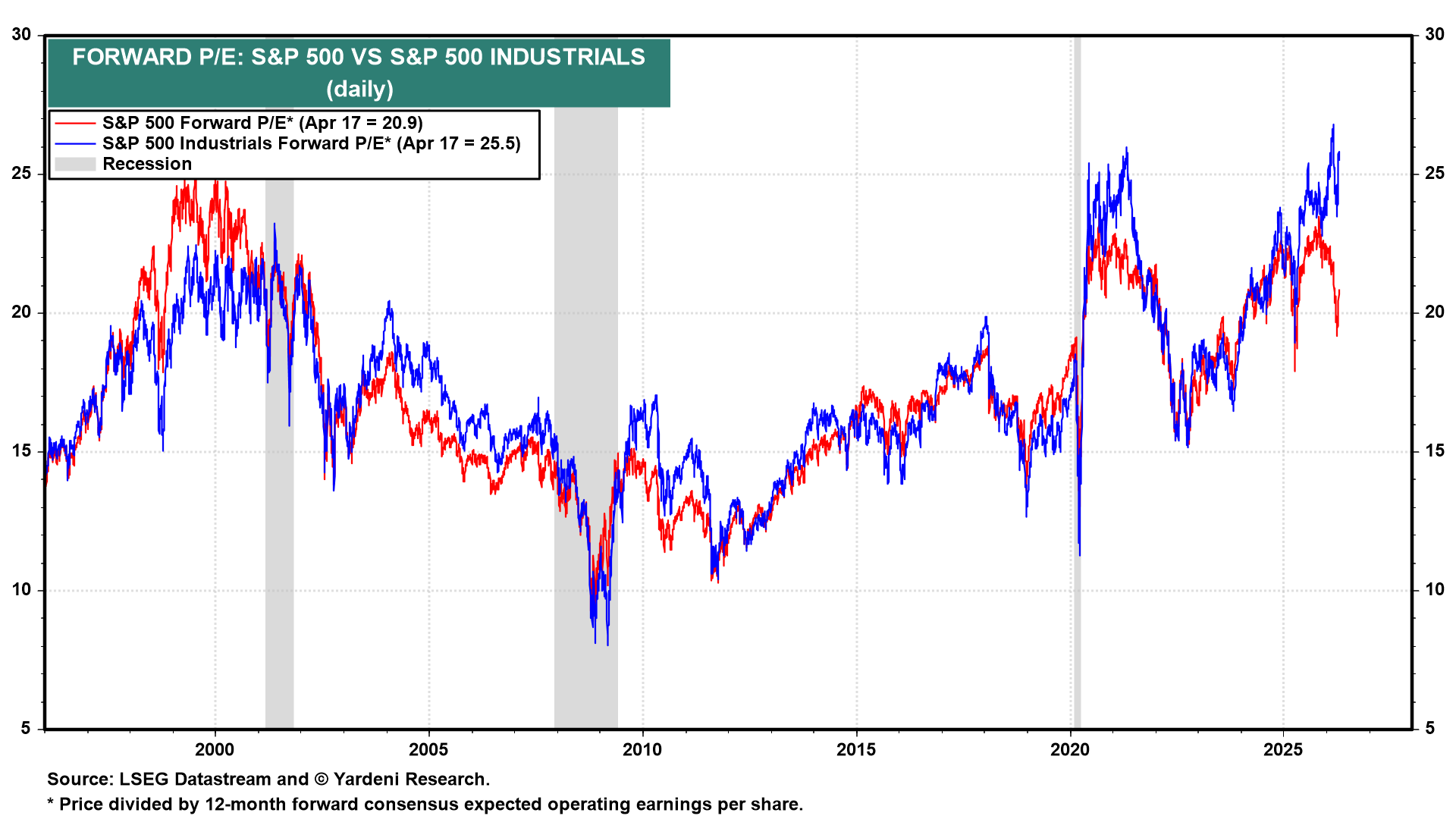

(2) The sector's forward P/E has increased from roughly 16.0 in late 2022 to 25.5 today, compared with 20.9 for the broader index currently (chart). Industrials has historically traded in line with or below the broader market multiple, so the 4.6ppt premium is unusual. The sector has been repriced as a structural play on AI, onshoring, and domestic capacity investment.

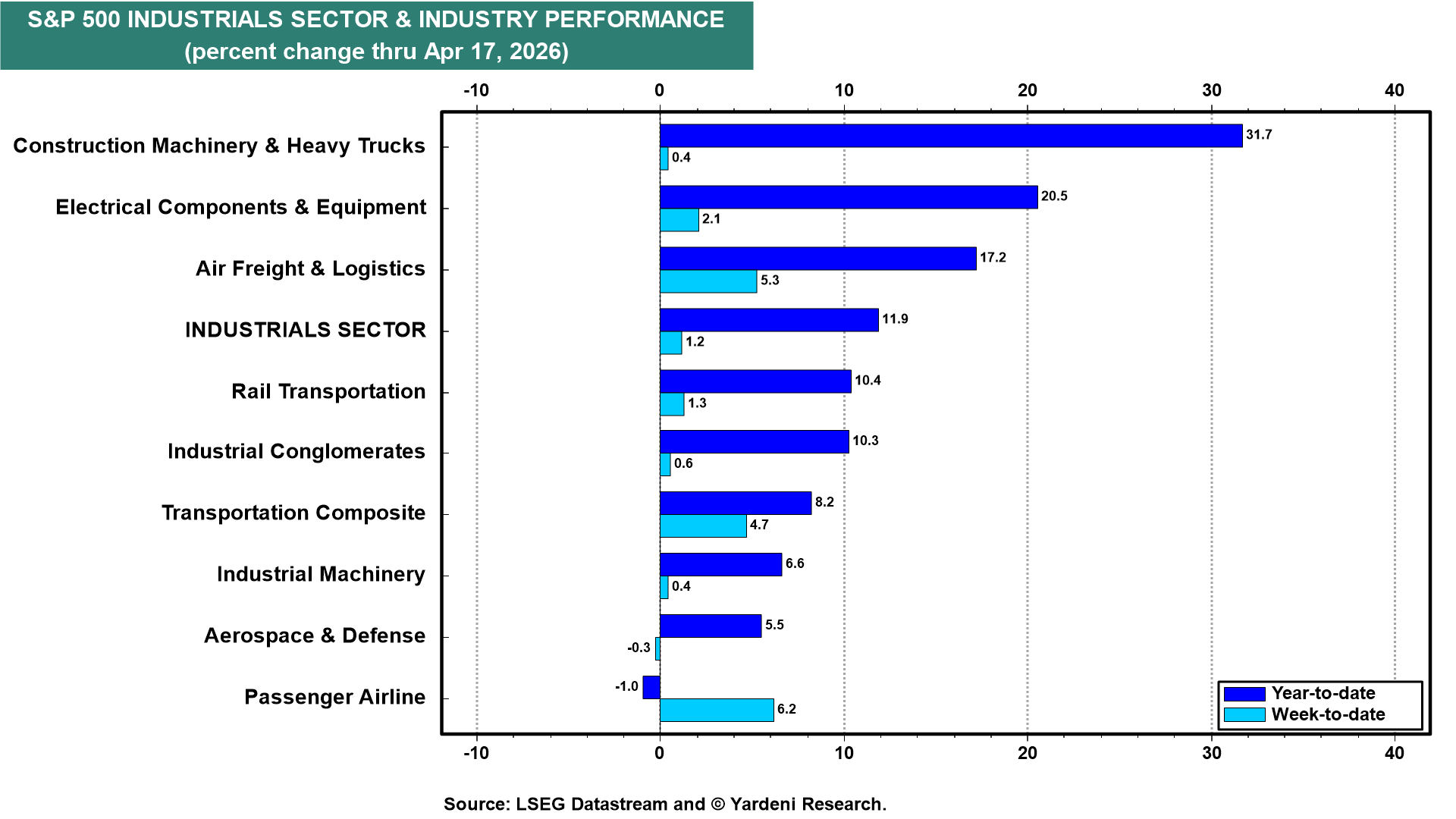

(3) The stock price indexes of most of the sector's major industries are soaring: Construction Machinery & Heavy Trucks industry is up 31.7% ytd, Electrical Components & Equipment is up 20.5%, and Air Freight & Logistics is up 17.2% (chart). They are the onshoring and electrification trades. The drop in oil prices late last week gave a big boost to Transportation, led by Passenger Airline.

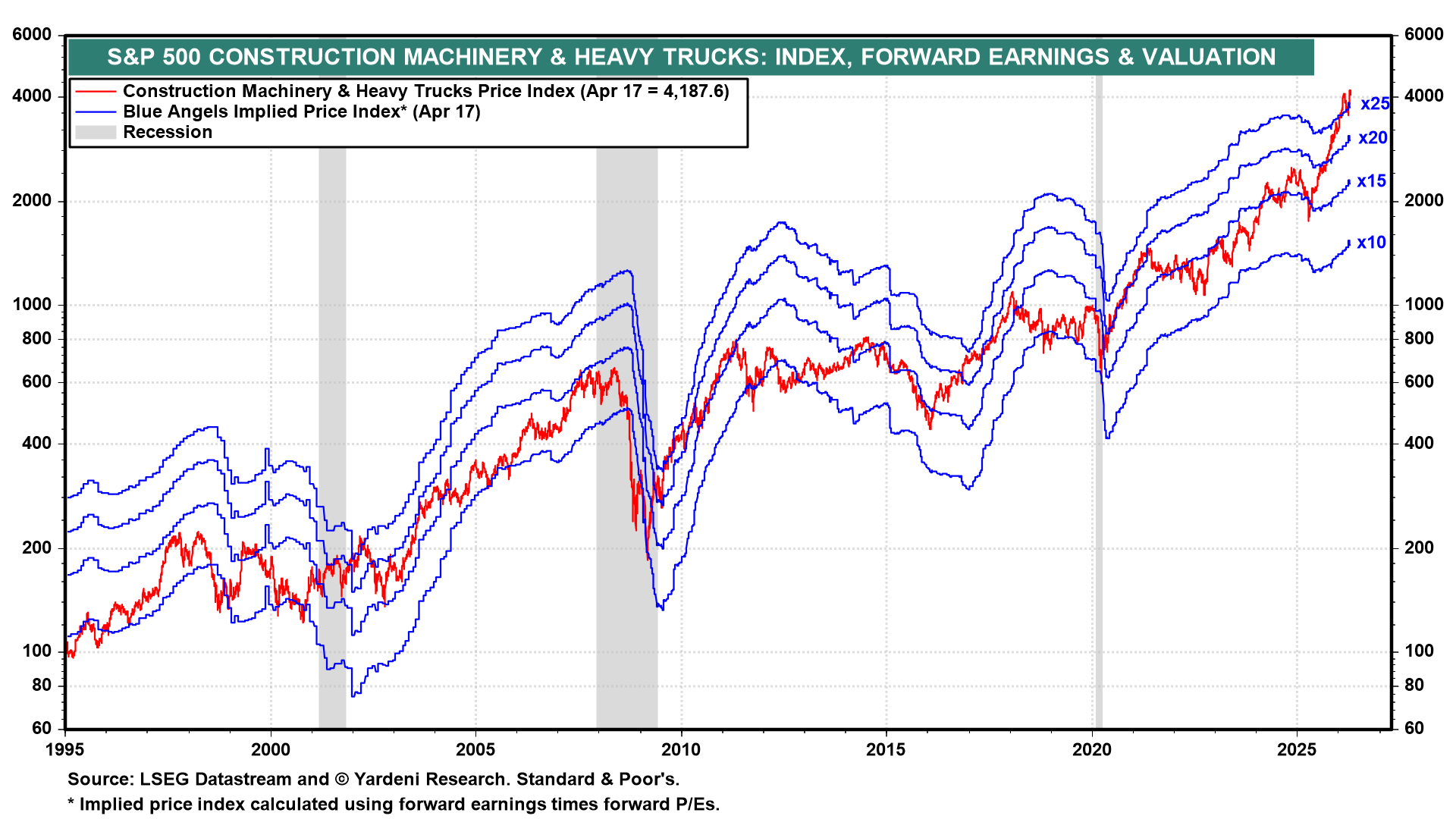

(4) The forward earnings of the Construction Machinery & Heavy Trucks industry index (comprising CAT, CMI, PCAR, WAB shares) has been rebounding strongly to record highs since spring 2025, which has boosted the forward P/E from under 15 to over 25 (chart). This industry has been propelled by the data center and manufacturing building booms.

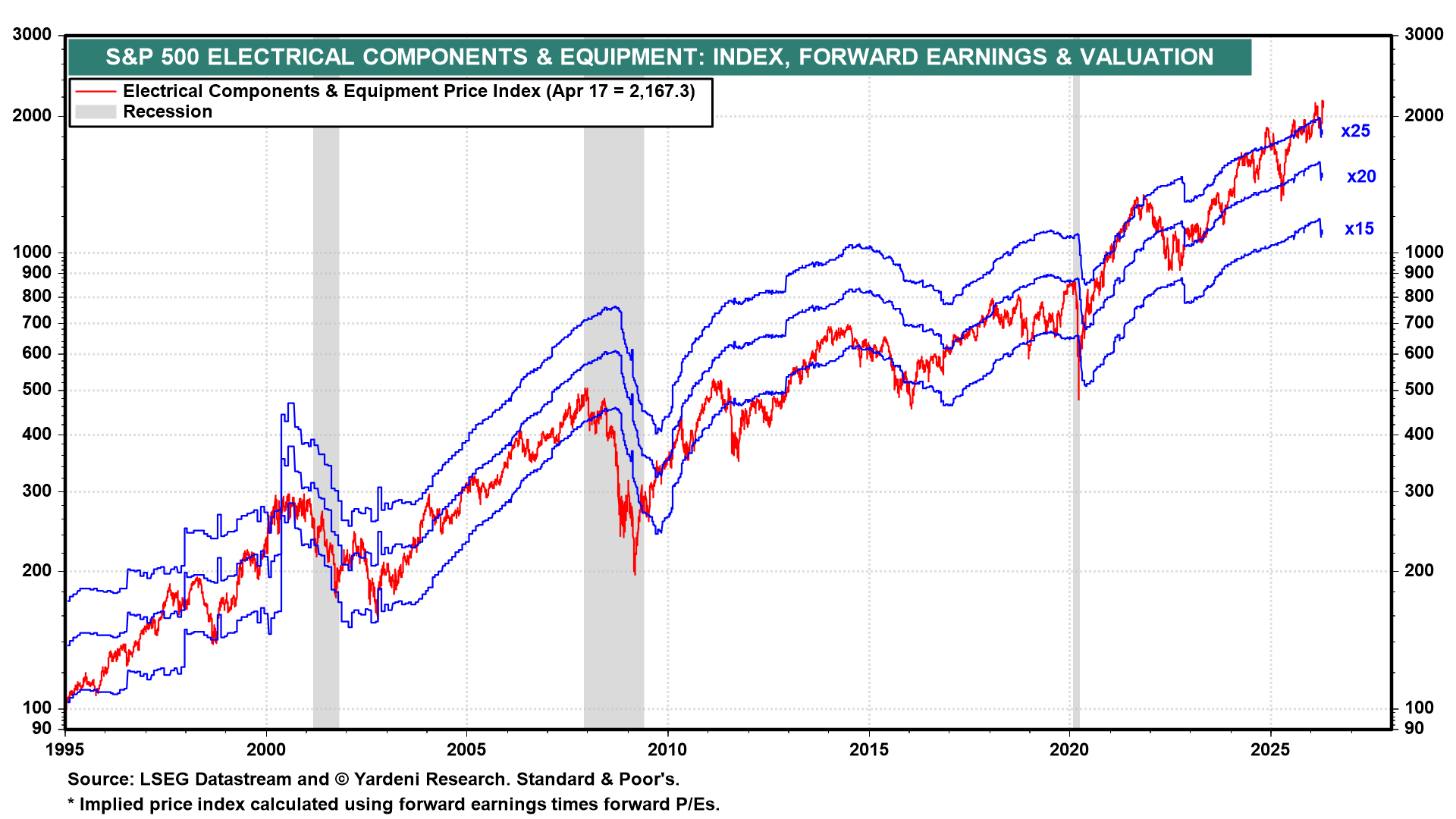

(5) The S&P 500 Electrical Components & Equipment (AME, EMR, ETN, GNRC, HUBB, ROK, VRT) index tells a similar story: AI needs lots of power. Forward profit margins have surged to 17.8%, more than doubling since the Great Financial Crisis. This industry is the picks-and-shovels play on the AI data center buildout and power grid modernization. The market is paying a hefty multiple, 28.7 times forward earnings, for the structural growth story (chart). (There was a one-time reset of the industry’s forward earnings when Vertiv was added during quarterly reindexing in March.)

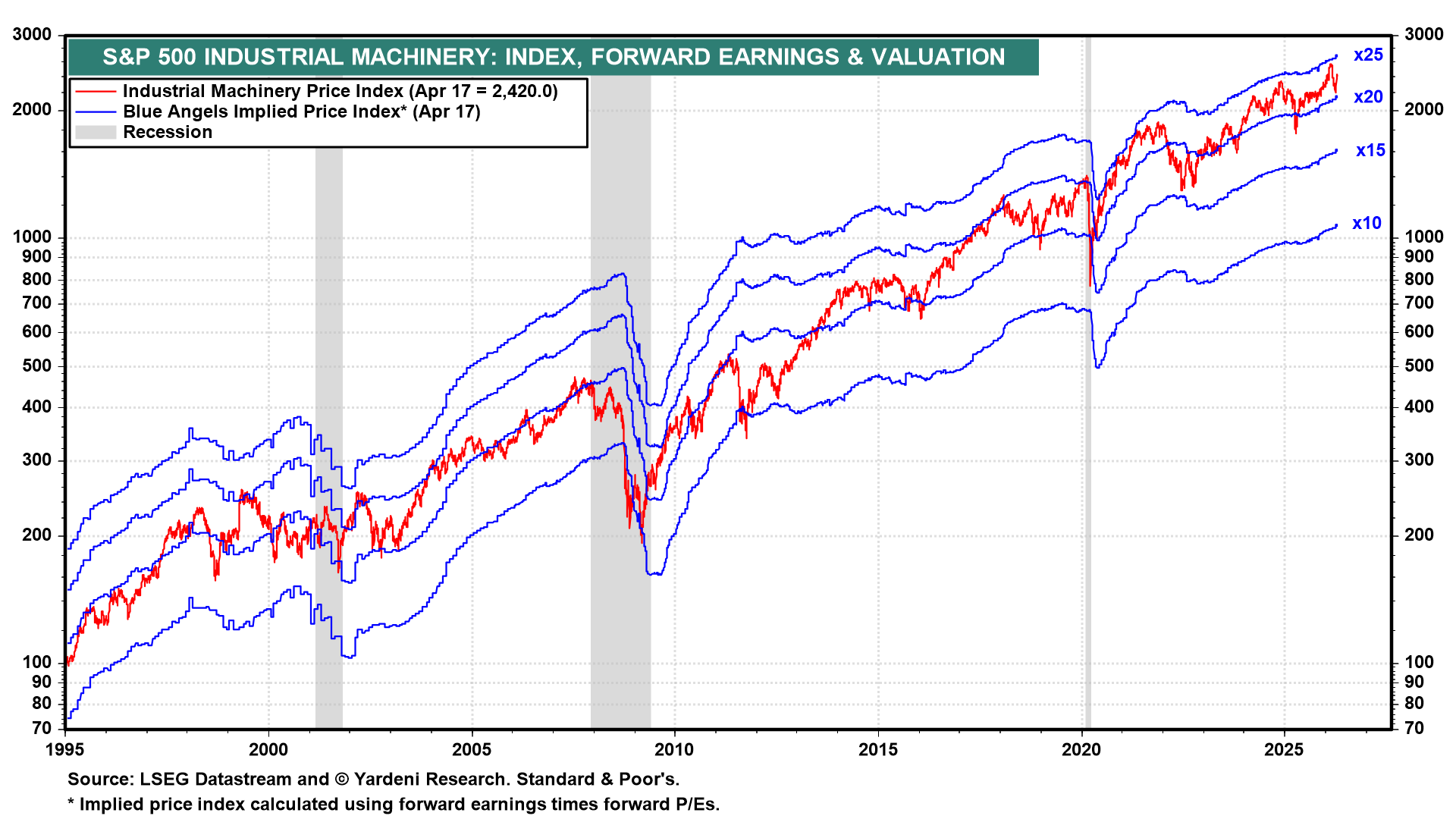

(6) Industrial Machinery (DOV, FTV, IEX, IR, ITW, NDSN, OTIS, PH, PNR, SNA, SWK, XYL) rose to record forward earnings in mid-April as both forward revenues and the forward profit margin (at 16.0) hit record highs (chart). The forward P/E is currently 22.2.

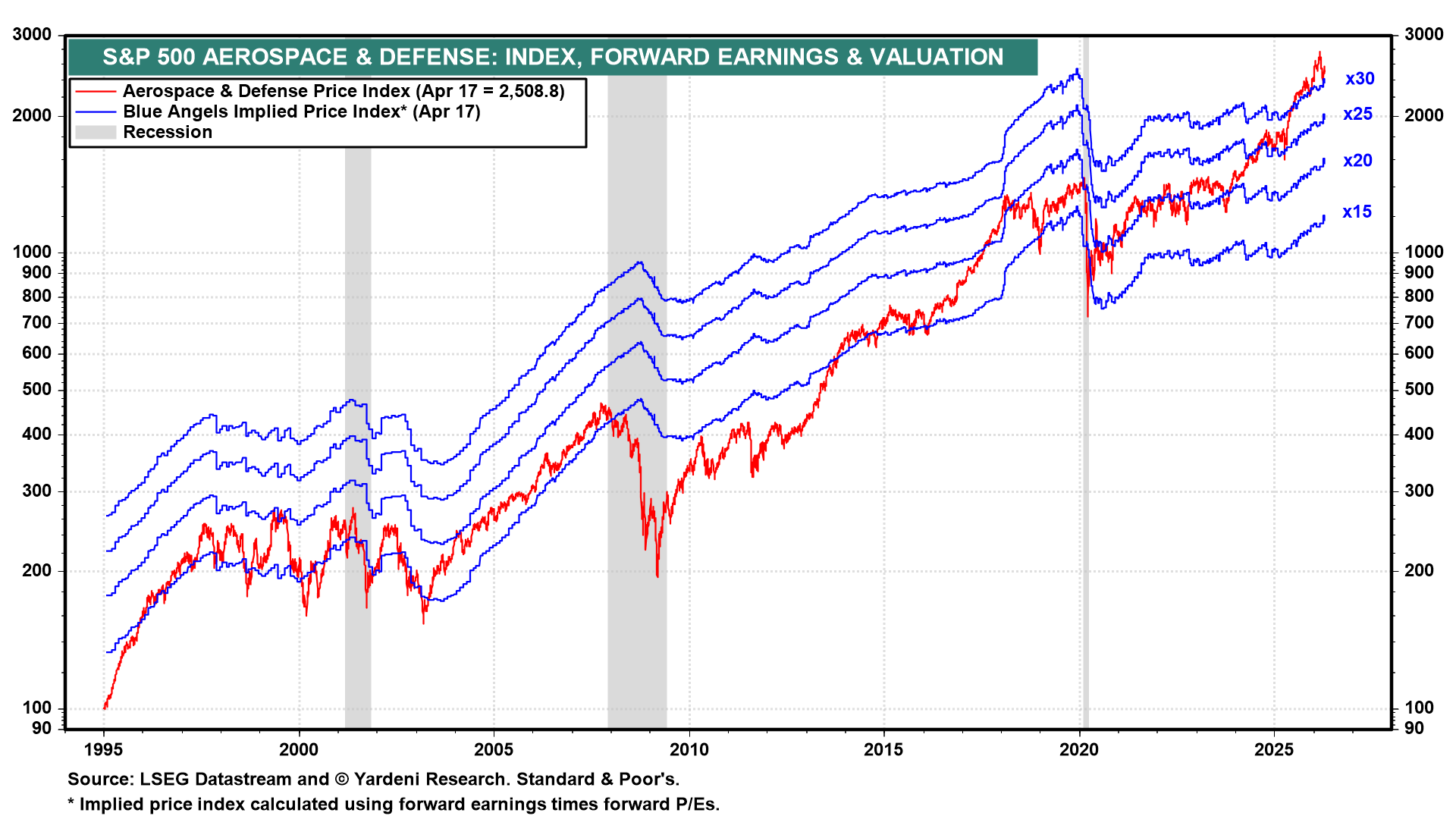

(7) Aerospace & Defense (AXON, BA, GD, GE, HII, HWM, LHX, LMT, NOC, RTX, TDG, TXT) now has a forward P/E of 32.5, well above its historical 15-20 range (chart). Geopolitical conflicts are boosting defense spending, driving up forward revenues and earnings. The forward profit margin remains relatively low at 8.6% currently.

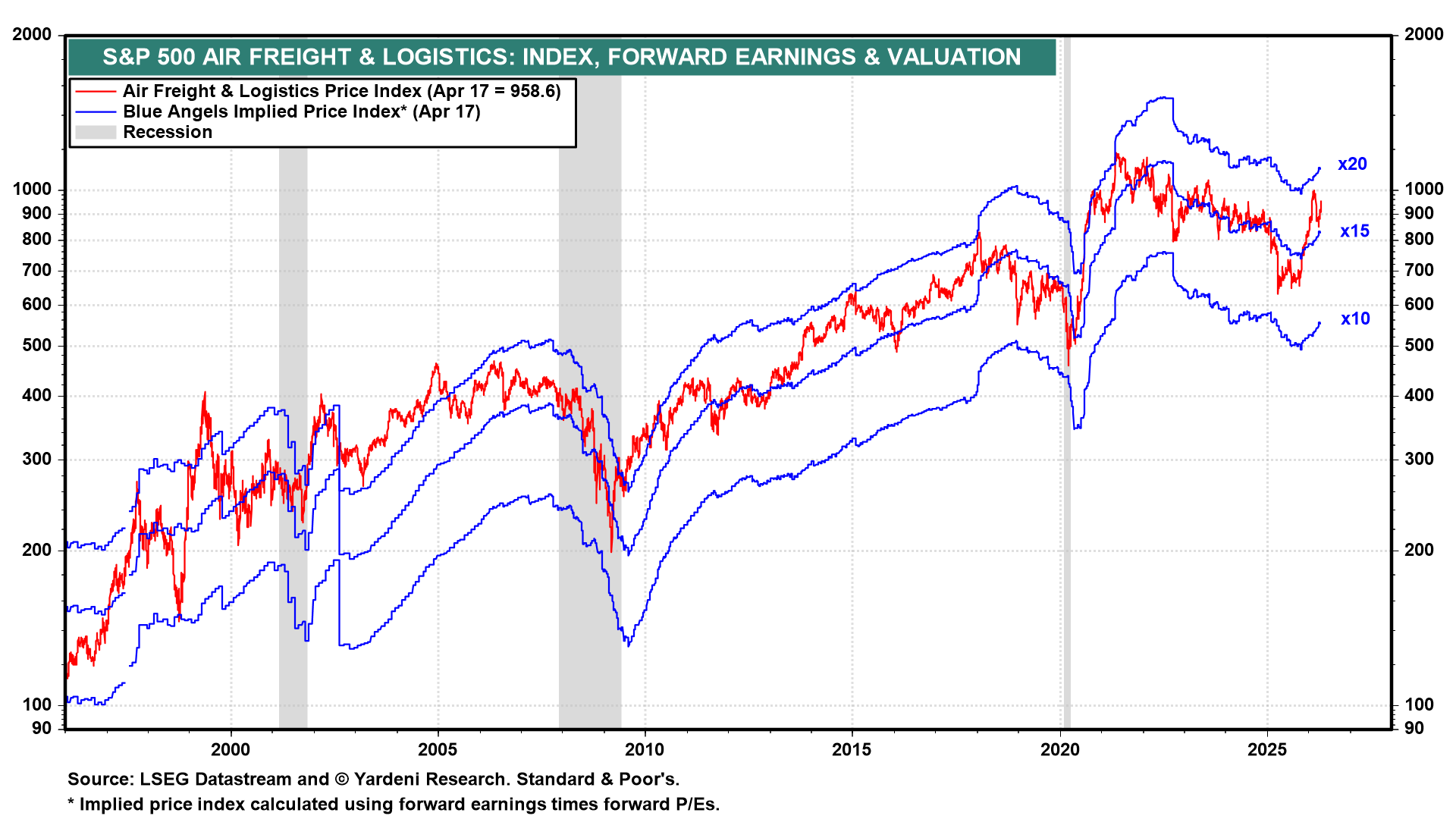

(8) Air Freight & Logistics (CHRW, EXPD, FDX, UPS) has been in a downward trend since 2022. That may be over, as the industry's stock price is rising on a recent rebound in forward earnings (chart).