When Kaiser Wilhelm II's Germany and Tsar Nicholas II's Russia squared off in the summer of 1914, the London Stock Exchange closed for five months. The New York Stock Exchange shut for four months. Investors assumed a continental war would be a calamity. World War I was a calamity for sure. However, by 1915, the NYSE had reopened, and the DJIA more than doubled by late 1916.

Last week, we wrote that the financial markets may be learning to live with the war in the Middle East, much as they learned to live with the war between Ukraine and Russia. We will get a test of that notion on Monday, given that crude oil prices are up around $5 a barrel this evening amid renewed tensions in the Strait of Hormuz.

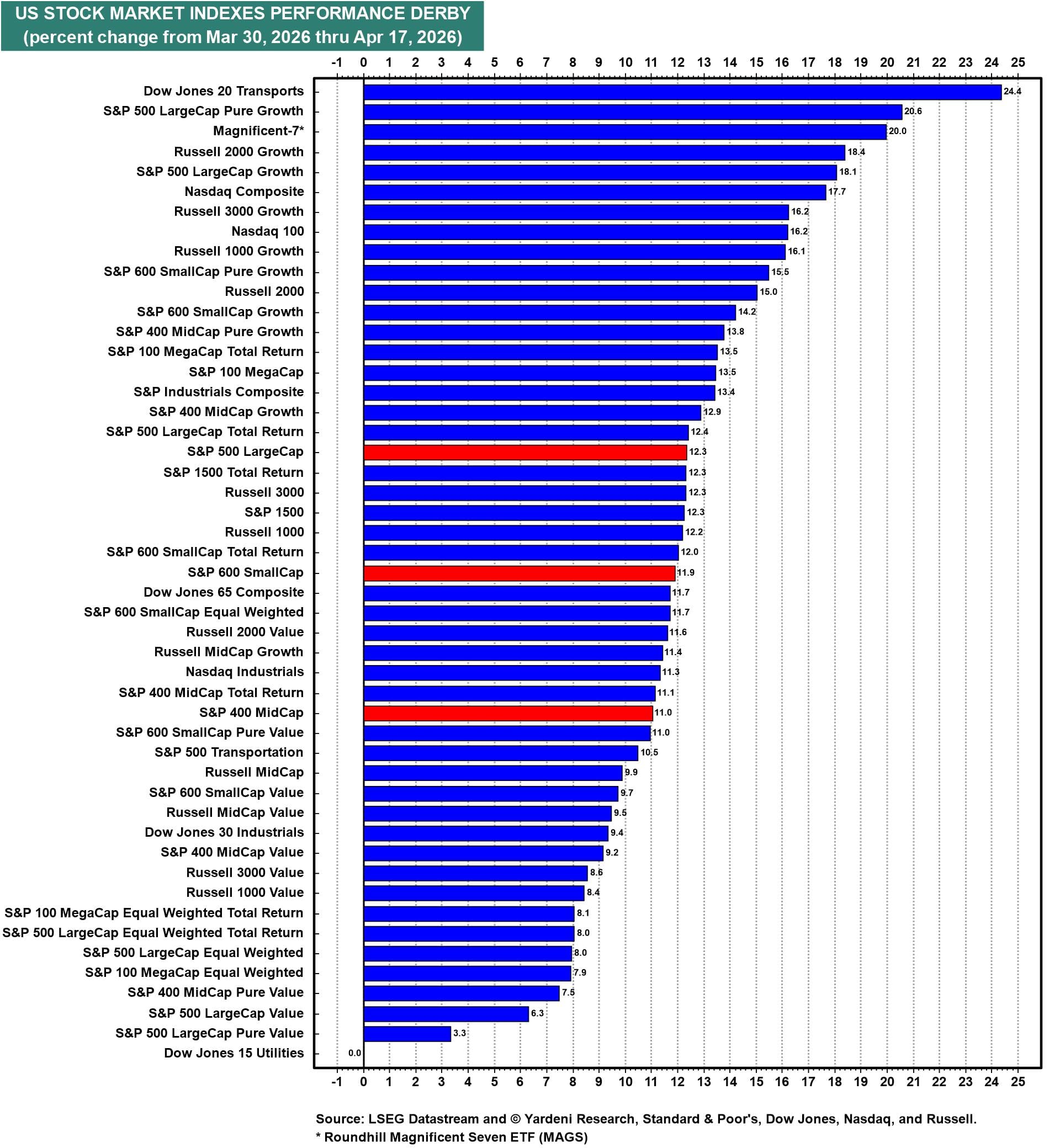

The S&P 500 is up 12.3% to a new record high over the past three weeks since it bottomed on March 30. The leader board reads like a risk-on checklist (chart). Leading the way have been Growth and Momentum stocks that fell hardest during the pullback from January 27 to March 30. DJTA is up 24.4% since March 30. LargeCap Pure Growth is up 20.6%. The Magnificent-7 is up 20.0%. SmallCaps and MidCaps are participating too. This is a broad melt-up. For now, animal spirits are back in the stock market.

The Nasdaq 100 Relative Strength Index (RSI) has seen the fastest oversold-to-overbought transition in its 40-year history over this period (chart). The war may not be over, but the stock market is trading as though it will be soon. We agree.

We called the bottom after the strong close on March 31, and now our 7,700 target for the S&P 500 looks achievable by the end of this year, if not sooner. But, again, let's see how the market trades on Monday. For now, we are back to 60% odds for our Roaring 2020s base case, 20% for a Meltup, and 20% for a Meltdown.

Now, let's look under the hood at the resilient earnings fundamentals which are powering this bull market:

(1) While the Magnificent-7 have led the rally since the March 30 bottom, stock market breadth should broaden, given that earnings breadth remains strong. The share of S&P 500 companies with positive 12-month forward revenue growth is 86.6%, and the share with positive forward earnings growth is 81.8% (chart). Both readings are near previous cycle highs.