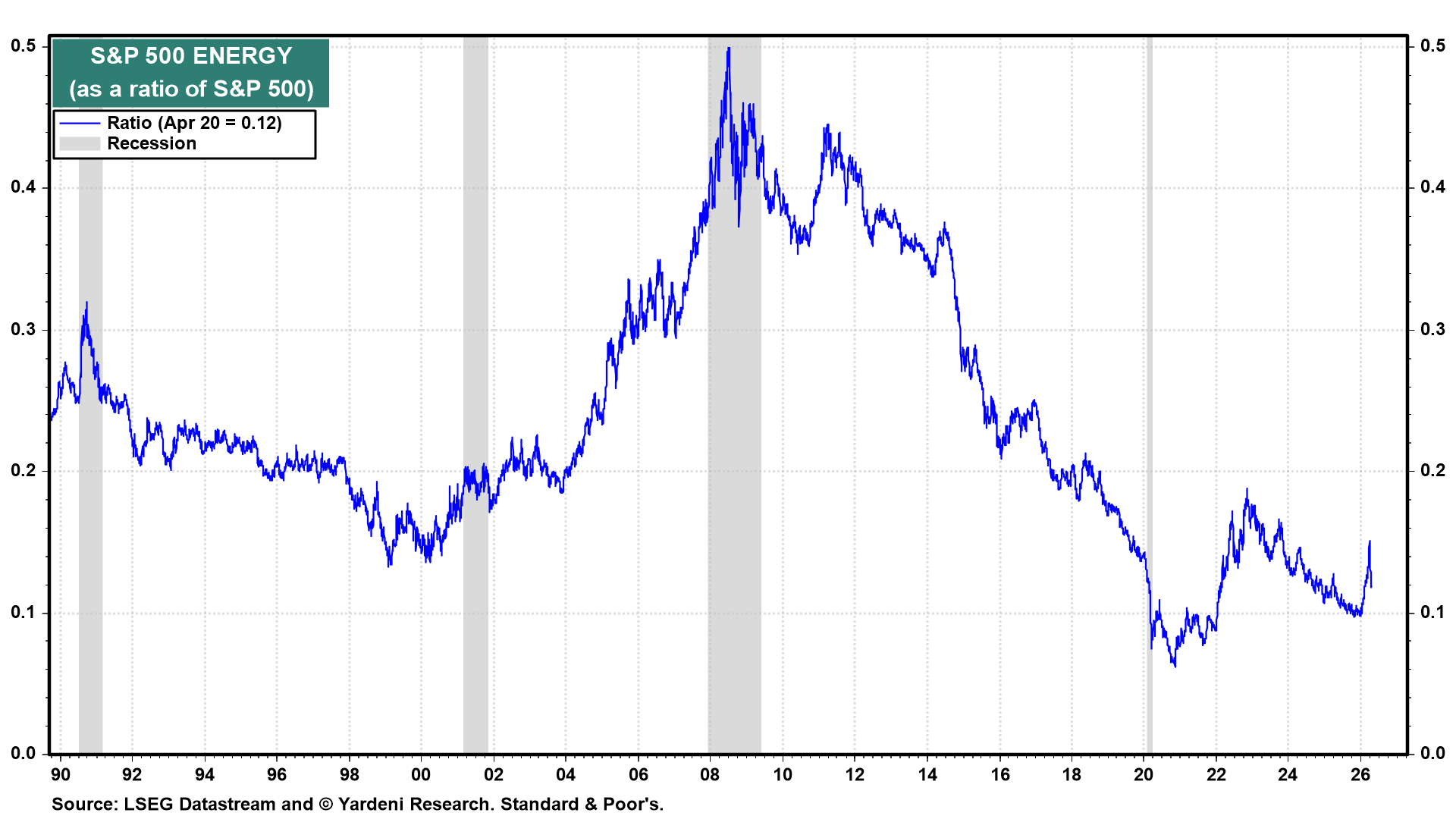

We gave up on the S&P 500 Energy sector a couple of years ago. It has been underperforming the S&P 500 since late 2022 (chart). As a result of the latest war in the Middle East, it has been an outperformer since the beginning of this year through Friday, March 27. The sector has been underperforming again since then, when President Donald Trump suggested that the war would end soon. We are inclined to use the recent selloff to overweight the sector.

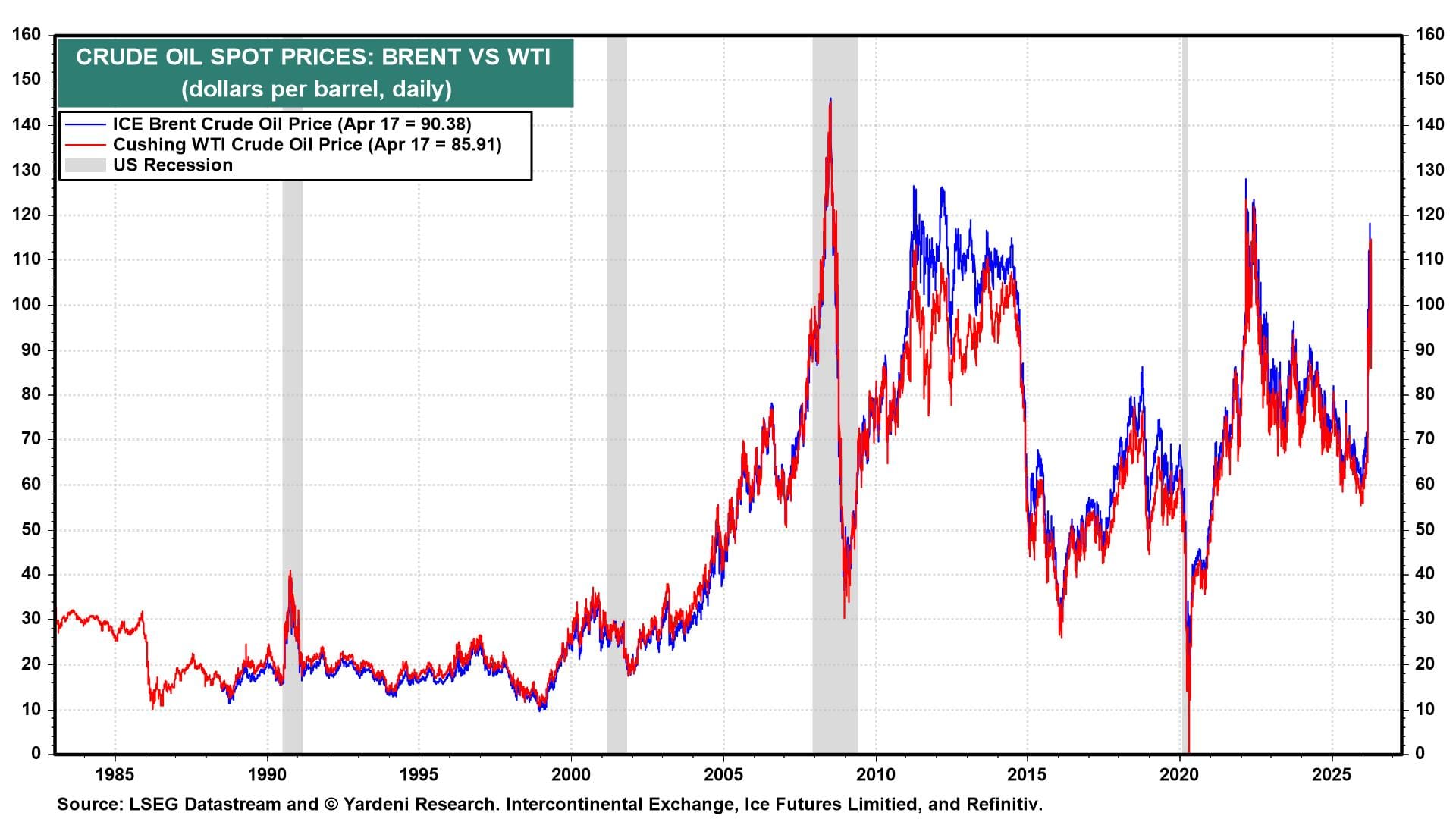

That's because we reckon that the price of a barrel of Brent crude oil will fluctuate between $75 and $95 once the war ends. We don't think it will fall back to the pre-war range of $55-$75 anytime soon (chart). Importantly, physical damage to energy infrastructure in the countries around the Arabian Gulf, combined with fundamental changes in maritime insurance and transit confidence, means that even a full reopening of the Strait of Hormuz would not immediately restore normal flows. The supply shock is likely to have a long tail.

Of course, if the war isn't over, then overweighting the S&P 500 Energy sector makes even more sense. The current two-week ceasefire is scheduled to end on Wednesday evening, April 22. Iran refuses to engage in another round of negotiations unless the US ends the blockade of Iran's ports.

Let's consider the implications of a $75-$95 oil price to the US economy, the domestic oil industry, and oil stock prices:

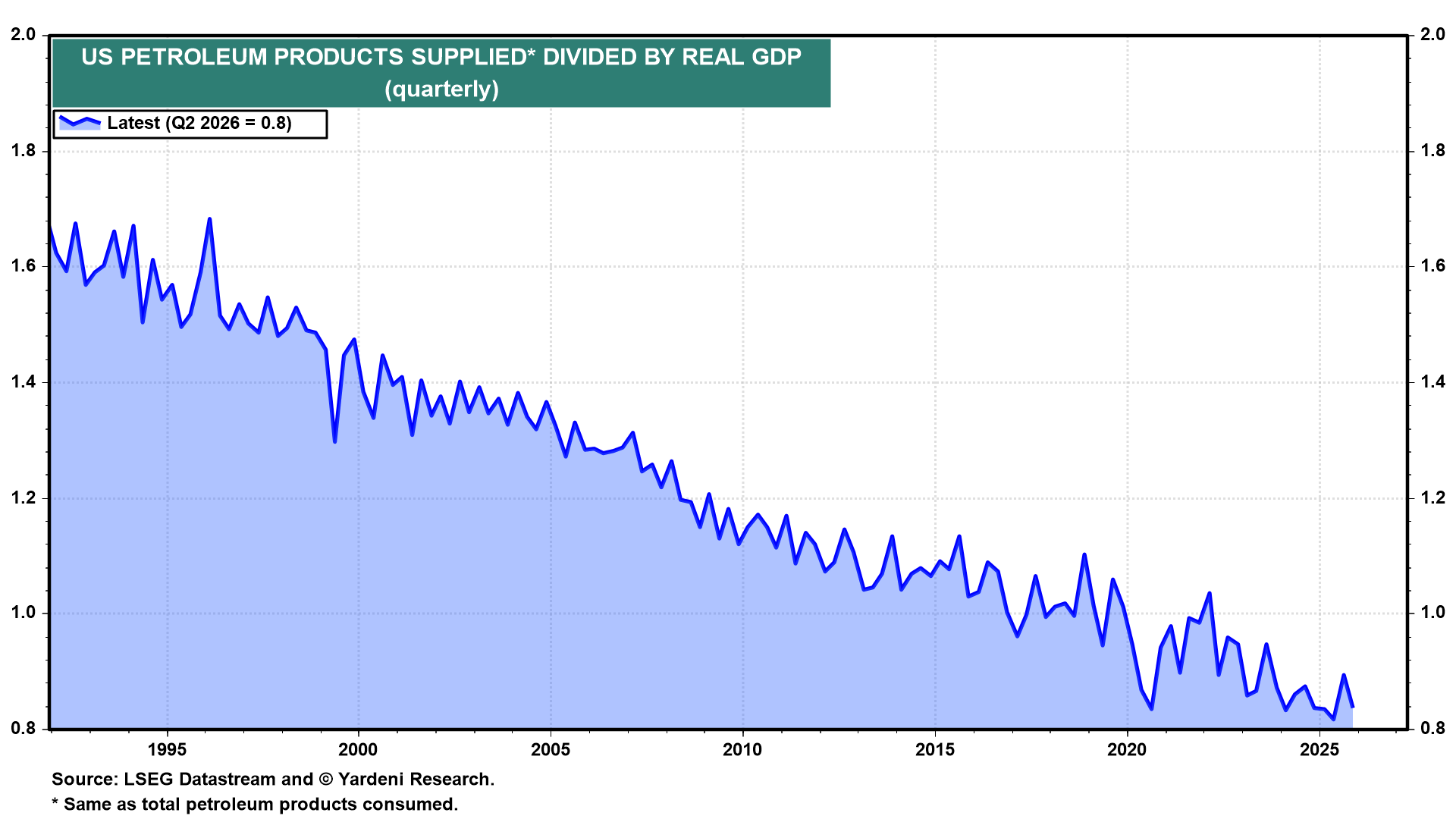

(1) US economy. The US economy is far better equipped to absorb oil price shocks than it was many years ago. The ratio of US petroleum products supplied (a measure of physical demand) to US real GDP has been in a secular downtrend since the early 1990s (chart). The economy now requires roughly half as many petroleum inputs to generate the same unit of output as it did in the early 1990s.

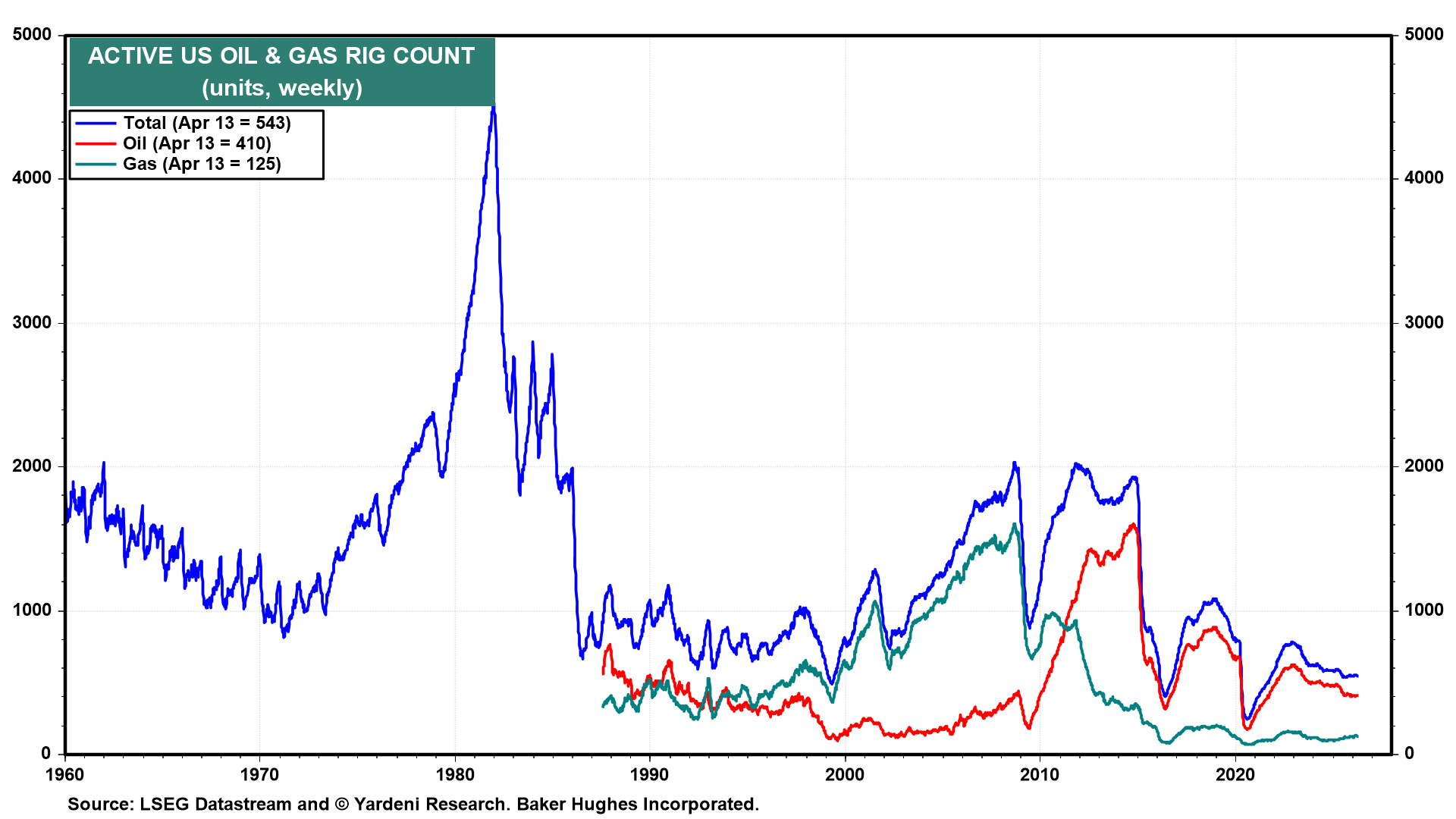

(2) US oil industry. The US energy sector has undergone a quiet structural revolution over the past four decades. The active rig count peaked in the early 1980s and has never come close to those levels since, reflecting a fundamentally leaner and more technologically advanced industry that today wrings far more production from each well than at any prior point in history.

US domestic production has climbed relentlessly, exceeding domestic petroleum consumption in 2023 (chart). This has reduced US vulnerability to geopolitical supply shocks. US production is best measured as oil field crude output (currently 13.6 mbd) plus natural gas plant liquids and renewable fuels (currently 10.0 mbd).