The unresolved Middle East conflict will remain center stage this week. It is having an immediate impact on energy prices in the United States. The US blockade of the Strait of Hormuz will push prices up again at the start of the week. The impact on the US inflation pipeline remains the dominant macroeconomic theme, ahead of Tuesday's March PPI release.

A relatively quiet week on the economic data front means attention will also fall heavily on the Talking Fed Heads, including Barr, Barkin, Collins, Goolsbee, Bowman, Williams, and Waller, as the blackout period for public speaking approaches. ECB President Lagarde speaks on Tuesday and BoE Governor Bailey on Wednesday, adding an international dimension to the central bank narrative.

Here are the key US economic releases most likely to shape investors' thinking on inflation, the labor market, and business activity this week:

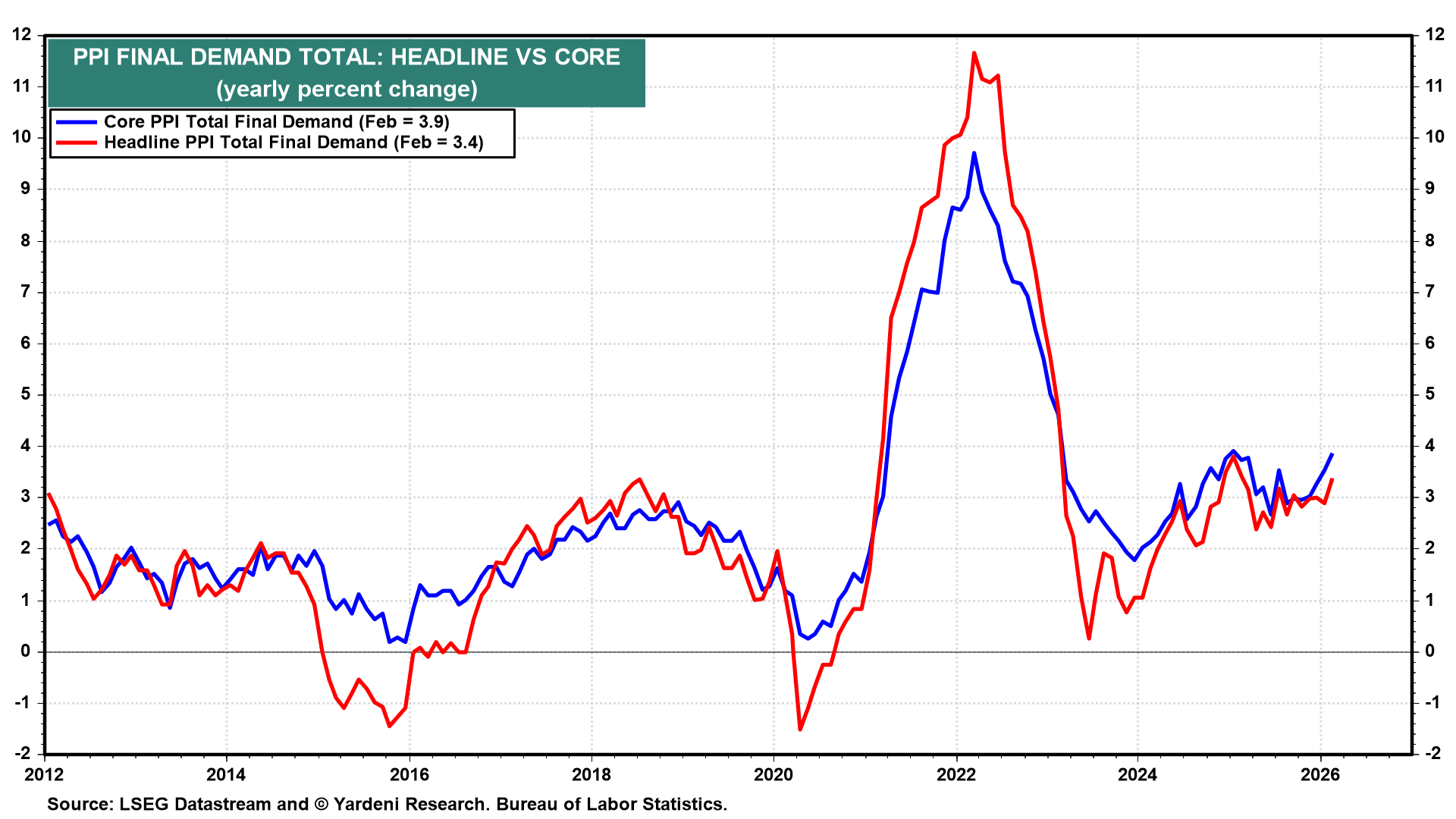

(1) PPI. The March PPI report (Tue) will show that the headline and core inflation rates of this measure of producer prices heated up significantly last month. They were already heating up during February before the war started (chart). Both are likely to rise to 4.0% y/y.

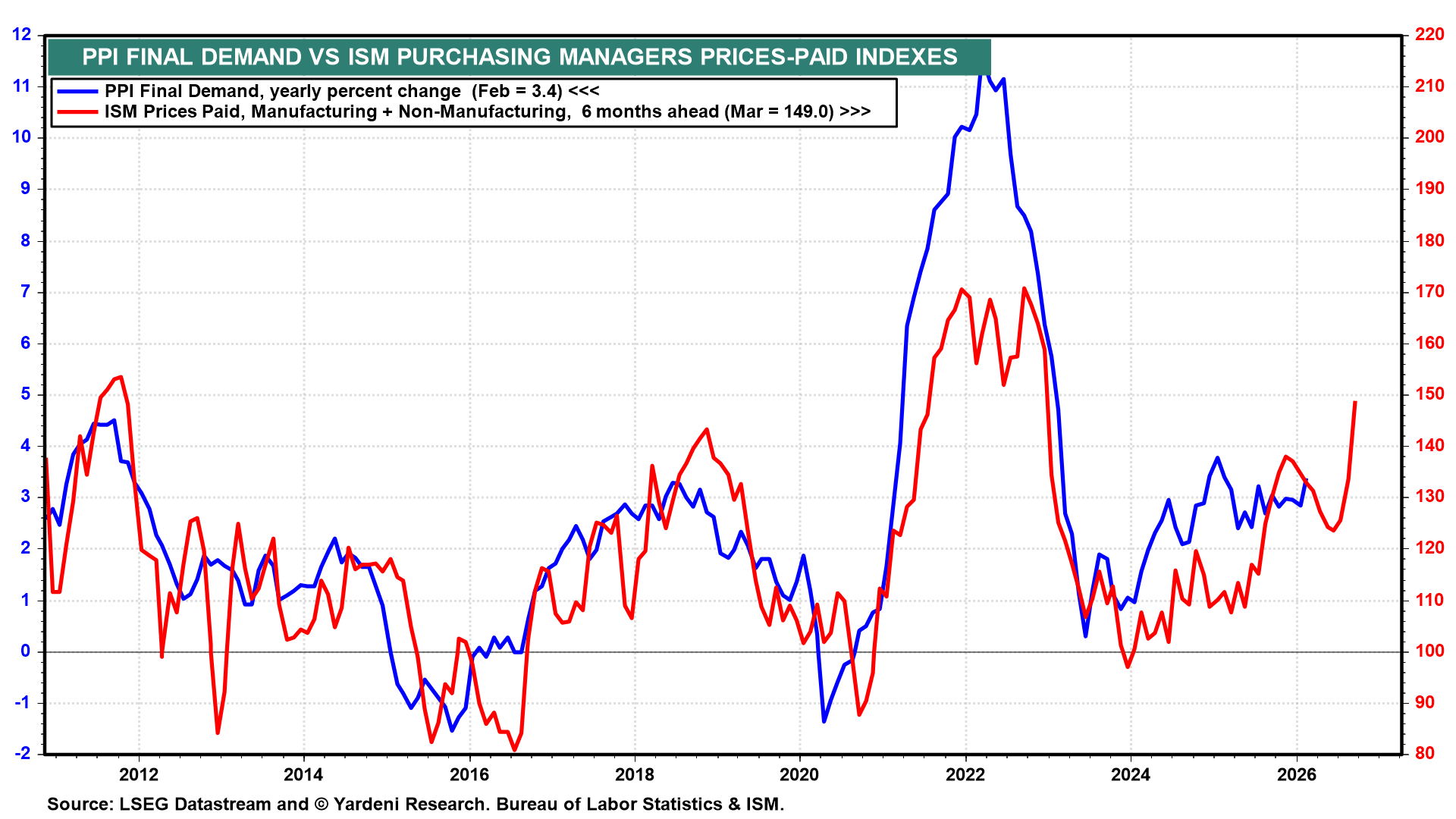

The ISM prices-paid indexes rose sharply in March, indicating that inflationary pressures on the PPI will build over the next six months (chart).

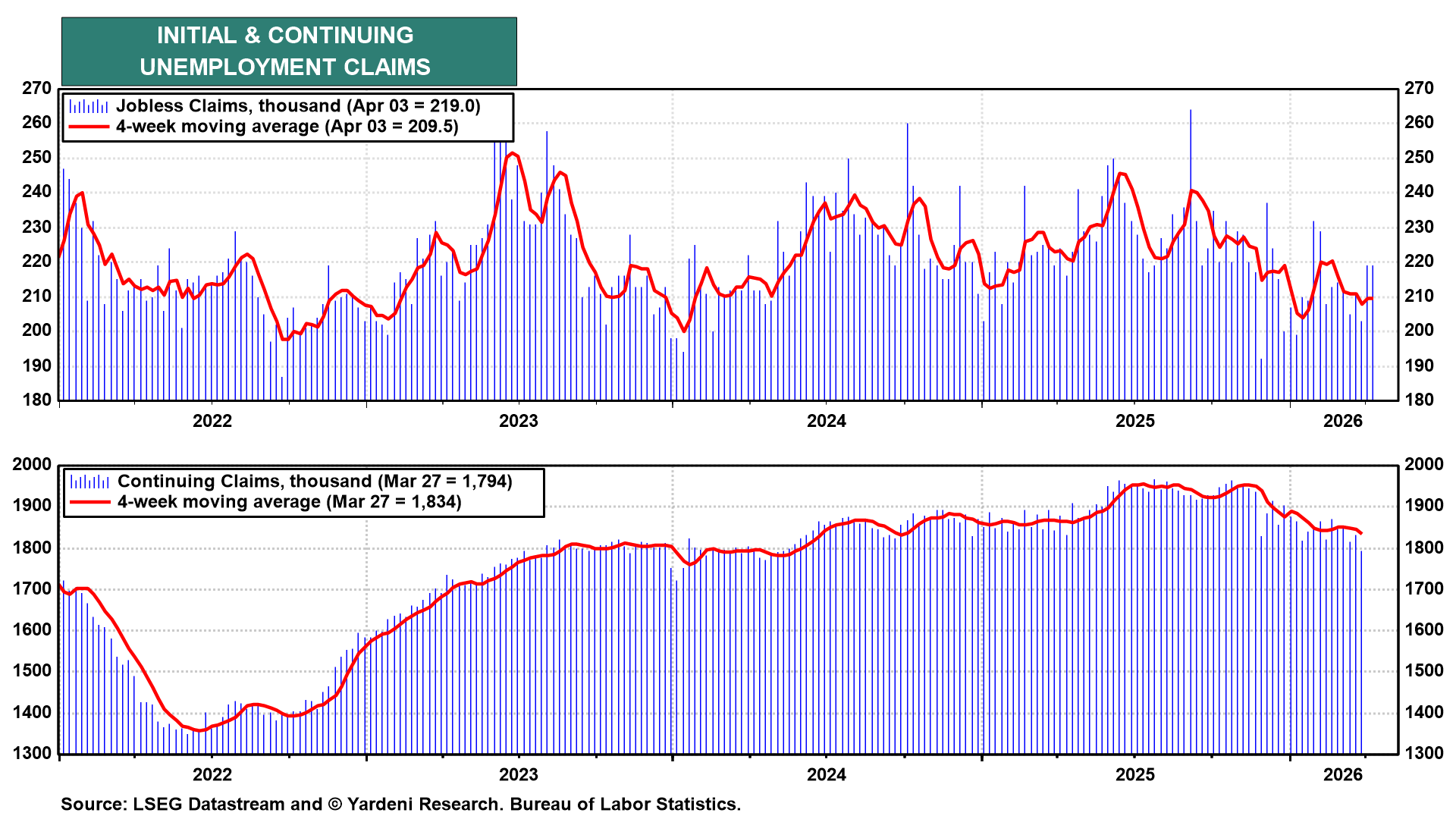

(2) Unemployment. Initial jobless claims (Thu) ticked up to 219,000 for the week of April 3, with the four-week moving average rising to 209,500, its first uptick in several weeks (chart). Continuing claims fell to 1,794,000, with the trajectory suggesting that the duration of unemployment may be shortening (chart). This week's data are likely to confirm that the labor market remains resilient; the energy shock has yet to hit it.

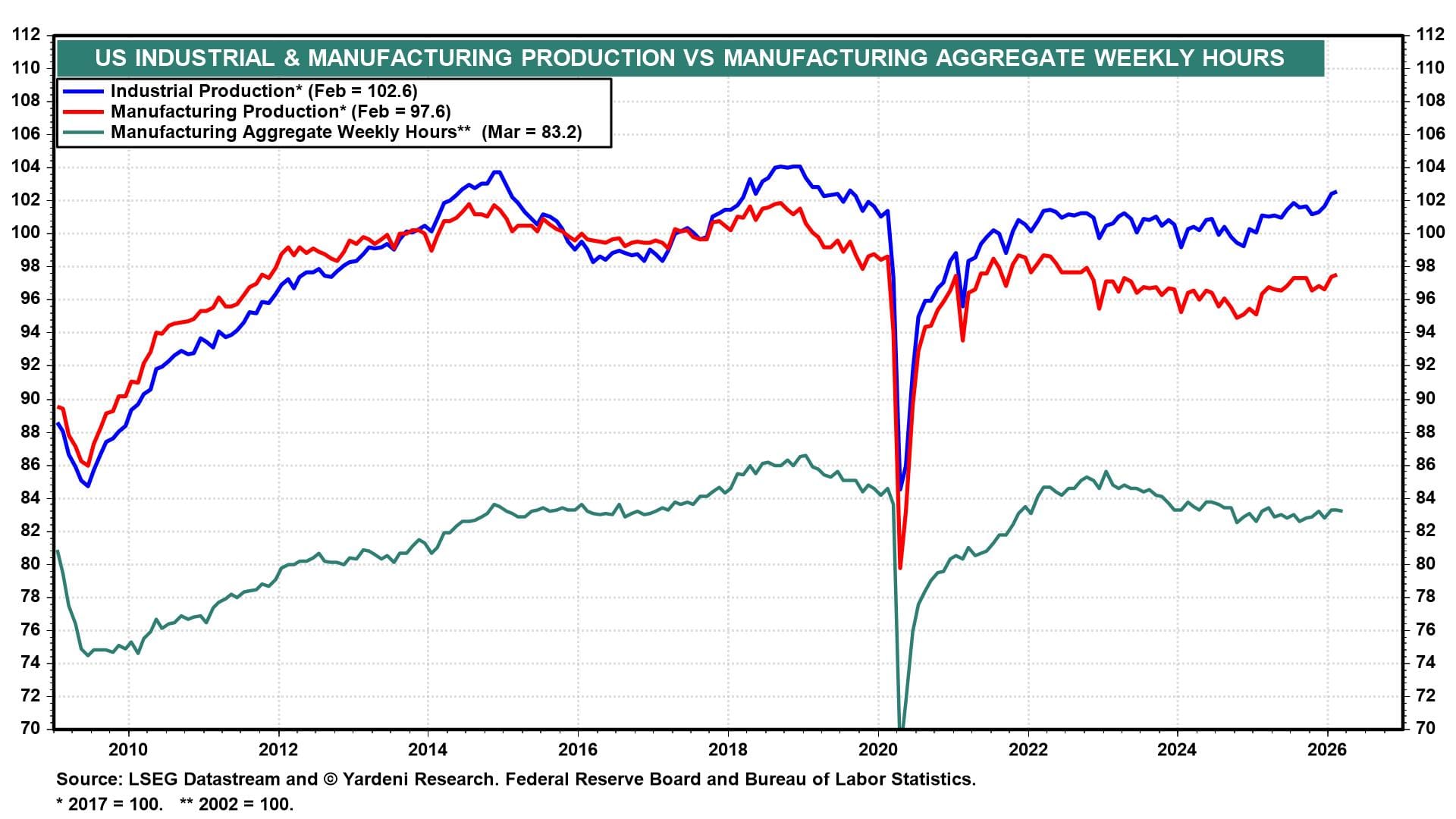

(3) Industrial production. Industrial production (Wed) stood at 102.6 in February, with manufacturing at 97.6, still below their pre-pandemic highs (chart). However, both have been trending higher since early 2025 while manufacturing hours worked have been relatively flat, suggesting that productivity is growing. We expect more of the same in March, with strong gains in output of information technology hardware and defense.

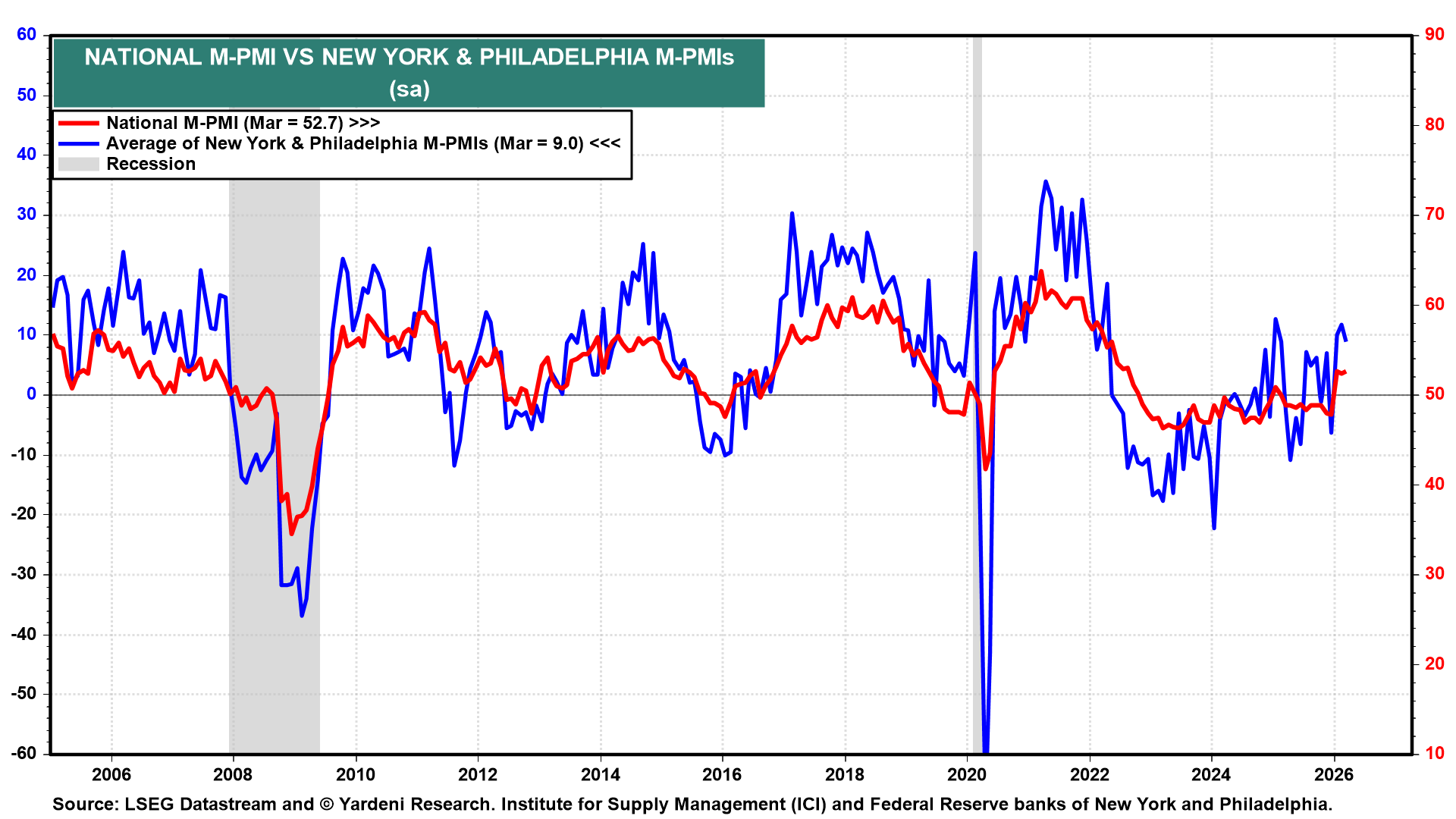

(4) Business & regional surveys. April's regional Fed surveys will be the first forward-looking reads on business conditions since the war started, with the NY Fed (Wed) and Philly Fed (Thu) surveys due. Both tend to be very volatile (chart).

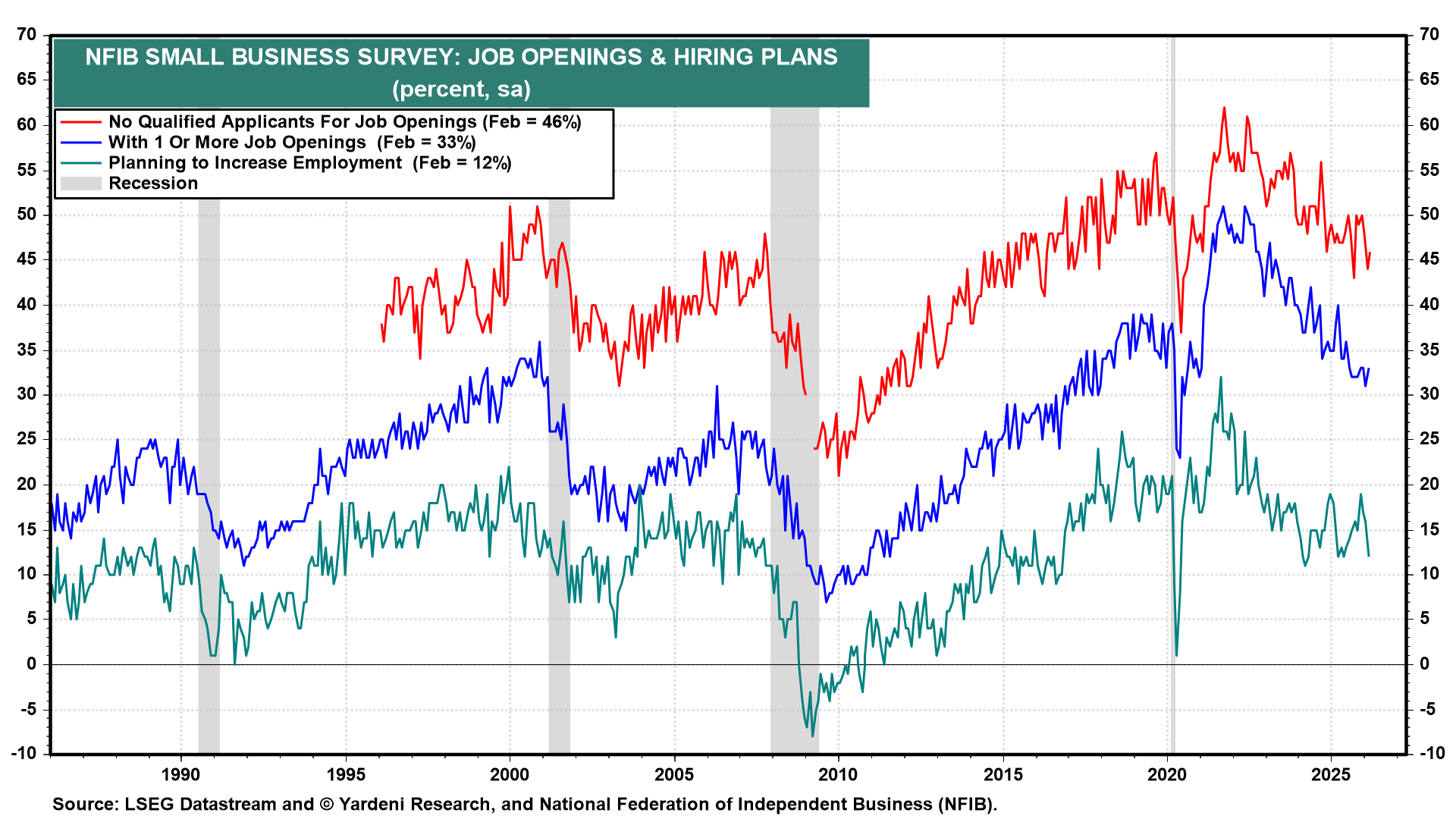

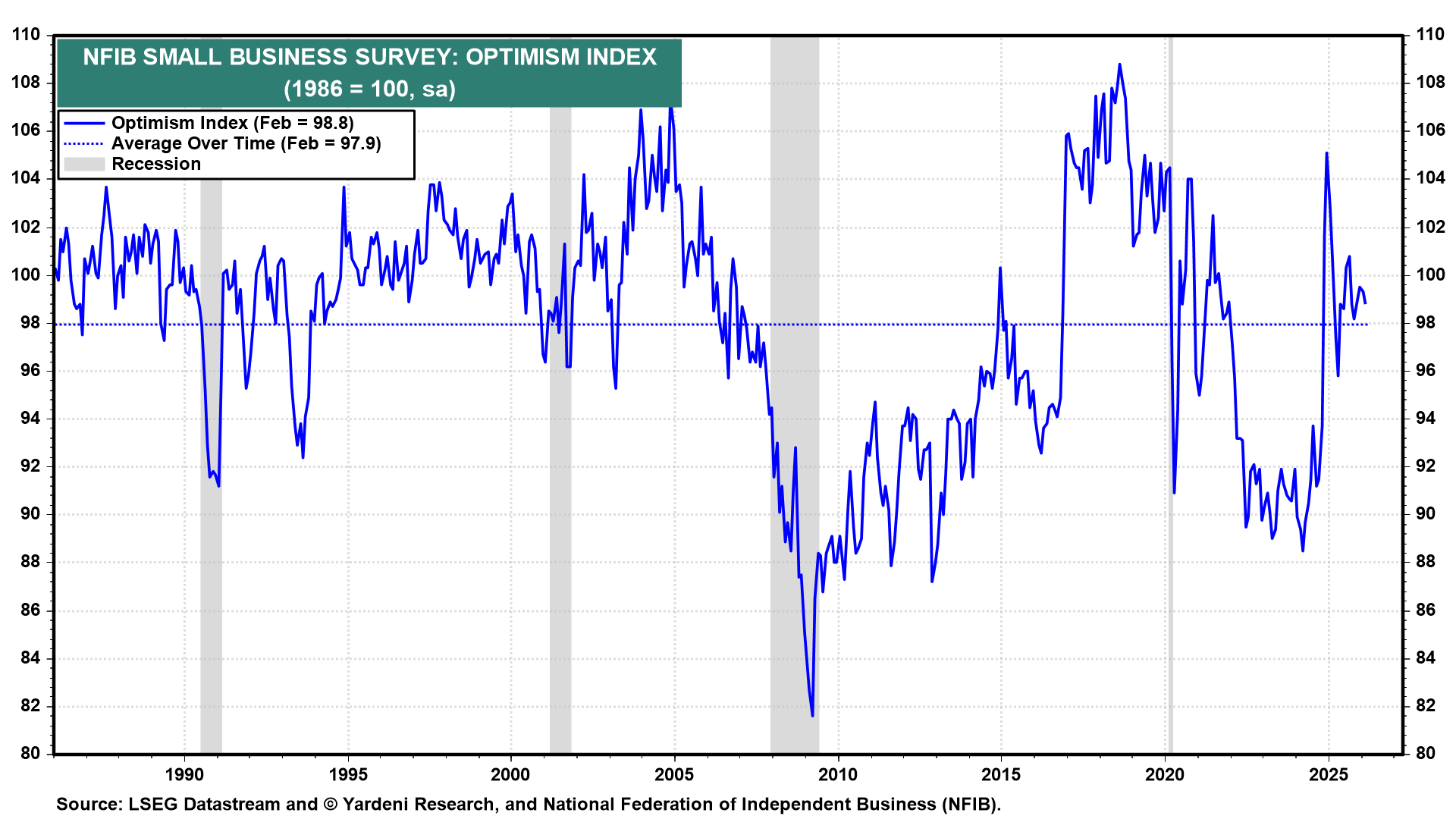

The March NFIB Small Business survey (Tue) will offer insights on how small businesses are responding to the war. The NFIB Optimism Index stood at 98.8 in February, just above its long-run average of 97.9 (chart). It dropped sharply during the energy shock in 2022. It is likely to do so again.

We will also be watching the labor market indicators in the NFIB survey for indications that the war is depressing hiring plans (chart).