The week ahead is light on economic data. The entire week falls inside the Fed's blackout period ahead of the July 28-29 FOMC meeting, so there's no Fedspeak to parse before the committee revisits the current 3.50%-3.75% funds rate range. Odds are that the committee's statement will remain hawkish but postpone any rate hiking.

On the other hand, the earnings reporting season is jam-packed this week. And of course, the fireworks show has resumed in the latest Middle East conflict. One major downside of earnings is that they might only meet analysts' already high expectations. Another is that hyperscalers might scale back their guidance for capital spending (and/or returns from such spending), or announce unforeseen delays in building data centers.

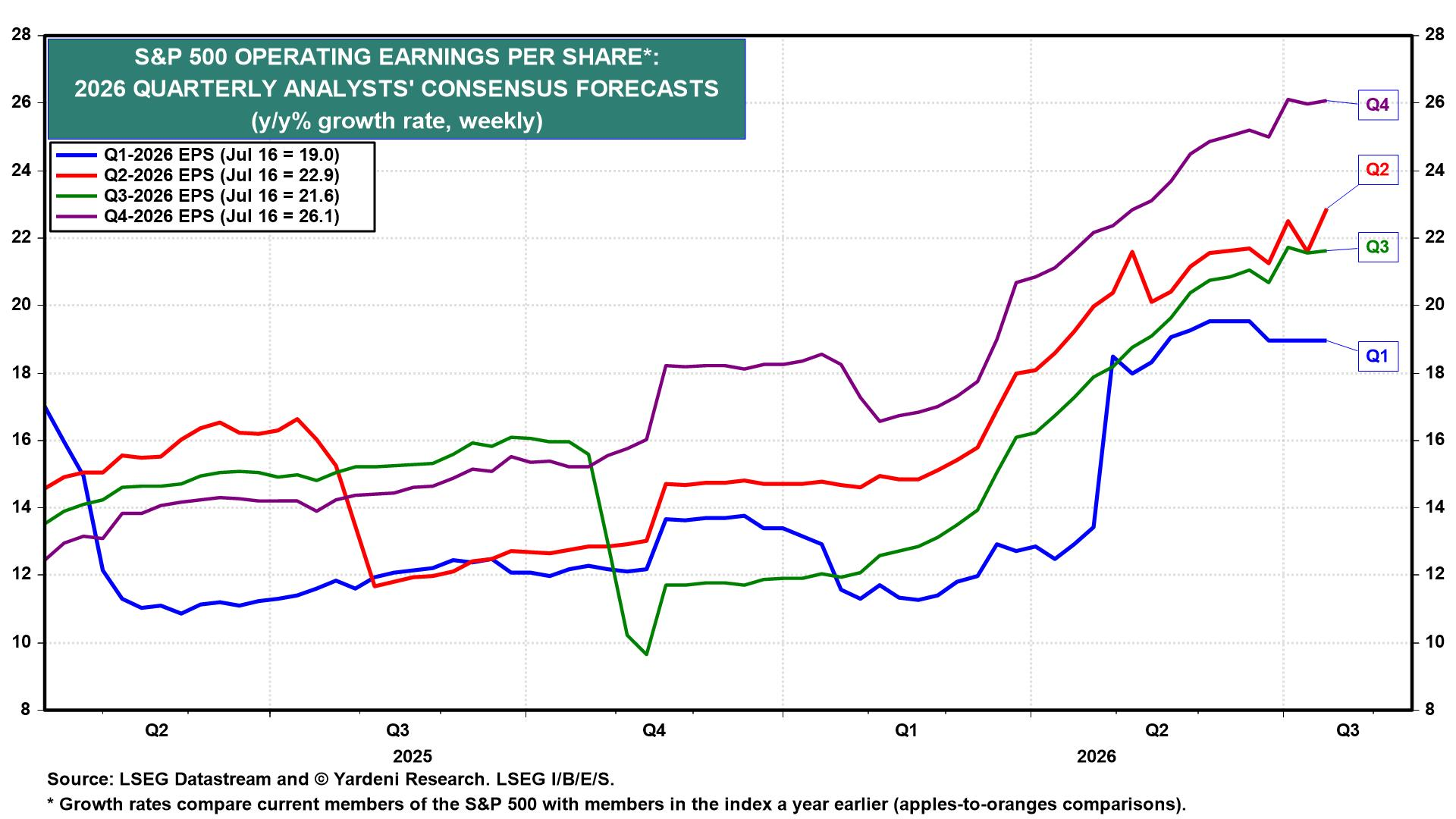

Wednesday stacks up as the busiest day of the earnings reporting week. GE Vernova, Texas Instruments, Alphabet, IBM, and Tesla all report that day. Intel reports on Thursday. The consensus of analysts’ estimates now implies Q2-2026 operating EPS growth for S&P 500 companies of 22.9% y/y, up from 21.6% a week earlier (chart).

The risk in the oil market is excessive complacency about the impact of a reescalation of the Gulf War on oil prices. US forces carried out a fifth consecutive night of strikes against Iran this week, according to US Central Command, keeping oil prices elevated and pressuring borrowing costs. The price of West Texas Intermediate crude oil settled Friday at $82.49 a barrel and Brent ended last week at $88.10, both up over 10% for the week (chart).

Here are the key economic releases most likely to shape investors' thinking this week:

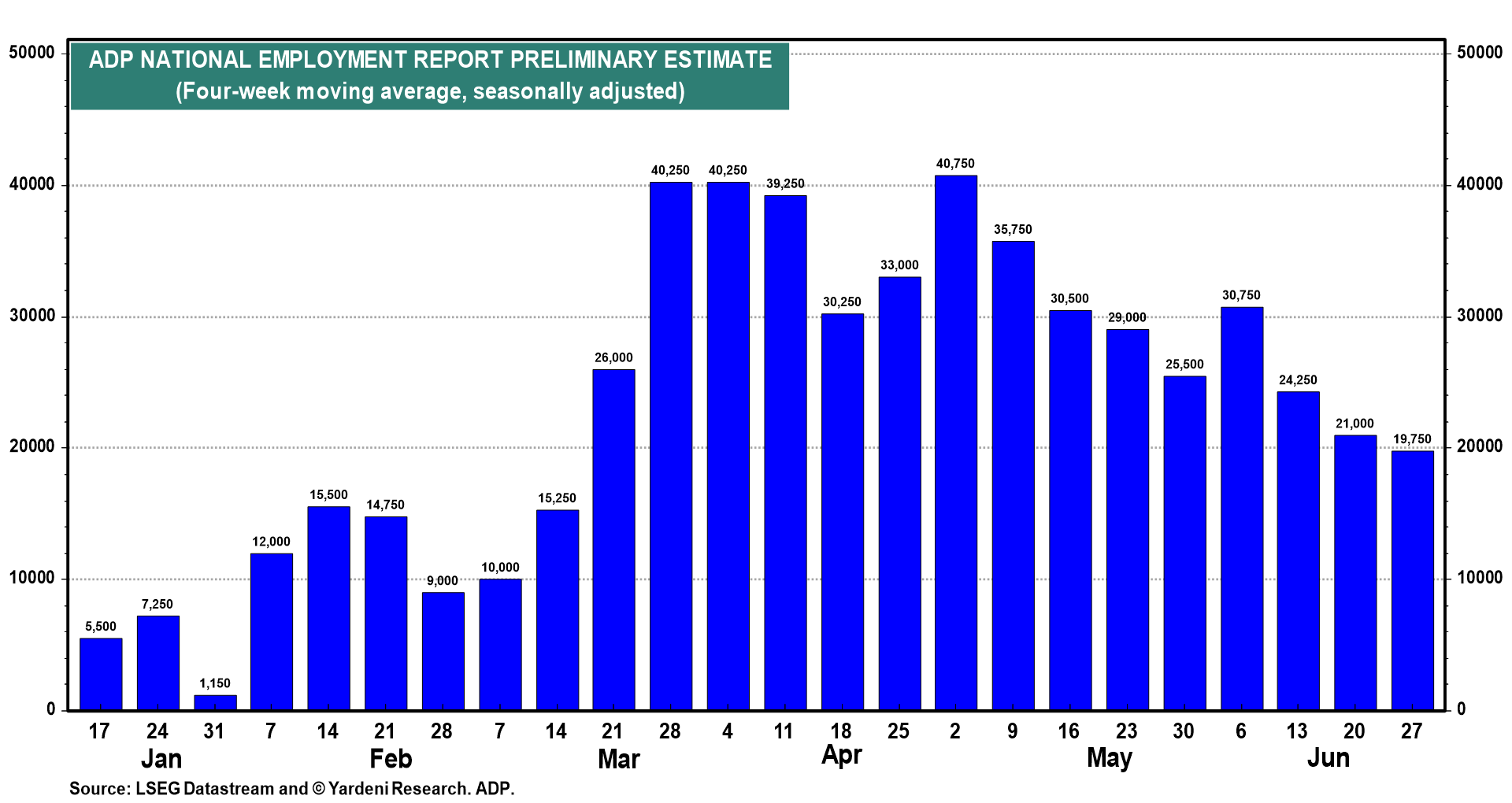

(1) Employment. ADP's weekly National Employment Report Pulse (Tue) has shown hiring slowing for three straight readings, with private employers adding just 19,750 jobs per week on average in the four weeks through June 27 (chart). Still, this remains comfortably above early 2026 levels.

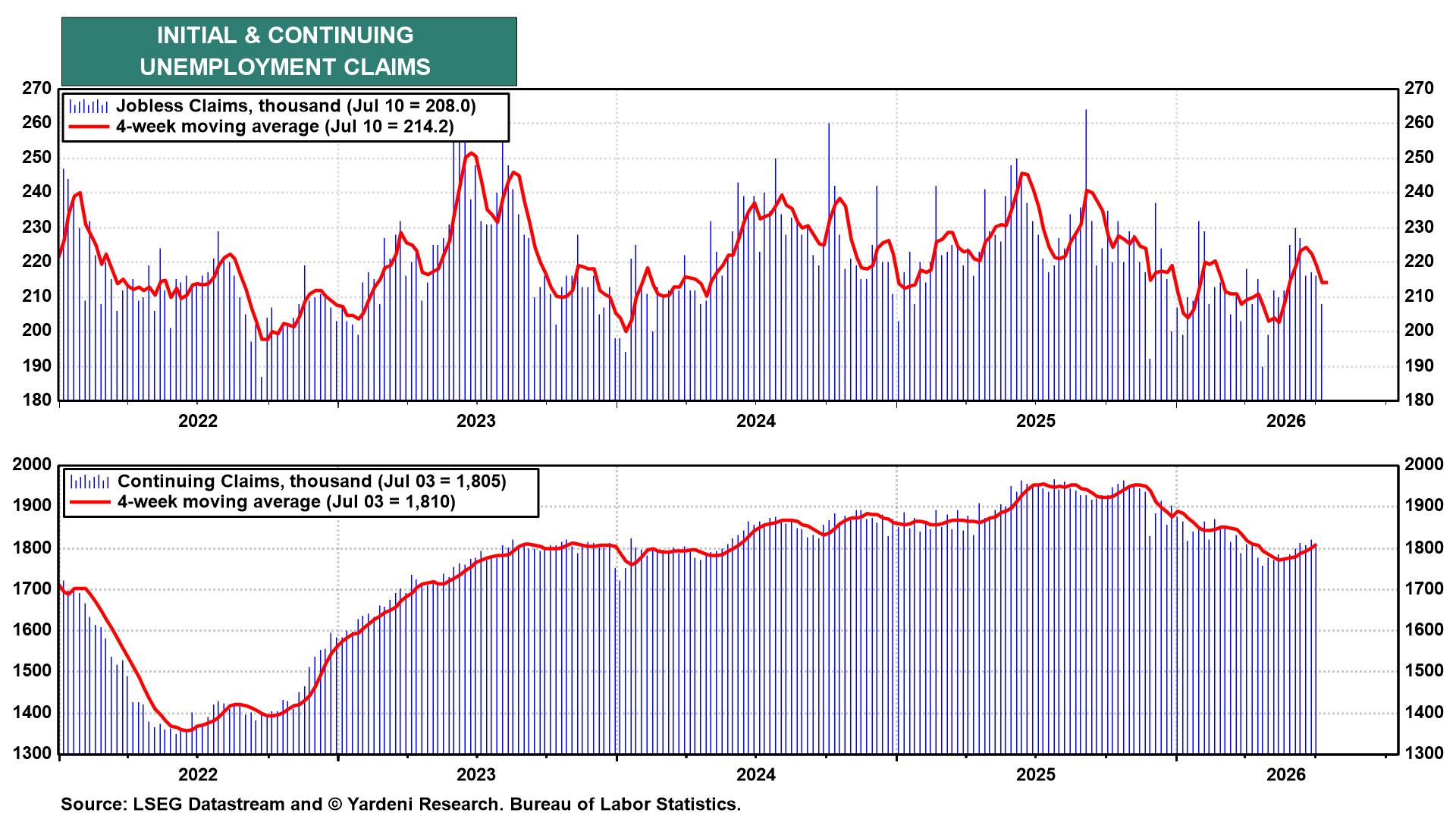

Initial unemployment insurance claims (Thu) fell 8,000 to 208,000 for the week ended July 11, a 10-week low, with the four-week average down to 214,250 and continuing claims at 1.805 million (chart).

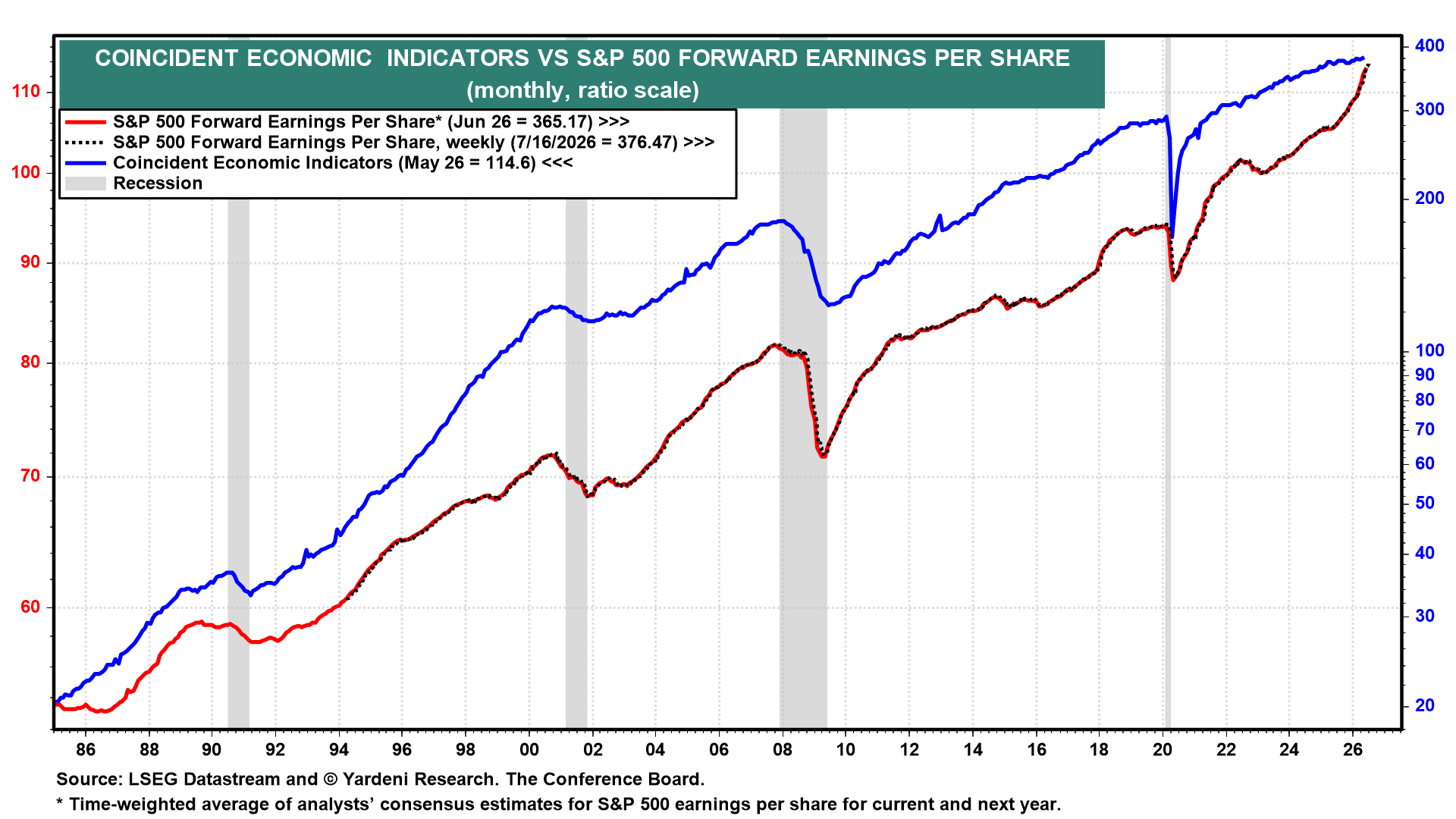

(2) Composite Economic Indicators. June's Index of Composite Economic Indicators probably remained flat (chart). It may be misleadingly weak given the recent surge in S&P 500 forward earnings.

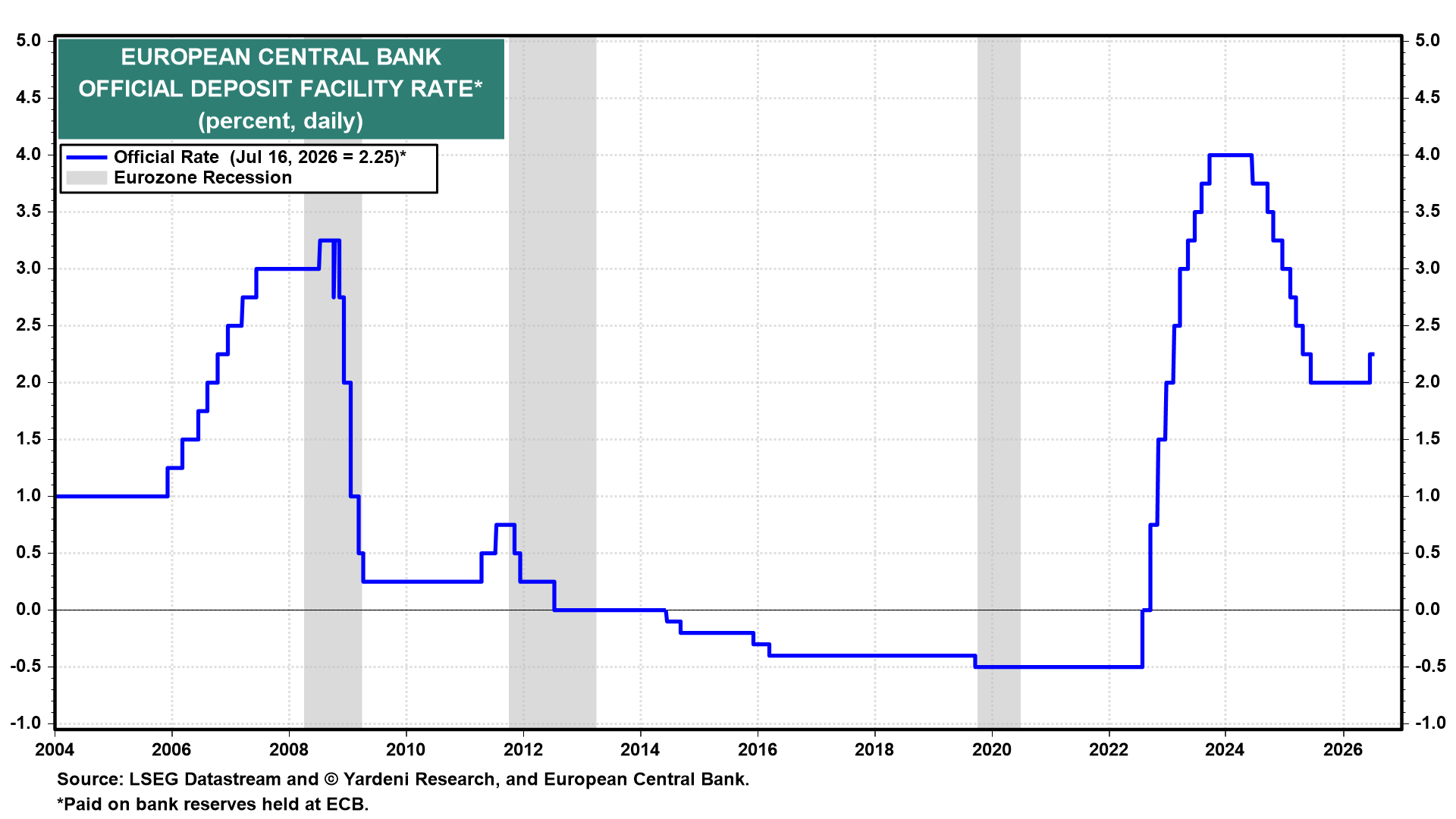

(3) ECB Policy. The European Central Bank meets Thursday and is widely expected to hold its deposit rate at 2.25% following June's hike, the first since 2023 (chart). The more interesting question is guidance. Financial markets currently price roughly 70%-80% odds of a September hike, given the oil-driven inflation risk from the Iran conflict, so Lagarde's press conference tone matters more than the decision itself. It's a heavy week for global data more broadly, with Canada's CPI (Mon), UK jobs and CPI (Tue/Wed), and Japan's CPI and flash PMIs across the Eurozone, Japan, and the UK (Fri) all on the calendar.