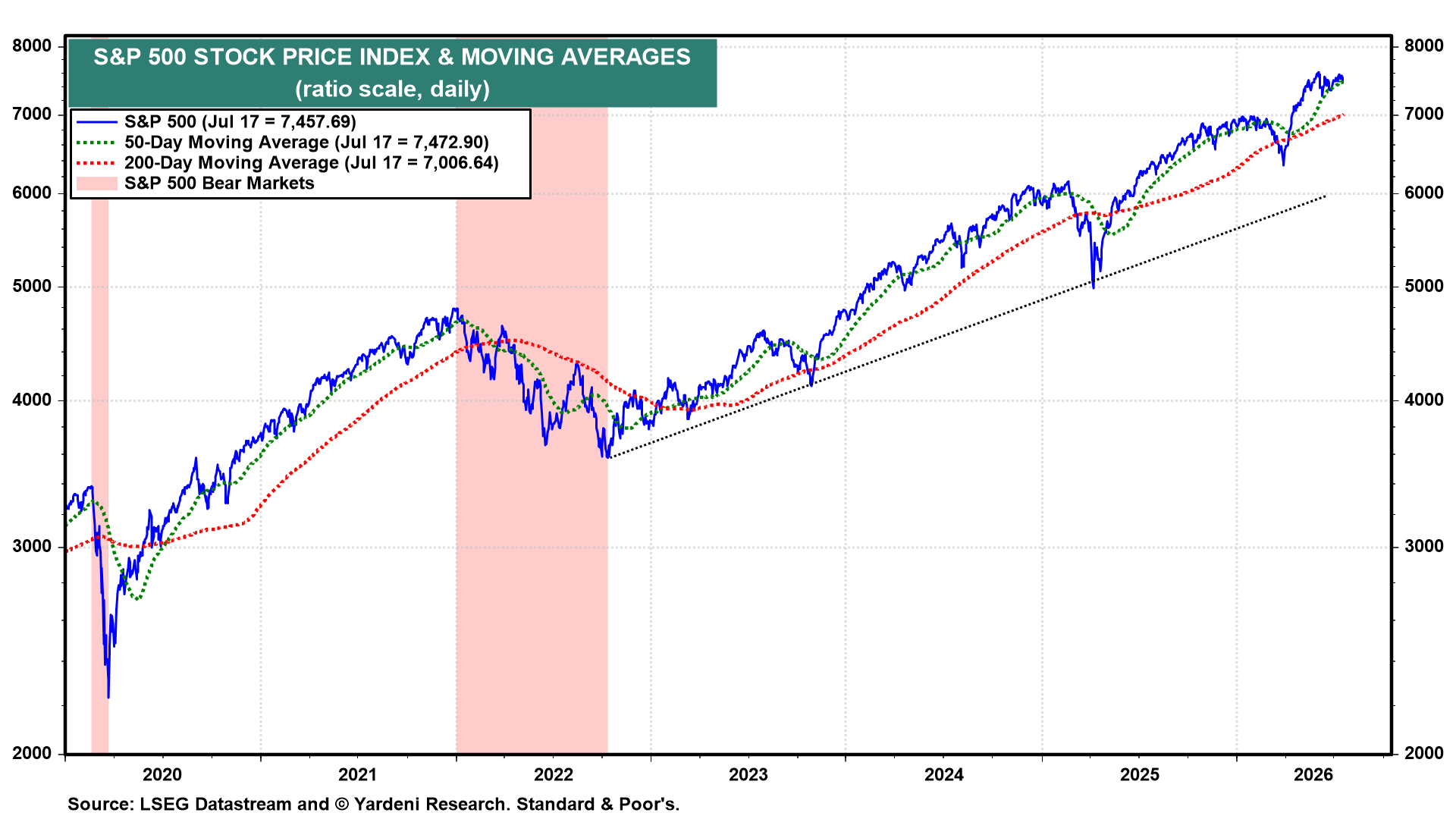

The S&P 500 first hit 7,500 on May 14 and has remained stuck around that level. The index continues to cruise along its 50-day moving average. A 6.0% drop would send it back to its 200-day moving average (chart). We have seen this movie before, recently, during late 2024 into early 2025 and again during late 2025 into early 2026. Both saw similar bouts of sideways consolidation, followed by pullbacks that attracted dip buyers. That's a plausible scenario through September, in our opinion. We are still aiming for 8,250 by the end of this year.

Consider the following:

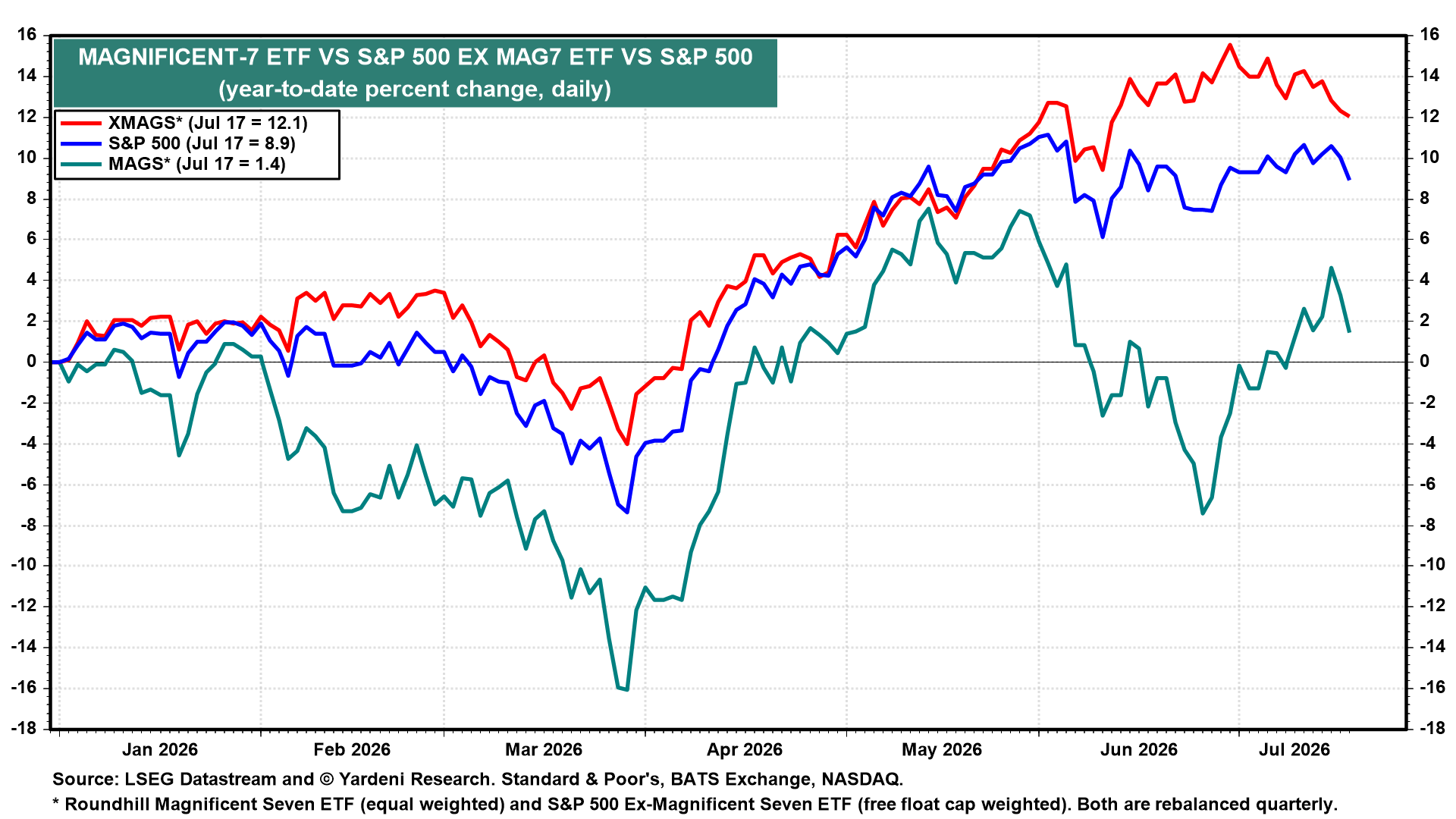

(1) Stock Market Performance. So far this year, the S&P 500's bull market leadership has rotated from the Magnificent-7 to the Impressive 493 (chart). The Mag-7 had a June swoon and has recovered somewhat so far in July. However, the S&P 493 collectively has outperformed the S&P 500's Mag-7 so far this year.

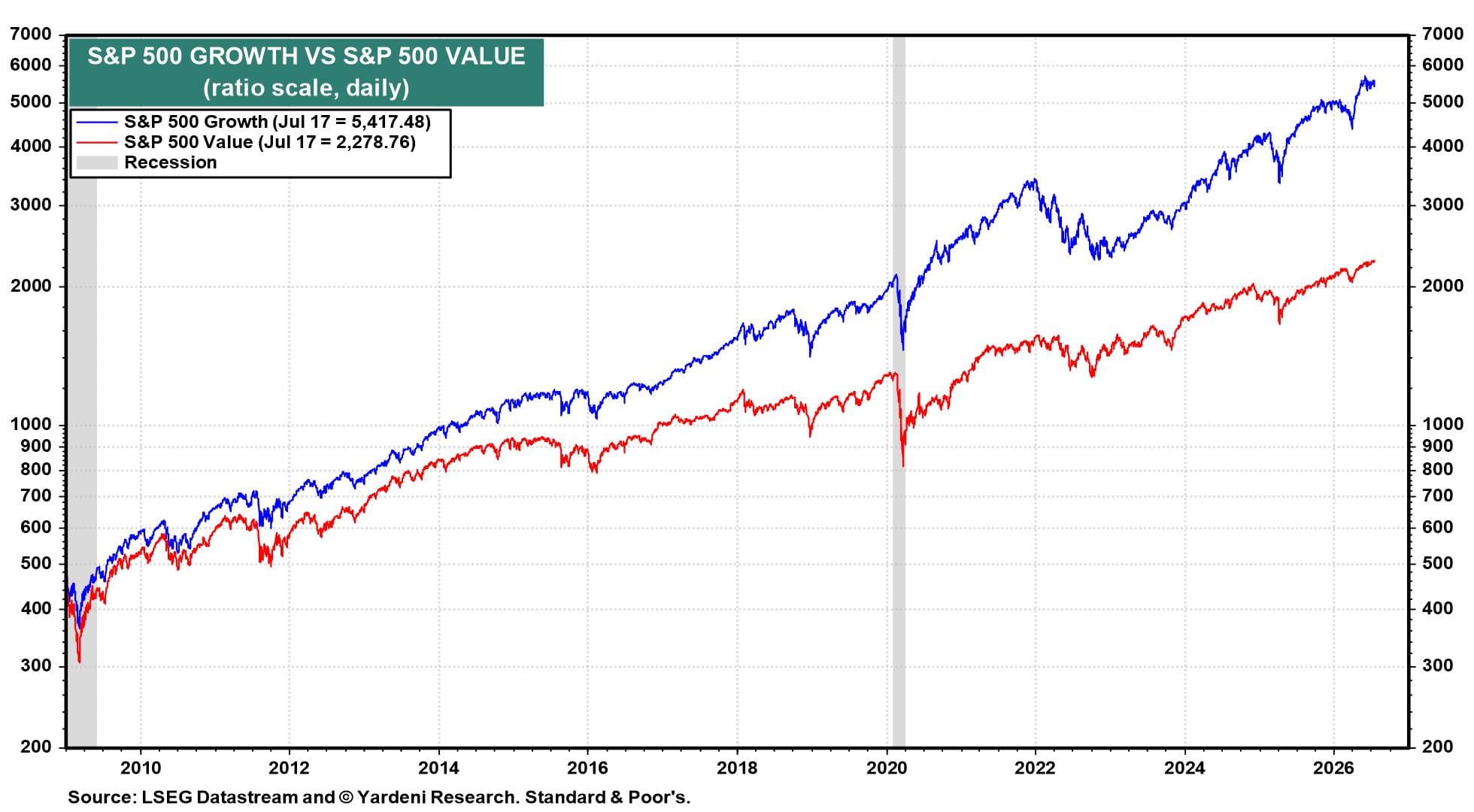

Recently, S&P 500 Value has been outperforming S&P 500 Growth (chart). Fabulous earnings momentum (FEMO) has bolstered Growth's earnings expectations to such a high level that simply meeting them this earnings season could read as a letdown. Value carries no such burden.

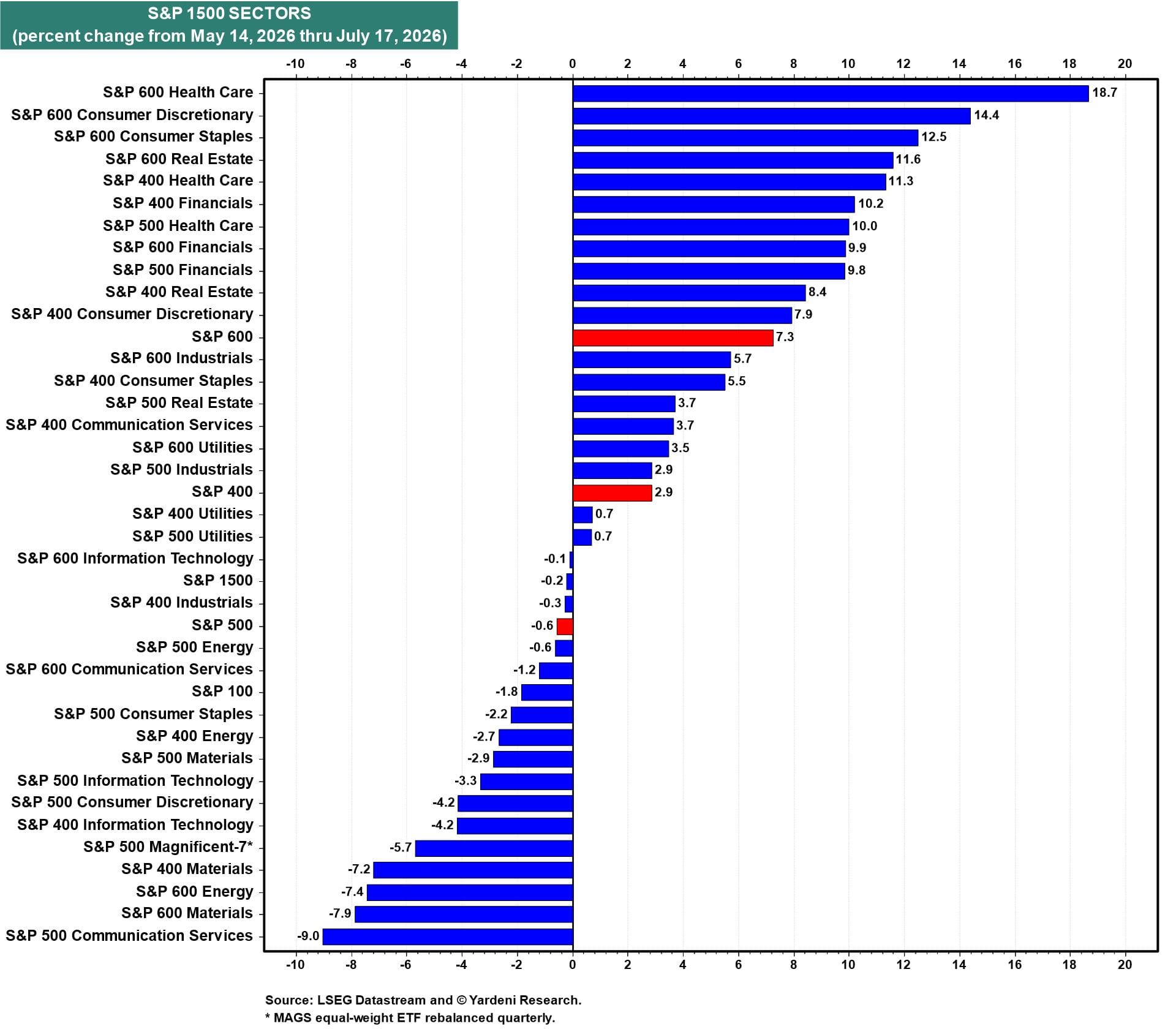

The rotation in market leadership shows up clearly across the S&P 1500 sectors. Cheaper, more defensive corners of the market have outperformed since May 14, led by the S&P 600 Health Care, up 18.7%, and the S&P 600 Consumer Discretionary, up 14.4% (chart). The S&P 500 itself is down just 0.6% over that span, a modest headline number that masks a wide spread between winners and losers. The Magnificent-7 is at the other end of that dispersion, down 5.7%. Information Technology looks tired. New catalysts are scarce, and a bit of AI fatigue has set in. Semiconductor momentum has faded as one of the market's most crowded trades corrects. SOXX is down 20.3% since it peaked at a record high on June 22.

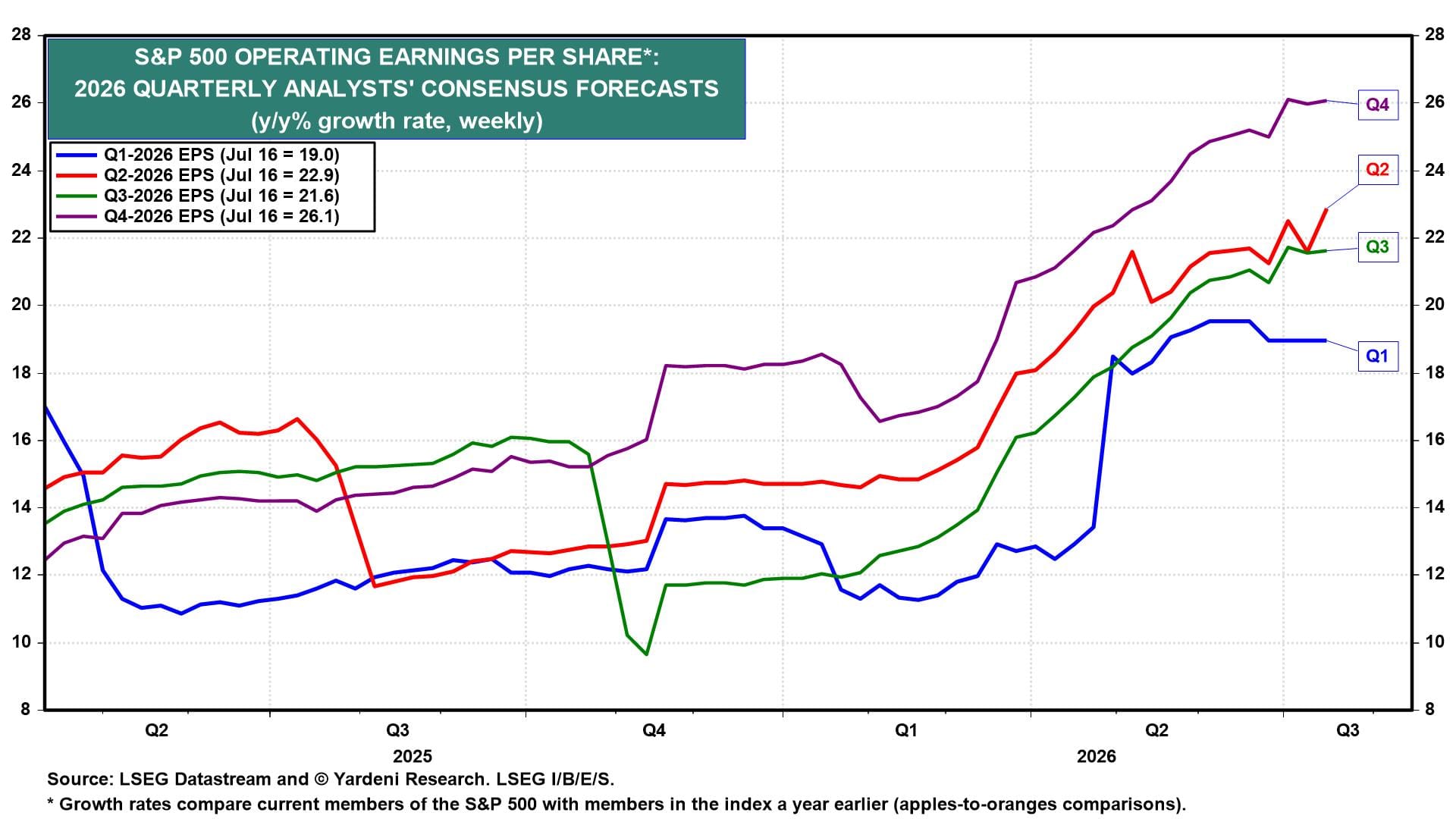

(2) Current Earnings Season. The analysts' consensus Q2 EPS growth estimate rose to 22.9% y/y on an apples-to-oranges basis, up 1.3% on the week (chart). Great expectations are held for Q3 and Q4, as well.

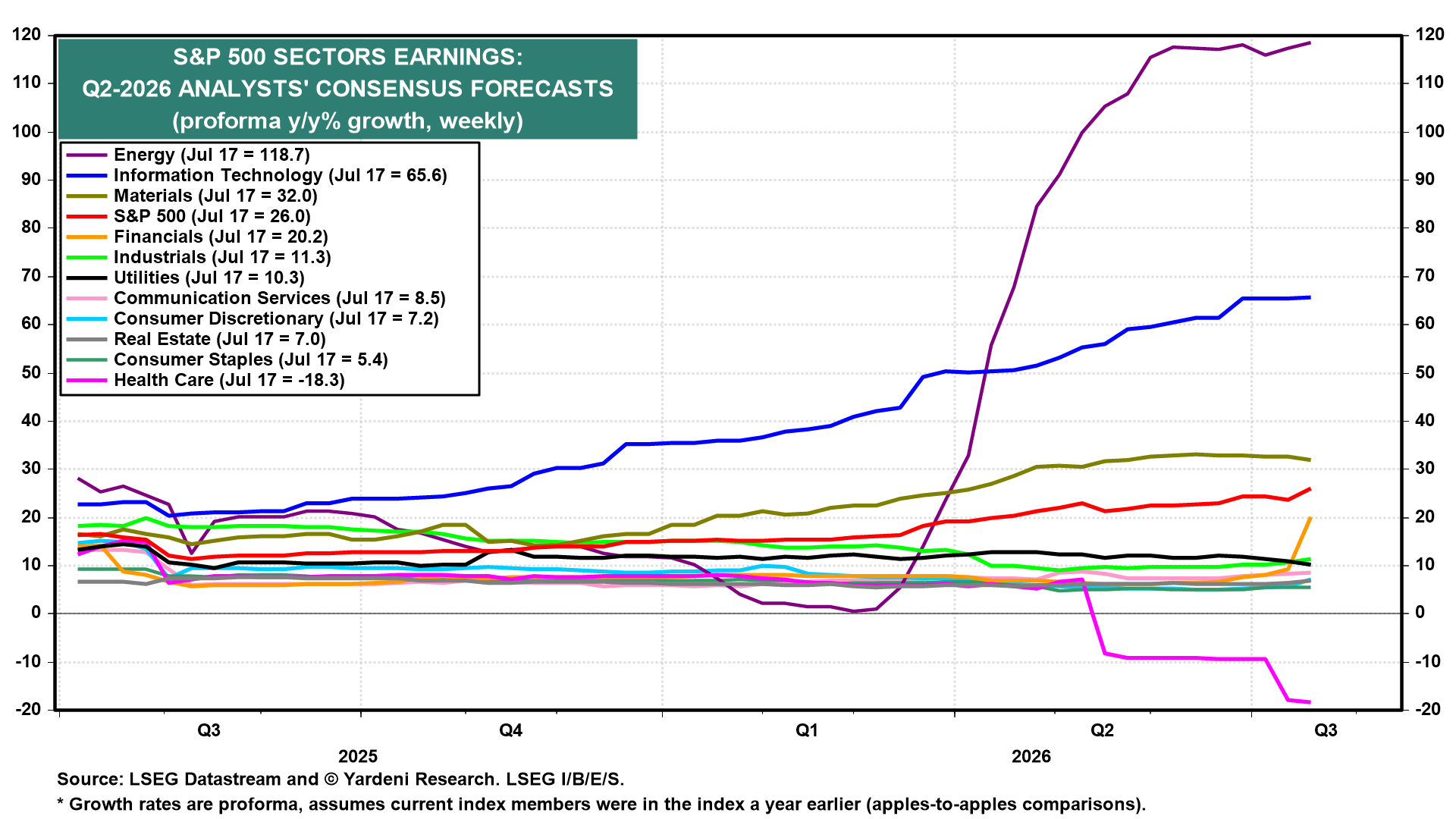

On a pro forma basis (apples-to-apples), Q2 earnings growth is running at 26.0% (chart). Energy accounts for a large share of that figure given the war's impact on energy prices. Technology earnings growth has held steady. Health Care continues to lag on an earnings basis despite decent sector stock performance. Financials drove much of last week's improvement. Goldman Sachs beat EPS estimates by 46%, and JPMorgan beat by about 10%.

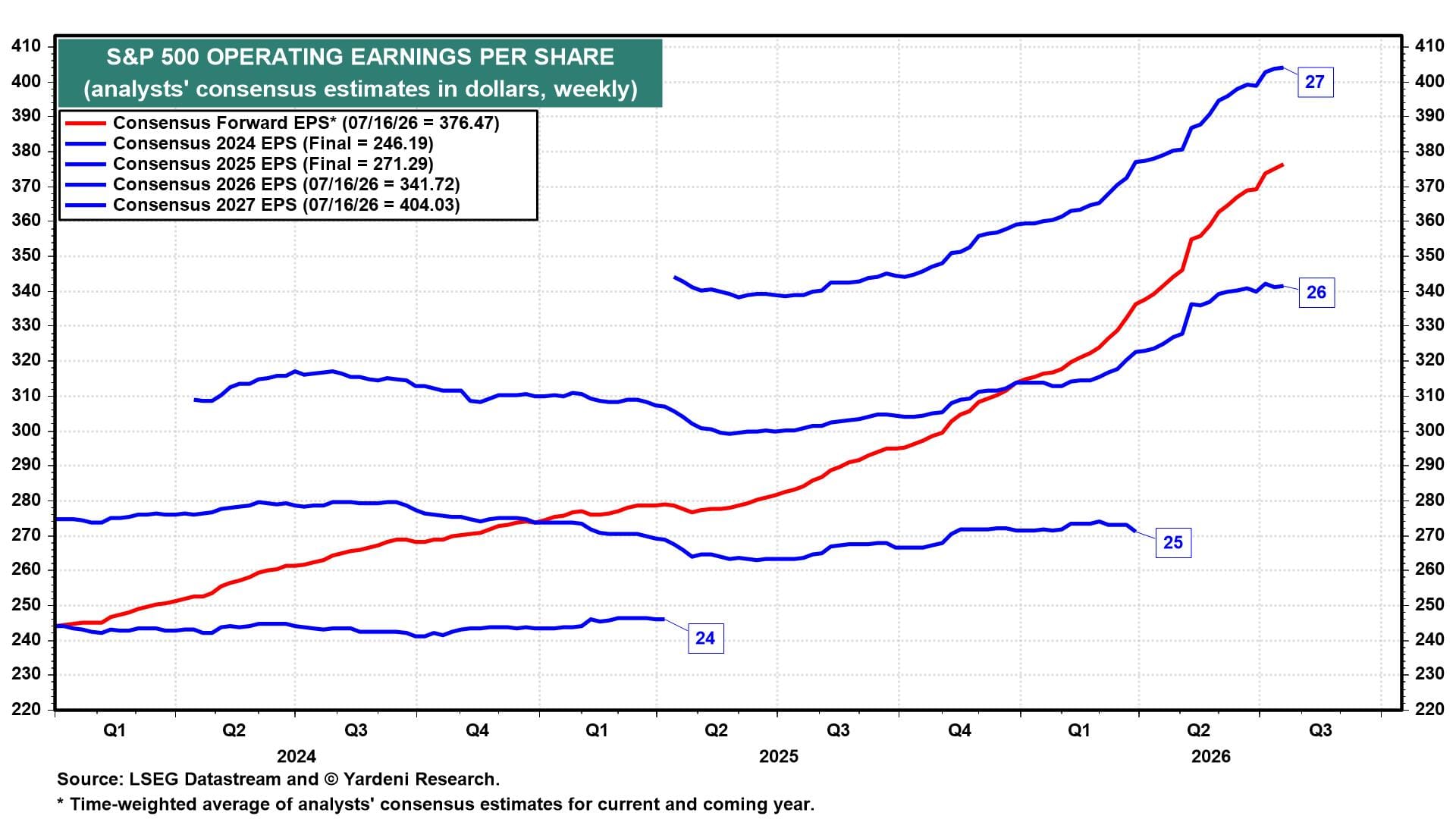

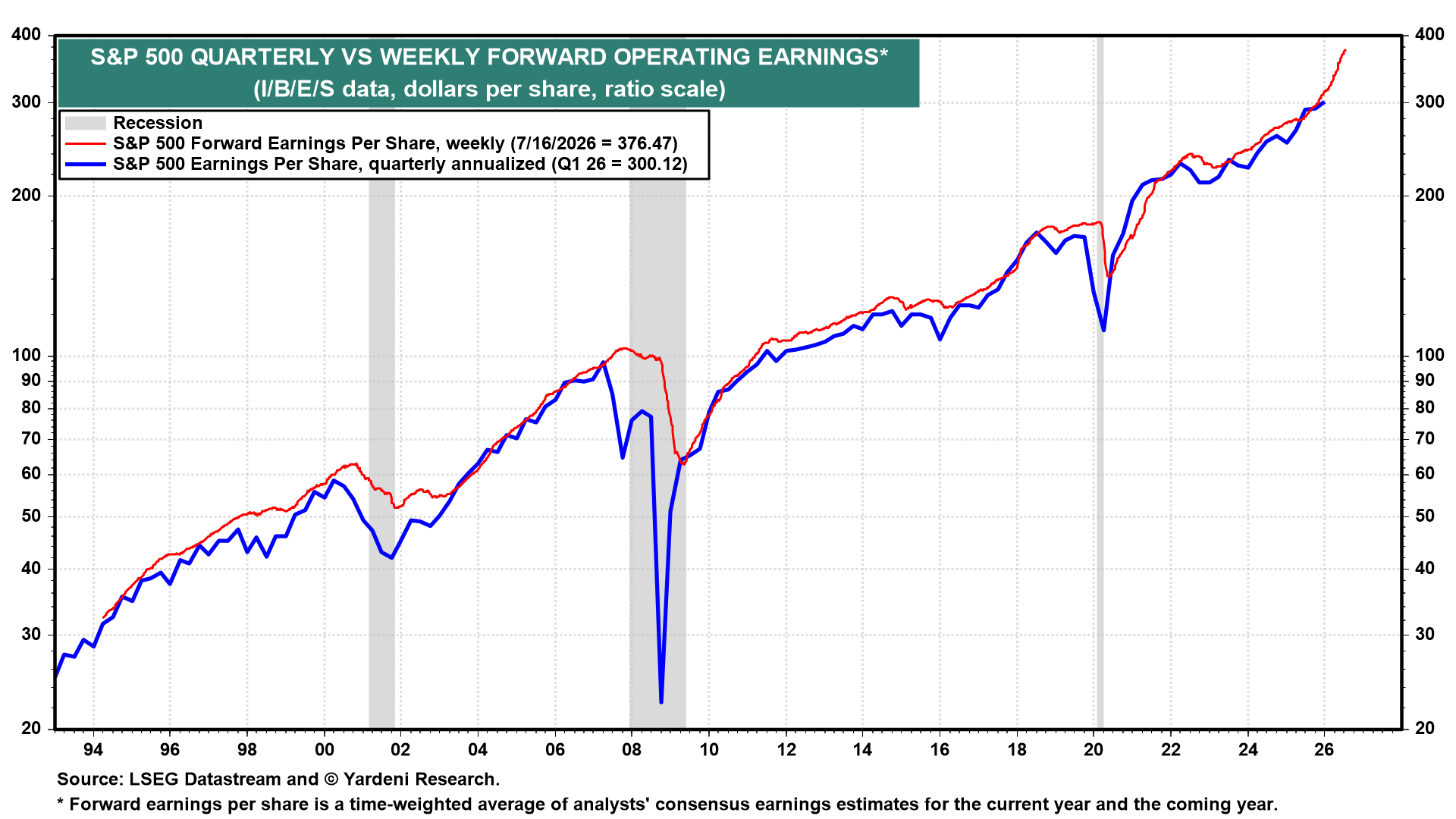

(3) Revenues, Earnings, And Profit Margin. Analysts' consensus EPS estimate for S&P 500 companies this year has flattened recently, while the 2027 estimate has continued to climb above $400 (chart). Forward earnings, the time-weighted average of the two, rose to a record high last week, buoyed by the fact it converges toward the 2027 estimate as 2026 wears on.

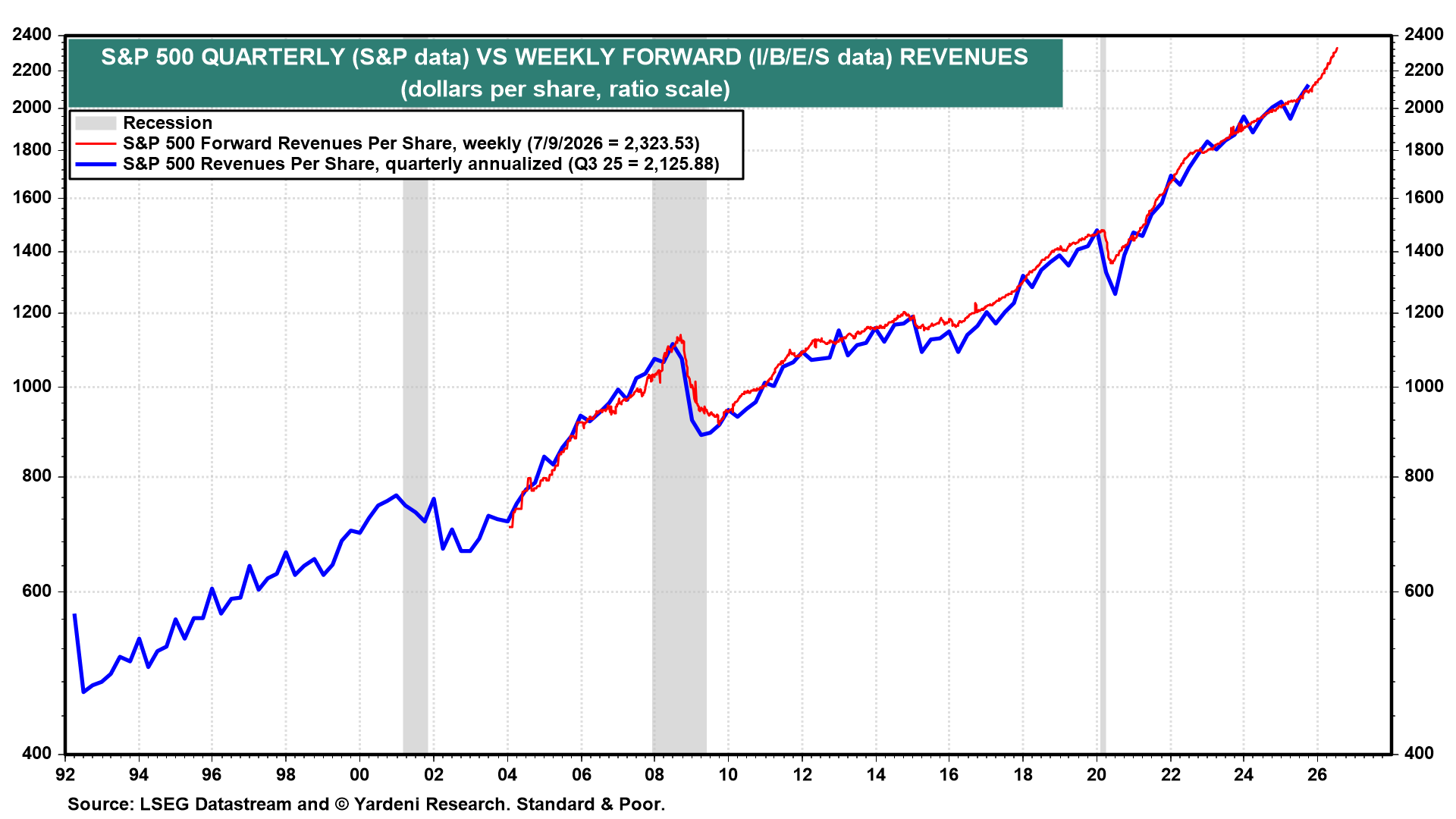

S&P 500 forward revenues per share also reached a new all-time high, climbing even faster recently (chart).

The forward earnings series has been a reliable predictor of actual earnings during economic expansions but fails during recessions. Given the economy's resilience, the current run of record forward estimates is a realistic read on where earnings are headed over the next 12 months (chart).

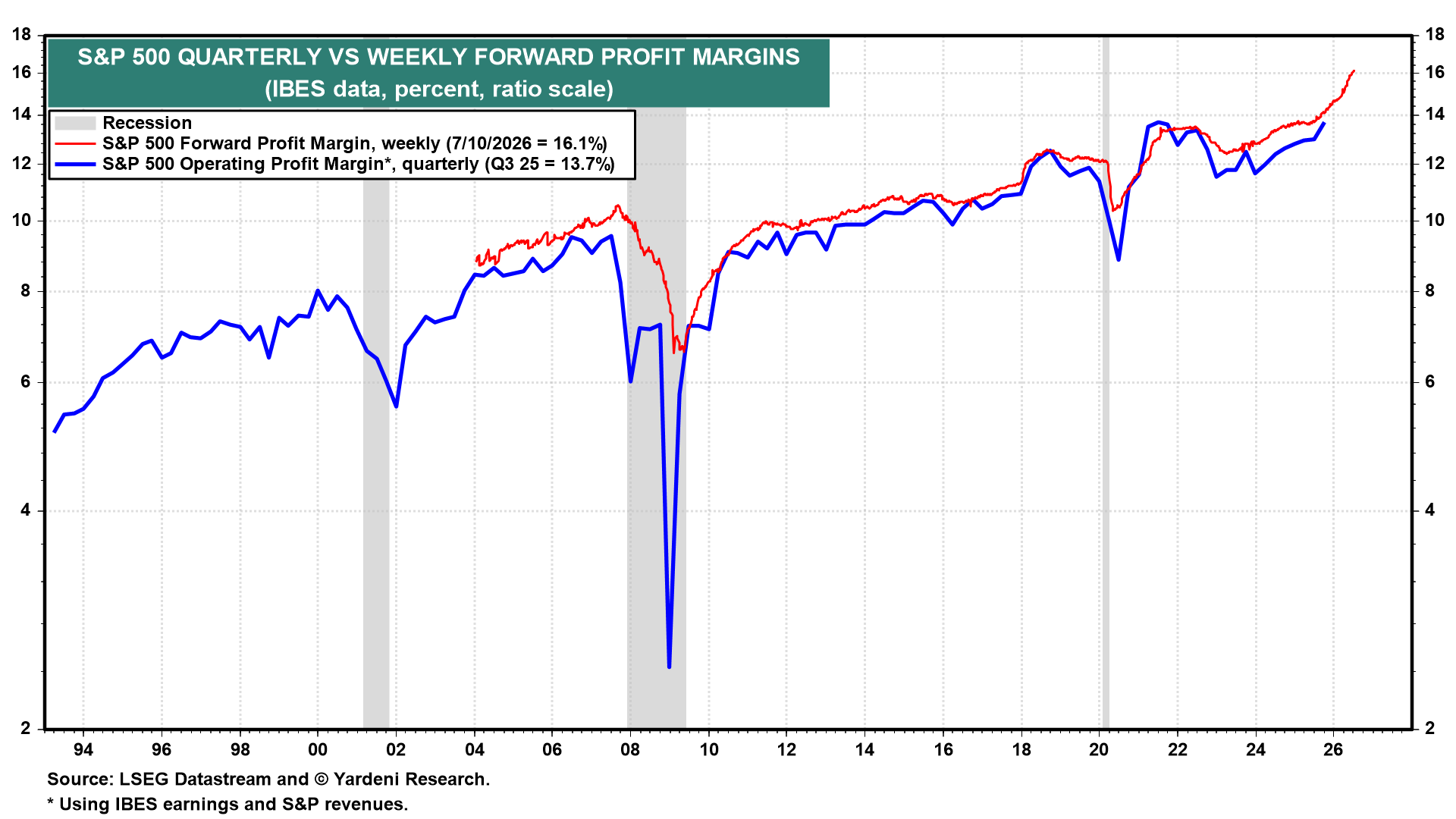

If a bubble exists anywhere in this market, it is not in valuation and not in revenues. It is in profit margins. The forward profit margin rose to a record 16.1% last week (chart).

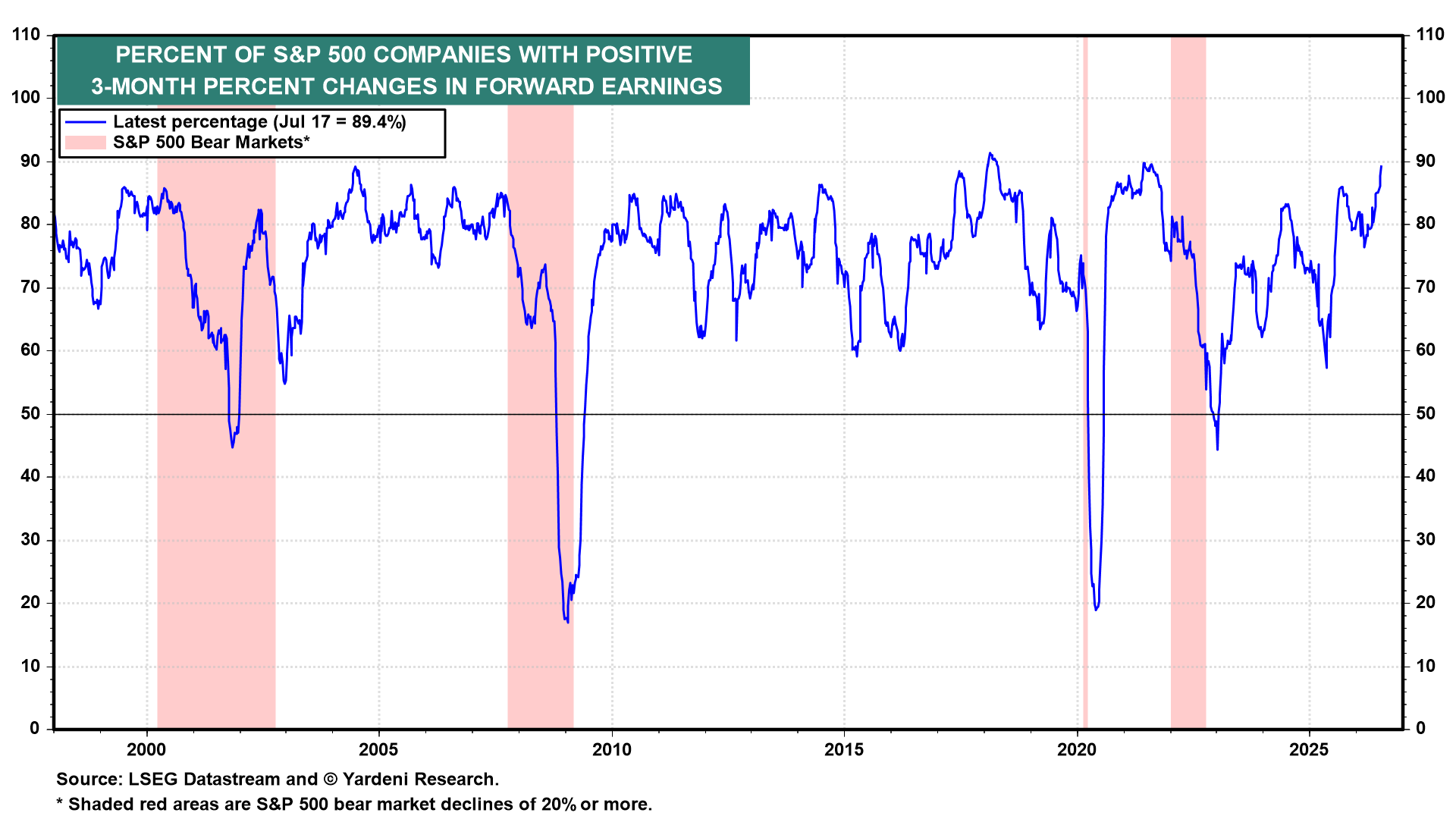

The percentage of S&P 500 companies with positive three-month forward earnings growth is at 89.4%, a level associated with past cyclical earnings peaks (chart). That's a harbinger of more rotation in a broadening bull market, in our opinion.

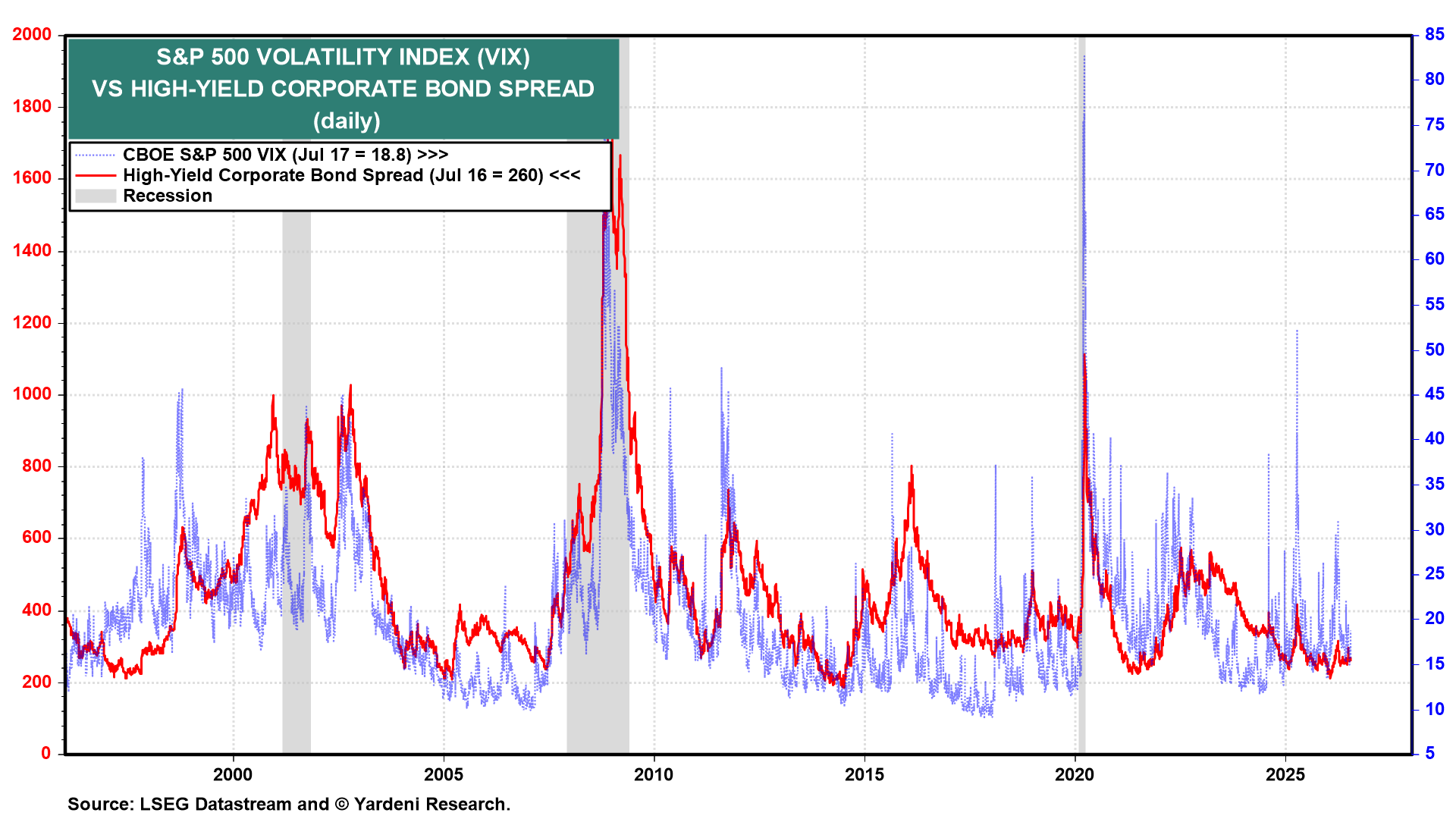

(4) Credit. The 10-year Treasury yield is consolidating around 4.50%, squarely within the 4.00%-5.00% range we consider to be the "old normal" (chart).

Corporate high-yield credit spreads remain tight despite ongoing worries about private credit (chart). That's helped to keep a lid on the S&P 500 VIX.