The S&P 500 climbed to another record high on Friday, closing at 7,580.05. Fabulous earnings momentum (FEMO) and falling oil prices boosted stock prices. Brent crude settled at $92.05 a barrel, the lowest weekly close since April 17. Axios reports that the US and Iran have reached a ceasefire-extension deal, pending President Trump's approval. The odds that the US blockade of the Strait of Hormuz will be lifted by June 30 are up to 68% from 42% on May 20.

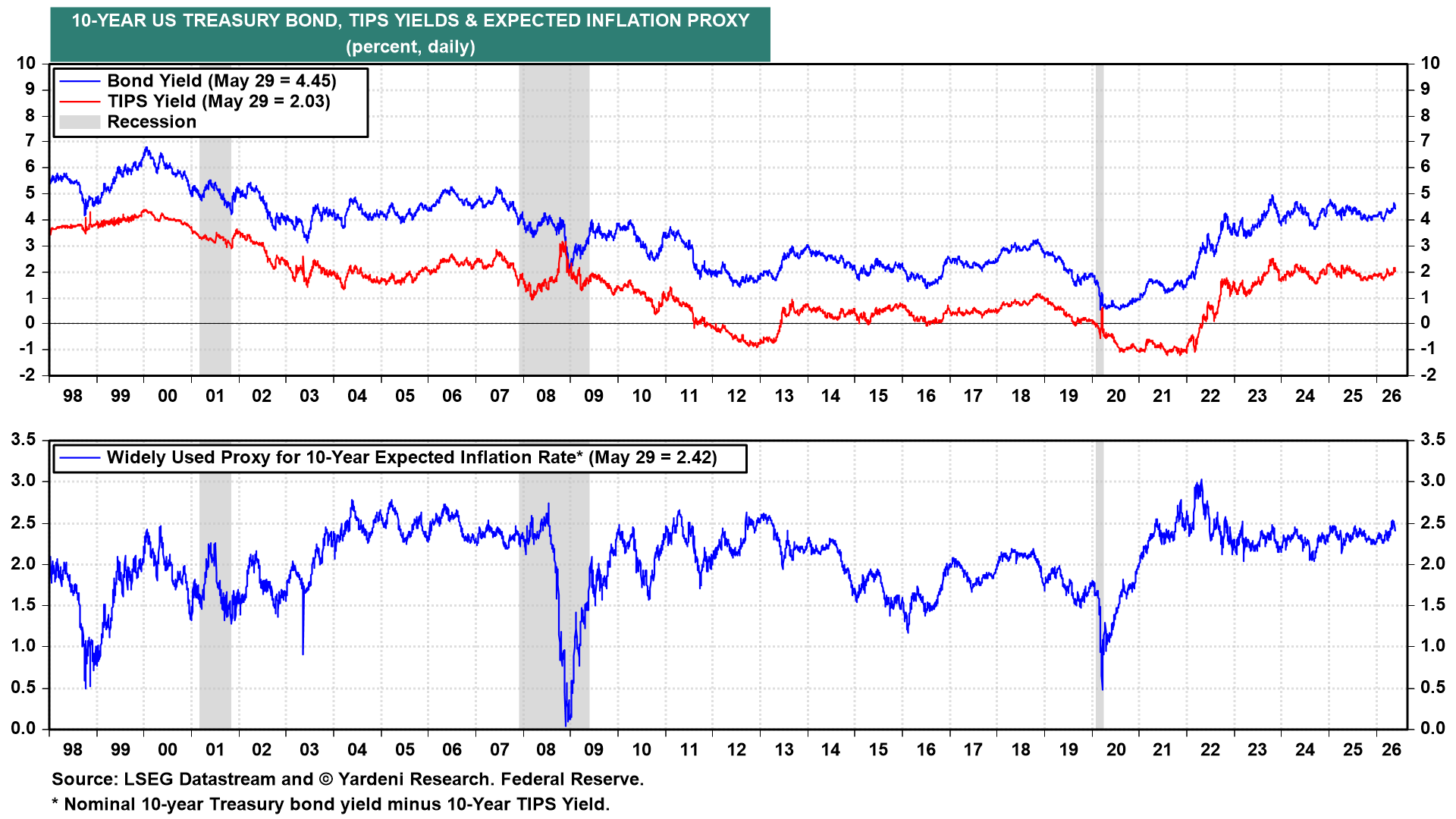

The 10-year US Treasury yield fell 12 basis points for the week to 4.45% (chart). So far, the bond yield continues to follow our "Old Normal" script. The 10-year Treasury yield has been range-bound between 4% and 5% since mid-2023. That was also its range (with a few brief exceptions) from 2001 to 2007 before the Great Financial Crisis and the Great Virus Crisis.

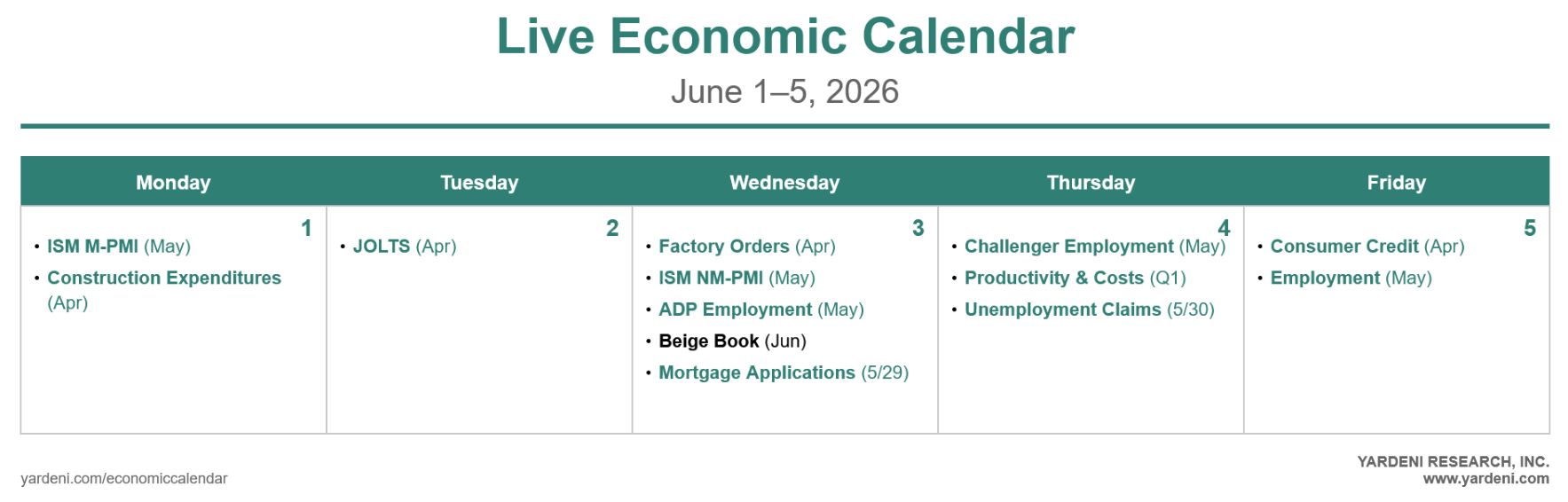

The week ahead is heavy on labor market data releases, including JOLTS (Tue), ADP private payrolls (Wed), Challenger layoff announcements (Thu), and BLS employment (Fri). ISM PMI reports will be released on Monday (manufacturing) and Wednesday (non-manufacturing). Thursday brings revised Q1-2026 productivity and unit labor costs, along with weekly jobless claims. Eight Fed speeches fill the docket, with Barr appearing twice plus Waller, Kashkari, Hammack, Logan, Barkin, and Daly. The Fed's Beige Book will be released on Wednesday afternoon. Broadcom reports its Q2 results on Wednesday.

Here are the key economic releases most likely to shape investors' thinking this week:

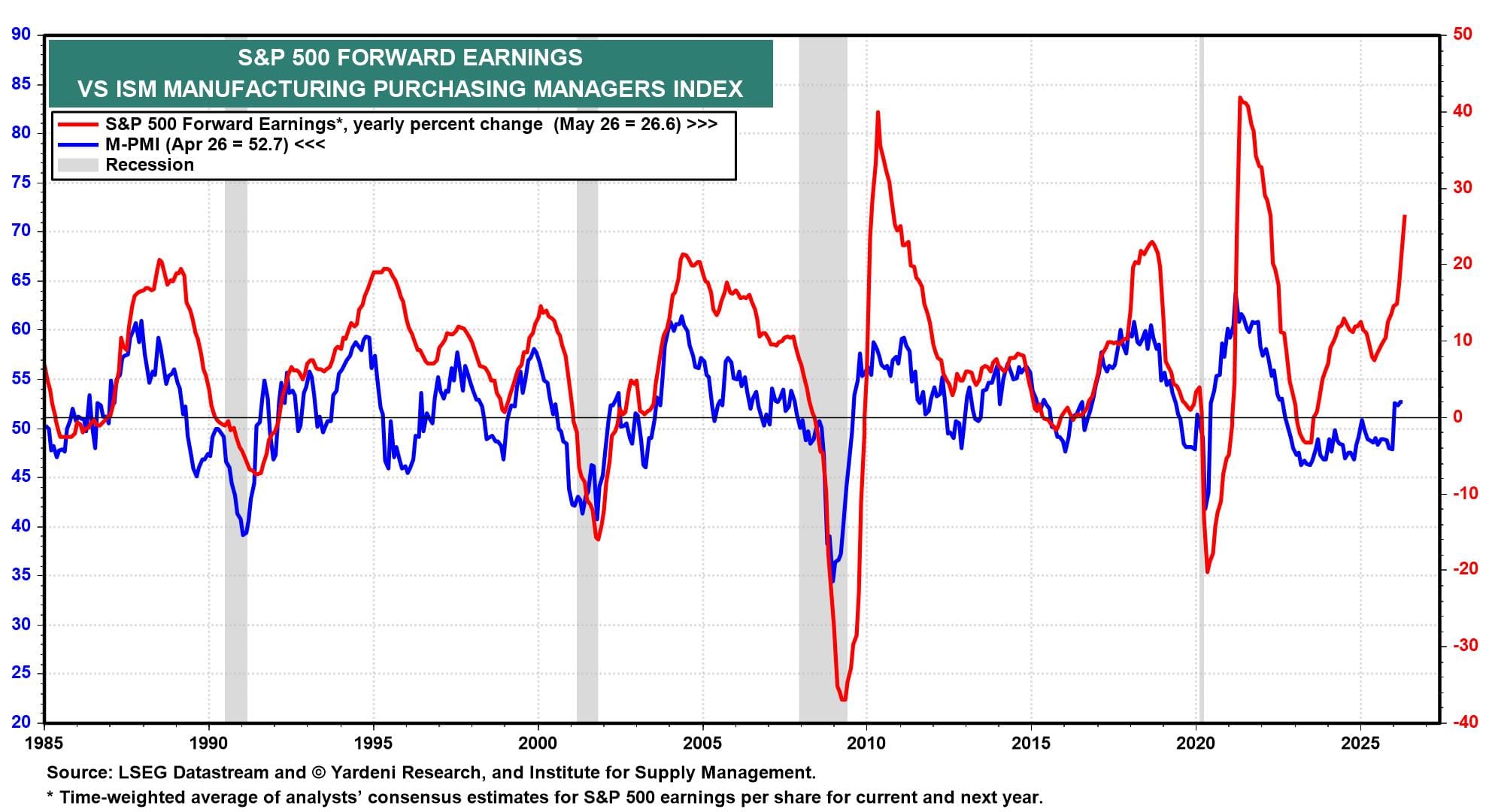

(1) ISM PMIs. ISM and S&P Global release the May results of their purchasing managers’ surveys this week, the M-PMI (Mon) and NM-PMI (Wed). Manufacturing has been expanding for four straight months as of April, while services industries’ business has been drifting lower but has remained in expansion. The y/y growth rate of S&P 500 forward earnings has tended to lead the M-PMI. The former is pointing to further upside for the latter, given recent FEMO (chart).

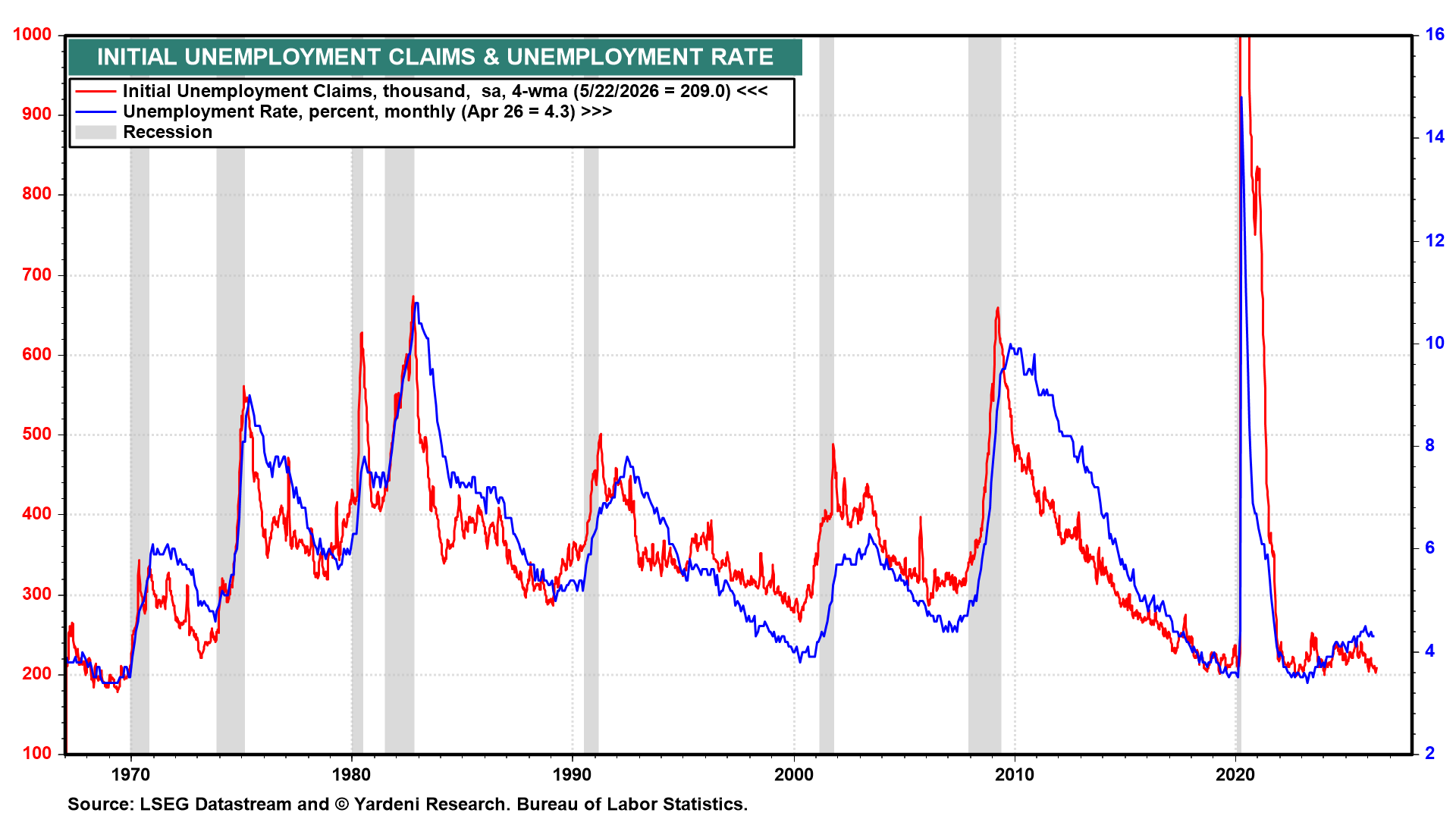

(2) Employment. May's employment report (Fri) is the headliner for the week. April's payrolls rose 115,000, with the three-month average cooling to 48,000. April's unemployment rate held at 4.3% and likely stayed there in May, given the low pace of initial unemployment claims.

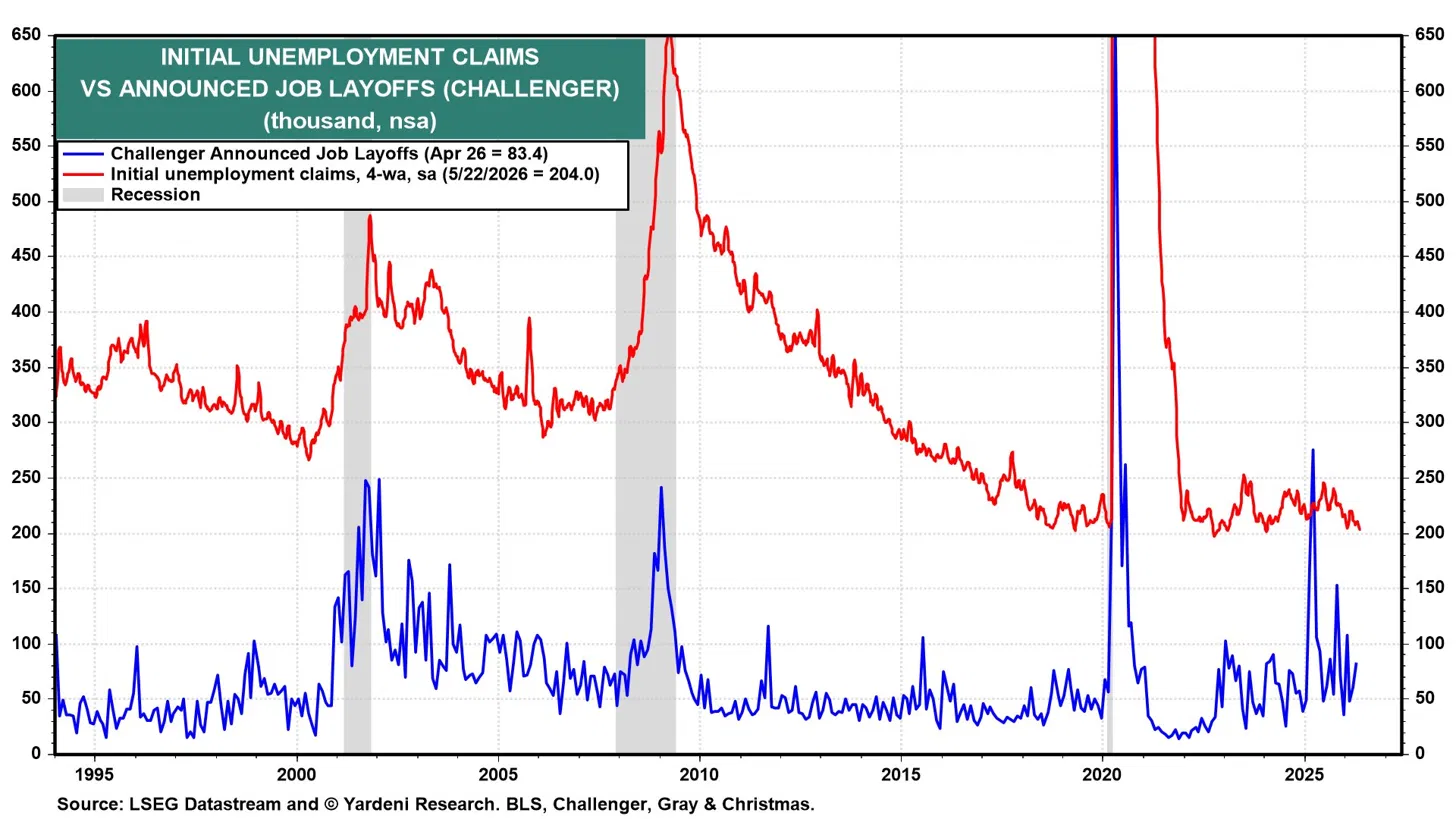

Jobless claims also suggest that Challenger layoff announcements (Thu) remained subdued in May. April's announced layoffs printed at 83,400, well below the 2022-2023 peaks (chart).

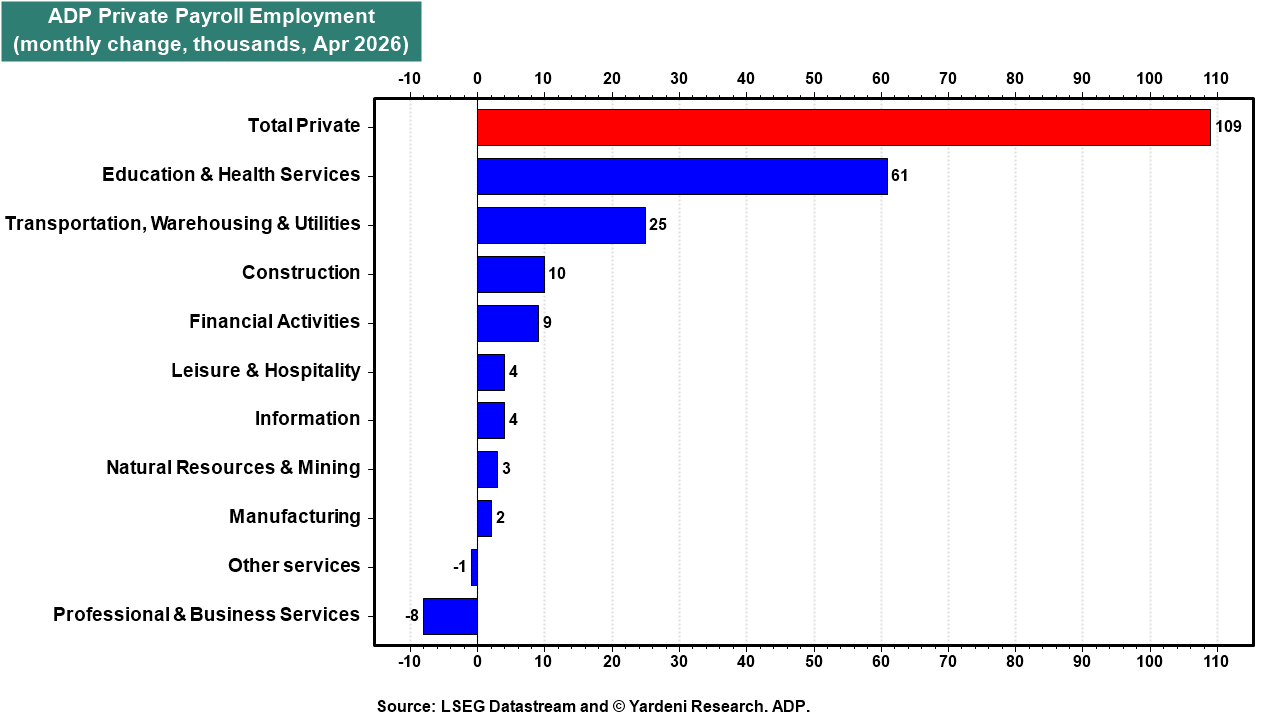

As we discussed on Thursday, the ADP NER Pulse implies a monthly private payroll pace of about 143,000 through May 9. May's ADP private payrolls report (Wed) should also confirm continued hiring strength. April's report came in at 109,000, with Education & Health Services contributing 61,000 (chart).

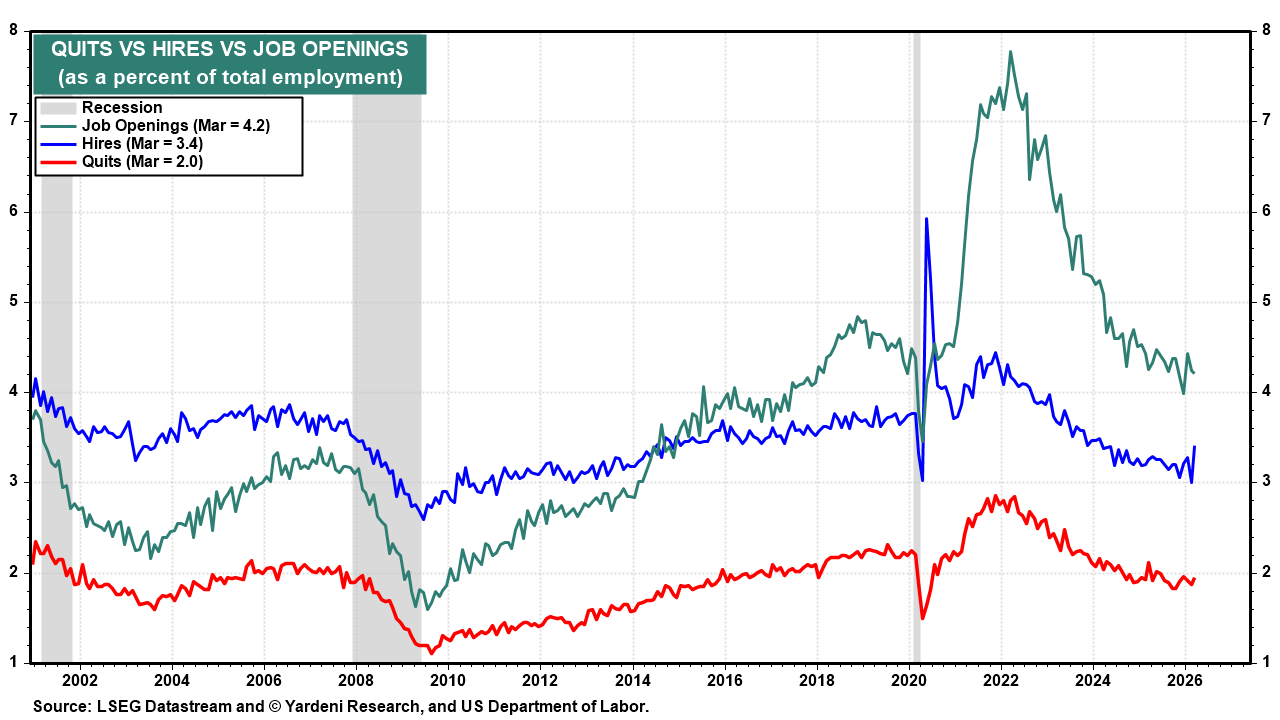

April's JOLTS data (Tue) should show labor market turnover activity continuing to normalize. March's quits rate held at 2.0%, back in its mid-2010s range. The job openings rate at 4.2% is also back to its pre-pandemic normal. The hires rate at 3.4% showed improvement (chart).

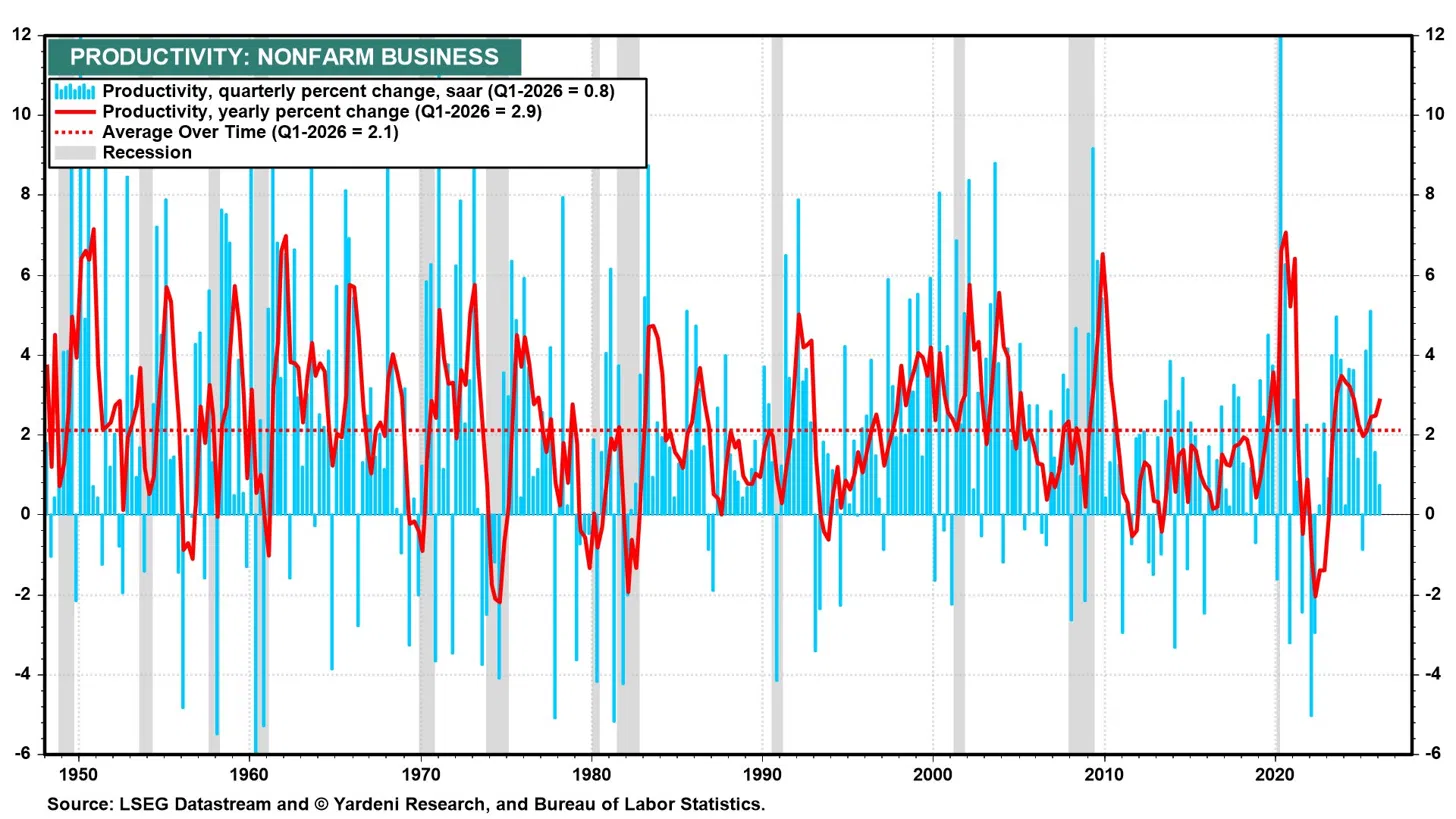

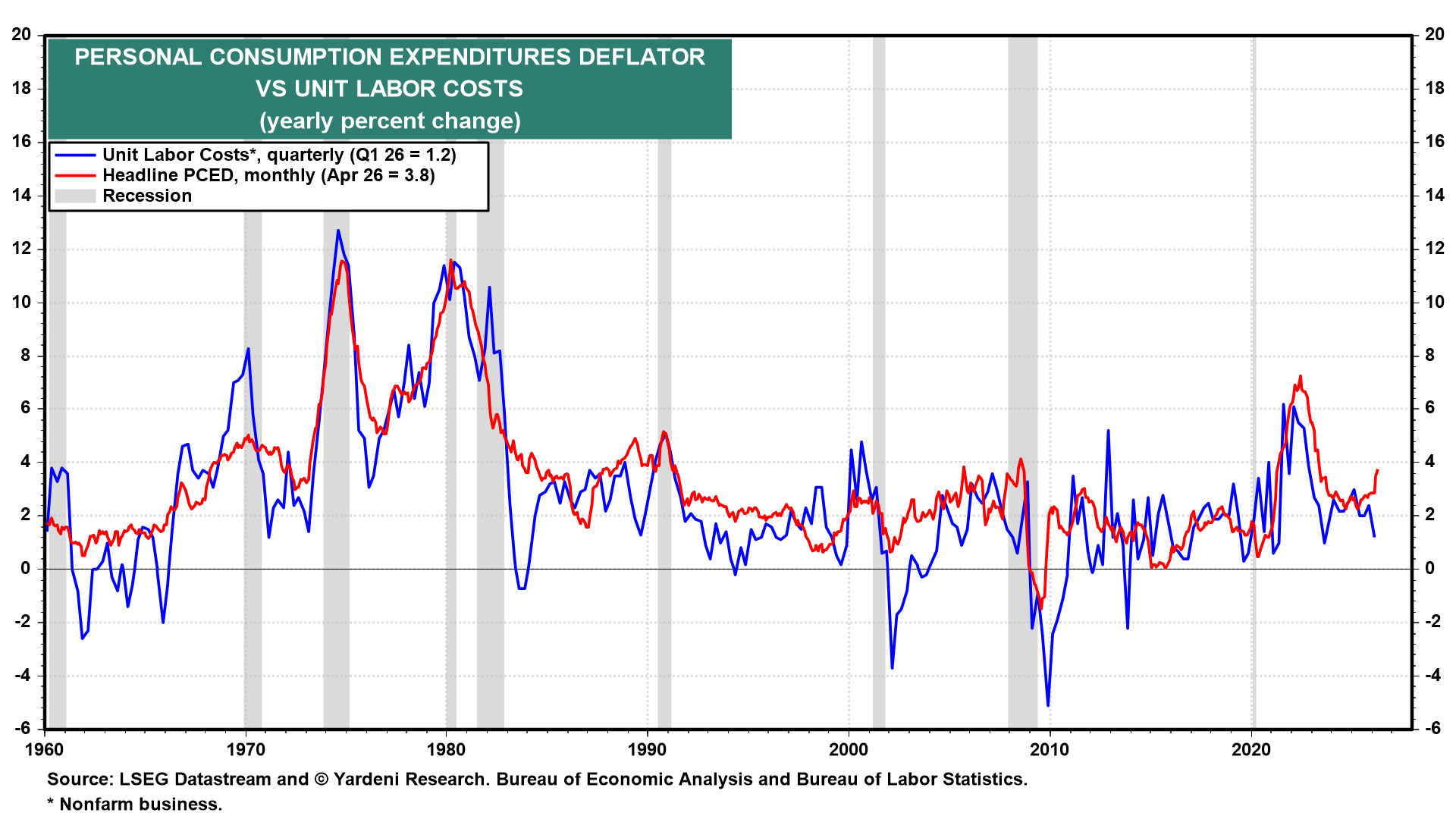

(3) Productivity and labor costs. Q1's revised nonfarm productivity and unit labor costs (Thu) should confirm the divergence underway between price and labor cost inflation. The headline PCED was 3.8% y/y in April, while unit labor costs rose just 1.2% over the past four quarters (chart).

According to the preliminary Q1 report, productivity rose 2.9% y/y, above its long-run average of 2.1% (chart). It might be revised down as was real GDP growth during Q1.