The US economic calendar is mostly quiet this week, but Thursday packs a heavy data load: final Q1-2026 GDP, May PCED, May durable goods orders, and weekly jobless claims.

Lots of Fedspeak will be provided by FOMC participants this week. They will not lack for opinions to compare with those Fed Chair Warsh expressed in his debut presser last week.

Globally, the Bank of Canada's Tiff Macklem speaks alongside Tuesday's May CPI release, and flash PMIs from Germany, France, the Eurozone, and the UK also drop on Tuesday.

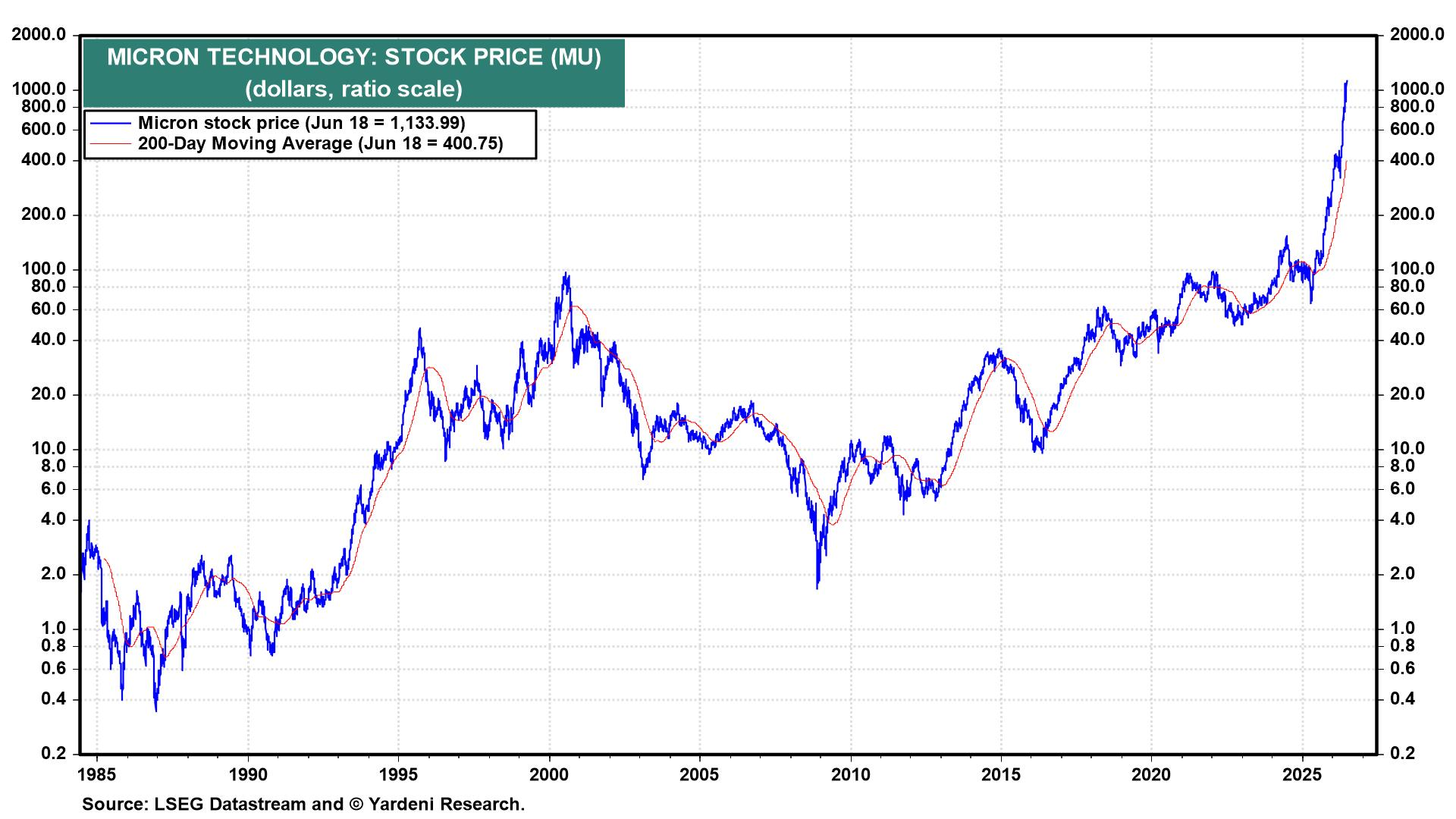

On Wednesday after the close, Micron Technology, arguably one of the world's most important companies, reports fiscal Q3 earnings (chart).

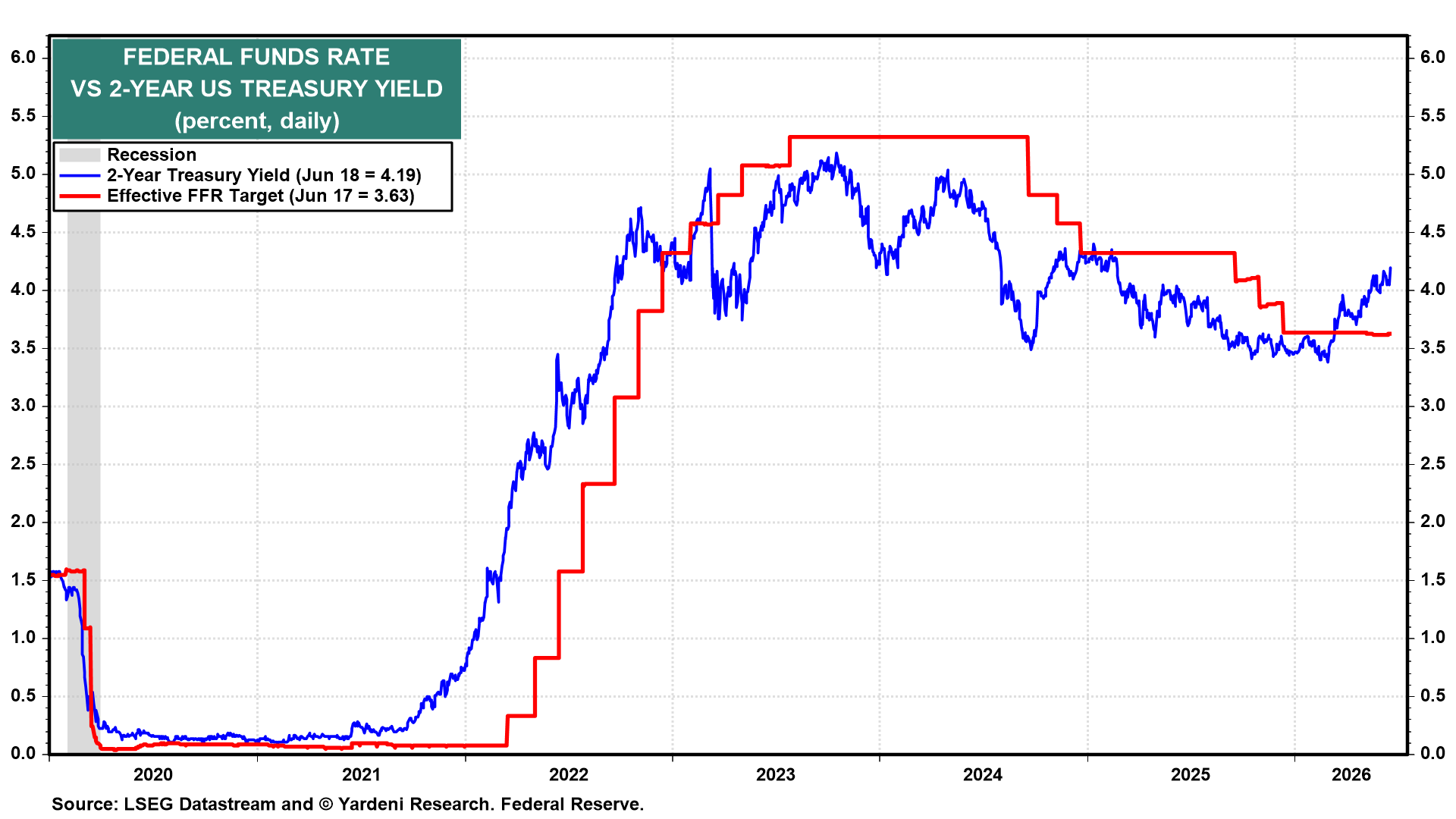

Wednesday's FOMC meeting reset the bar. The June Summary of Economic Projections raised the median 2026 federal funds rate projection from 3.4% to 3.8% and the median 2026 core PCED inflation projection from 2.7% to 3.3%. Nine of 18 dots now pencil in hikes by year-end. The 2-year US Treasury note jumped to 4.19% in response (chart).

Warsh's first press conference left no ambiguity. He called inflation "a choice," insisted price stability is the FOMC's number-one goal, and signaled the Fed will look through any supply-side disinflation from Iran. We continue to expect a first hike as soon as July. That expectation is more hawkish than the markets’, which put the odds of a hike in July at just 38% and one by September at 92%.

Here are the key economic releases most likely to shape investors' thinking this week:

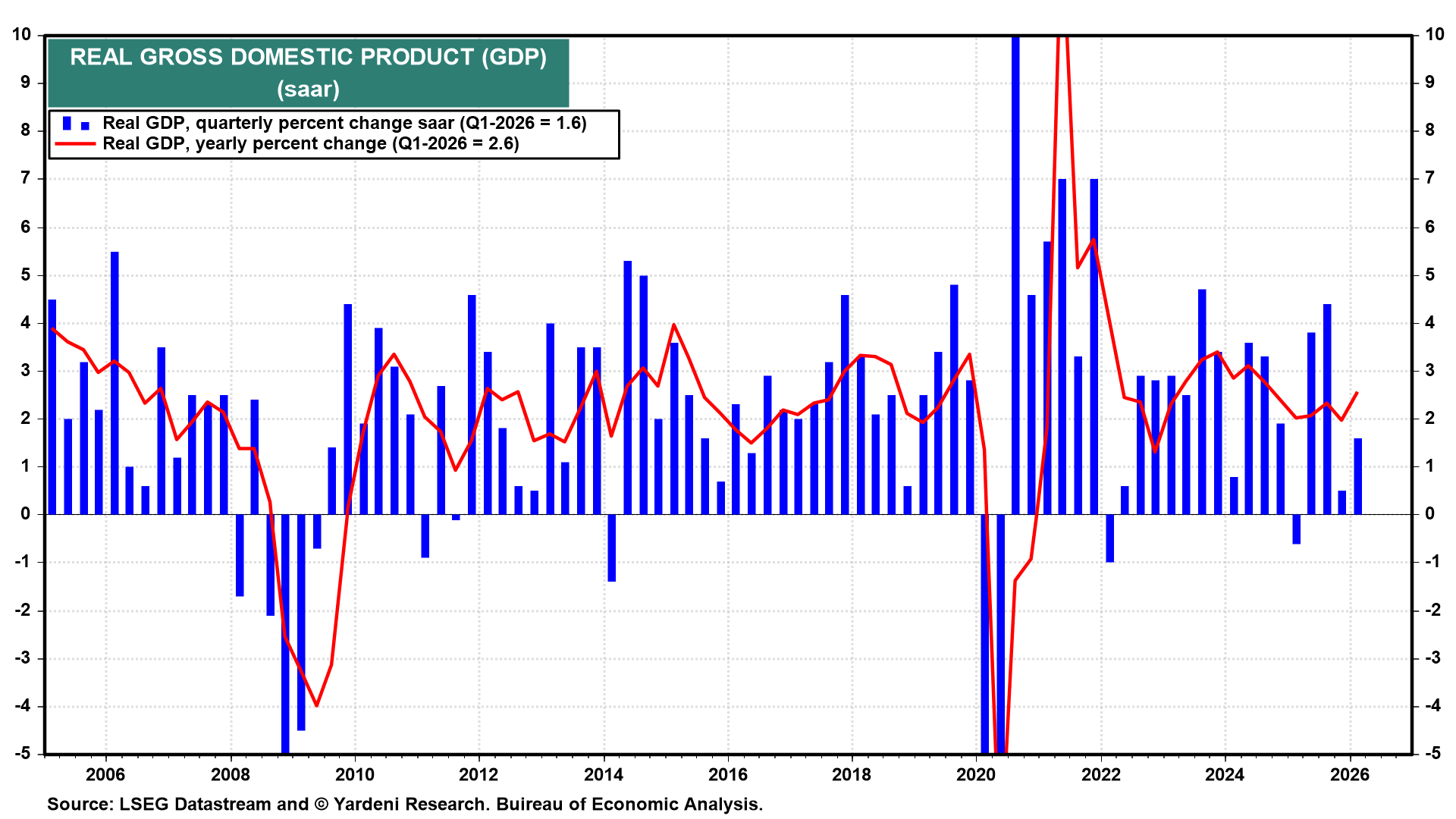

(1) GDP. The final reading of Q1-2026 GDP (Thu) should hold near the 1.6% second estimate (chart).

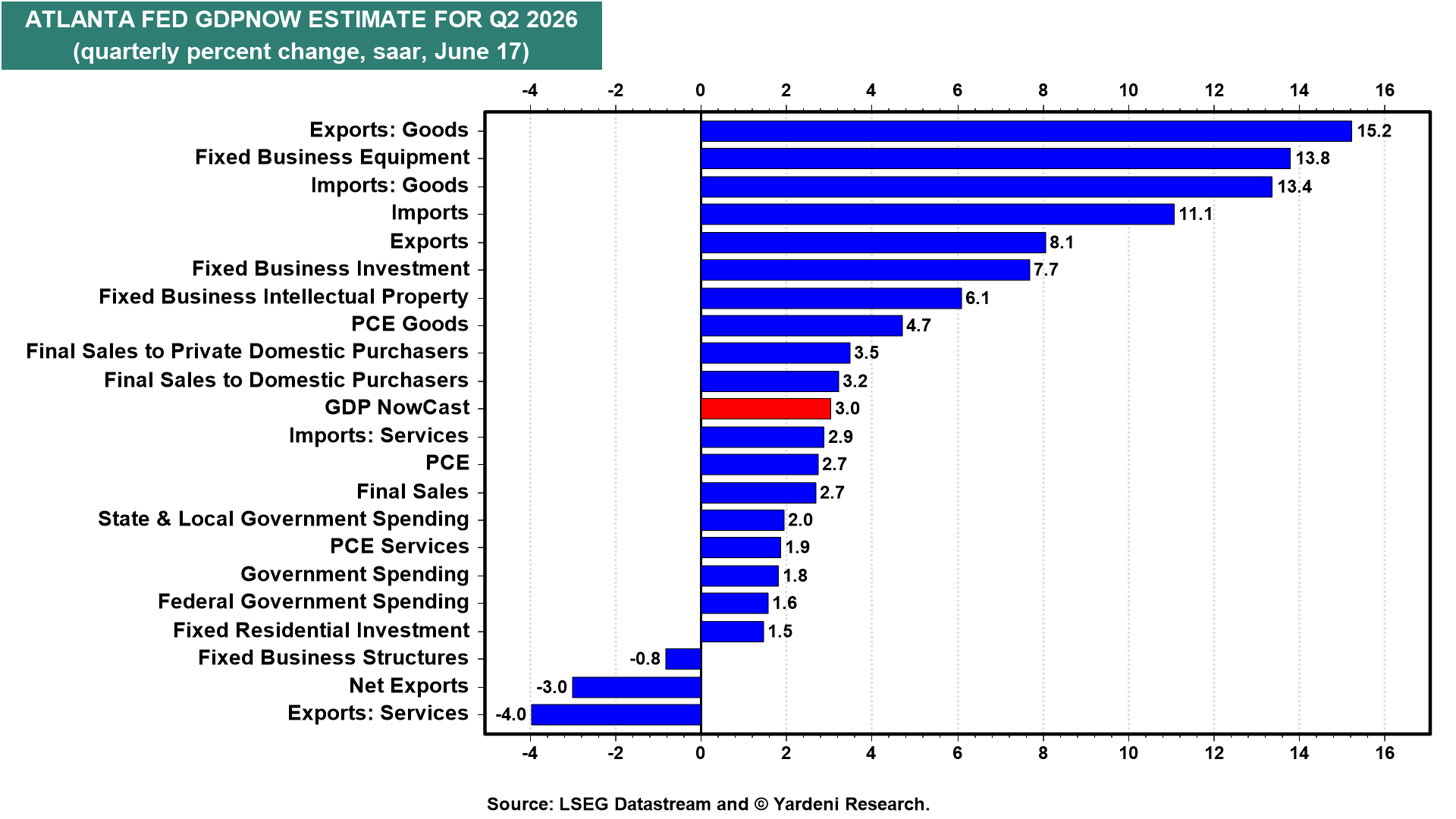

The Atlanta Fed's GDPNow model has Q2-2026 tracking 3.0% saar as of June 17, led by surging fixed business equipment (+13.8%) and goods exports (+15.2%) (chart). The AI-led capex cycle remains the engine of the Roaring 2020s.

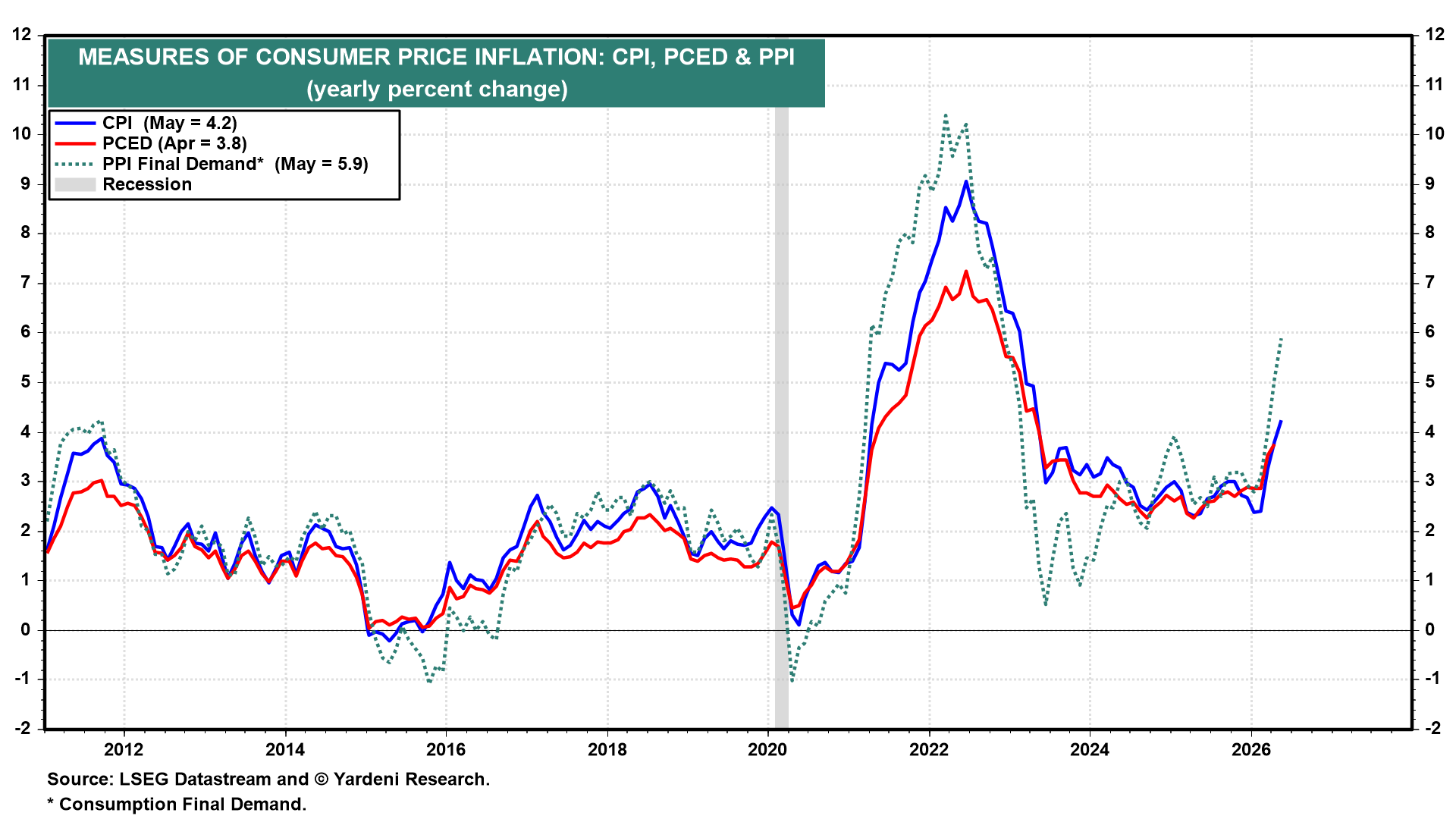

(2) PCED. May's headline and core PCED (Thu) are expected to be up 0.38% and 0.24%, according to the Cleveland Fed's Inflation Nowcasting. On a y/y basis, the numbers are hot at 3.97% and 3.30%. April's headline and core PCED inflation rates were 3.8% and 3.3% y/y. May's CPI rose 4.2% y/y, and PPI Final Demand rose 5.9% (chart). The risk again skews to an upside surprise.

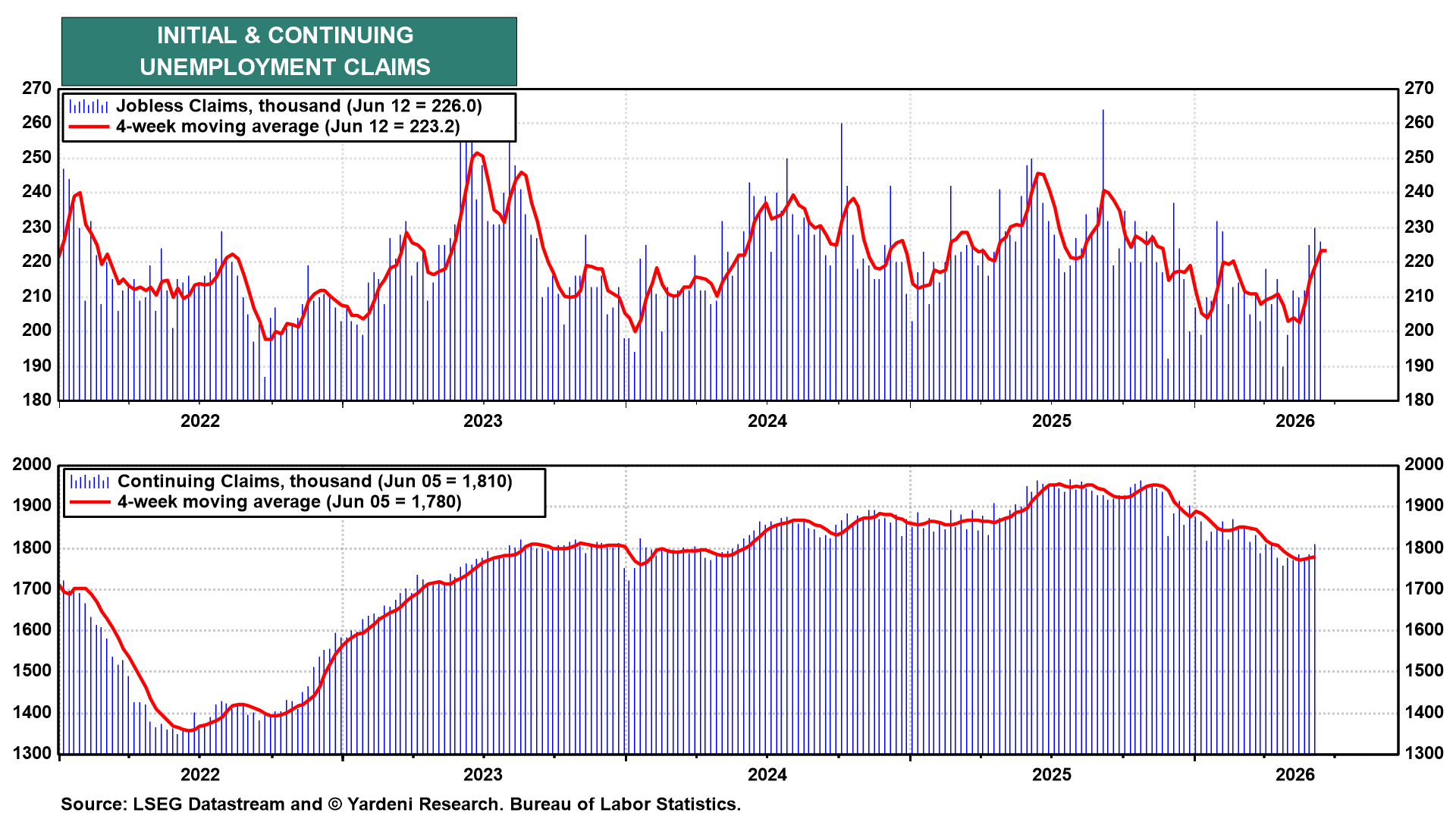

(3) Unemployment. Initial unemployment insurance claims (Thu) totaled 226,000 in the latest week, with the four-week moving average continuing to rise to 223,200 (chart). Continuing claims were 1,810,000 in the week ended June 5, with the four-week moving average rising to 1,780,000.

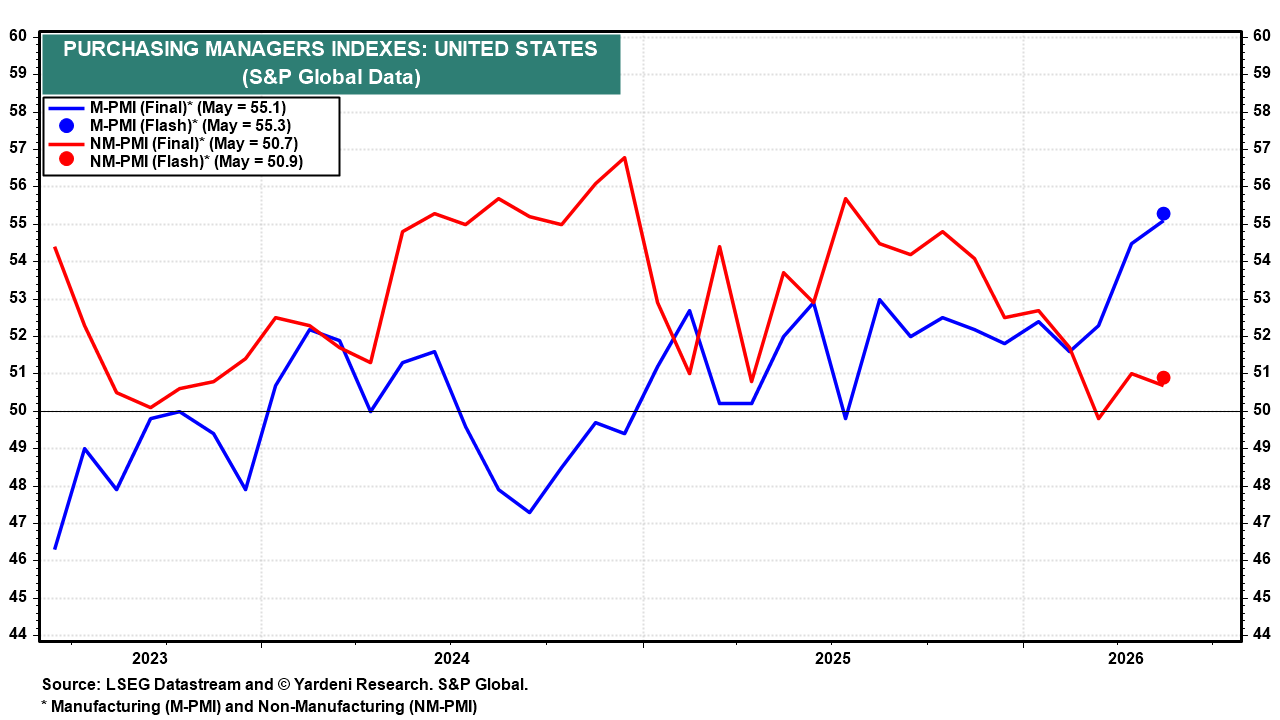

(4) PMIs and business surveys. S&P Global's June flash PMIs (Tue) follow May's final readings of 55.1 for manufacturing and 50.7 for services (chart).

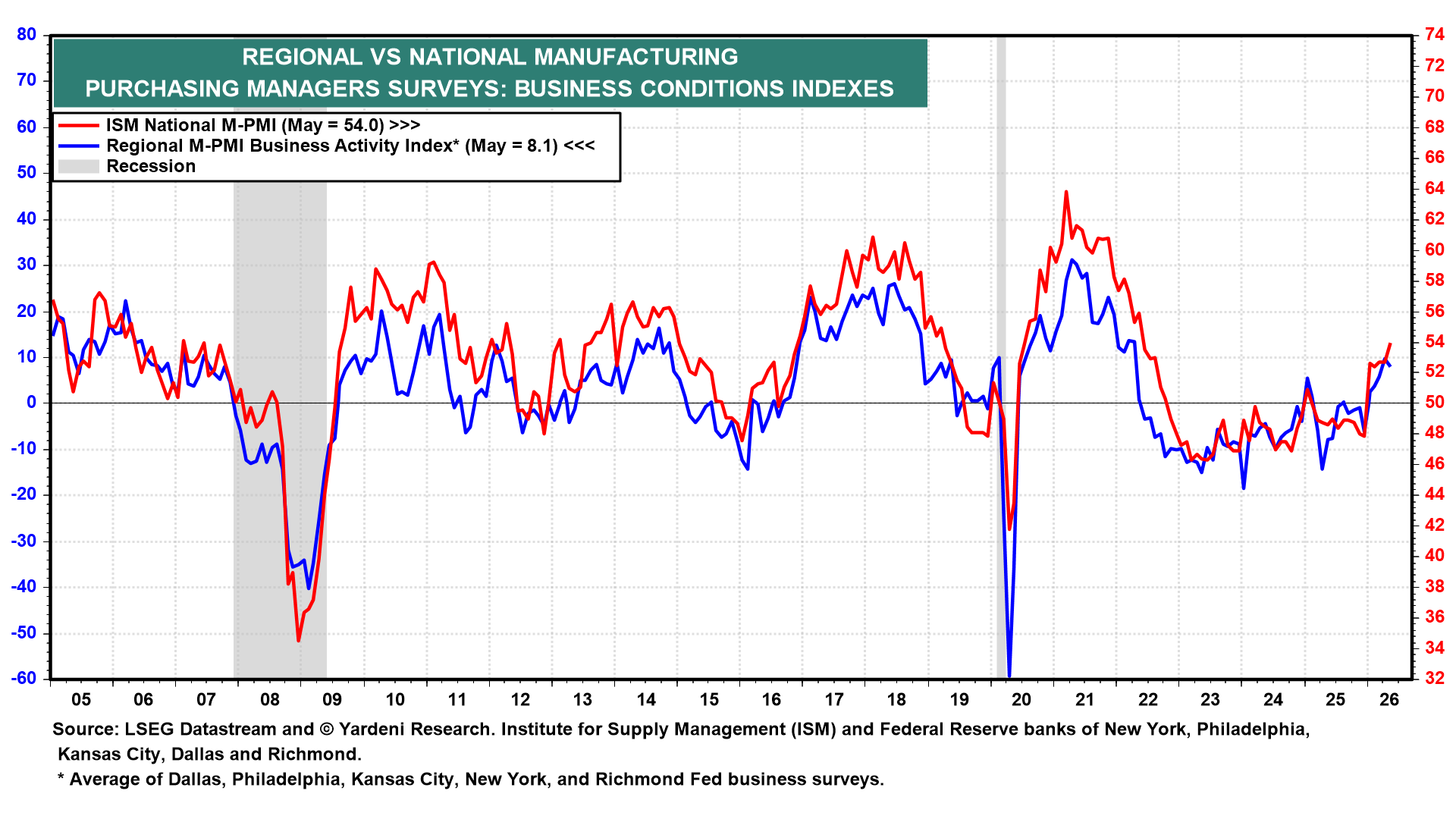

The week's regional Fed business surveys include Richmond (Tue), Chicago (Thu), and Kansas City (Thu). Both the ISM national M-PMI and the regional Fed average have turned higher in recent months, confirming that the manufacturing recovery is broadening (chart). Prices-paid components remain elevated, with the regional average at 55.2 in May, reinforcing the upside inflation risk.

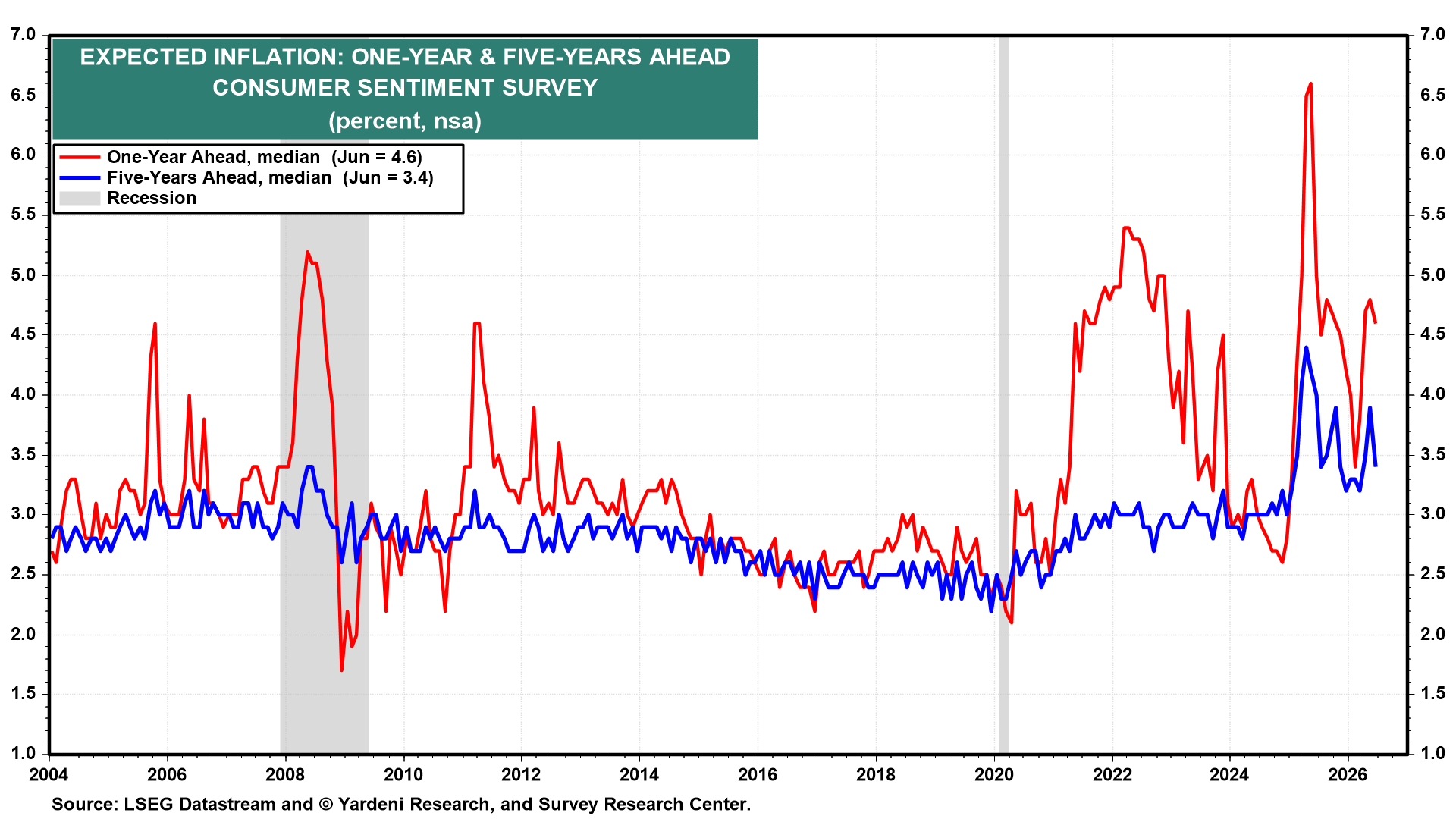

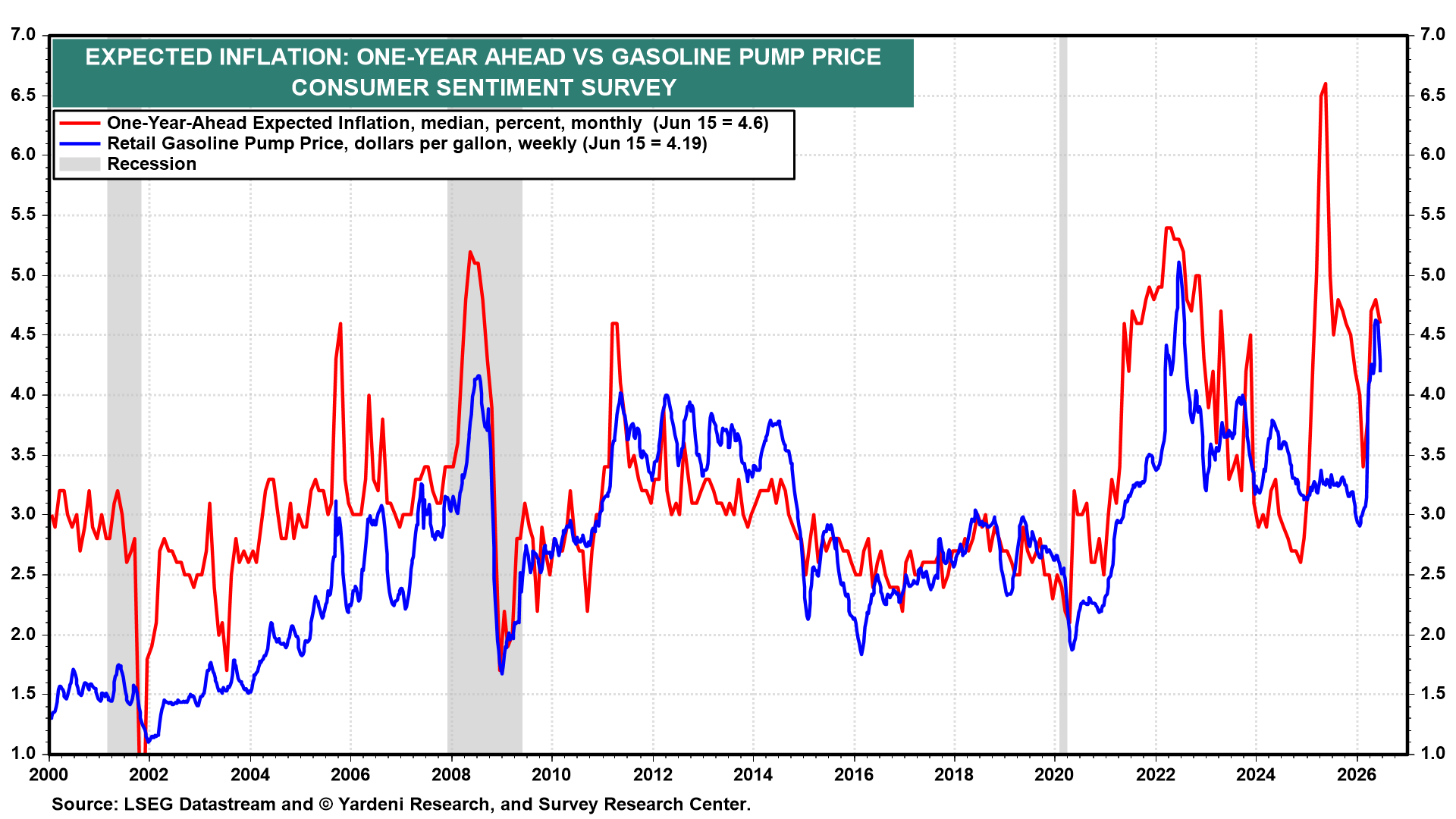

(5) Consumer sentiment. The final June University of Michigan reading (Fri) follows June's preliminary print of 48.9, with current conditions at 48.4 and expectations at 49.3. The more important numbers are the one-year and three-year inflation expectations. The former should decline along with the price of gasoline (charts).