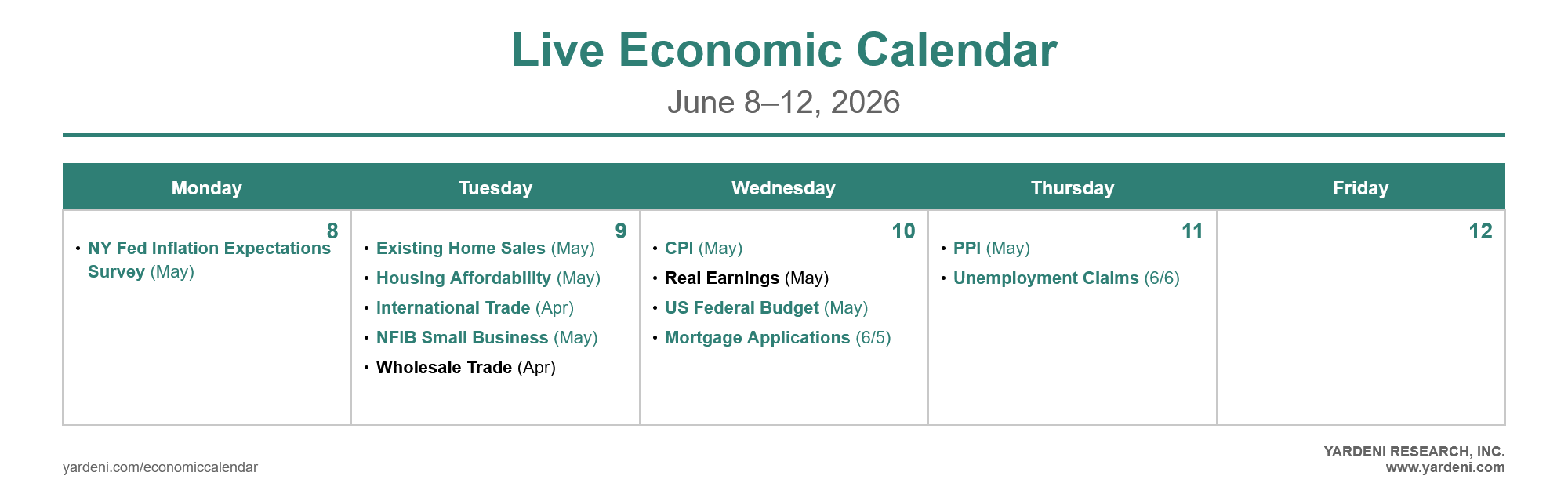

The week ahead is dominated by inflation prints. The May CPI (Wed) and PPI (Thu) top the calendar. From a consumer perspective, we will also see the NY Fed's consumer inflation expectations survey (Mon) and the University of Michigan’s preliminary sentiment release (Fri). The “Federal Open Mouth Committee” is in the blackout period ahead of next week's committee meeting—i.e., the talking Fed heads won't be talking. The Bank of Canada meets on Wednesday and is expected to hold its overnight rate steady at 2.25%. Most importantly, the SpaceX IPO will continue to dominate headlines, with the company's stock set to begin trading on Friday.

The S&P 500 closed Friday at 7,383.74, 7.7% above its 200-day moving average (chart). The equal-weight index closed at 8,398.26, also well above its 200-dma. Friday's session retreated after a much stronger-than-expected May payrolls gain of 172,000, which increased the odds of a Fed rate hike in coming months. The broad uptrend in stock prices remains intact across both market-cap and equal-weight measures.

Here are the key economic releases most likely to shape investors' thinking this week:

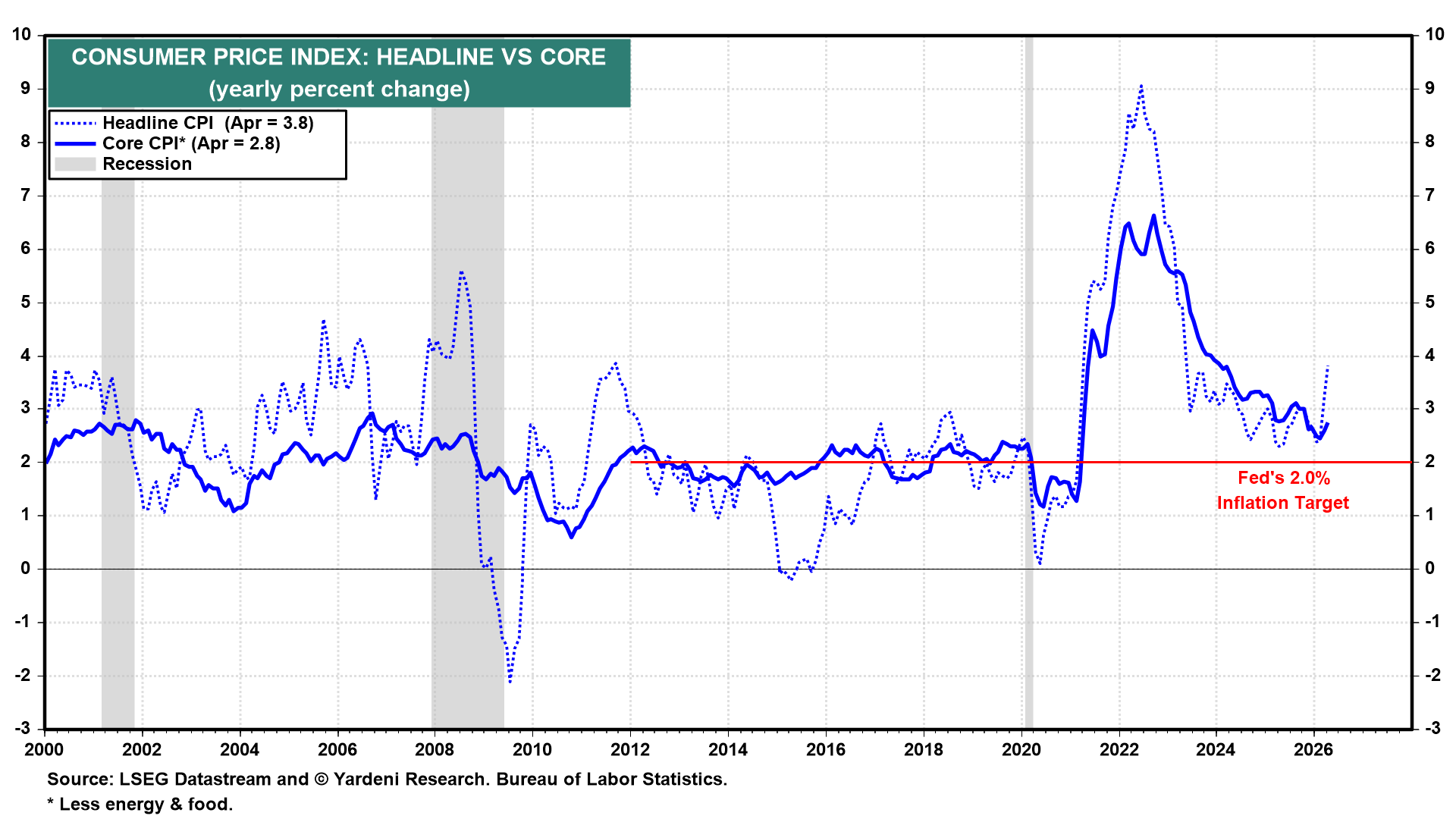

(1) Inflation. The Cleveland Fed Inflation Nowcasting model has May's headline CPI (Wed) rising 0.46% m/m, enough to push the annual rate to 4.18% y/y, up from 3.8% in April. The core CPI looks more benign, rising 0.23% m/m, with the annual rate edging up to 2.82% y/y from 2.80% in April (chart). The model's June preliminary nowcast points to headline inflation easing back to 4.05% y/y, reflecting the recent drop in nearby gasoline futures to $3.05 on June 5 from above $3.70 earlier this year.

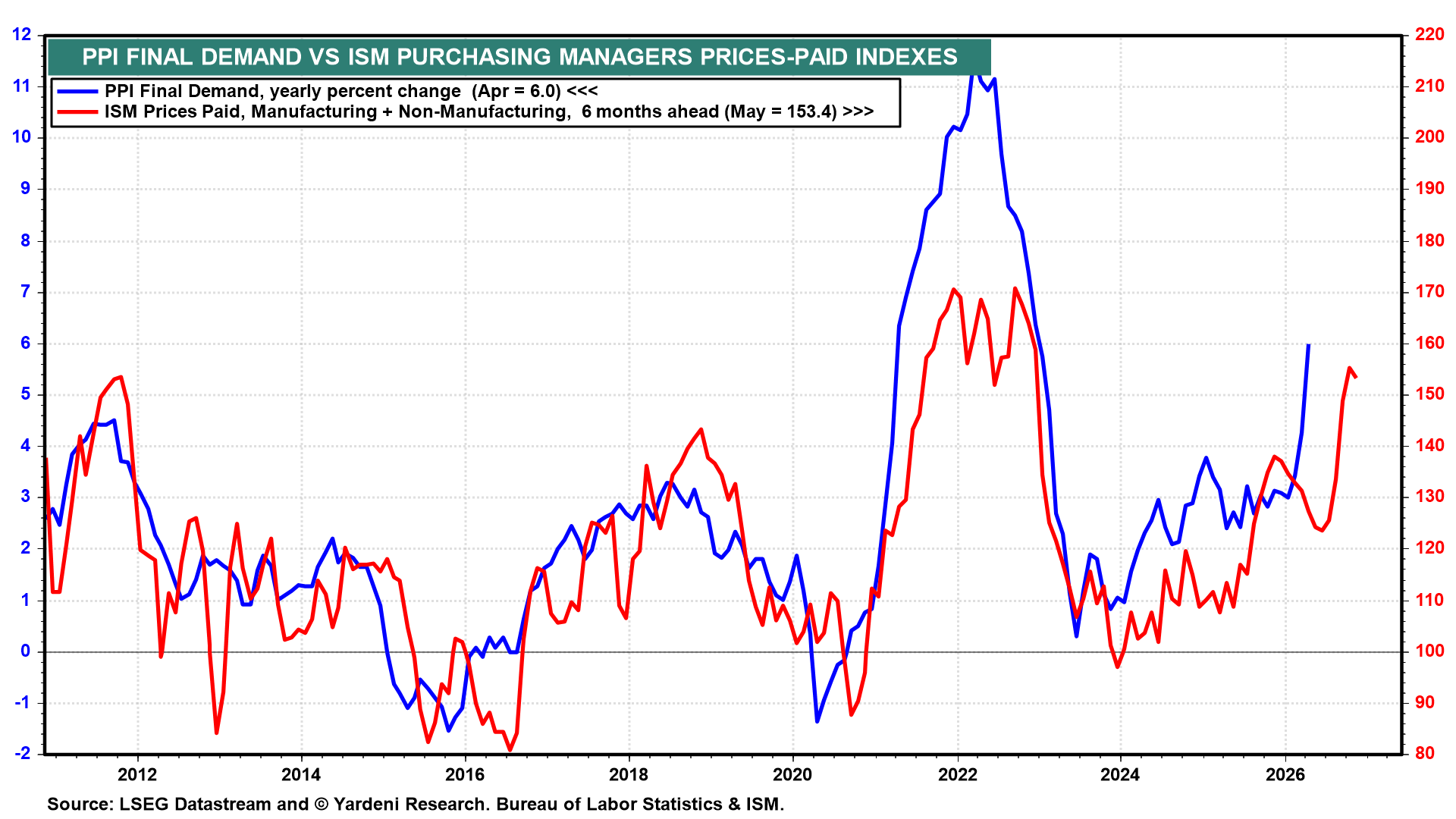

April's PPI Final Demand rose 6.0% y/y. The composite ISM Prices-Paid Index, a six-month forward inflation signal, eased to 153.4 in May from 155.3 in April but remains elevated (chart).

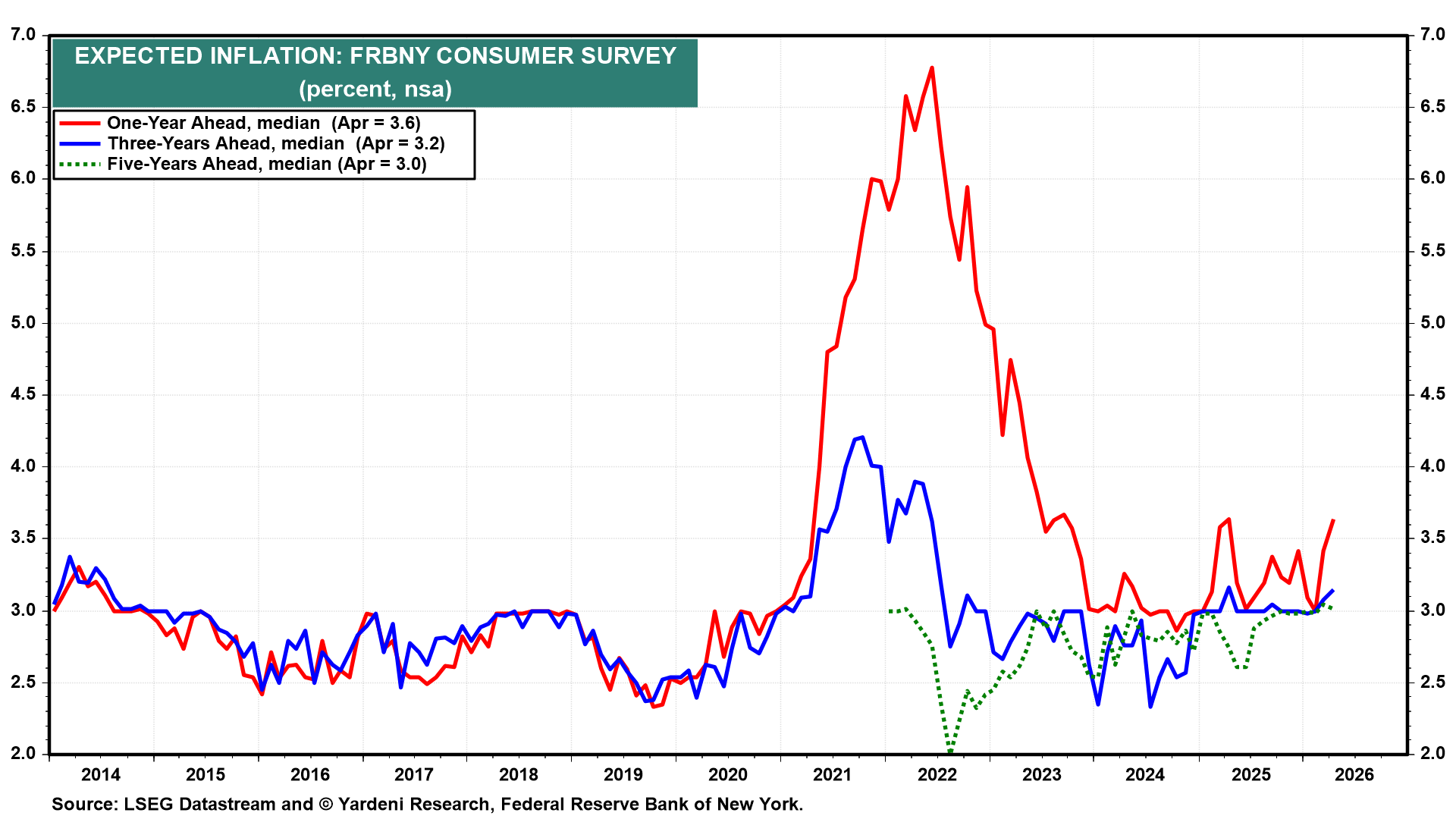

(2) Inflation expectations. The NY Fed's Survey of Consumer Expectations (Mon) covers May. April's release showed the median one-year-ahead inflation expectation at 3.6%, with three-year expectations at 3.2% and five-year at 3.0% (chart). Long-term inflation expectations remain well anchored.

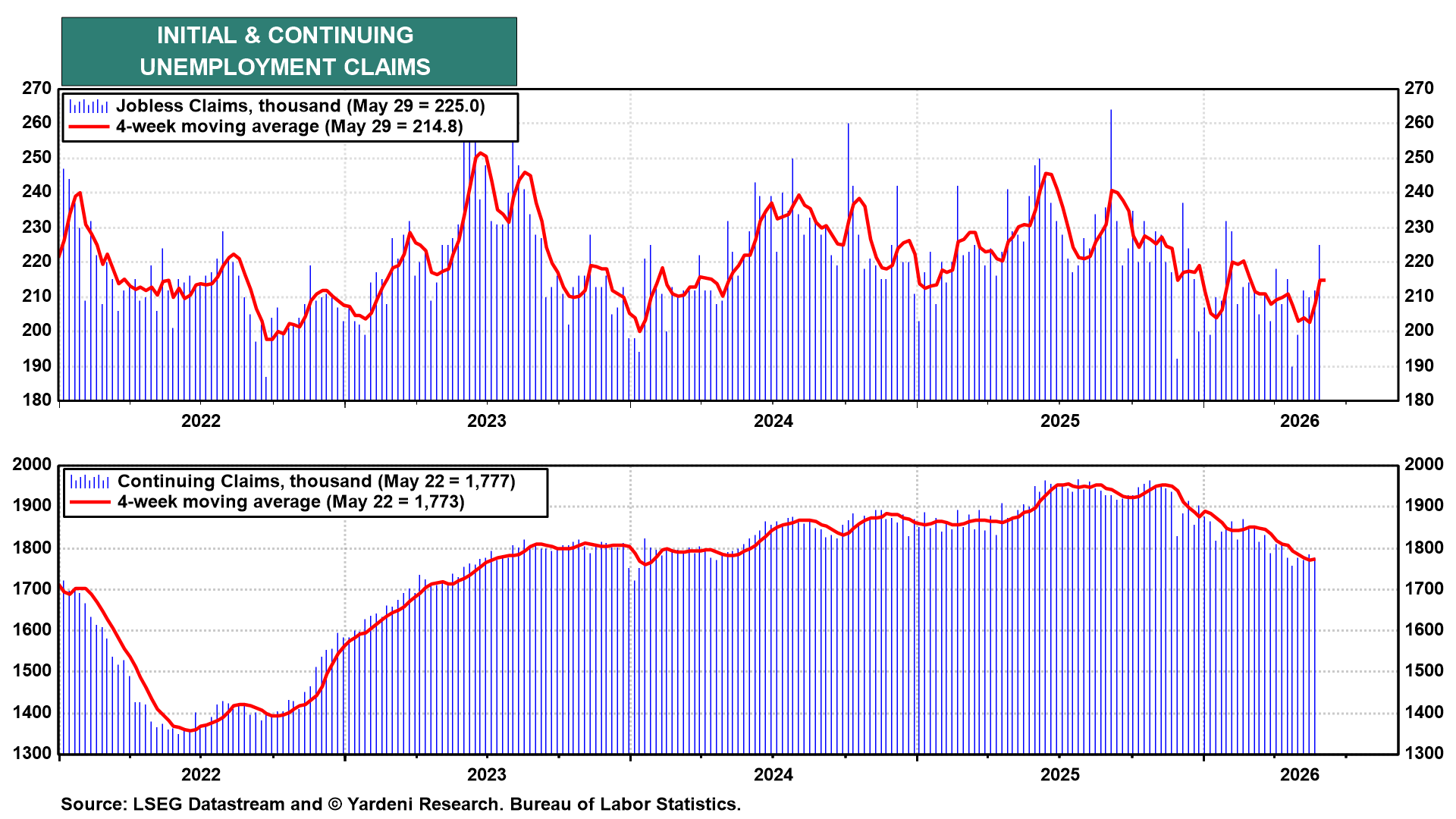

(3) Unemployment. Friday's 172,000 May payrolls increase is consistent with the subdued trajectory of initial jobless claims (Thu). Initial unemployment insurance claims printed at 225,000 for the week of May 29, with the four-week moving average ticking up to 214,800 (chart). The drift higher remains well below levels that would signal labor-market stress. Continuing claims are trending down. The labor market continues to add jobs without meaningfully shedding them.

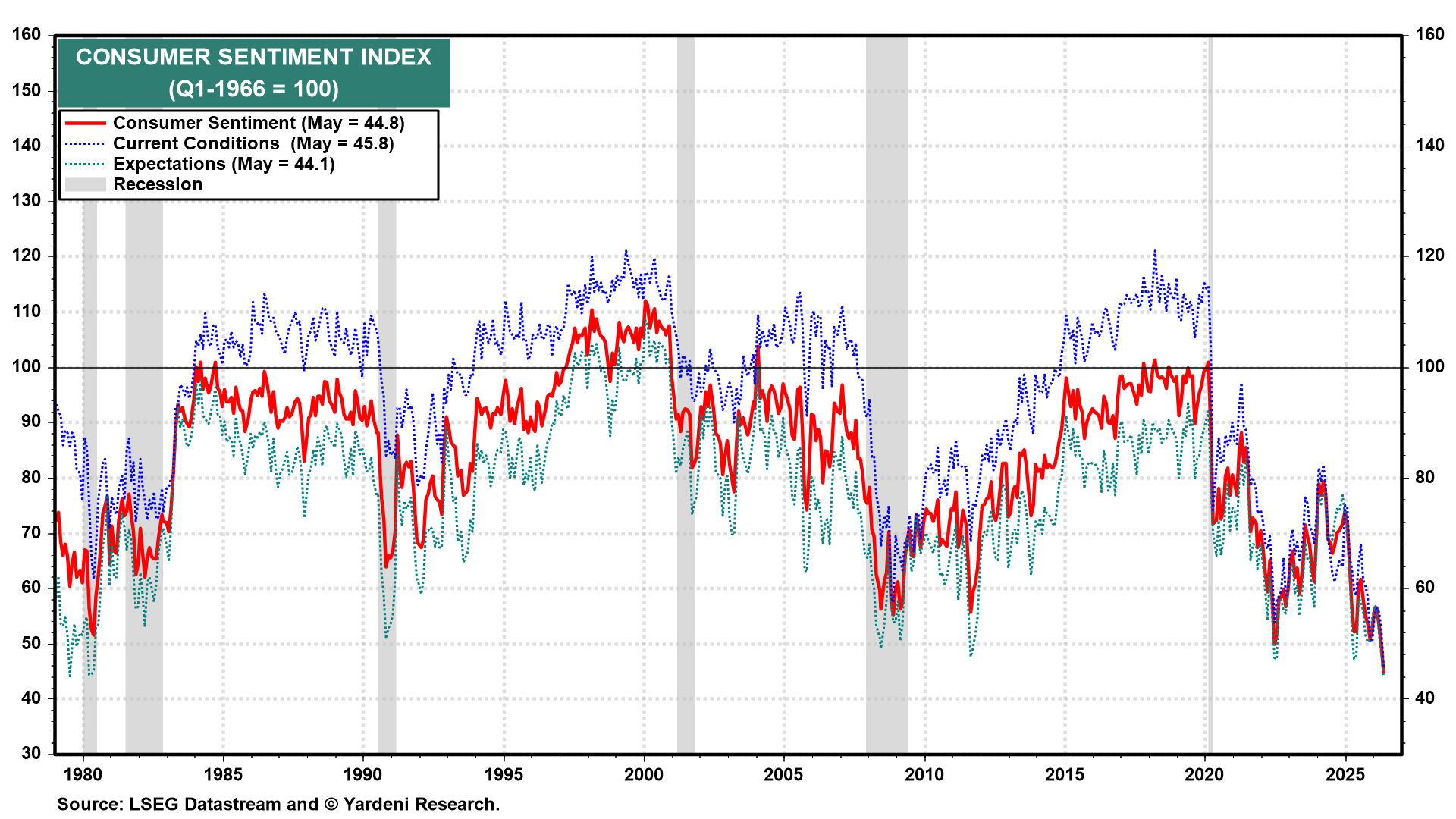

(4) Consumer sentiment. May’s final University of Michigan sentiment dropped to 44.8, an all-time low (chart). Current conditions printed at 45.8, with expectations a touch below the headline at 44.1. The June preliminary release (Fri) will test whether the strong May payrolls print has lifted sentiment off these depressed levels.

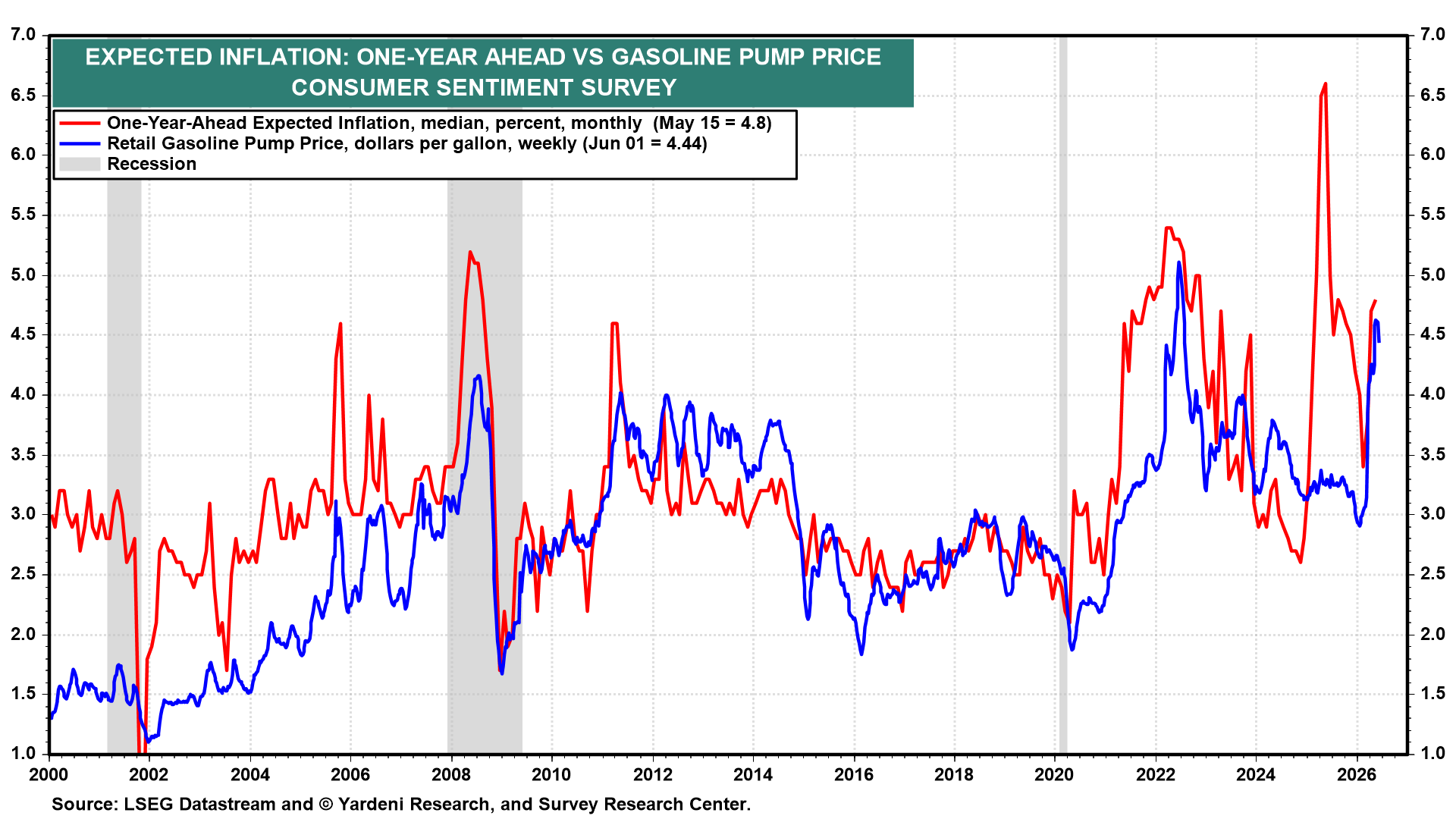

The one-year-ahead inflation expectations stood at 4.8% in May, tracking the trajectory of retail gasoline prices, which printed at $4.44 per gallon on June 1 (chart). Easing nearby gasoline futures should pull this expectation lower in the coming months.

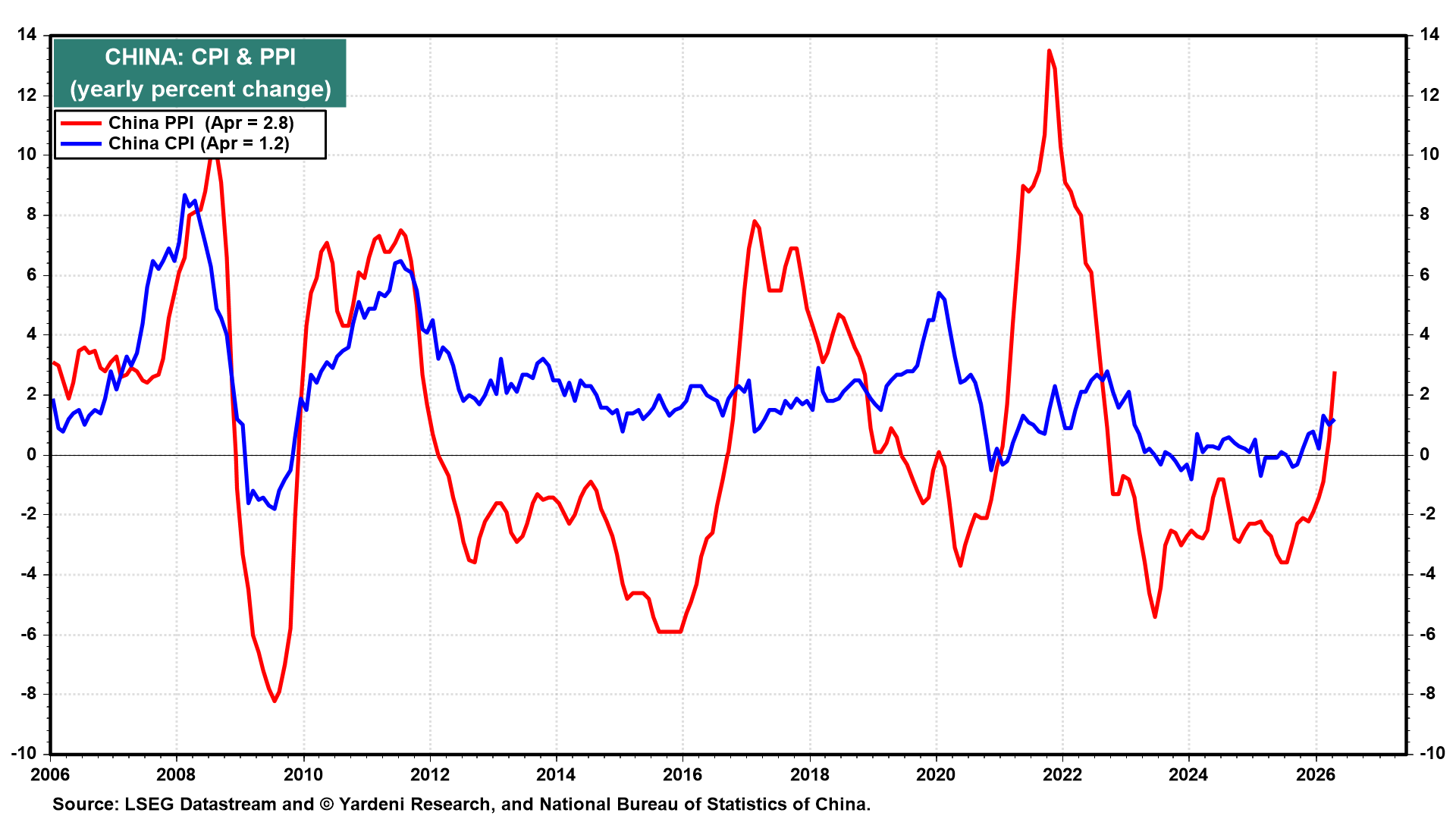

(5) Global inflation. April data showed China's CPI rising 1.2% y/y while the PPI climbed to 2.8%, the first sustained positive PPI reading after a long stretch of deflation (chart). May's release (Wed) is expected to show the CPI ticking up slightly.

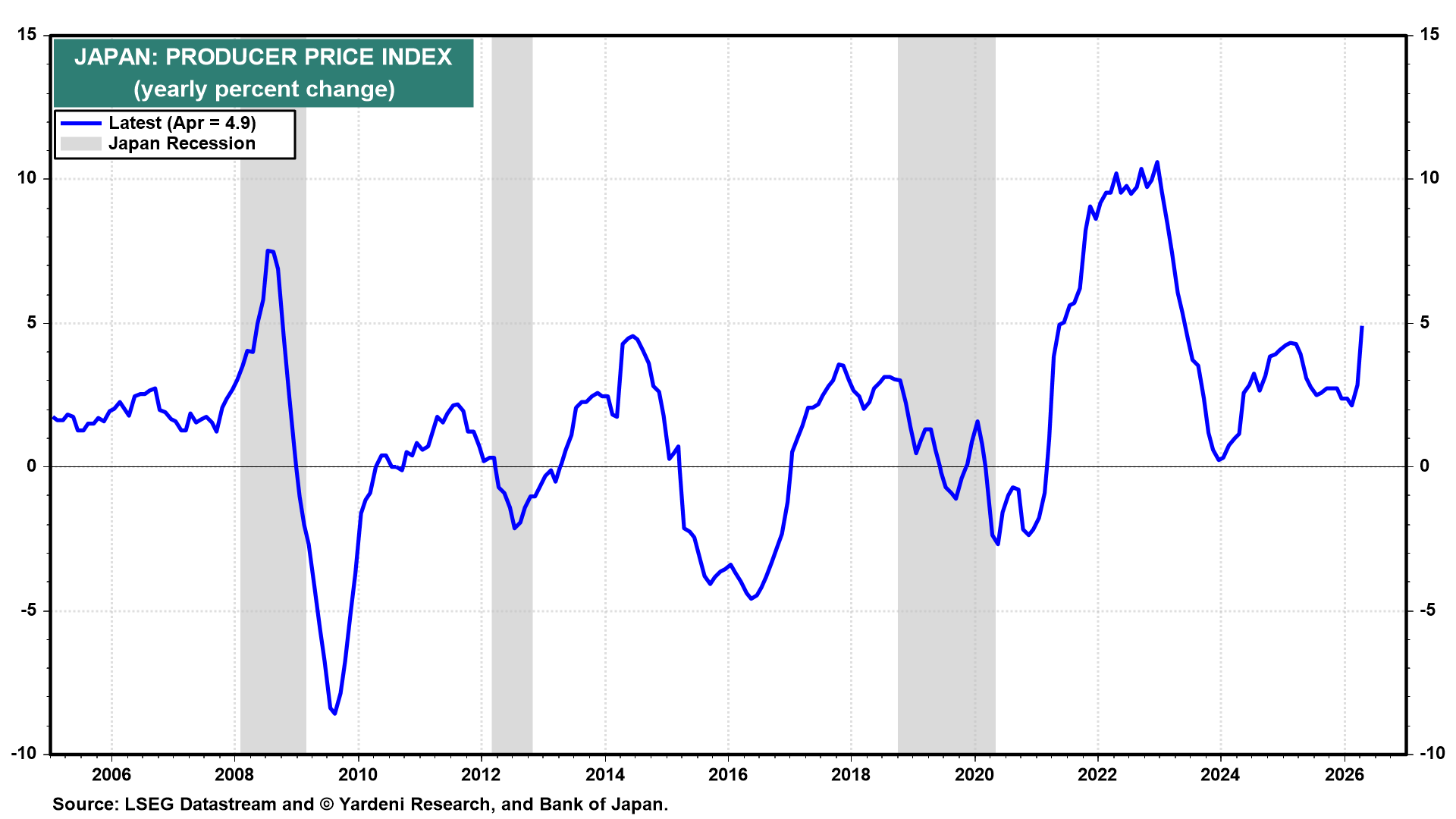

Japan's PPI (Tue) accelerated to 4.9% y/y in April and is expected to push above 5.0% in May (chart). Markets are pricing an 82% probability of a rate hike at the Bank of Japan’s June 16 meeting. A hot print would tip those odds close to certainty.