This week will continue to be dominated by developments in the Middle East. On Friday, the US and Israel struck Iranian nuclear and steel facilities, with Iran retaliating across the Persian Gulf, while President Trump pushed back a deadline for Tehran to reopen the Strait of Hormuz or face further attacks on its power infrastructure. The escalation marked a sharp shift in tone from earlier in the week, when the financial markets had stabilized following Trump’s walk-back of threats targeting Iran’s energy infrastructure.

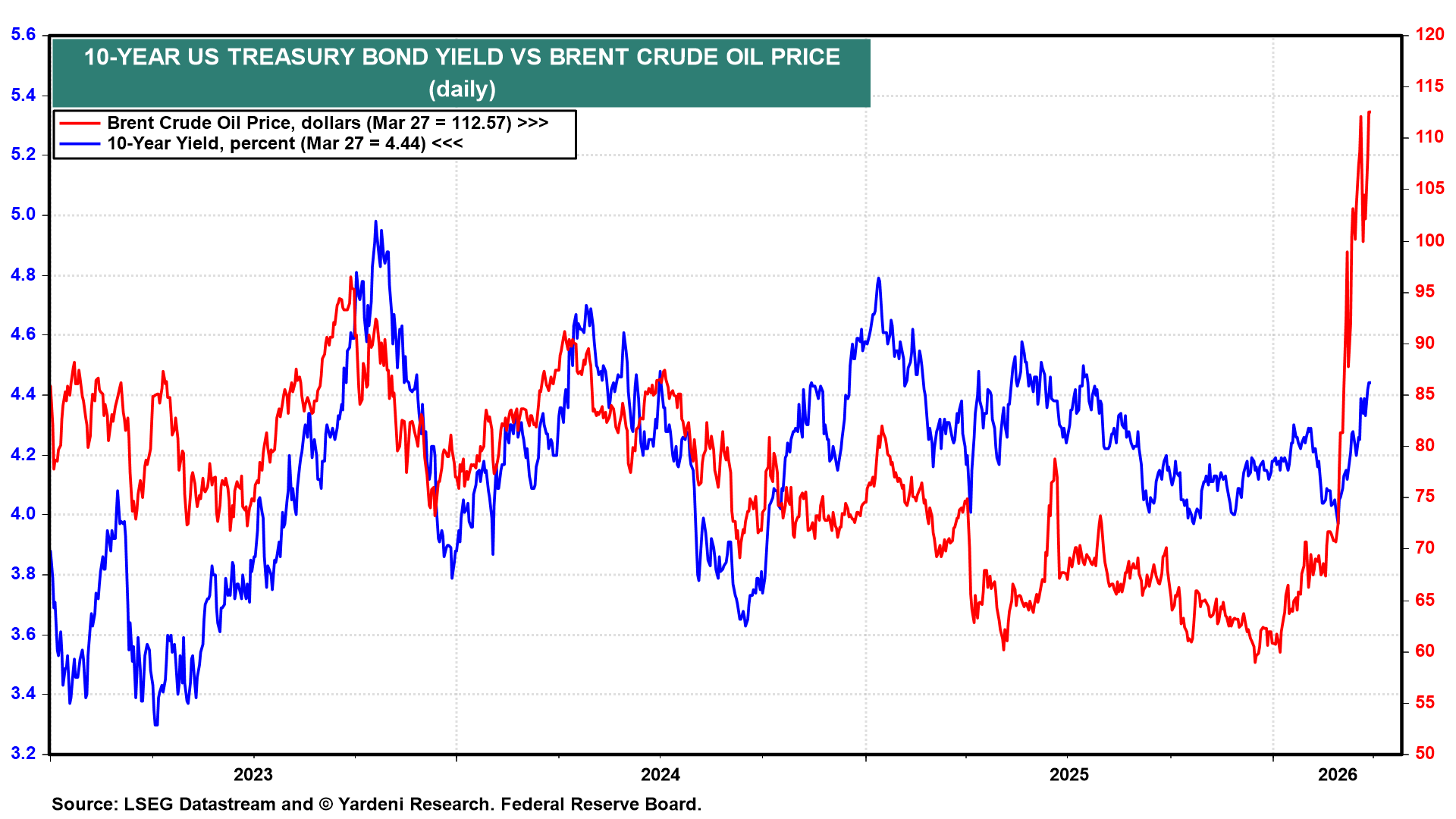

Oil markets have responded accordingly. WTI crude closed at $99.64 a barrel, up roughly 18.7% from Tuesday’s low of $83.96 and marking its highest weekly close since the conflict began, while Brent finished at $112.57, up about 16.6% from its weekly low of $96.52 (chart). The speed and magnitude of the move underscore how quickly energy markets are repricing geopolitical risk, challenging earlier efforts to keep both oil and bond markets anchored, and reinforcing the risk of sustained disruption in the Strait.

As a result, this week’s data will take on added significance. A heavy slate of releases, including consumer confidence, PMIs, and the March employment report, will provide the first meaningful read on how higher energy prices and heightened uncertainty are feeding through to the real economy. The key question is whether the US economy’s resilience can withstand this shock, or whether cracks begin to emerge across activity, sentiment, and the labor market.

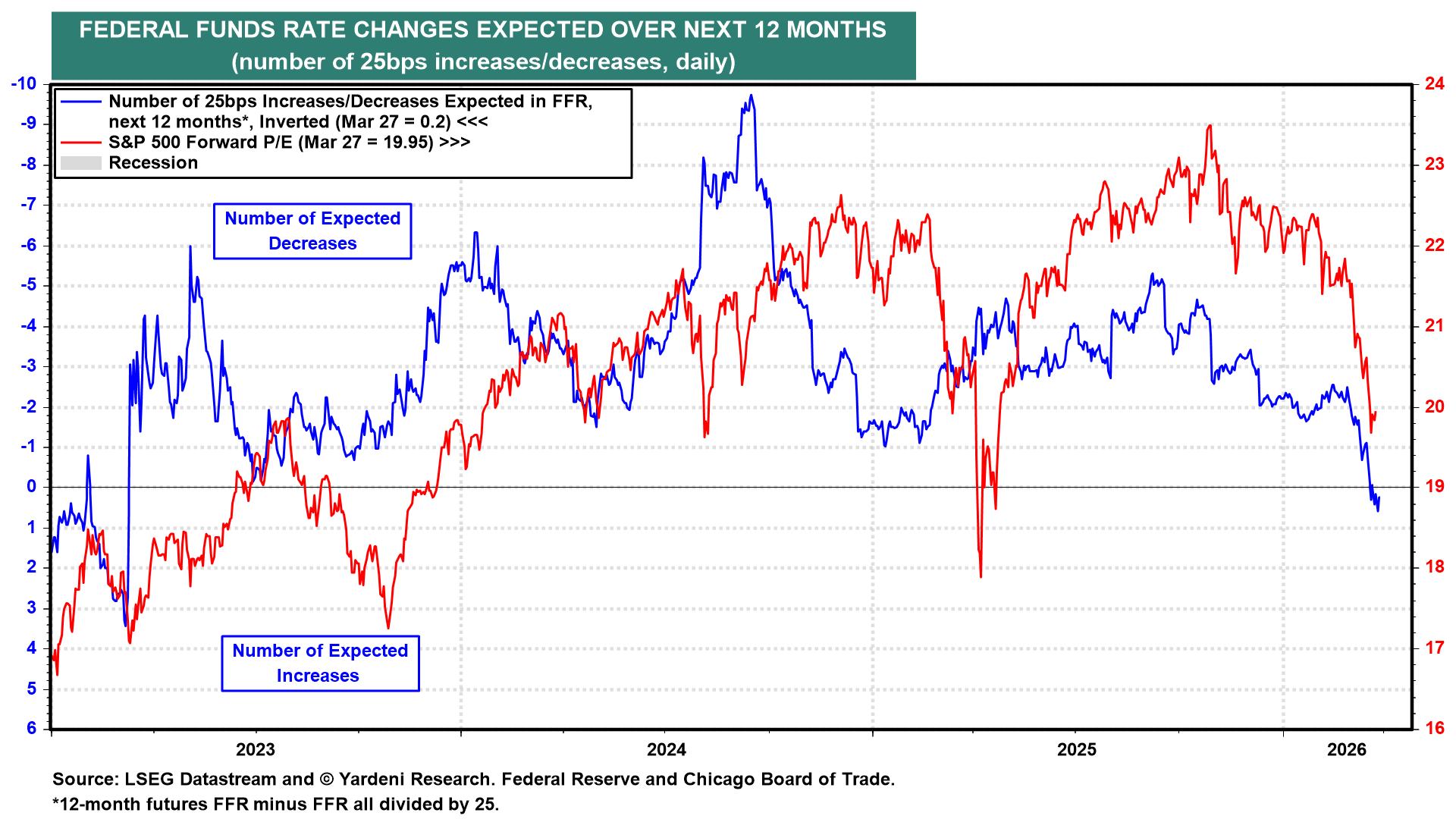

As the conflict drags on and energy prices remain elevated, rate hikes increasingly are being priced back into the outlook, further weighing on equity valuation multiples (chart).

Here are the key US economic releases most likely to shape investors' thinking on the labor market, growth outlook, and monetary policy path this week:

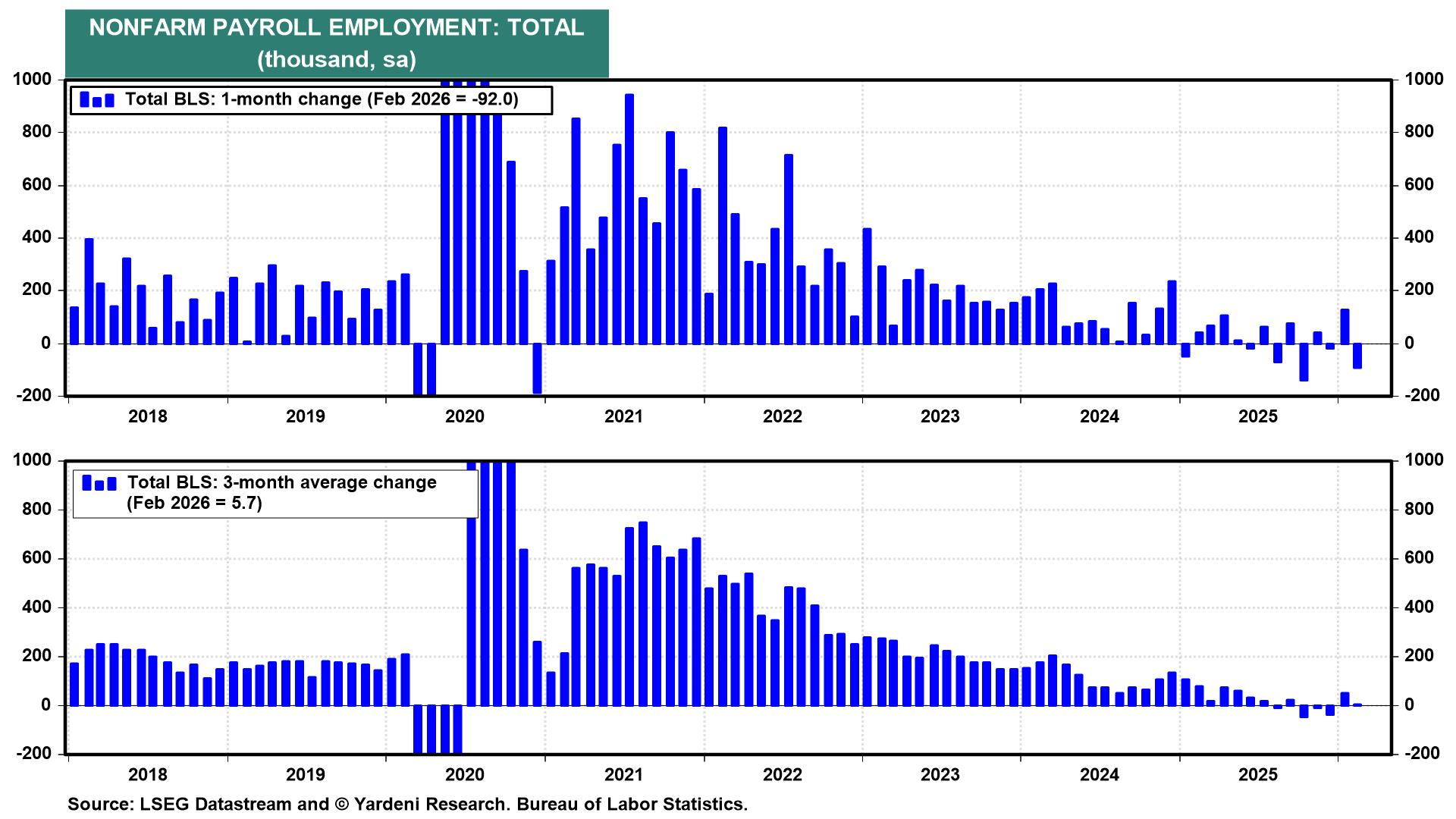

(1) Employment. The March payrolls report (Fri) will take on added significance following February’s unexpected decline of 92,000 and the rise in the unemployment rate to 4.4%. The median Bloomberg estimate is for a 60,000 increase, with no forecasters expecting outright job losses, suggesting that the labor market remains resilient despite a less certain macro backdrop. We’ll also get additional signals from ADP (Wed), Challenger (Thu), and weekly jobless claims (Thu), which should help clarify whether February’s weakness was a one-off or the start of a broader slowdown.

Payroll growth has already shown signs of losing momentum, with monthly gains becoming more uneven and the three-month average trending lower (chart).

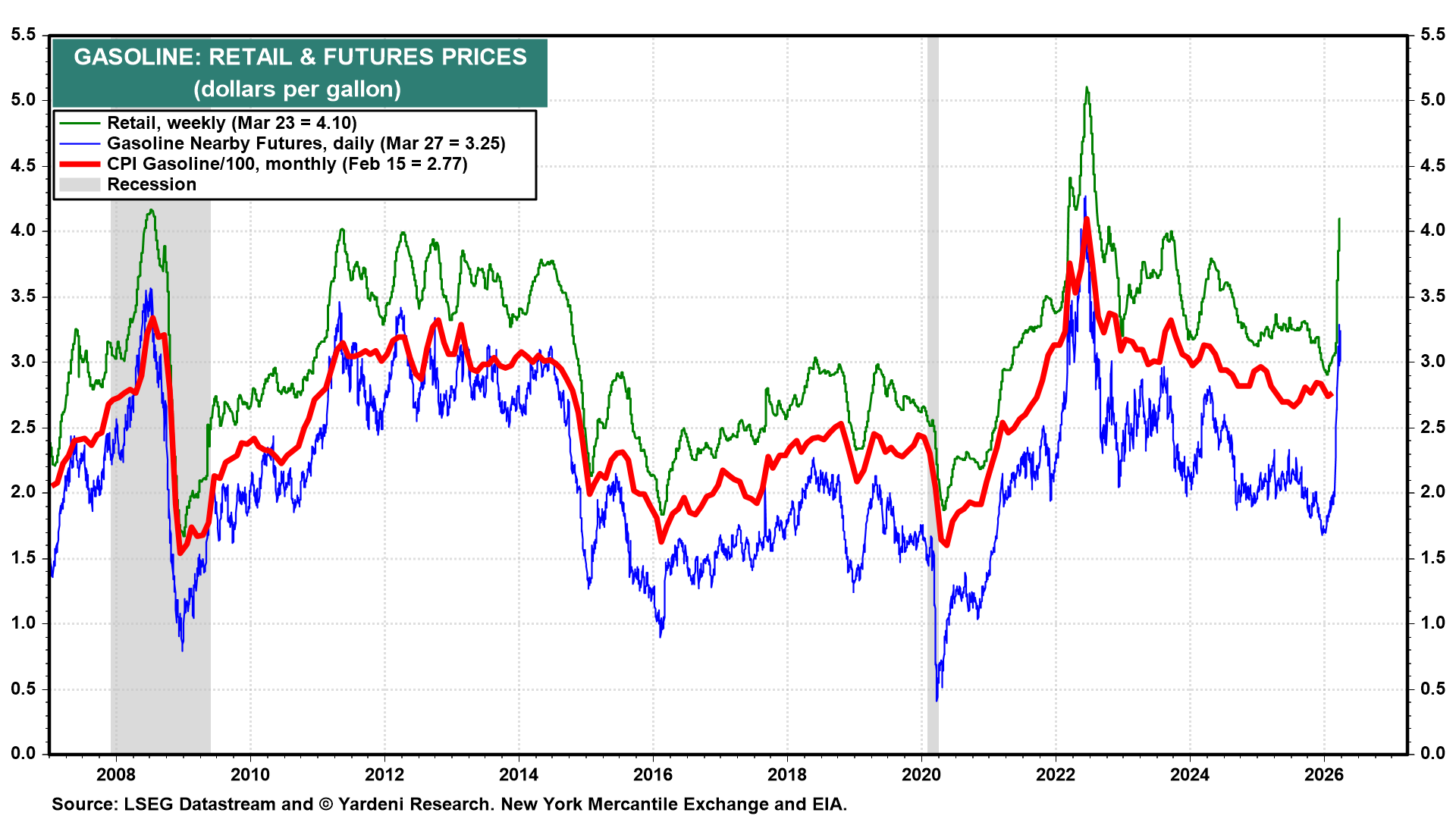

(2) Consumer confidence. Consumer confidence will be closely watched this week as one of the first quantifiable readings on how the surge in energy prices is affecting households. National average gasoline prices have jumped from $2.98 on February 26 to $4.10 per gallon on March 23, a roughly 38% increase that is likely to weigh on consumer perceptions (chart).

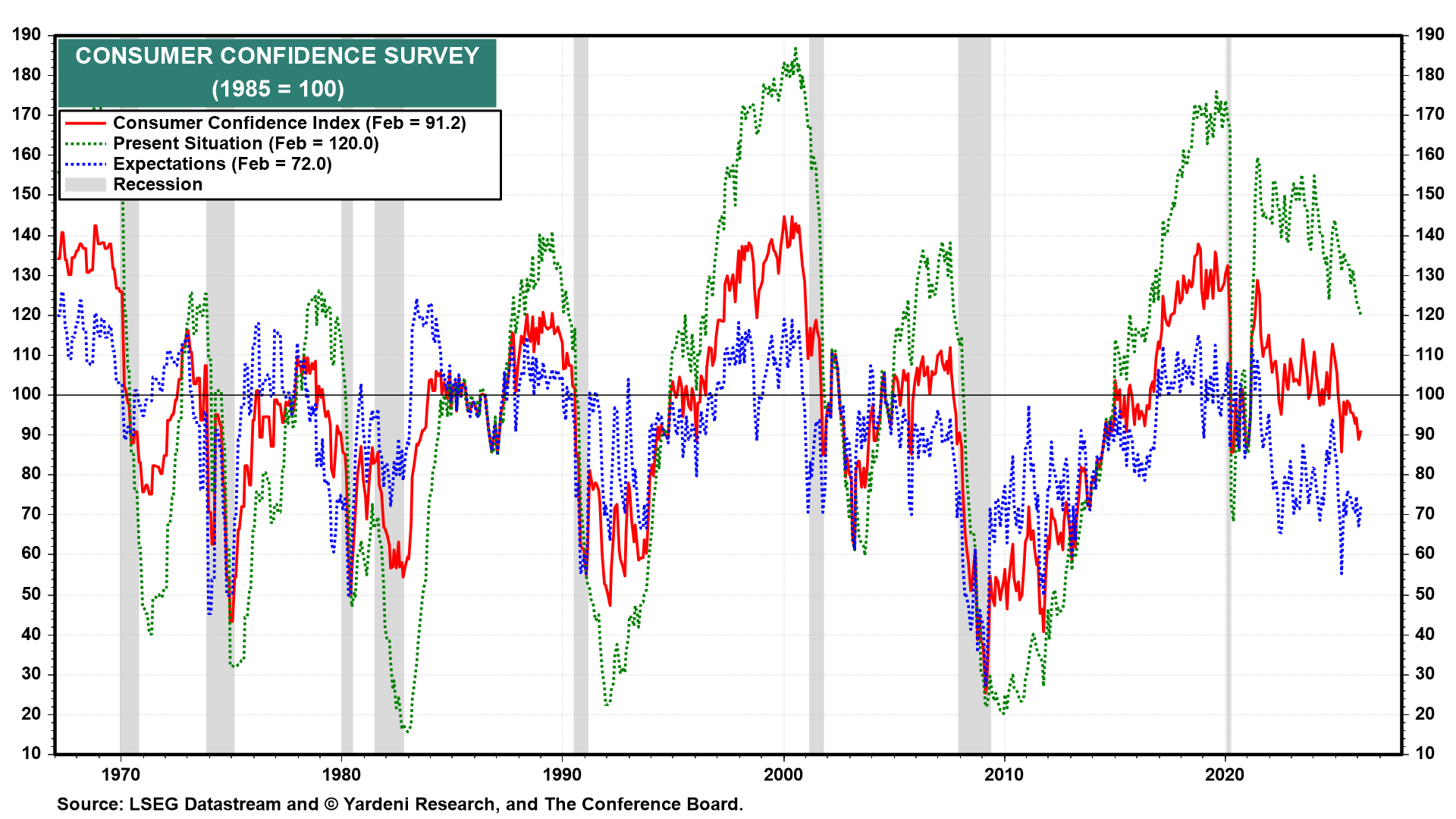

Since July, headline confidence has been trending lower, and expectations have weakened considerably (chart). This should likely continue. We will be particularly focused on expectations given the likelihood that elevated gasoline prices persist in the months ahead.

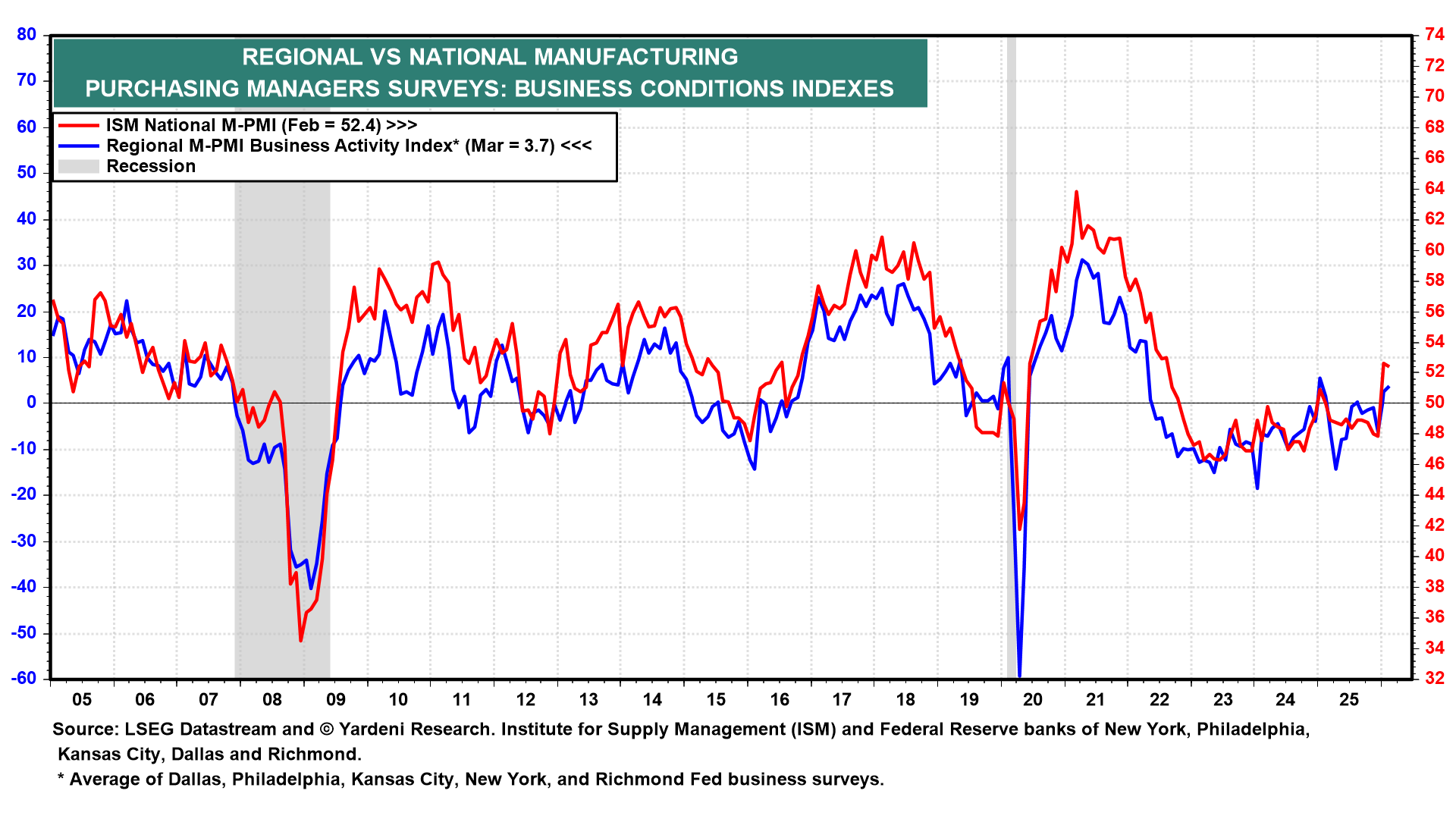

(3) PMIs. Manufacturing data will be in focus this week, with Chicago PMI, final S&P 500 PMIs, and ISM manufacturing due. With uncertainty elevated by rising oil prices and a repricing of the Fed policy path, forward-looking components will be key. March regional surveys have remained soft relative to the still-expansionary ISM, highlighting a divergence between weakening local activity and more resilient national readings (chart). If the ISM begins to converge toward weaker regional readings, it may suggest that manufacturing momentum is losing traction after a period of resilience.