The US financial markets are closed on Monday for Memorial Day, and the holiday-shortened week is light on economic data releases. On Thursday, the second estimate of Q1-2026 GDP will be reported alongside April's core PCED, the Fed's preferred inflation gauge. Eight Fed officials speak over the week. With little fresh data to help investors gauge whether the FOMC is turning more hawkish, they’ll be parsing the speakers’ commentary for signs. The markets now reflect a 62.5% chance of a rate hike this year, arriving in December, up from 50.0% a week ago. We think one could come as early as July.

The wild card is whether President Donald Trump's latest "likely negotiated" peace deal is the real deal. On Saturday, he said that it would reopen the Strait of Hormuz. The deal under discussion includes a memorandum of understanding as a first phase, Iran’s foreign ministry said Saturday, with broader talks to follow within 30 to 60 days. The two sides remain far apart on key issues.

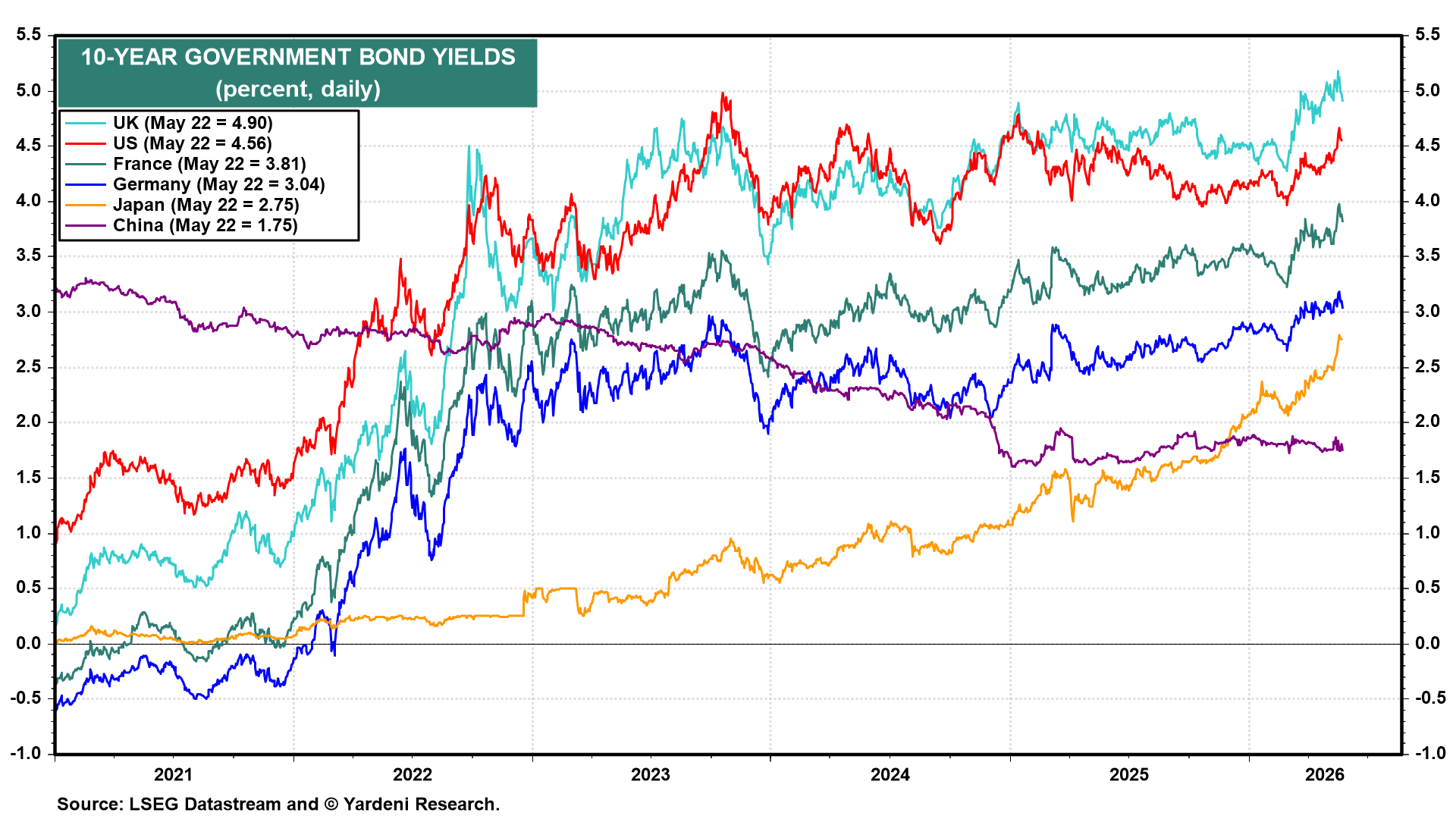

Globally, bond yields backed off this week’s highs but stayed elevated. The 10-year US Treasury yield eased to 4.56% from a 4.69% peak, and the UK 10-year gilt slipped to 4.90% from 5.19% (chart).

Here are the key economic releases most likely to shape investors’ thinking this week:

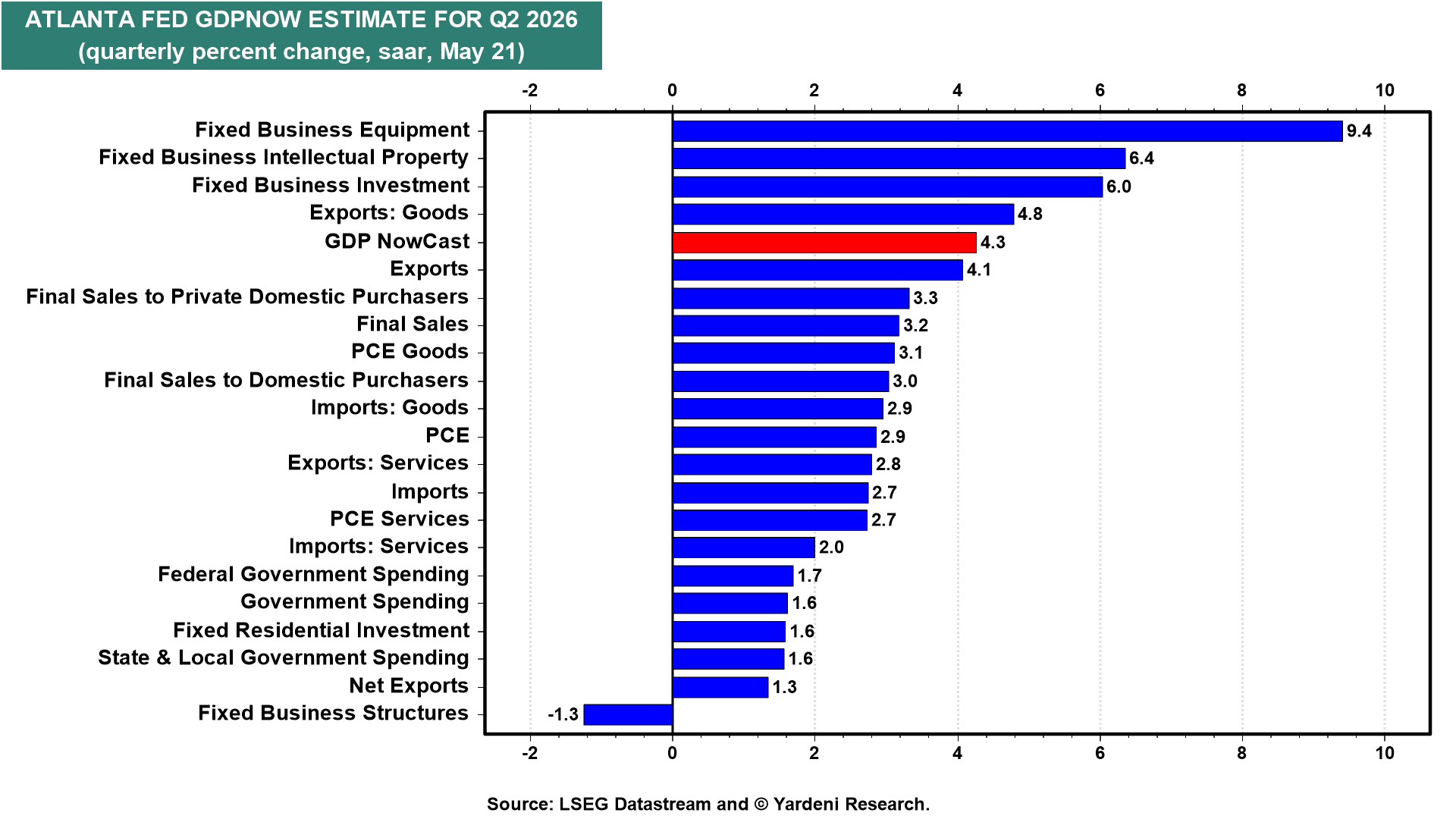

(1) GDP. Thursday's second estimate of Q1-2026 GDP should hold near the 2.0% advance reading. The Atlanta Fed's GDPNow model already has Q2 tracking 4.3%, led by a surge in business equipment spending (chart).

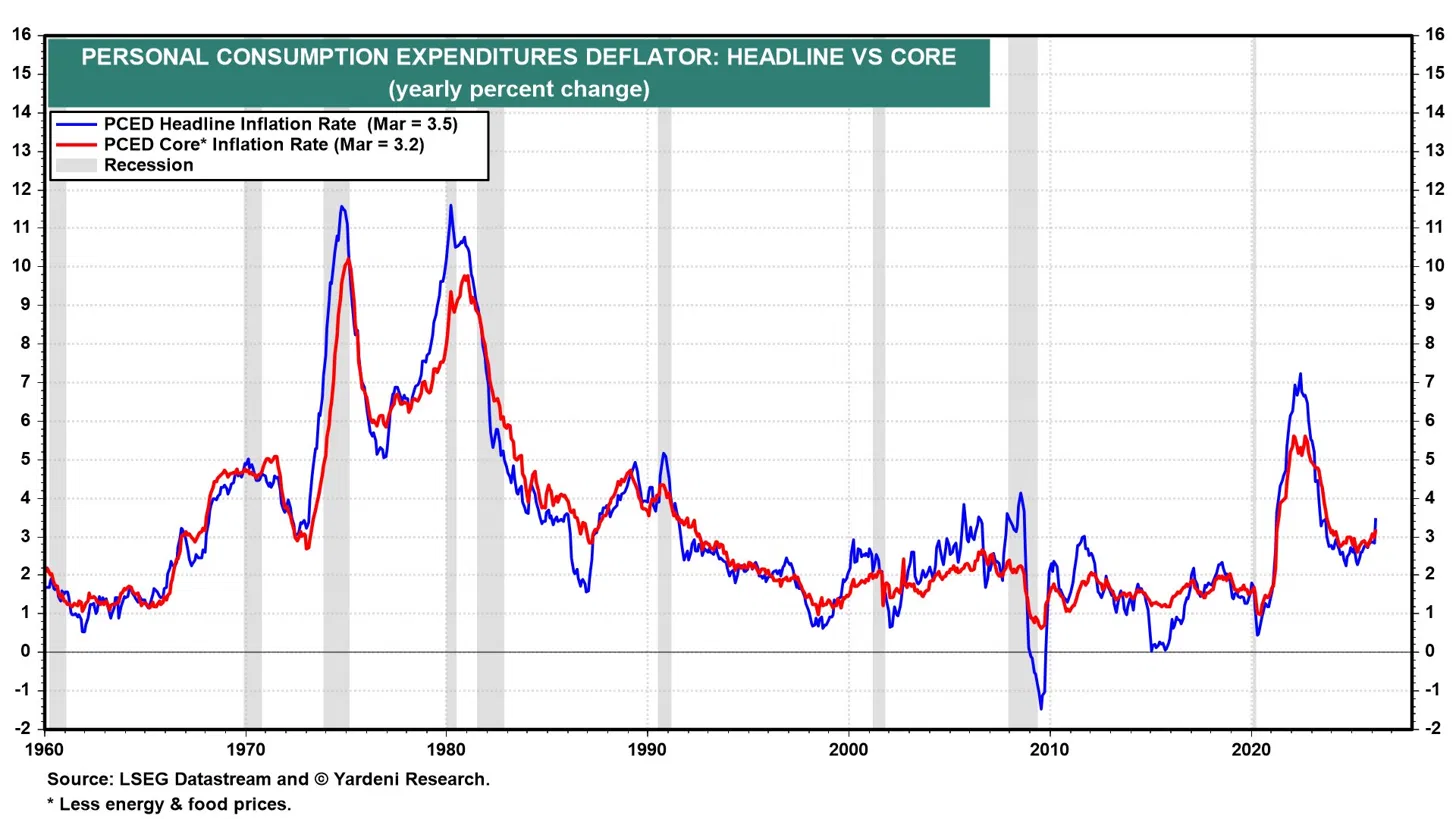

(2) Core PCED. April's core PCED, the Fed's preferred inflation gauge, arrives Thursday. It ran at 3.2% y/y in March, up from 3.0% in February, with headline inflation at 3.5% (chart). Given that the latest CPI and PPI both ran hot, the risk is another upside surprise that further strengthens the case for a Fed rate hike.

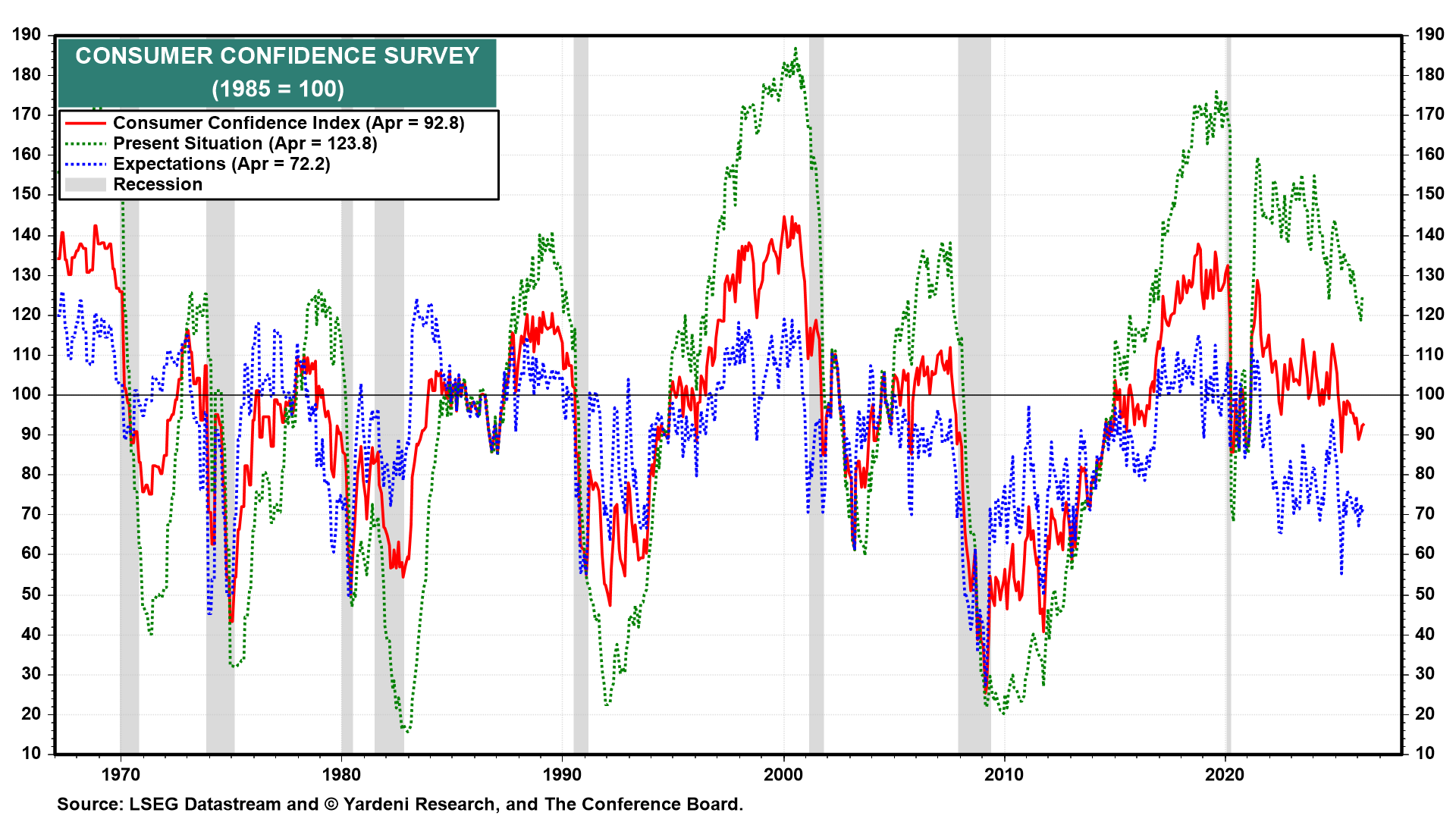

(3) Consumer confidence. May's Consumer Confidence Index survey (Tue) should tick higher from April's 92.8 (chart). We will focus on the labor market indicators, which are likely to show some improvement.

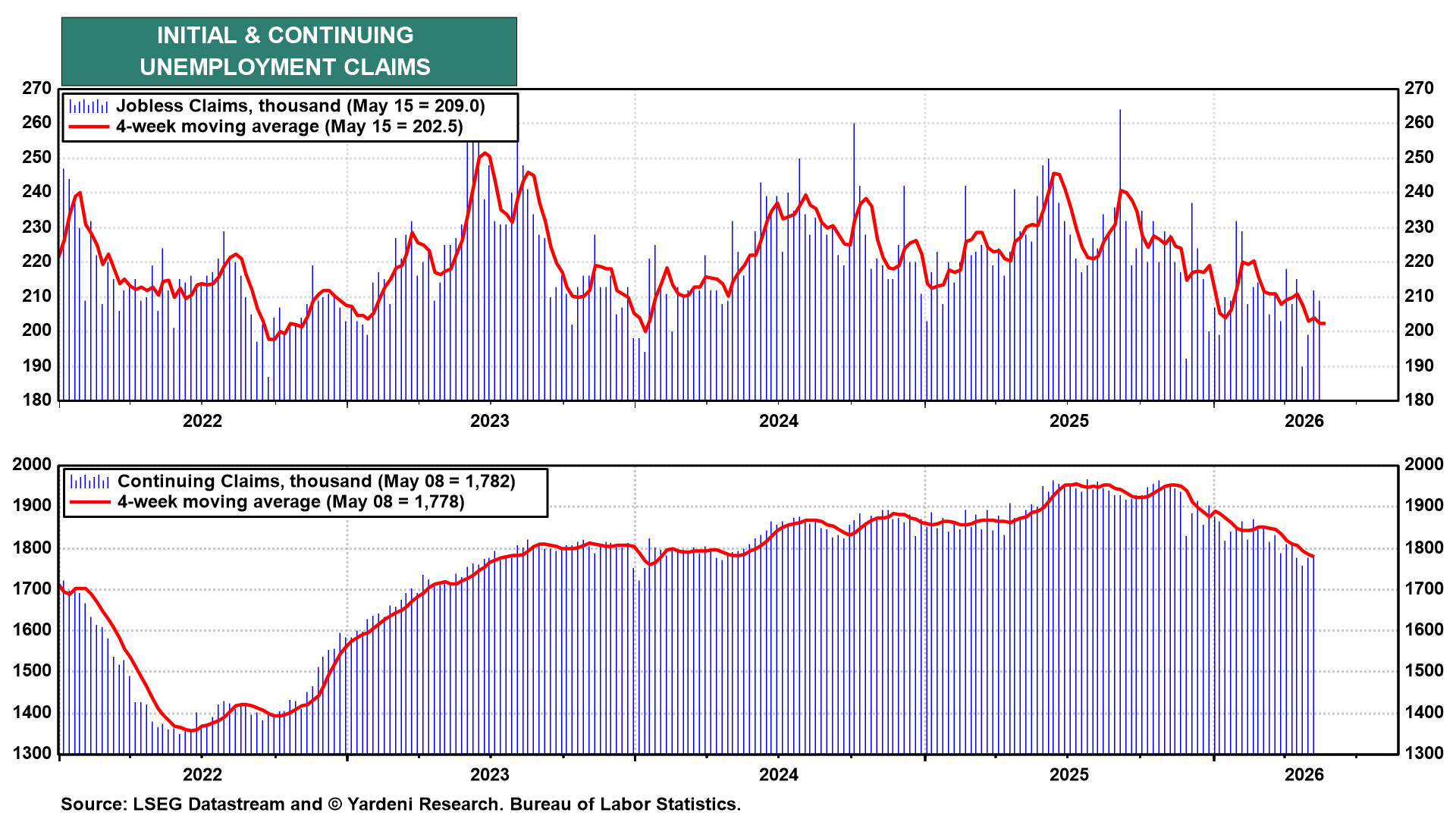

(4) Unemployment. Initial jobless claims (Thu) came in at 209,000, with the four-week moving average at 202,500 (chart). Continuing claims were 1,782,000, with the four-week moving average at 1,778,000. The labor market continues to improve.

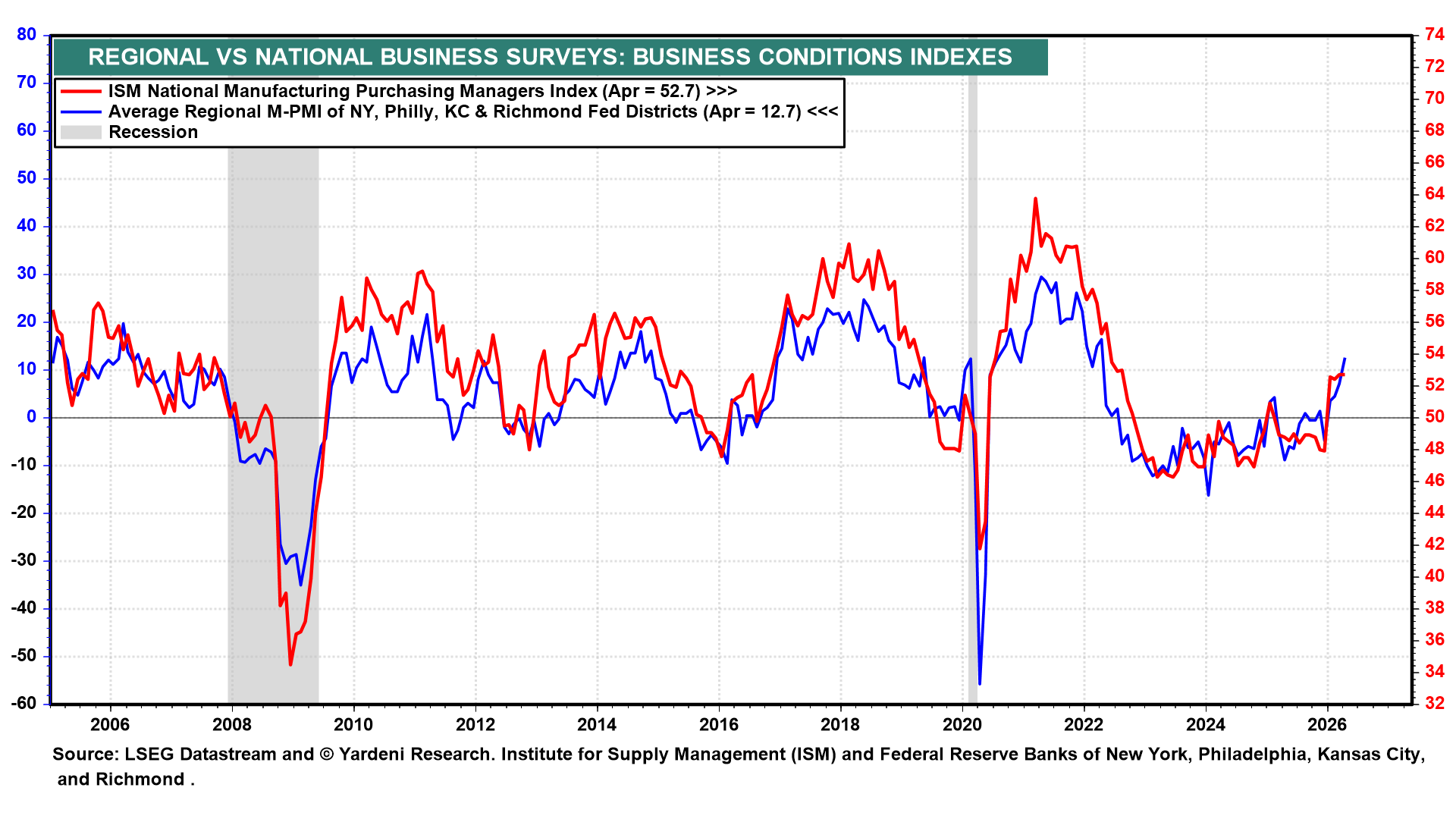

(5) Regional business surveys. The week's regional Fed business surveys include Dallas (Tue) and Richmond (Wed). Both the ISM national M-PMI and the regional average of the five Fed surveys have turned higher in recent months (chart). The recovery in manufacturing is broadening.

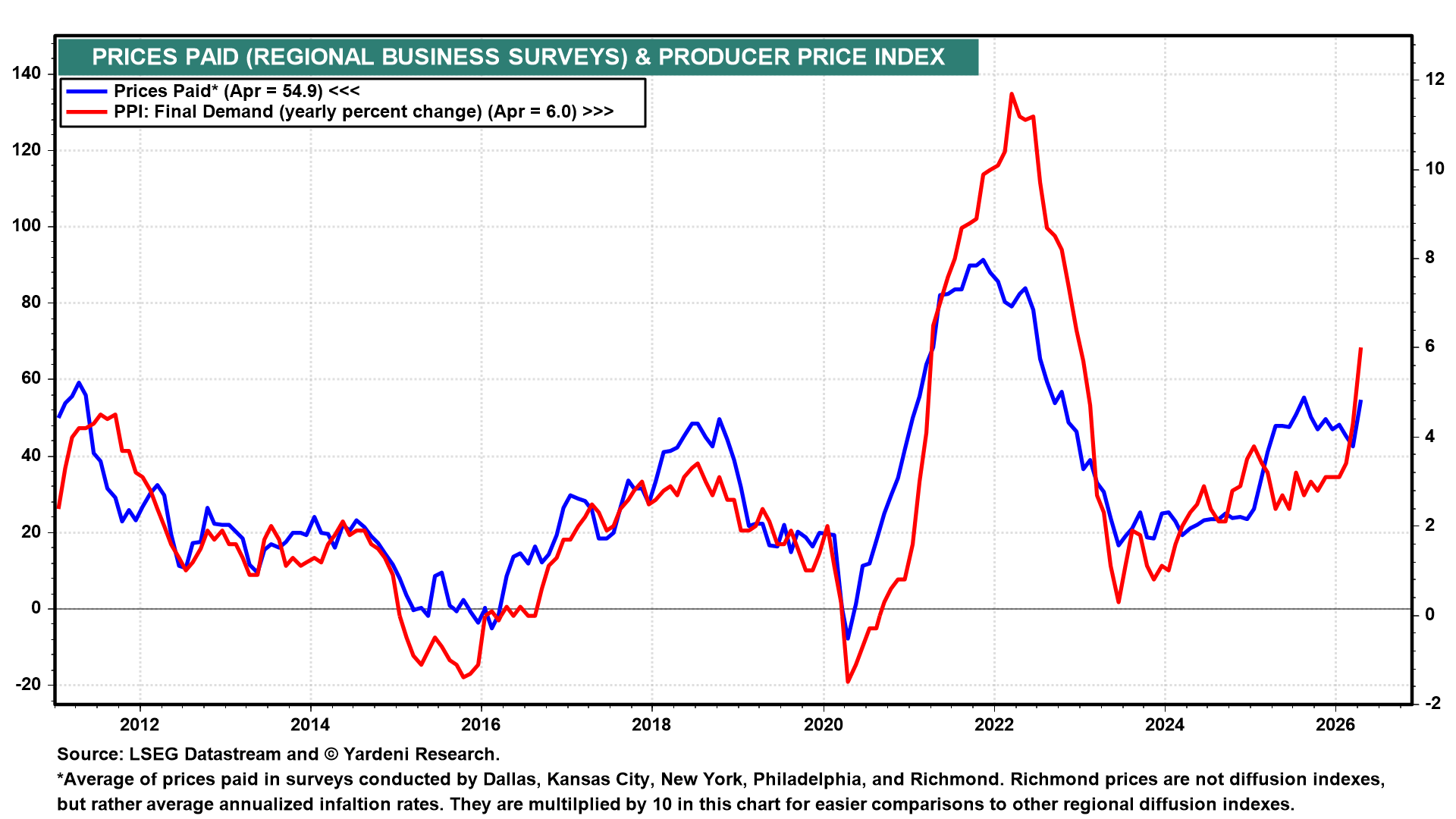

The regional prices-paid average has climbed back to 54.9, and PPI final demand is already running at 6.0% y/y (chart).