The stock market has had an exuberant stretch since the S&P 500 bottomed on March 30. The index is up 17.8% since then through Friday, after hitting a record high on May 14. The DJIA rose to a record high this past Friday. The bears say the exuberance is irrational, driven by lots of excitement about AI. We say it is rational, based on our Buzz Lightyear Theory (BLT) of "To Infinity and Beyond!"

According to our BLT, there’s a fourth factor or production, not just the historically recognized three. In addition to land, labor, and capital, which are relatively scarce, there’s now data, the supply of which is unlimited. The Digital Revolution, which began in the 1960s, is all about processing as much information as possible, as quickly as possible and as cheaply as possible. Today's AI technologies can certainly do all that much better than IBM mainframes back in the mid-1960s.

Instead of focusing on rational versus irrational exuberance, let's compare FOMO to FEMO. The former stands for “Fear Of Missing Out.” Investors pile into stocks, bidding up their price-to-earnings multiples. FEMO is “Fabulous Earnings Momentum.” Analysts raise their earnings estimates because hard data and company guidance give them reason to do so. We would rather see FEMO than FOMO every time.

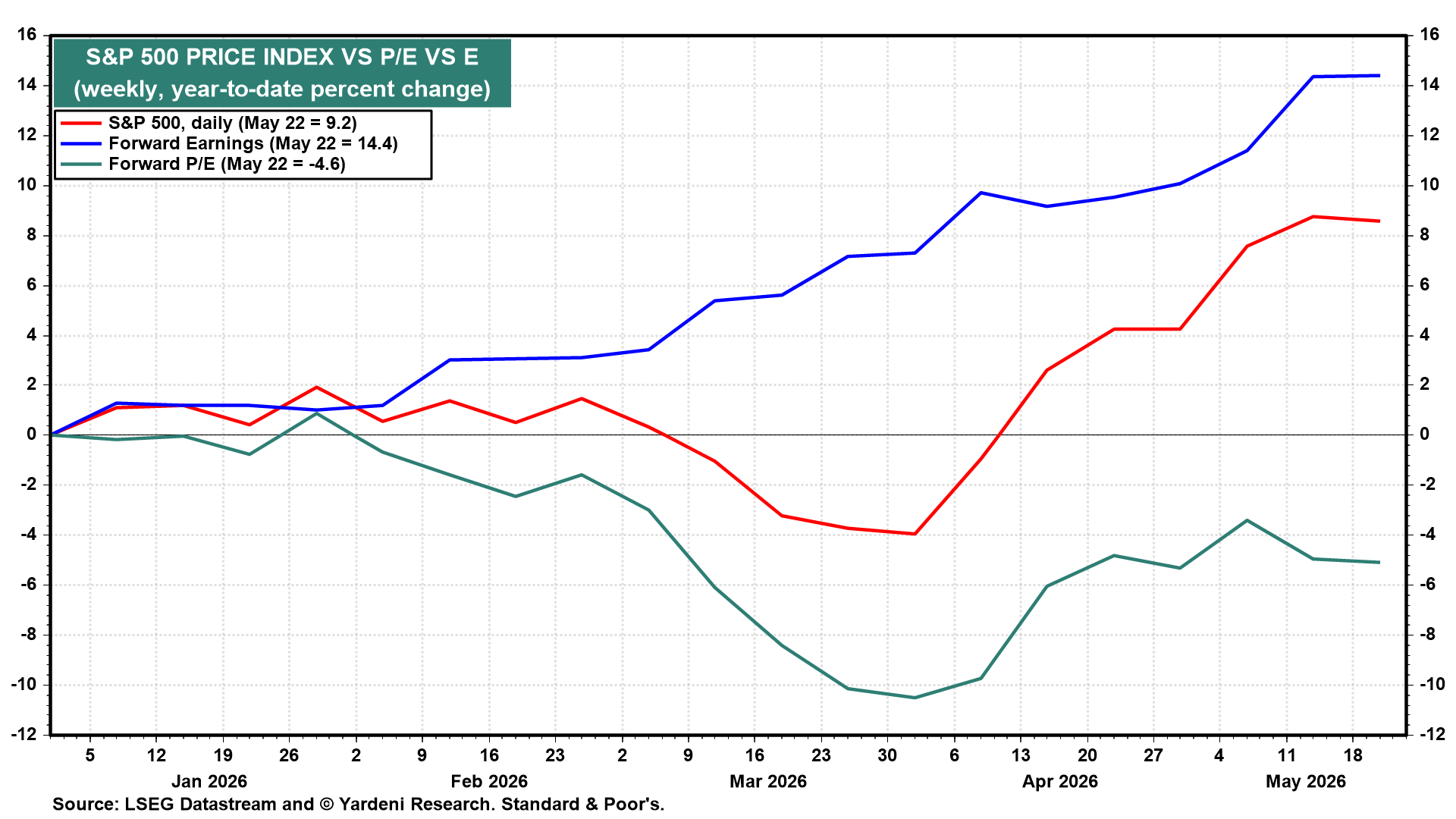

This year has been all about FEMO. Through Friday, the S&P 500 is up 9.2% ytd, forward earnings is up 14.4%, and the forward P/E is down 4.6% (chart). The entire rally has been driven by forward earnings. The multiple has contracted. FOMO inflates the P/E. This market did the opposite. That is why we are not in the bubble camp. FOMO is based on hope and hype. FEMO is based on fundamentals. At 21.1 times forward earnings, the S&P 500 is not irrationally valued unless a recession is coming in the foreseeable future. We don't see one.

Now consider the following: