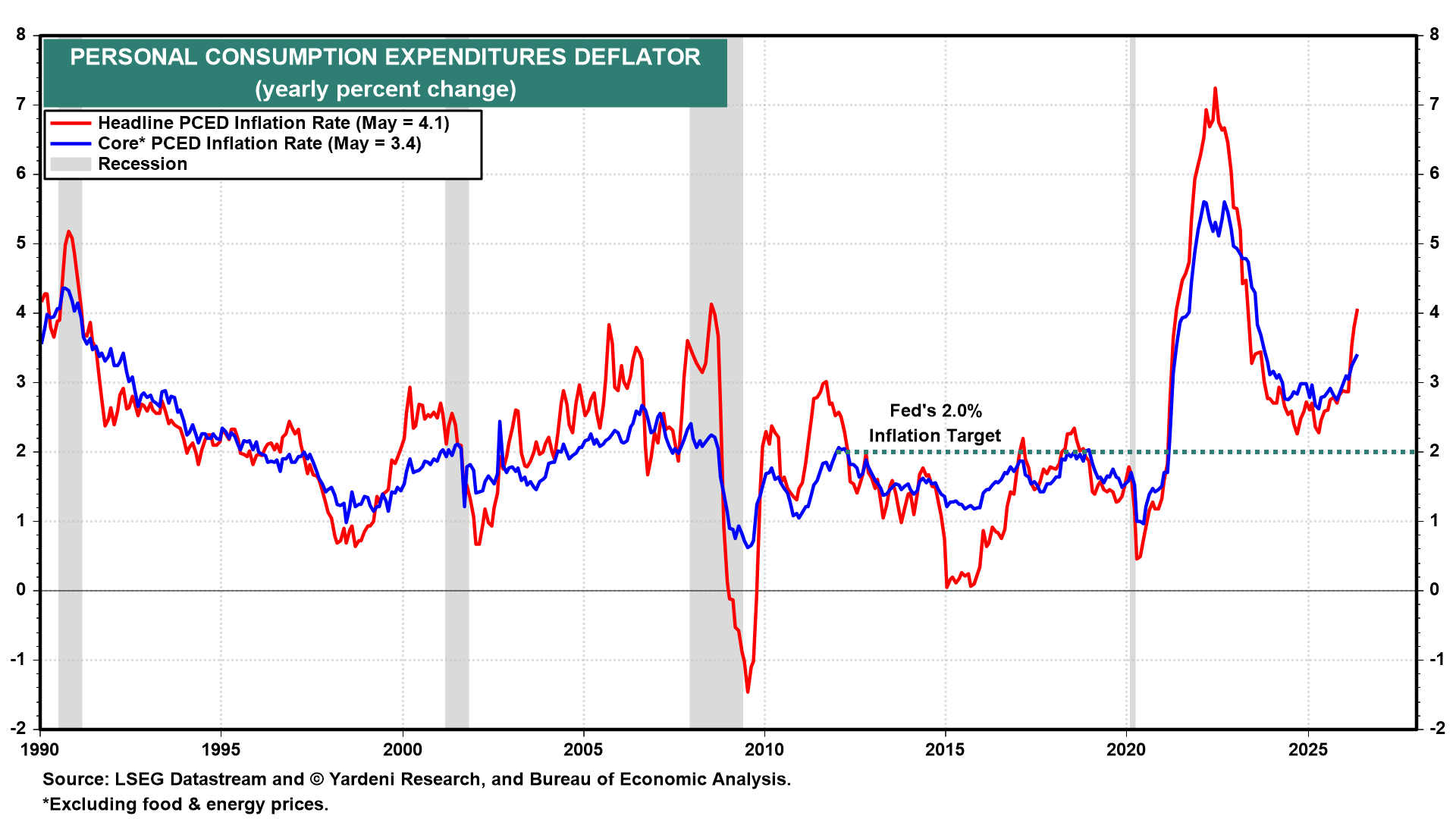

The FOMC’s policy stance is determined by the balance of risks to its dual mandate of price stability and full employment. In the current environment, those risks remain firmly skewed toward inflation, justifying last week's FOMC pivot from an easing bias to a tightening one. Today's plethora of May economic data shows that the economy and the labor market are in great shape, while both headline and core PCED inflation rates rose further above the Fed's 2.0% target (chart) .

June's plunge in oil prices will certainly reduce the headline inflation rate, but the core rate is now up to 3.4% y/y. Before the war, it was stuck just below 3.0%. In his press conference last week, Fed Chair Kevin Warsh acknowledged that inflation has exceeded the FOMC's target for more than five years and committed the Fed to restoring price stability. Accordingly, we remain inclined to expect at least one rate hike before year-end, with July a live possibility.

Falling energy prices may slow core inflation. However, the AI spending boom is driving up electricity bills and consumer electronics prices. Today, Apple announced significant price increases because of soaring memory chip prices.

The Cleveland Fed's Inflation Nowcasting projects that June's headline inflation fell to 3.9%, while the core inflation rate remained stuck at 3.4%.

Let's have a closer look at today's inflation report and economic indicators: