The April FOMC statement contained an easing bias, signaling that the Fed remained likely to cut the federal funds rate (FFR) over the rest of the year. That bias is becoming increasingly difficult to defend. Three voting members on the FOMC (Hammack, Kashkari, and Logan) already dissented against retaining it at the April meeting of the monetary policy committee. Boston Fed President Susan Collins has since added her voice to those calling for its removal.

The consensus on Wall Street has coalesced around June 16-17 as the next FOMC meeting at which the easing bias will be dropped. The question is whether the easing bias will be replaced with a tightening bias.

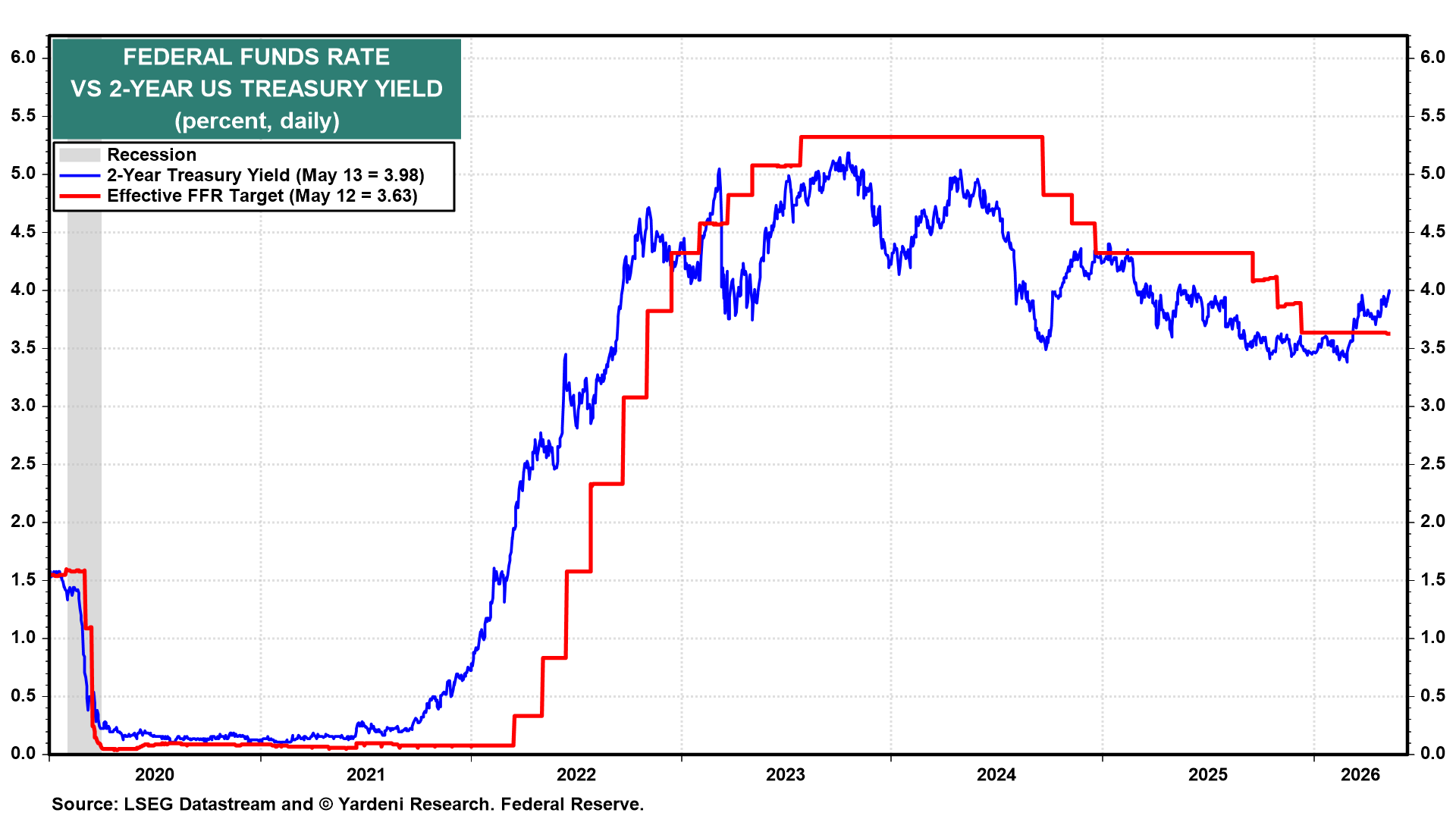

The US Treasury market is pushing for that outcome. The 2-year Treasury yield is currently trading above the effective federal funds rate (chart). When 2-year yields trade significantly above the policy rate, the market is signaling that the current FFR is too low to curb inflation and may have to be hiked–and certainly not cut.

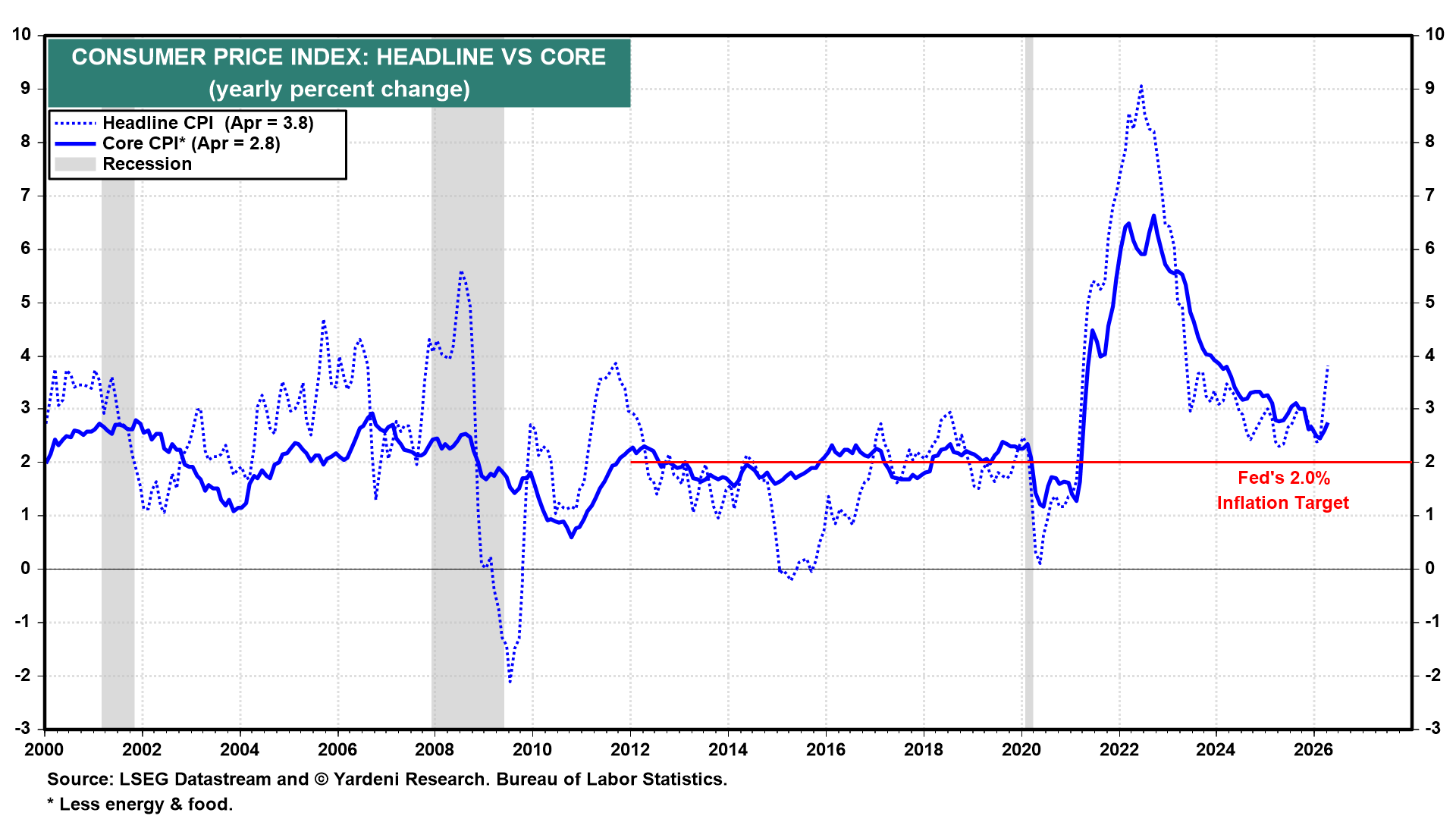

A simple removal of the easing bias may not be enough. After five consecutive years of above-target inflation, the Fed may need to signal a willingness to hike (chart).

The data support such a pivot. Consider the following: