Since ChatGPT was introduced in late November 2022, the AI trade has been mostly focused on the Magnificent-7, especially the big cloud companies, i.e., the "hyperscalers” (chart). For a while, they were all viewed as AI dominators until DeepSeek was released by a Chinese software company in late January 2025. Increasing confidence that US Large Language Models (LLMs) would remain competitive revived the Mag-7's stock market performance during the spring and summer of 2025.

Then, late last year, a growing concern that the AI boom was turning into an AI capital spending arms race among the Mag-7 was heightened by Michael Burry’s warnings that the hyperscalers' massive AI capex might prove unprofitable for various reasons. But those concerns have diminished in response to significant beats by the hyperscalers during the Q1 earnings season in April. Their cloud earnings continue to soar, confirming that rapidly growing demand for "compute" might justify all the AI capital spending after all.

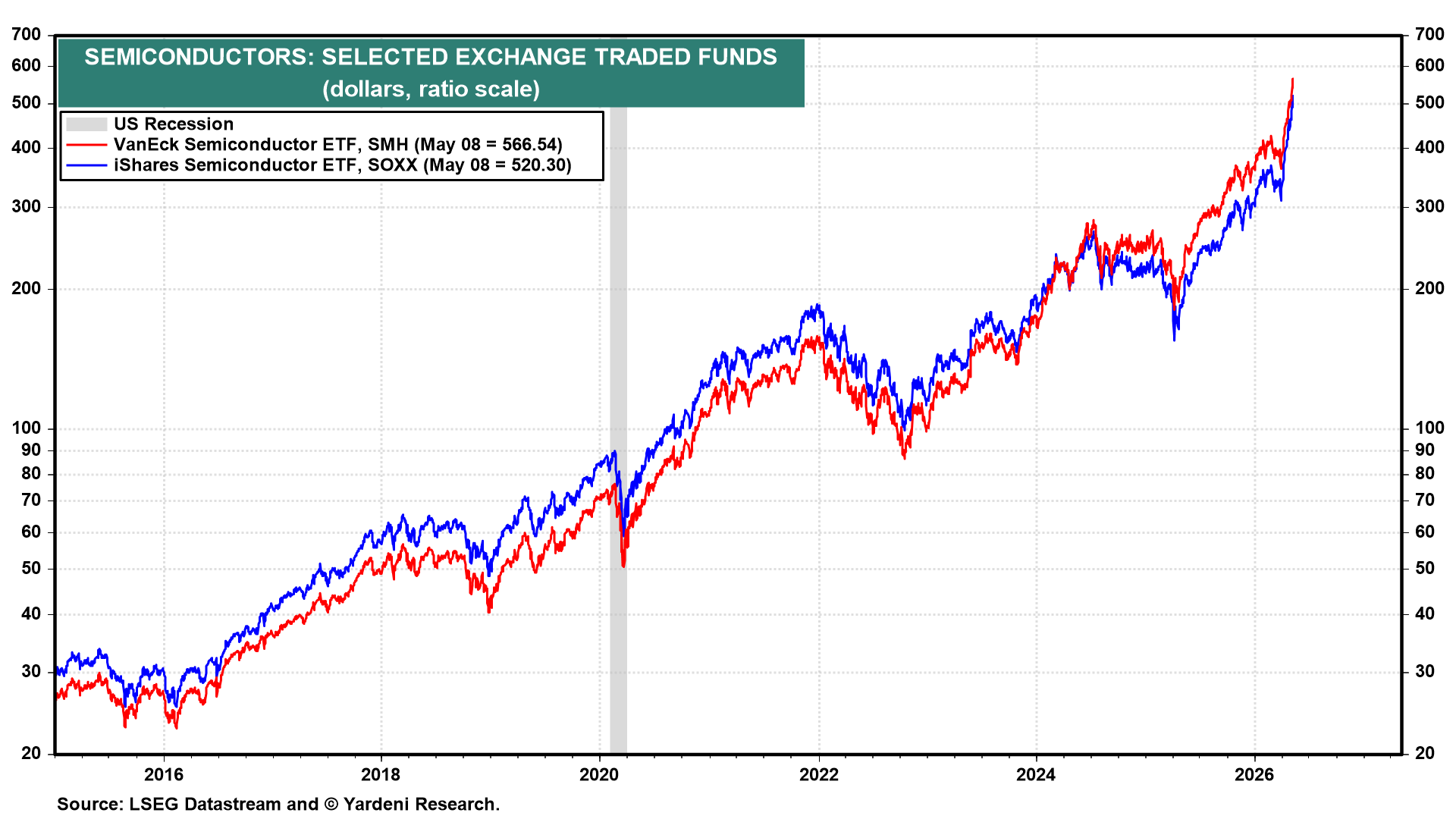

Since late last year, investors have come to realize that while there may be uncertainty about the profitability of hyperscalers’ AI capex, there is no doubt that their massive capex will boost demand for semiconductors and related AI components. As a result, the prices of ETFs investing in semiconductors soared to new record highs in April (chart).

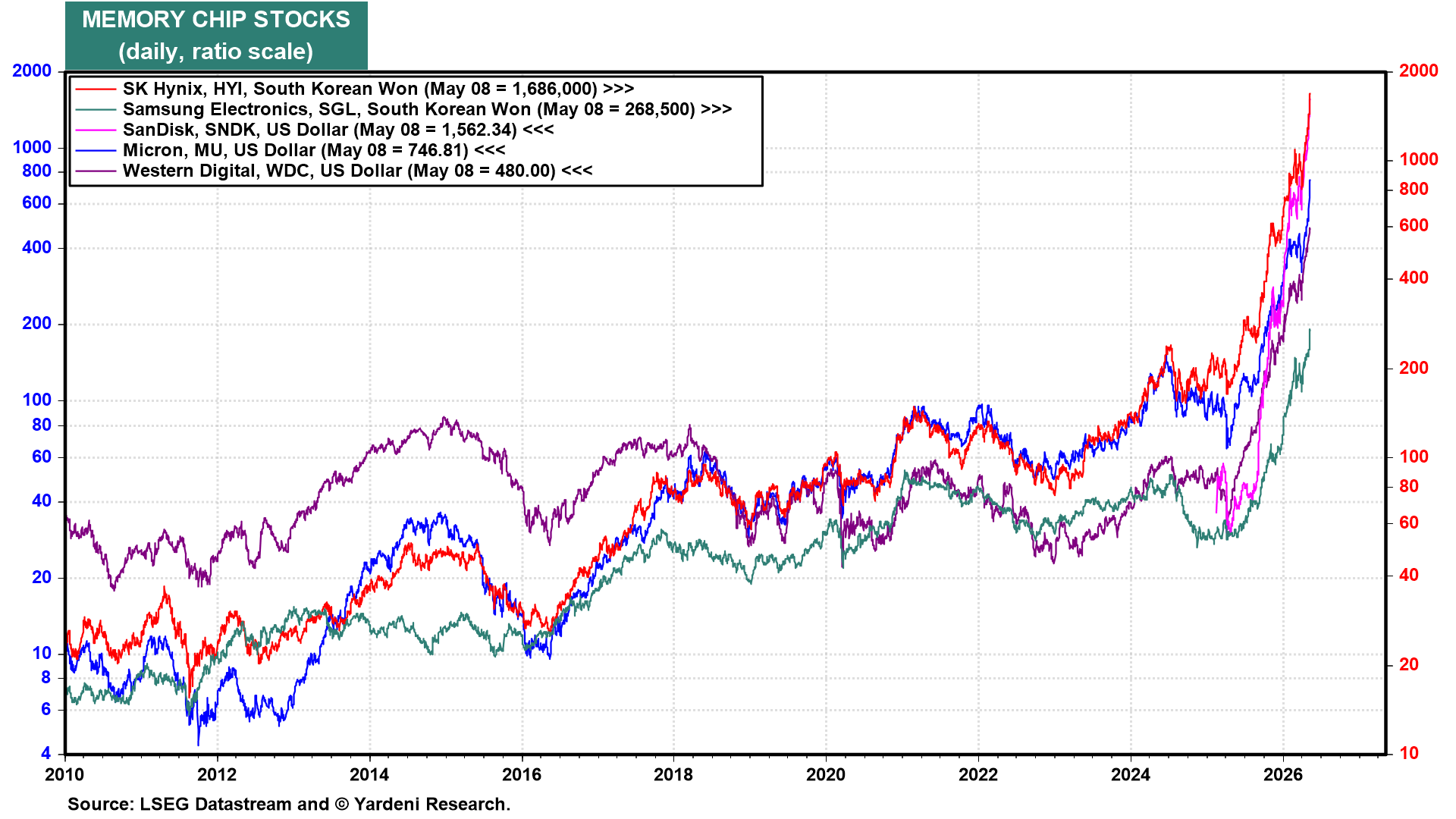

Leading the way higher have been the memory chip companies in the US and South Korea. We wrote about them with a positive tilt in our March 24 QuickTakes titled, "Thanks for the Memory." Their stock prices have continued to rise since. SK Hynix, Samsung, SanDisk, Micron, and Western Digital have all moved sharply higher (chart). As long as AI compute continues to outpace supply, we expect these names to remain strong.

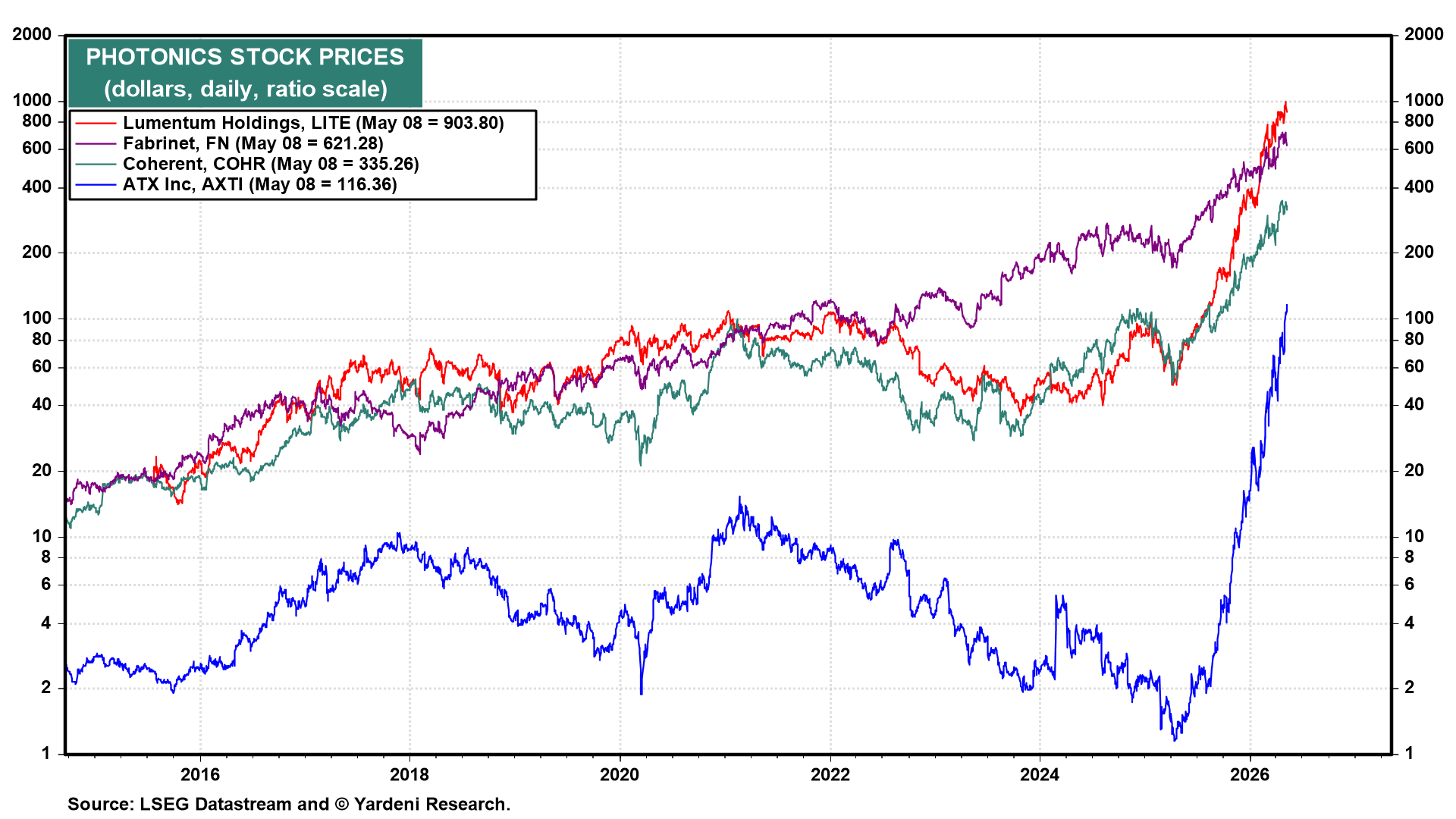

We also wrote about the photonics companies. Their stock prices have also continued to soar (chart).

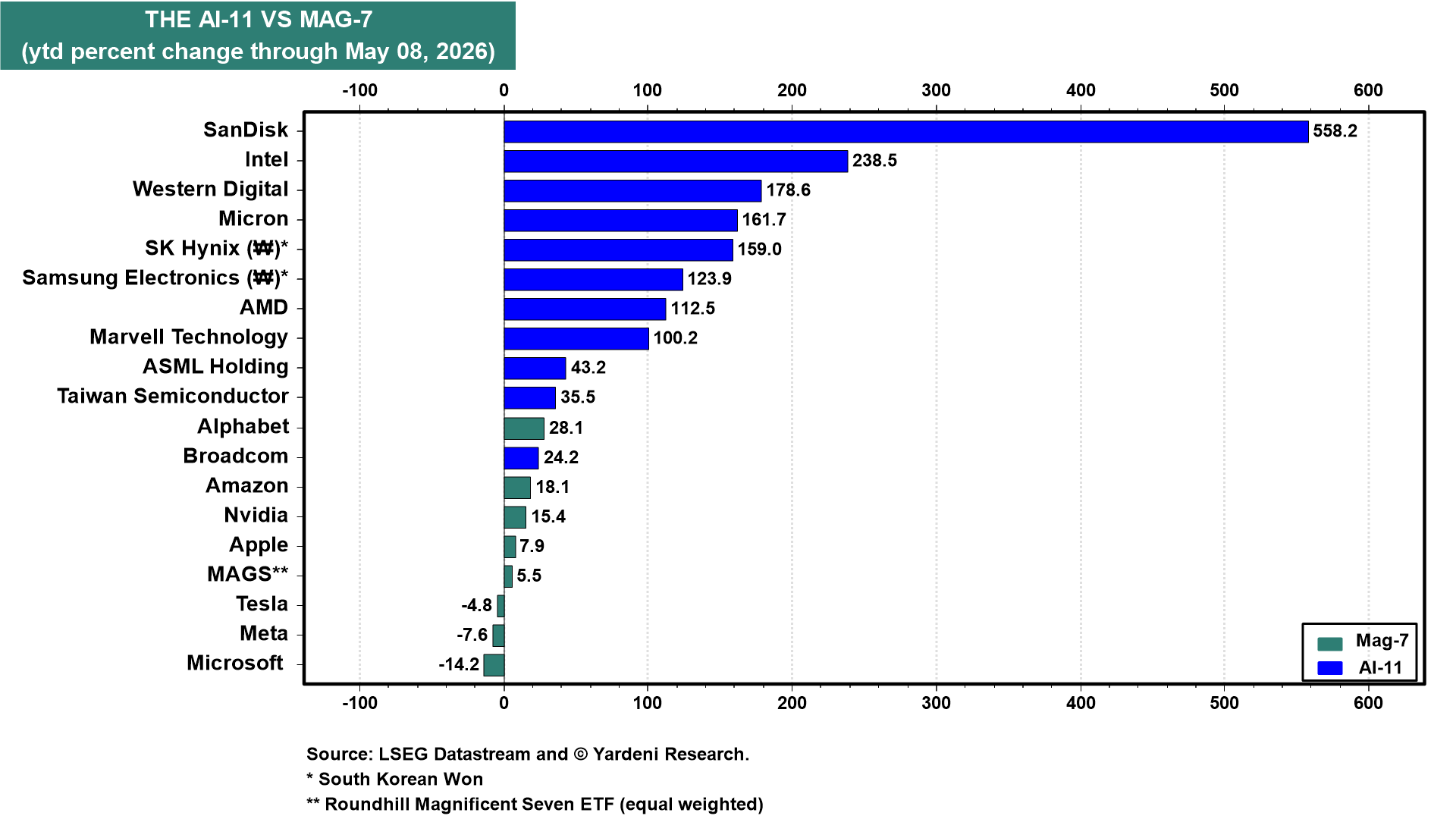

Investors have clearly concluded that the Mag-7 isn't the only AI trade in town. Indeed, so far this year, almost every major semiconductor stock price (in the "AI-11") has beaten all the Mag-7 names, except Broadcom (chart).

Here is a quick review of how the AI-11 fits into the AI supply chain:

(1) Foundry and lithography (TSMC, ASML). TSMC fabricates the leading-edge logic for everyone. ASML owns the EUV lithography chokepoint.

(2) Logic and custom silicon (AMD, Broadcom, Intel). AMD is taking a significant share in AI inference. Broadcom is the custom ASIC partner for hyperscalers and the incumbent in networking silicon. Marvell rounds out its custom silicon, networking, and optical connectivity offerings. Intel is the foundry comeback story with CPU exposure to the AI server cycle.

(3) Memory (Micron, SK Hynix, Samsung). Micron, SK Hynix, and Samsung supply the high-bandwidth memory that is the actual bottleneck for AI training. SK Hynix leads the HBM market globally.

(4) Enterprise NAND and storage. SanDisk has emerged as the pure-play beneficiary of NAND and enterprise SSDs. Western Digital provides the HDD complement.

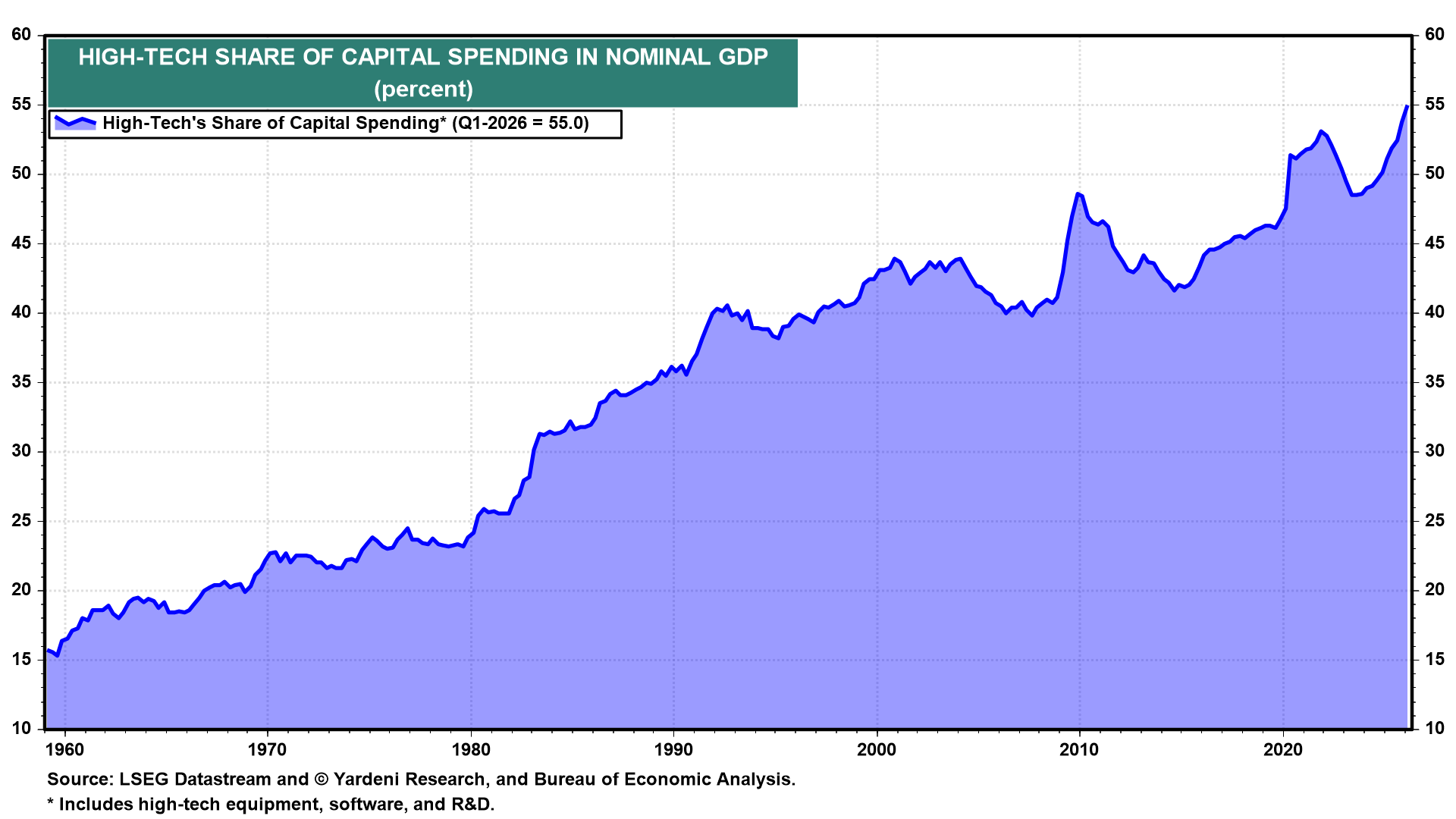

Every dollar of hyperscaler capex for AI infrastructure flows through this supply chain before reaching a server rack. No wonder that high-tech now accounts for a record 55% of US capital spending (chart).

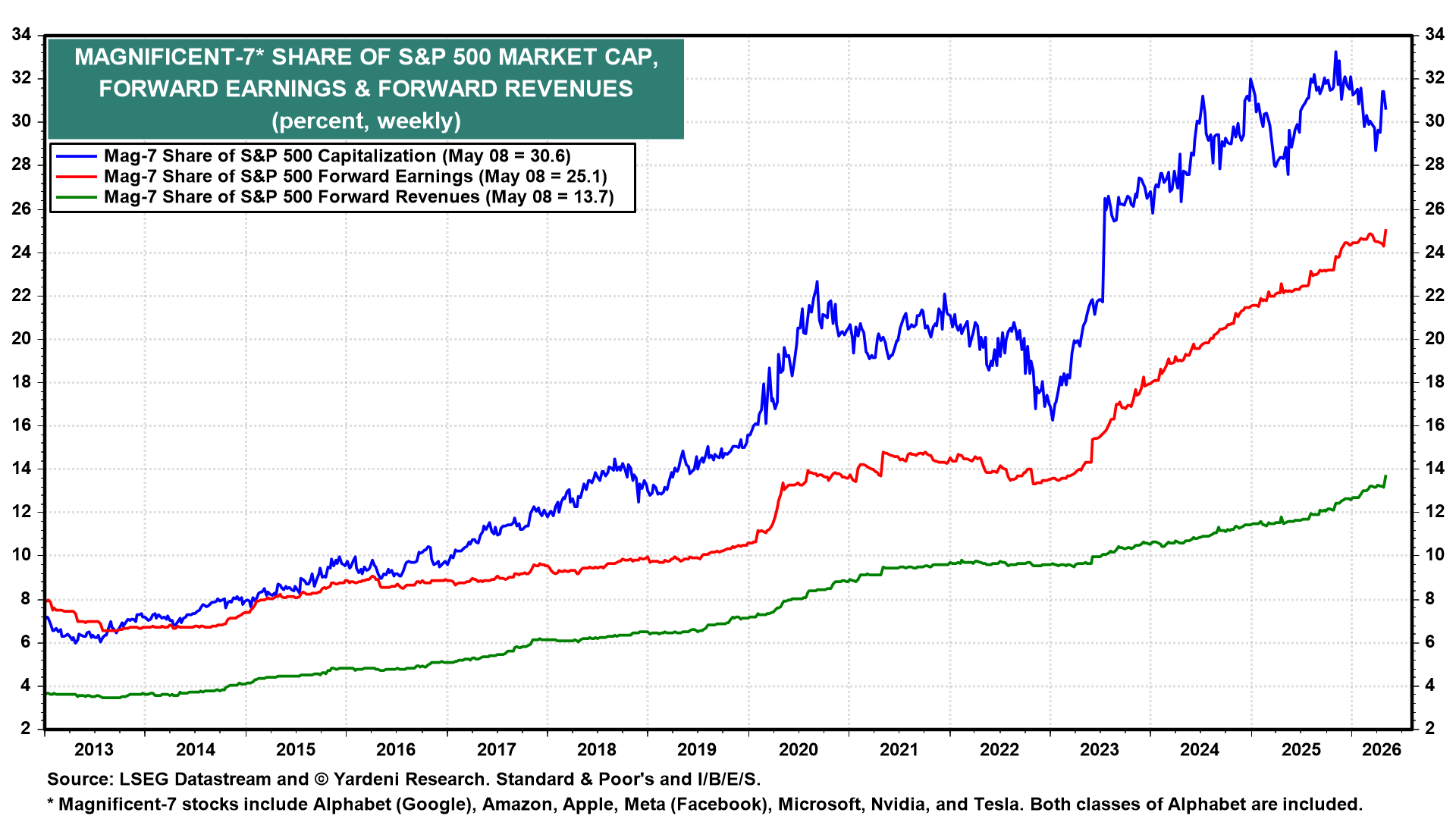

The Mag-7 still dominates the S&P 500 by every concentration metric, accounting for 30.6% of S&P 500 market capitalization, 25.1% of forward earnings, and 13.7% of forward revenues (chart). But the label may be outliving its cachet as discussed above.

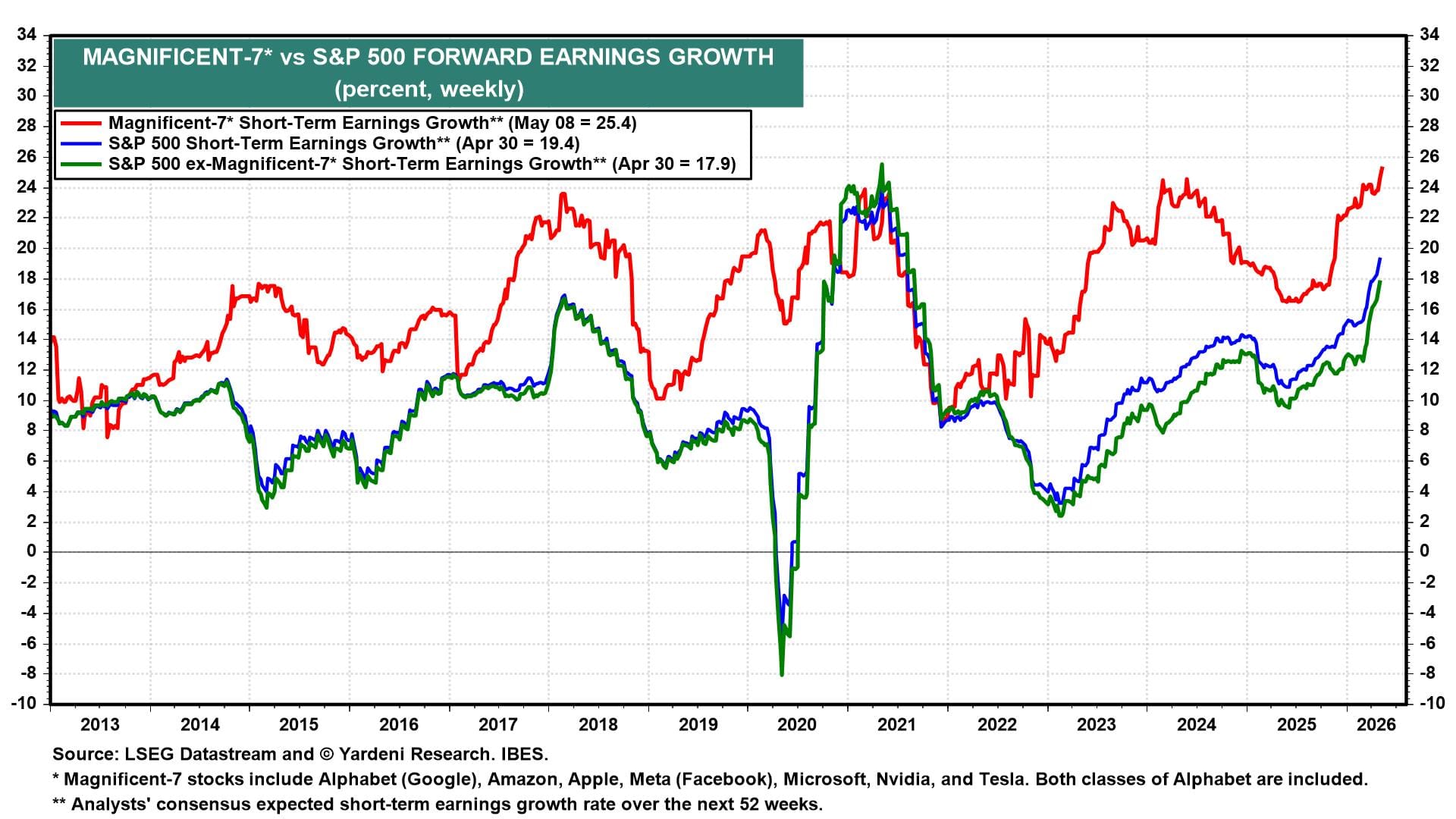

Mag-7 forward earnings growth is currently 25.4% versus 17.9% for the S&P 500 excluding Mag-7 (chart). That spread was wider a year ago. The S&P 493 is catching up in this growth derby. The premium the Mag-7 enjoyed on the basis of earnings growth scarcity is becoming less distinctive as growth broadens. The Mag-7 dominance is priced in. The marginal dollar of investor attention has moved on to what extends the AI trade beyond the original seven.