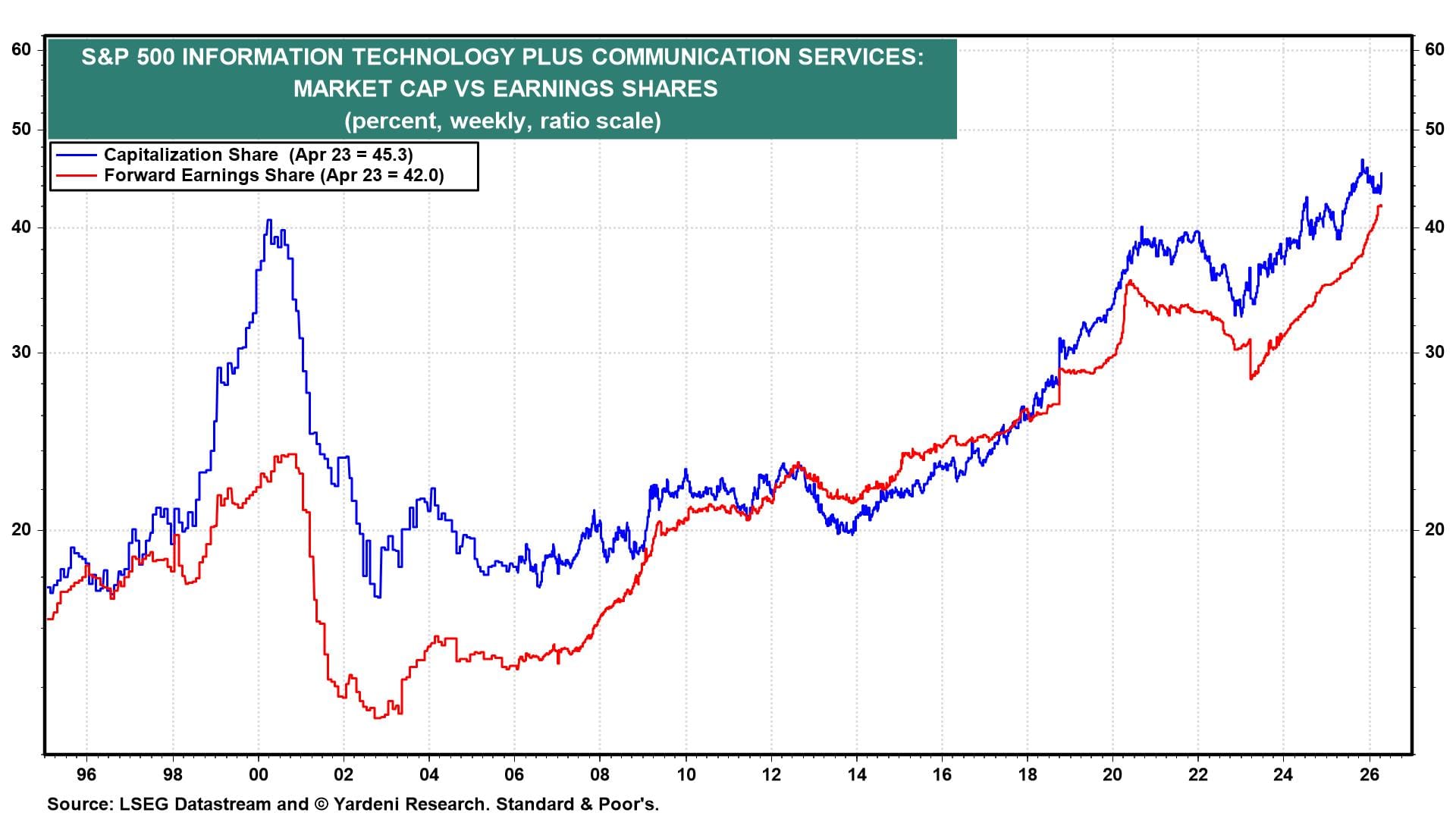

We lowered the S&P 500 Information Technology and Communication Services sectors from overweight to market weight on December 7, 2025. We did so because the two sectors together accounted for 45% of the S&P 500's market capitalization (chart). We were also concerned about the mounting uncertainties regarding the rate of return on hyperscalers' massive AI investments.

Since then, investors have concluded that the hyperscalers are also profitable semiconductor companies. Amazon, Google, and Tesla have been moving in that direction for a while. AI uncertainties have been repressed by the two sectors' record-setting forward earnings, which together account for a record 42% share of S&P 500 forward earnings.

In any event, we are sticking with our advice to market-weight the two sectors simply because we still believe in diversification across sectors. It's much easier to overweight Energy (as we recommended on April 20), which accounts for only 3.3% of the S&P 500's market cap.

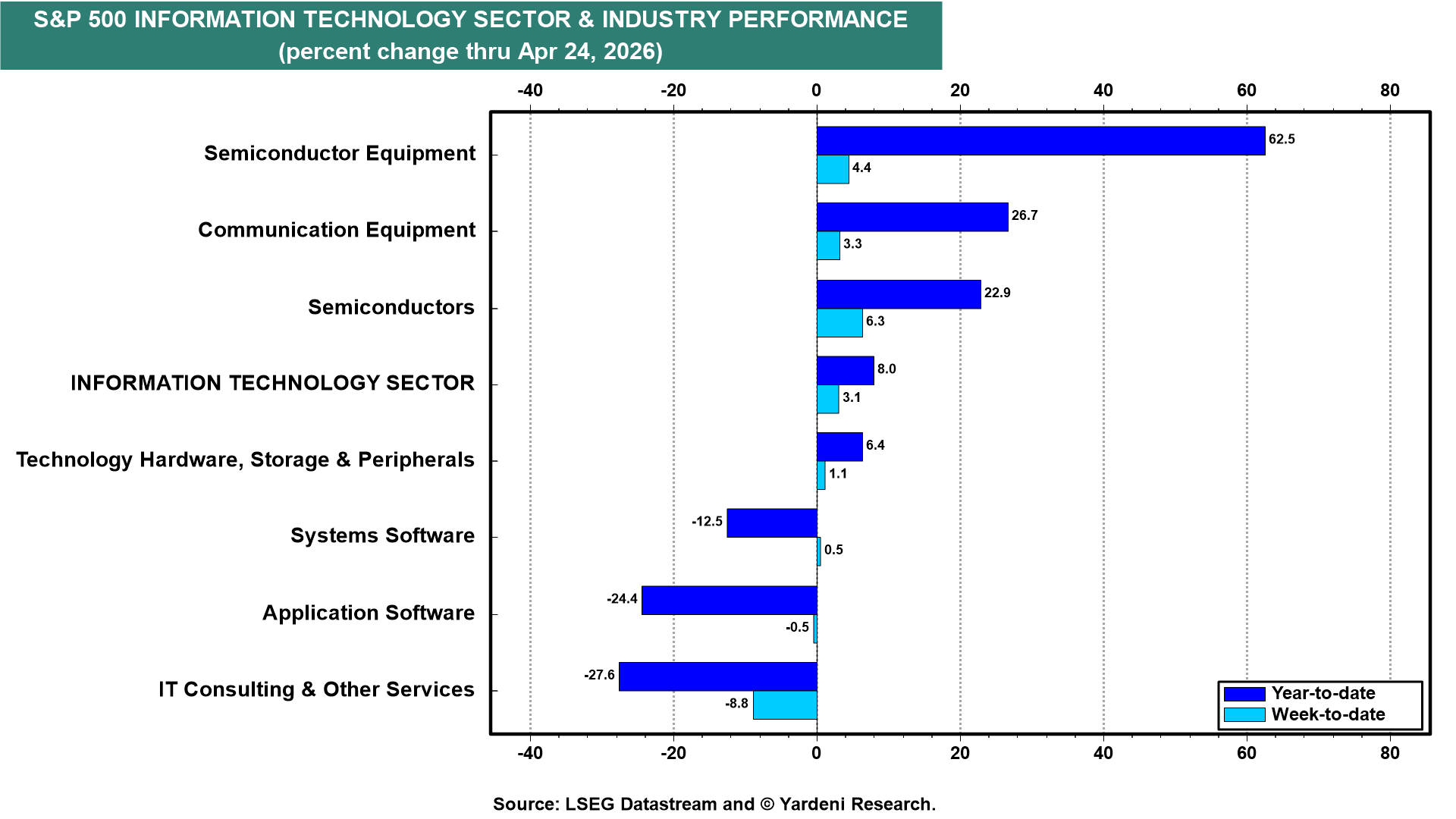

Focusing now on the S&P 500 Information Technology sector, it is up 8.0% ytd. However, there is an unusually large spread between the winners and the losers (chart). The former are all IT hardware industries that stand to benefit from rapid AI adoption, while the latter include IT software and services that face existential risks from AI replacement. It's a classic example of Joseph Schumpeter's creative destruction model of capitalism.

Let's have a closer look at the sector's latest dynamics:

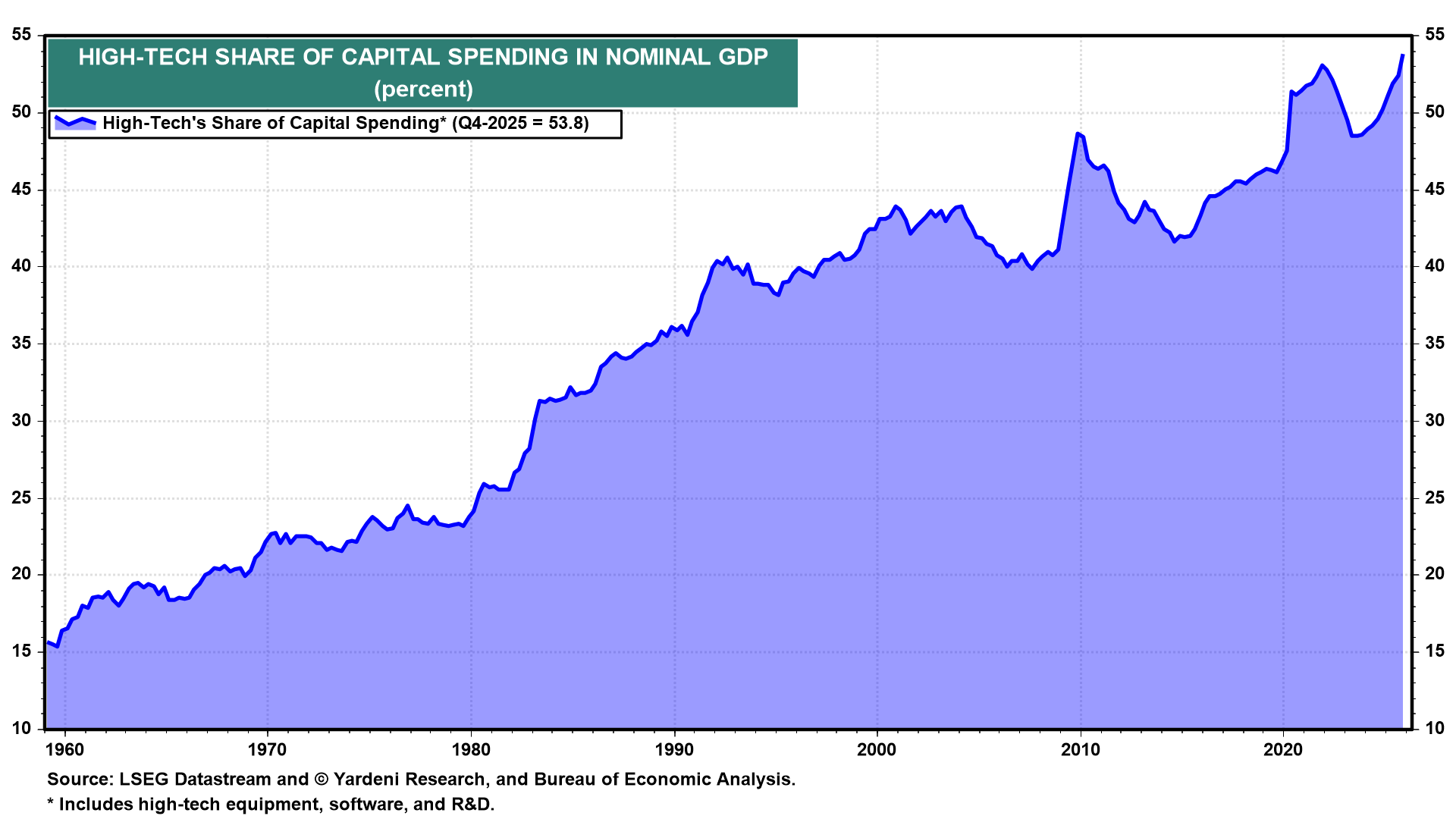

(1) High-tech accounts for a record 53.8% of nominal capital spending (chart). When the Digital Revolution began in the mid-1960s with the introduction of IBM mainframe computers, this percentage was just below 20%.

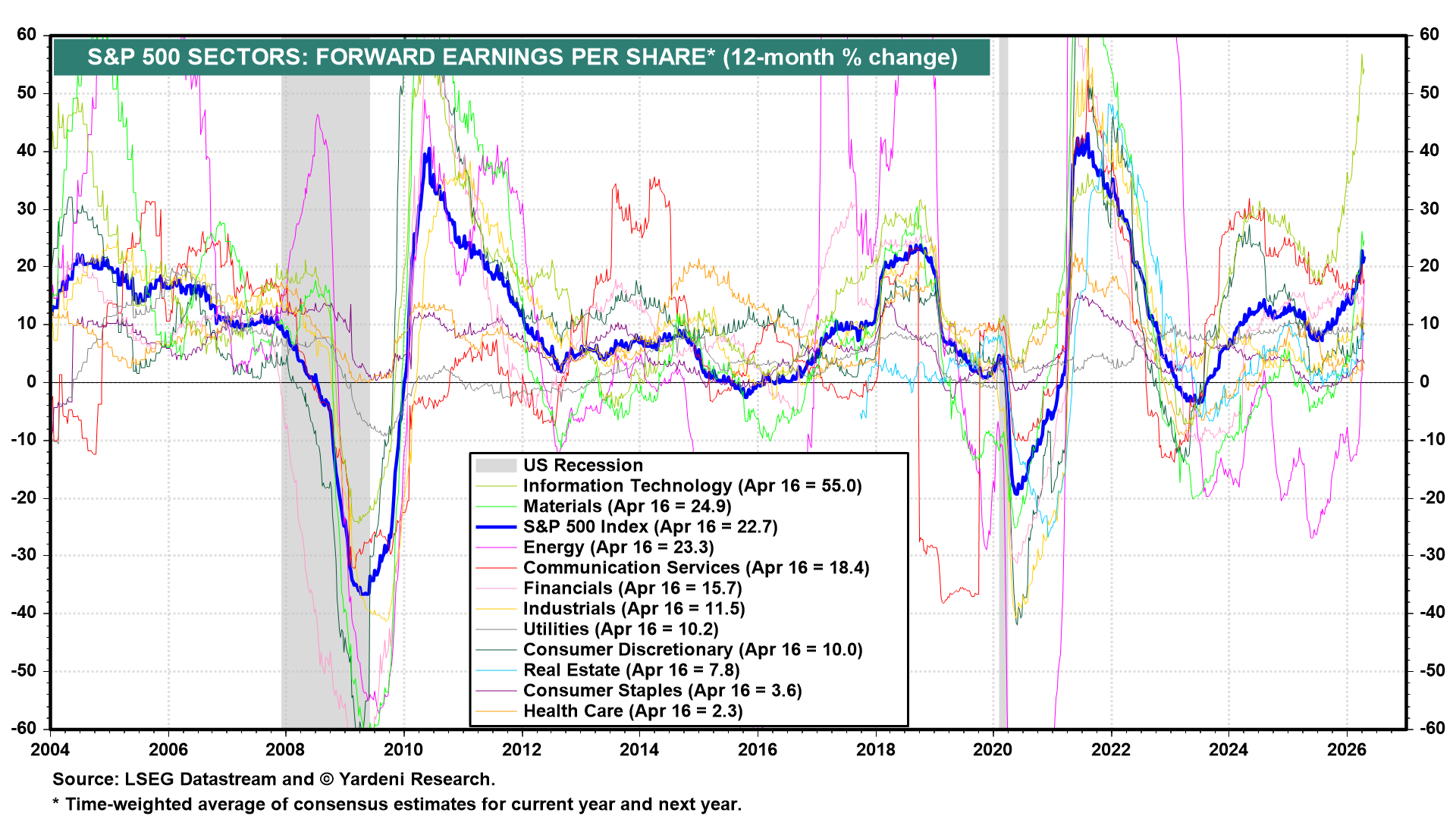

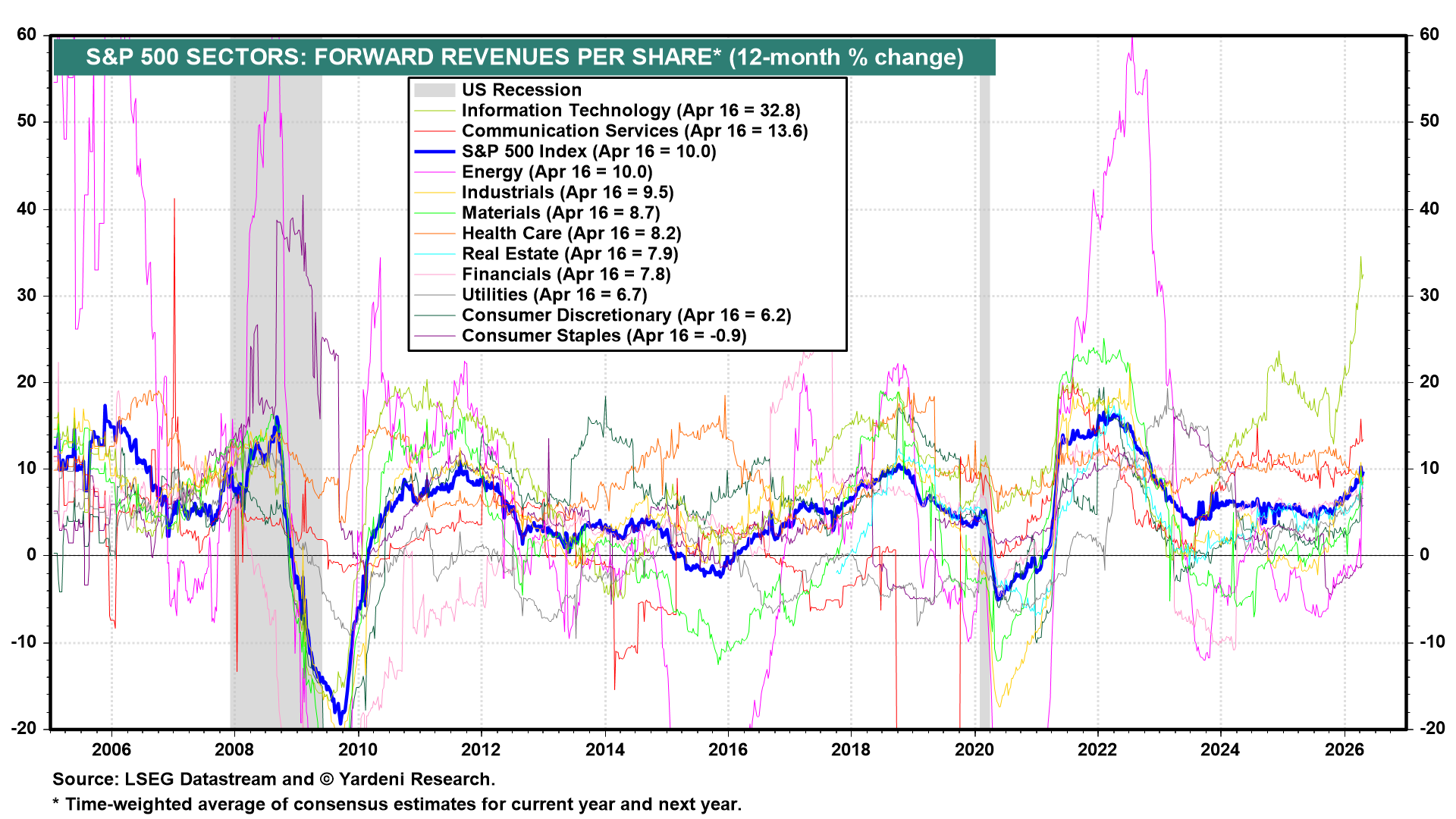

(2) Tech's fundamentals remain the strongest in the index. Forward earnings per share is up 55.0% y/y, and forward revenues per share is up 32.8% y/y through the week of April 16. Both are the highest growth rates of any S&P 500 sector by a wide margin (charts).

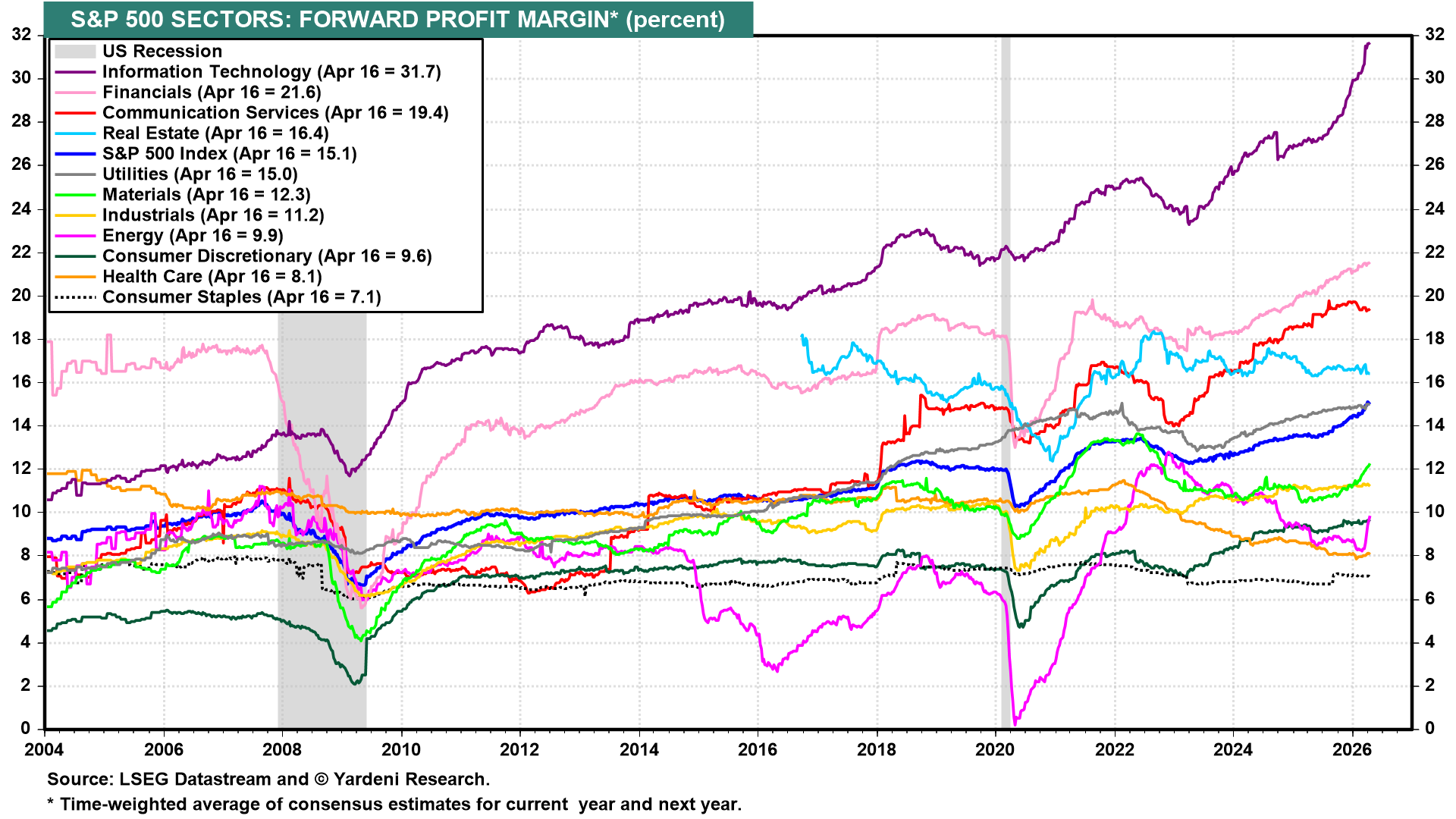

(3) The sector's forward profit margin is 31.7%, also a sector-leading figure and the highest on record for IT (chart). The sector's underperformance this year has nothing to do with deteriorating fundamentals.

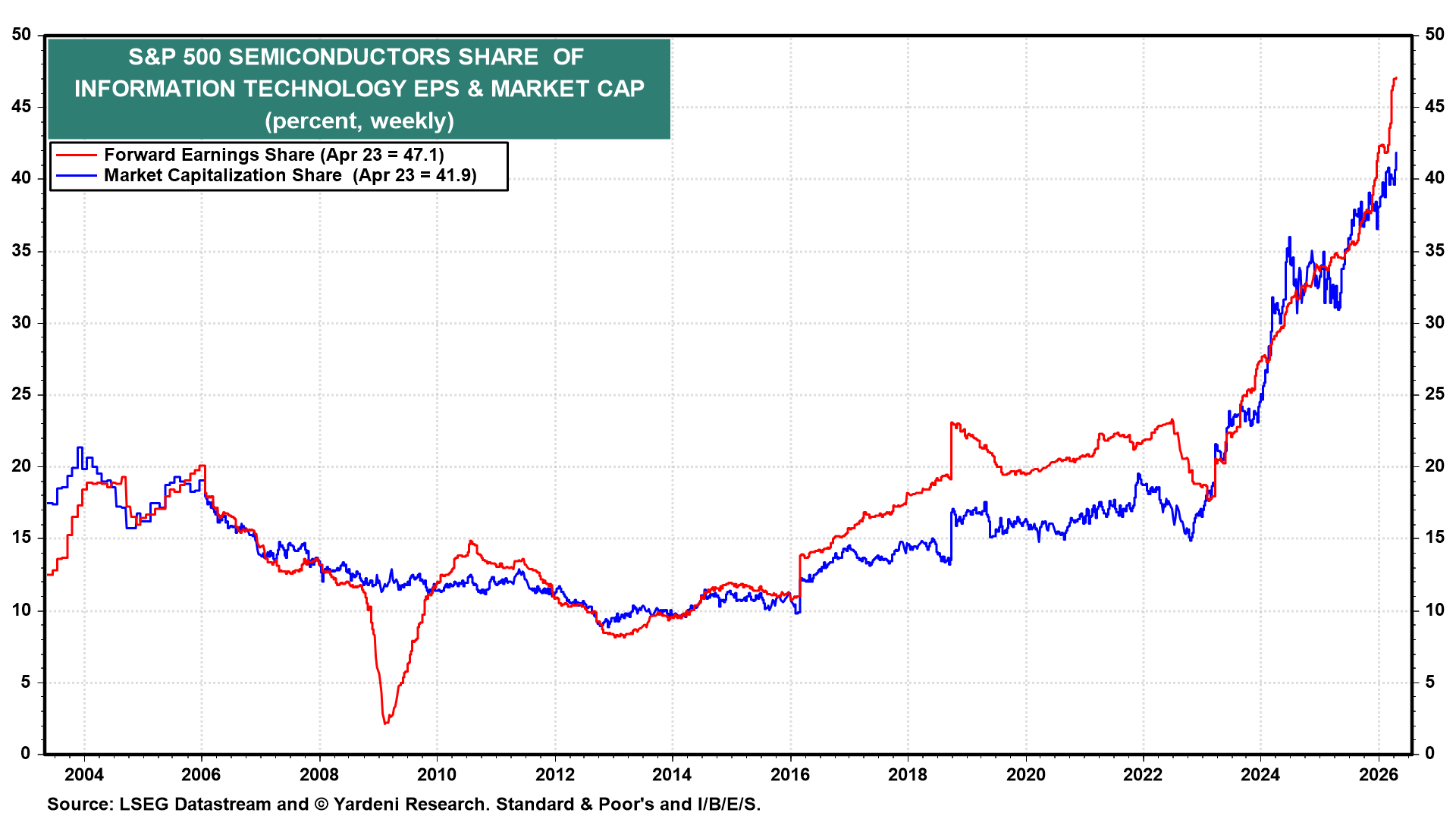

(4) The S&P 500 Semiconductors industry now accounts for a record 41.9% of the S&P 500 Information Technology market cap, up from roughly 15% a decade ago. Further, its share of IT forward earnings has moved even higher, to 47.1% (chart). Within a few quarters, half of every dollar of IT profits could come from chips!

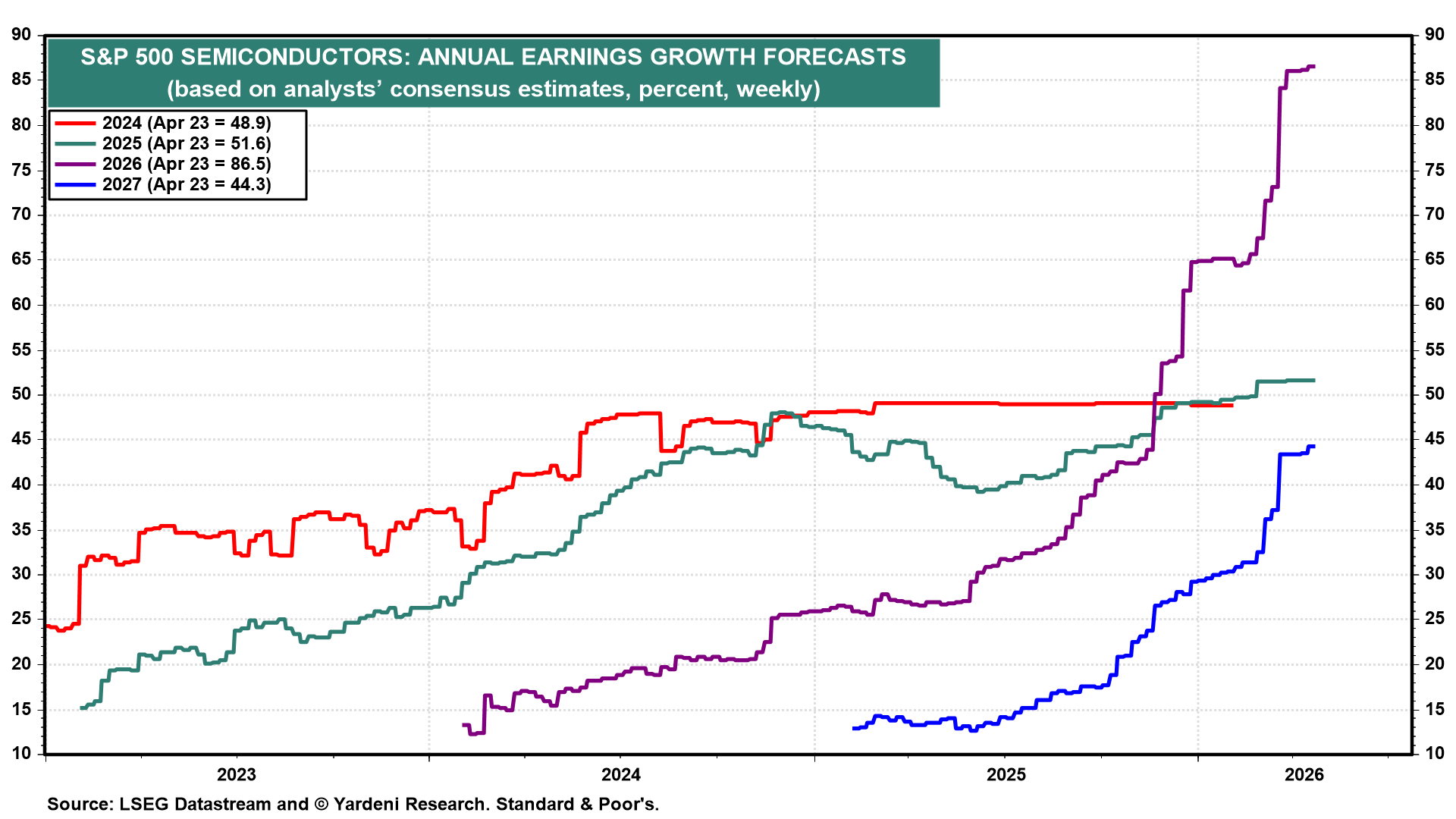

(5) Analysts' consensus 2026 earnings growth forecast for S&P 500 Semiconductors has been revised up to 86.5% from 65.0% at the start of this year (chart). The 2027 growth estimate is at 44.3% and climbing.

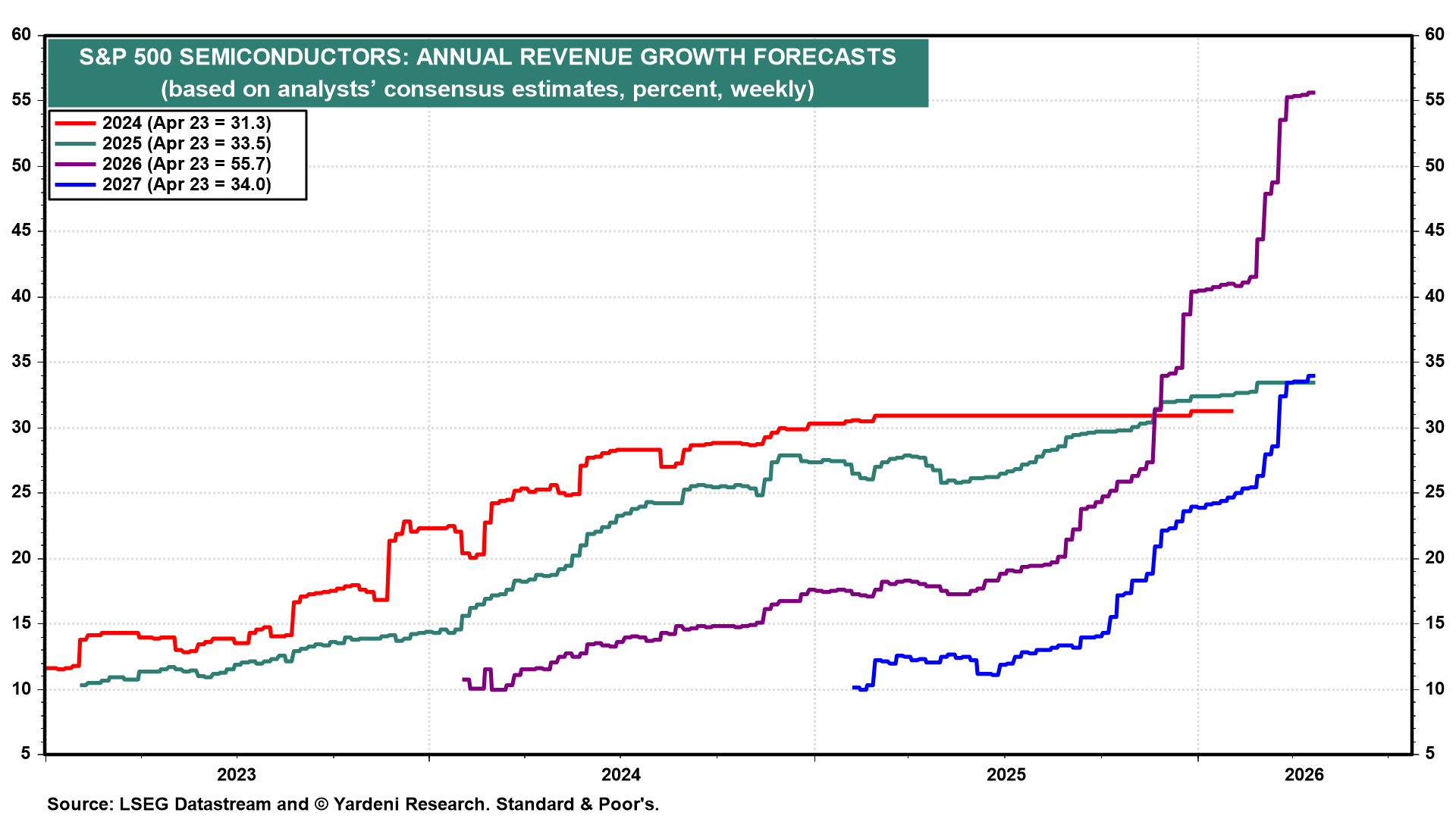

Revenue growth forecasts tell the same story, with 2026 at 55.7% and 2027 at 34.0% (chart).

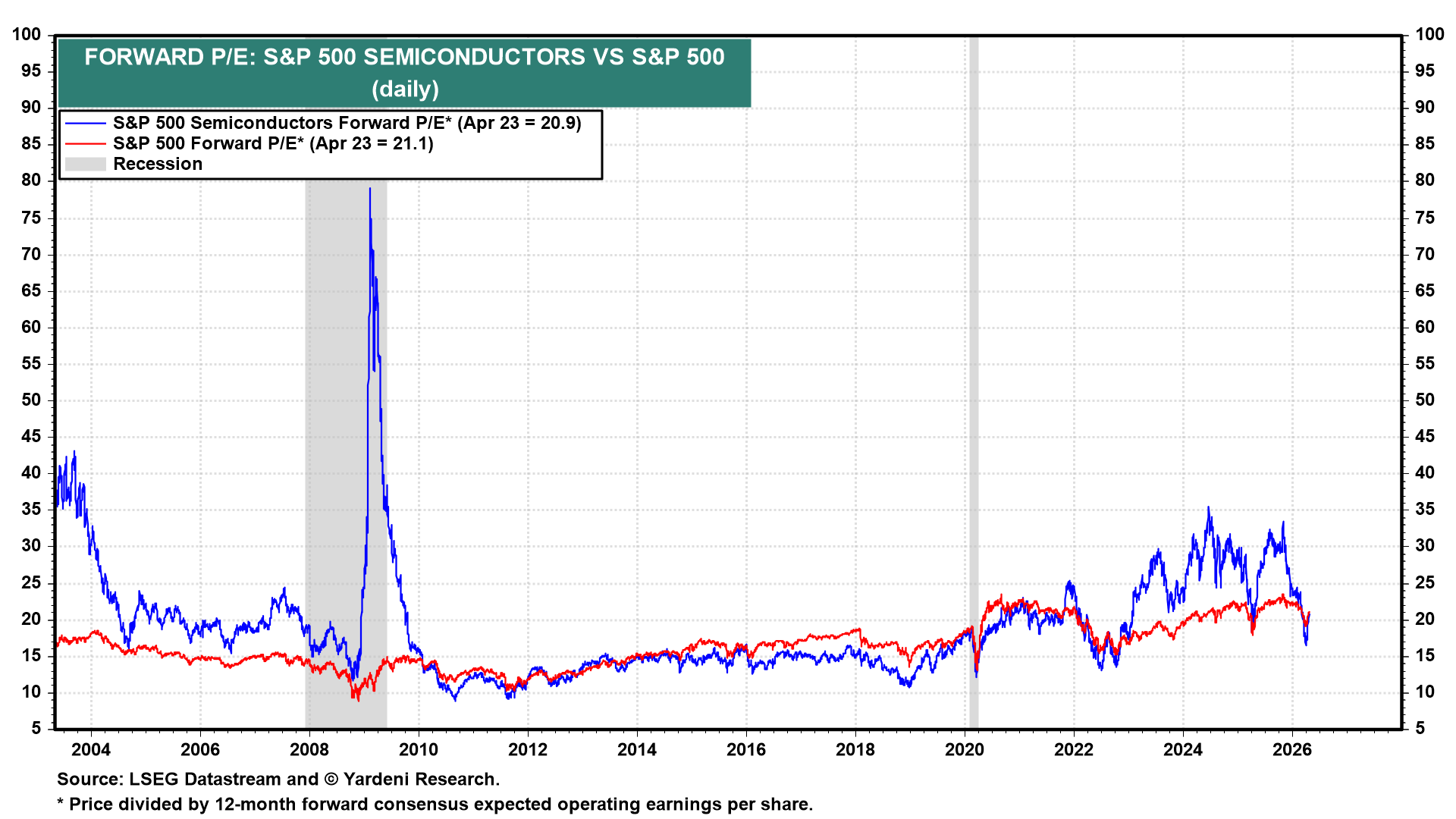

(6) Despite that heady earnings outlook, the S&P 500 Semiconductors forward P/E is currently 20.9, slightly below the S&P 500 P/E at 21.1 (chart). This multiple exceeded 35.0 in 2024. The industry most beneficially exposed to AI, the defining growth theme of the Roaring 2020s, is trading at a discount to the market!

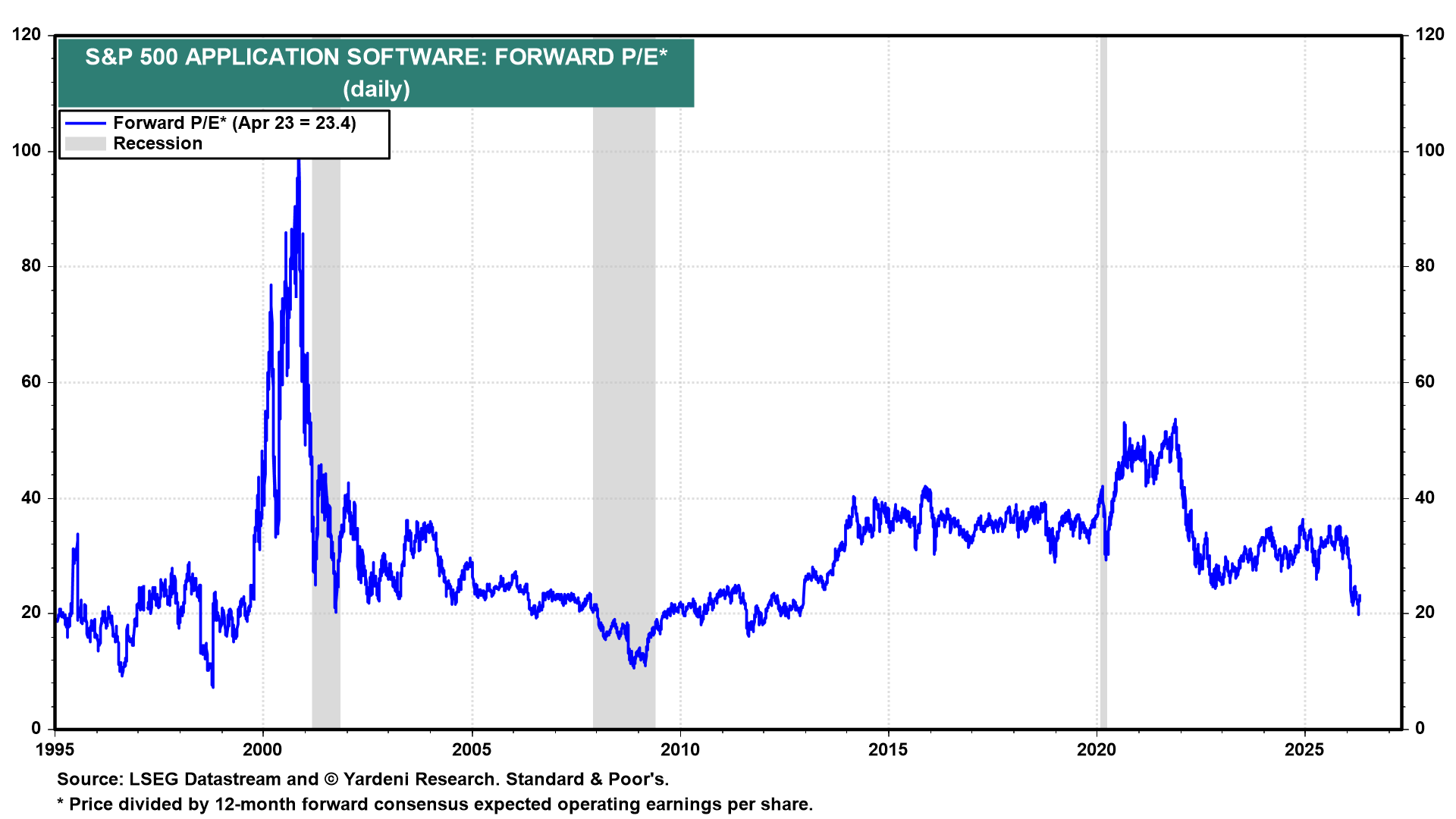

(7) The unhappier side of IT tells the opposite story. The S&P 500 Application Software forward P/E has compressed to 23.4, the lowest reading since 2014, and is roughly half the 2021 peak of 53.7 (chart). The industry's forward revenues, earnings, and profit margin all are at record highs. Investors are anticipating that these fundamentals all will deteriorate as AI adoption becomes more widespread.