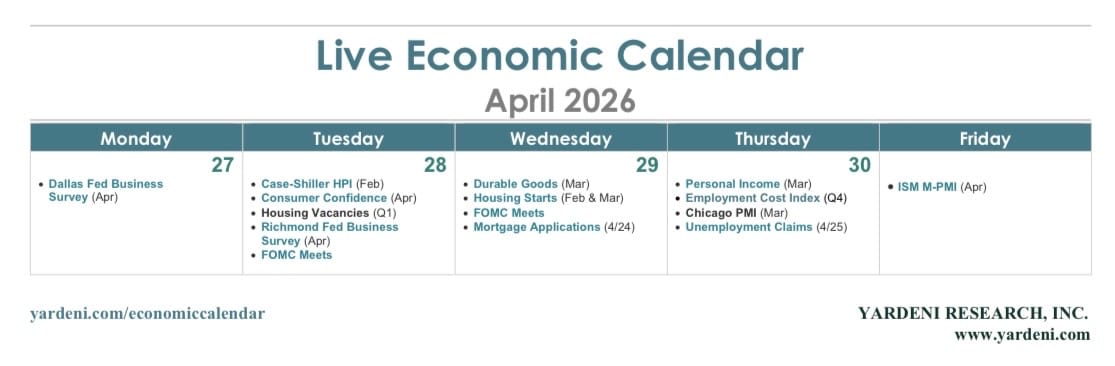

This is one of the busiest weeks of the year on the economic calendar. Five major central banks meet: the Fed, the Bank of Japan, the Bank of Canada, the European Central Bank, and the Bank of England. Five mega-cap tech names report earnings: Alphabet, Amazon, Meta, Microsoft, and Apple. Wednesday brings the advance Q1-2025 GDP report, and Thursday the March PCED, which will show how much of the oil shock has hit the Fed's preferred inflation gauge. There will also be plenty of fresh survey data, with regional business surveys complementing Friday's national M-PMI print, plus the Conference Board's April Consumer Confidence Index, all on tape.

The blockade of the Strait of Hormuz by both the US and Iran remains the overriding issue. Both the US and Iran declined to meet in Islamabad this weekend. The price of a barrel of Brent crude closed at $105.33 on Friday, almost $20 above last week's low (chart).

With that said, let's take a look at the key releases most likely to shape investors' thinking on growth, inflation, and the central bank reaction function this week:

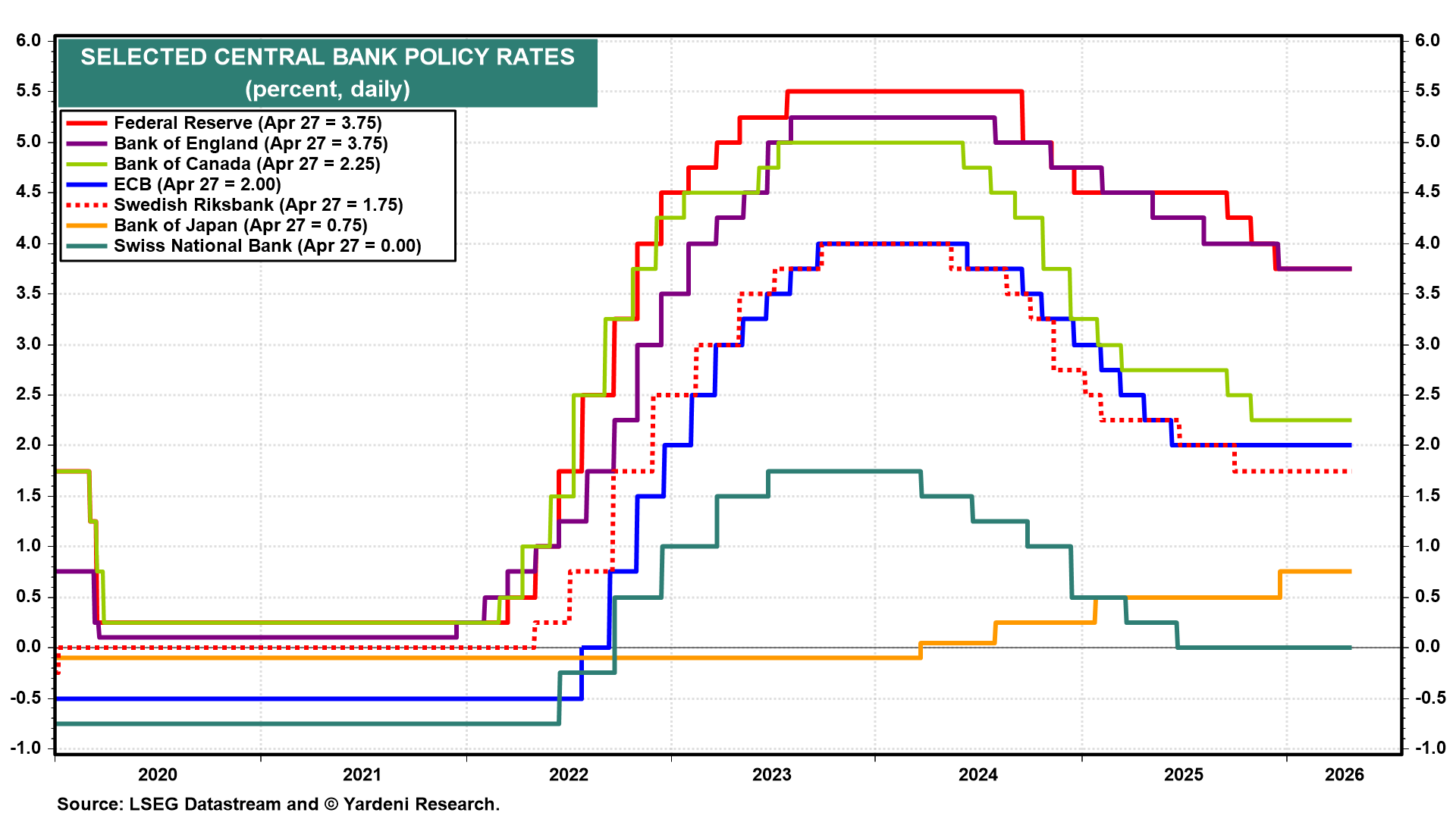

(1) FOMC and the global central bank docket. All five central banks are expected to remain on hold, leaving their policy rates roughly where they've been since late 2025 (chart). As is usually the case when the rate decisions themselves are foregone conclusions, investors will be reading the official commentary closely. Fed Chair Jerome Powell's press conference on Wednesday is the main event. The pronouncements of the other central bankers all will be parsed for how they frame the oil shock, the growth slowdown, and inflation pass-through.

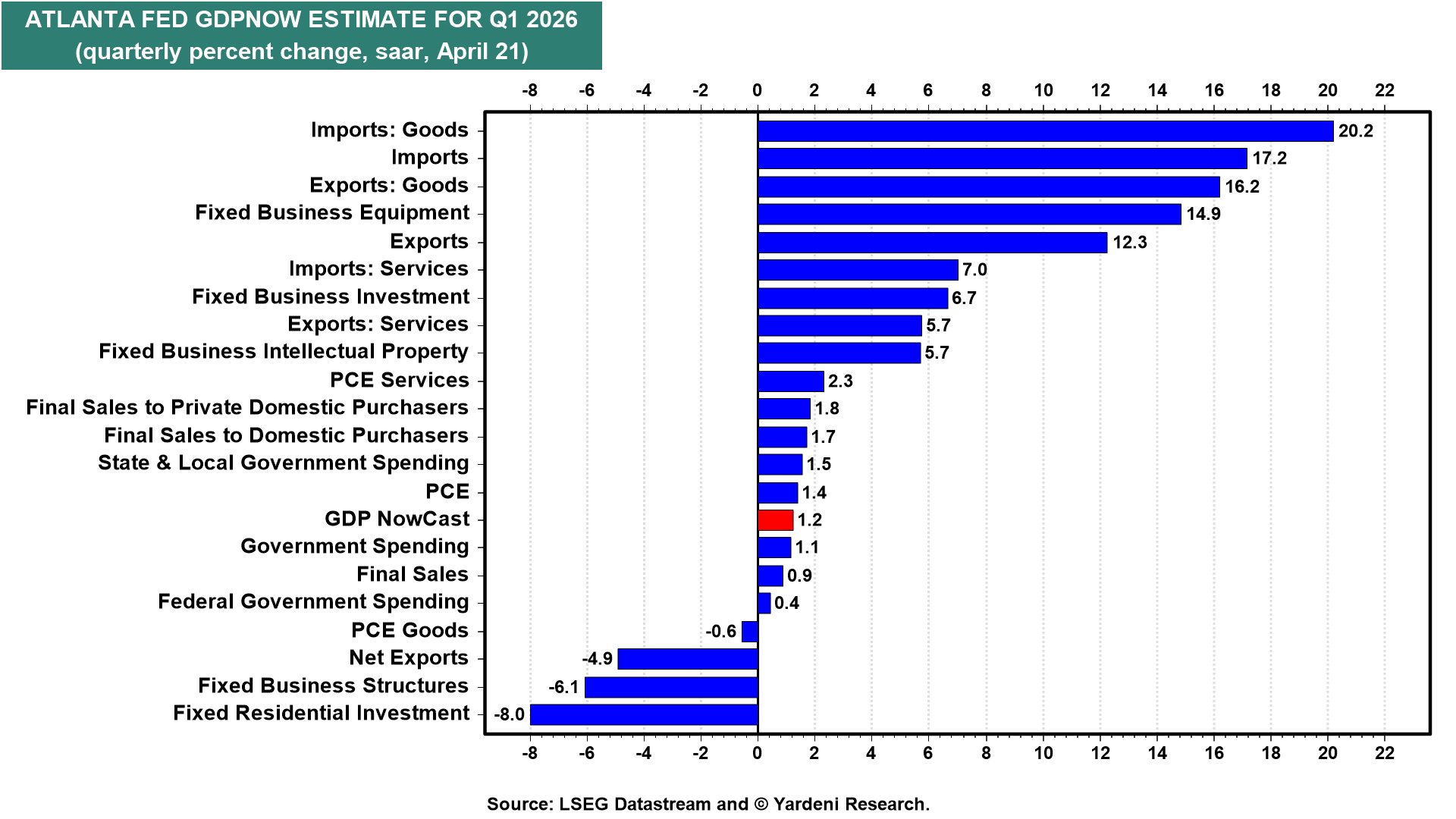

(2) GDP. Q1-2025 GDP (Wed) is likely to be up 1.2% according to the Atlanta Fed's GDPNow model. We are still blaming bad weather in January and February for the weakness (chart).

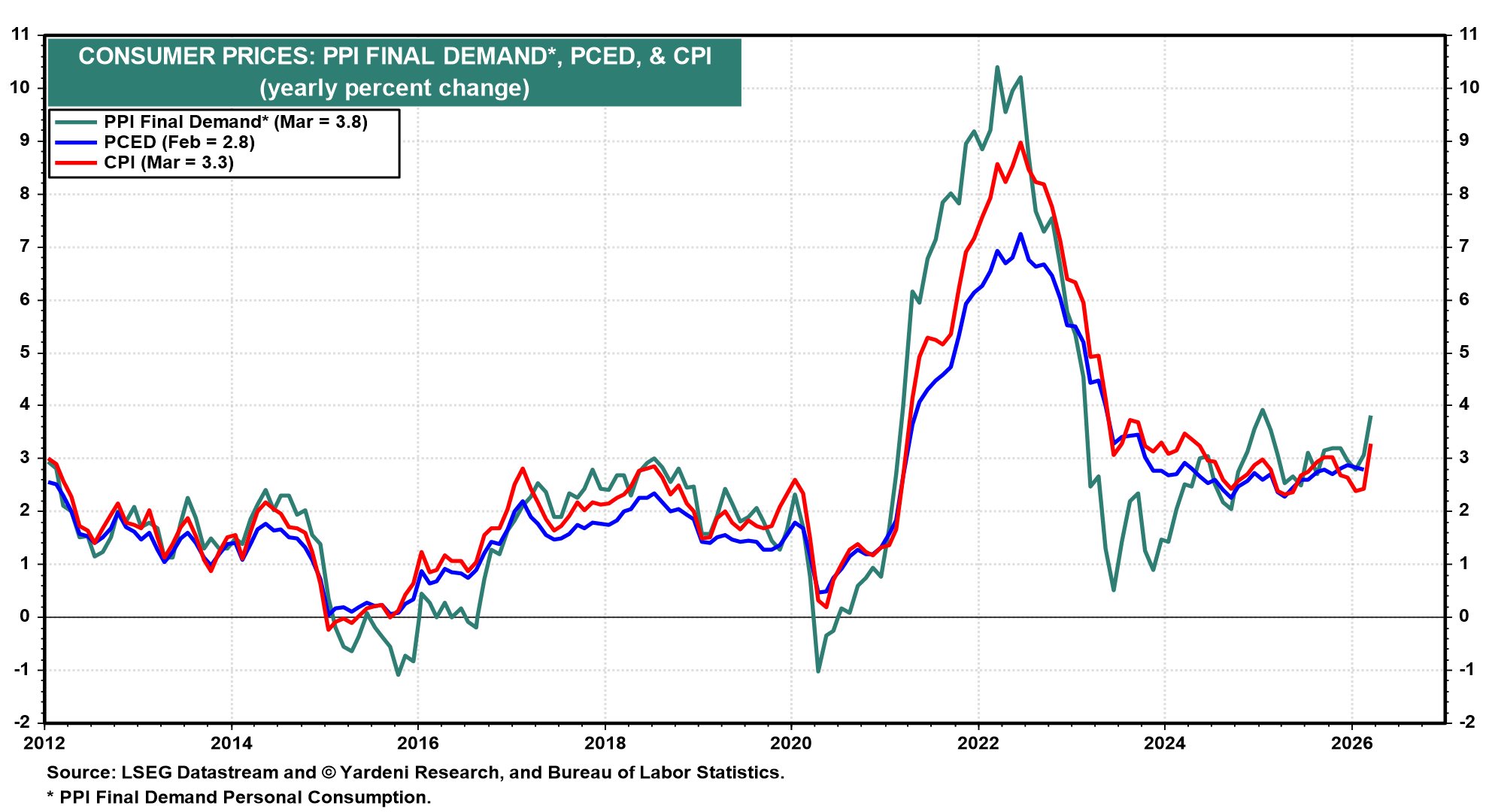

(3) Inflation. March PCED (Thu) is the first clean read on how much of the oil shock is reaching the Fed's preferred inflation gauge. Headline PCED inflation was 2.8% y/y in February (chart). The Cleveland Fed's Inflation Nowcasting model projects headline inflation to rise to 3.39% y/y in March (0.59% m/m).

The core PCED inflation rate is tracking at 3.10% y/y and 0.23% m/m (chart).

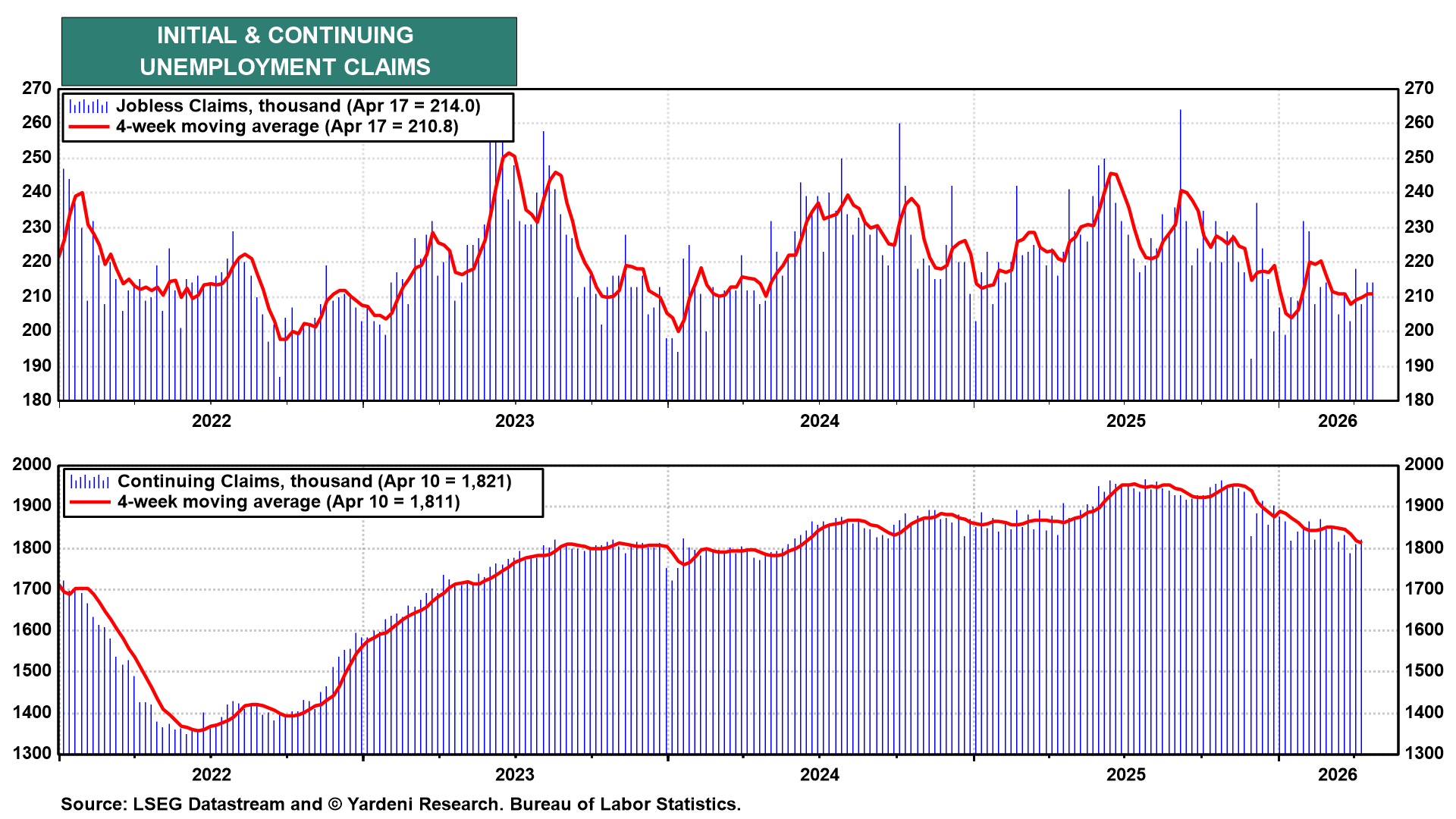

(4) Unemployment. Initial jobless claims (Thu) rose to 214,000 for the week of April 17, with the four-week moving average edging up to 210,800 (chart). Continuing claims ticked up to 1,821,000, though the four-week moving average continues to trend lower (chart). The labor market likely remained resilient during the second half of April.

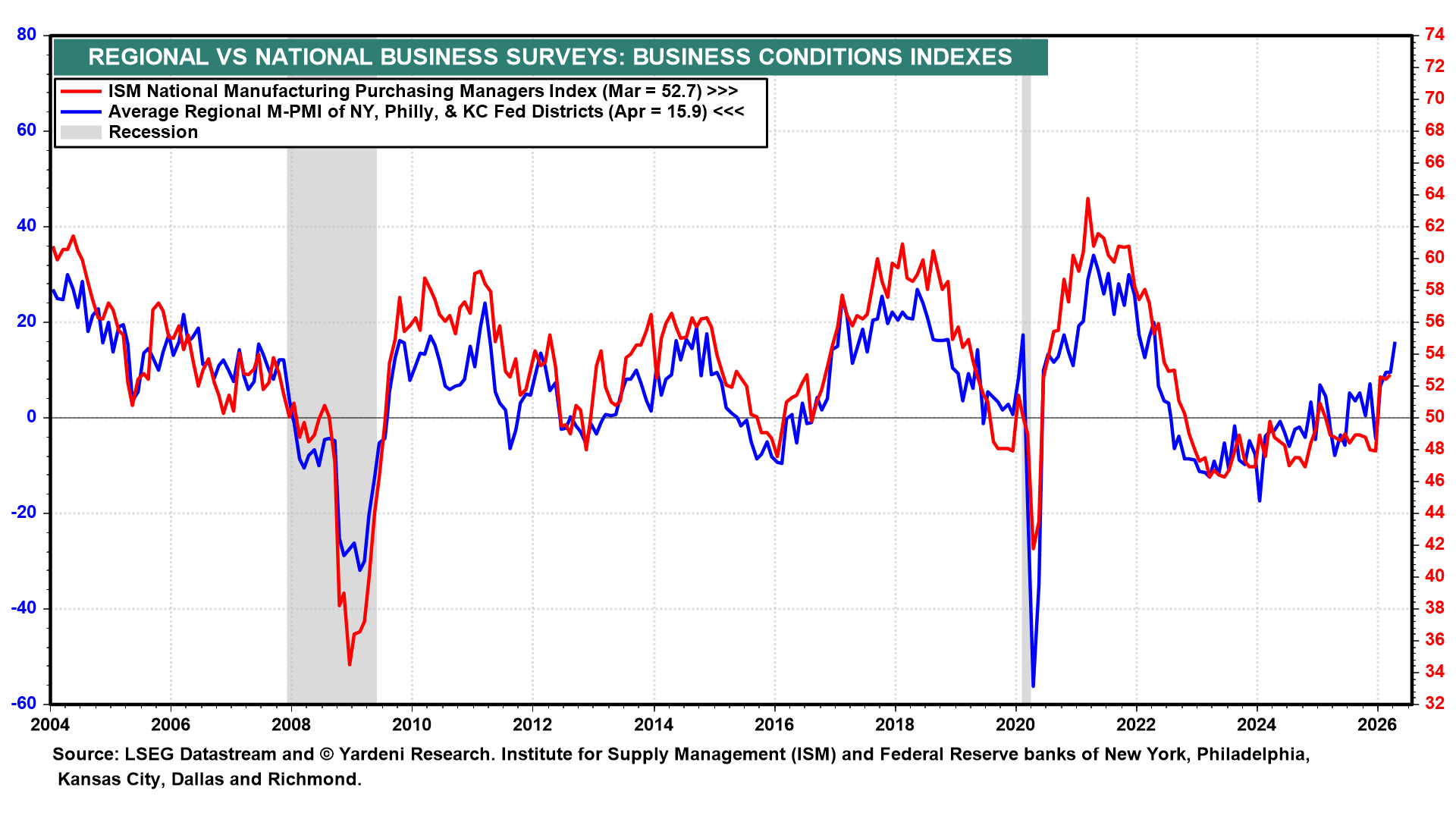

(5) Manufacturing surveys. Along with Friday's national M-PMI, business surveys will be released by the Dallas Fed (Mon), Richmond Fed (Tue), and Chicago PMI (Thu). The April regional composite already sits at 15.9 based on the three available surveys (chart). That suggests another solid reading for April's M-PMI.

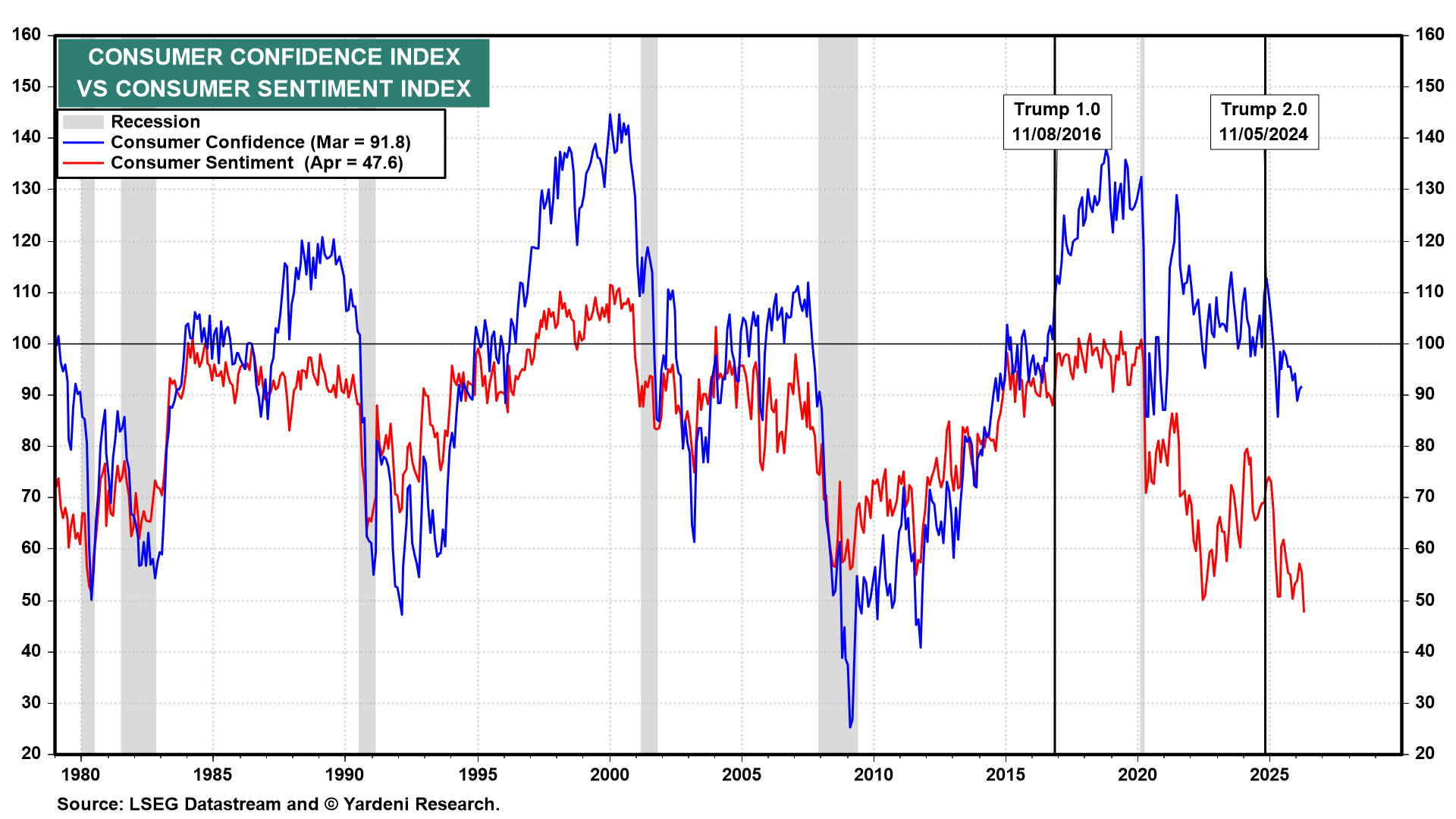

(6) Consumer Confidence. April's Consumer Confidence Index survey (Tue) might follow April's Consumer Sentiment Index lower (chart). While sentiment matters, consumers are still spending for now. The latest CCI survey might find that employment indicators are showing some signs of life, in our opinion.