In the autumn of 1956, Egypt's Gamal Abdel Nasser nationalized the Suez Canal. Britain, France, and Israel invaded. The canal closed for five months. Two-thirds of Western Europe's oil moved through it, and the price of crude doubled in dollar terms before the year was out. The Dow Jones Industrial Average fell about 10% from its July high to its October low. Tankers were forced to reroute. By the following spring, with the canal reopened, the DJIA had recovered and reached a new high. With the exception of the 1970s, geopolitical oil supply shocks have tended to be buying opportunities for stocks.

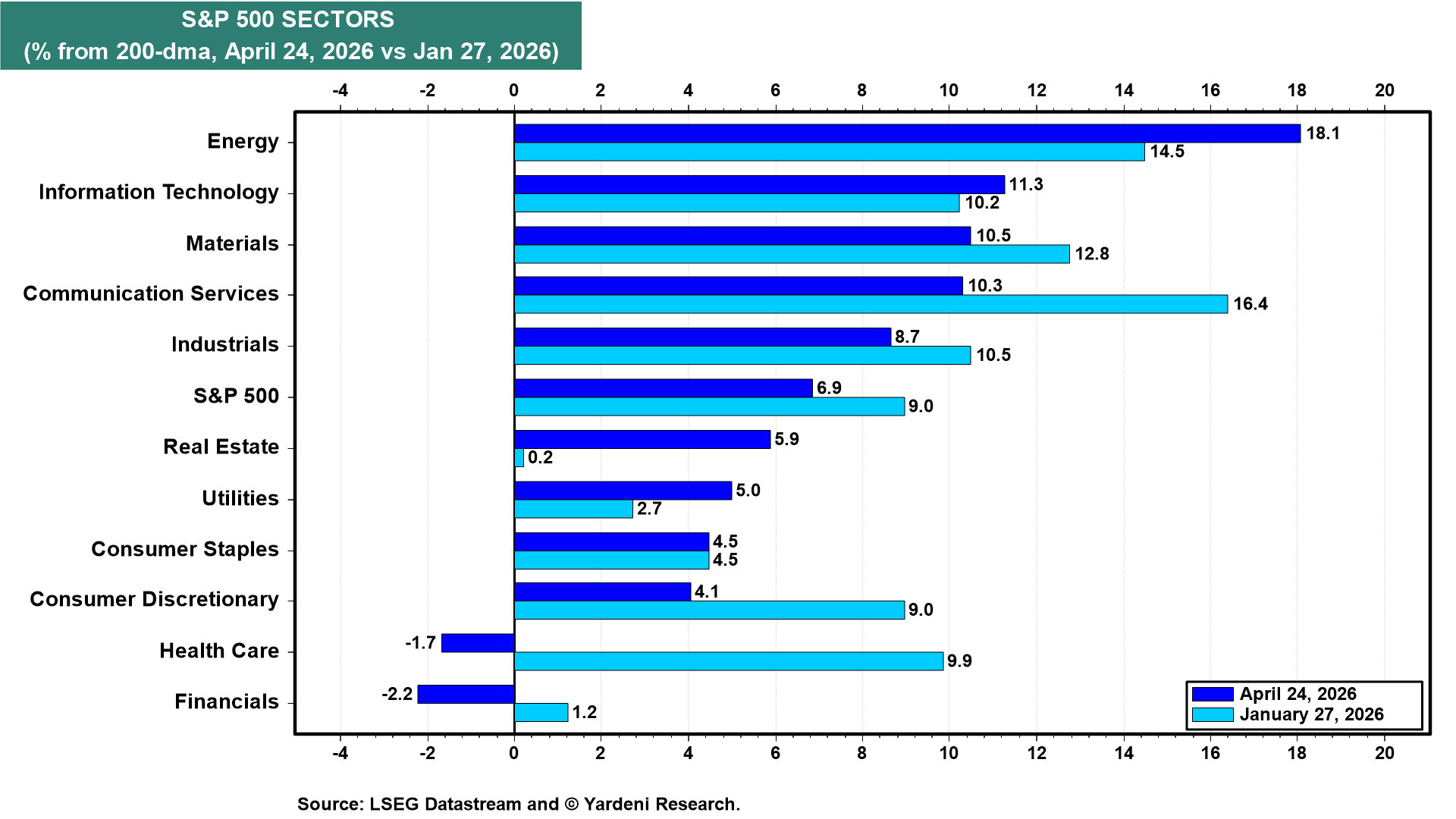

Investors reached the same conclusion again, this time on March 31. The fact that the Strait remains closed hasn't stopped the extraordinary stock market rally since then. Interestingly, the S&P 500 Energy and Information Technology sectors are now more overvalued relative to their 200-day moving averages than they were at the market's January 27 peak (chart). This suggests that many investors may have a barbell position across these two sectors, in case everything goes right (so IT wins) or wrong (so Energy wins). That makes sense to us since we are recommending a market weight in IT and an overweight in Energy.

This evening, the price of a barrel of Brent crude is up a couple of bucks because neither the US nor Iran showed up for another round of peace talks in Islamabad over the weekend. This morning, President Donald Trump said, "If they want to talk, they can come to us, or they can call us. You know, there is a telephone. We have nice, secure lines." For now, the ceasefire is holding, but so are the US blockade of Iranian ports and the Iranian blockade of the Strait of Hormuz. This could be the new status quo for a while.

Our base case from here is that the S&P 500 chops around 7,000 while the stalemate holds, then grinds higher in the second half of this year toward our 7,700 year-end target. That's assuming a deal by mid-year. Midterm elections drama might make the ride bumpy during the second half of this year. We think the March 30 low was the year's low.

There's no shortage of uncertainty, but it is quite certain that Kevin Warsh will be the next Fed chair, now that the Department of Justice has dropped its criminal investigation of Jerome Powell over the Fed headquarters renovation overrun. Polymarket puts the odds of Kevin Warsh’s confirmation by May 15 at roughly 87%.

Also relatively certain is that the economy and corporate earnings remain resilient: