Tomorrow night at 8:00 p.m. is the deadline by which Iran must accept President Donald Trump's ultimatum to reopen the Strait of Hormuz or face a US attack on its power plants and bridges. There is no way to predict the outcome. We can't rule out that Iran will cave in. Or, Trump may postpone the deadline again, explaining that negotiations are making progress. Or the war will escalate. The fog of war remains thick.

Nevertheless, we expect that one way or another, Trump will declare victory in two to three weeks. If so, then the US economy should continue to grow, with a brief period of higher inflation. That's the initial verdict of the March national Purchasing Managers Indexes for both the manufacturing (M-PMI) and non-manufacturing (NM-PMI) sectors of the economy. Consider the following:

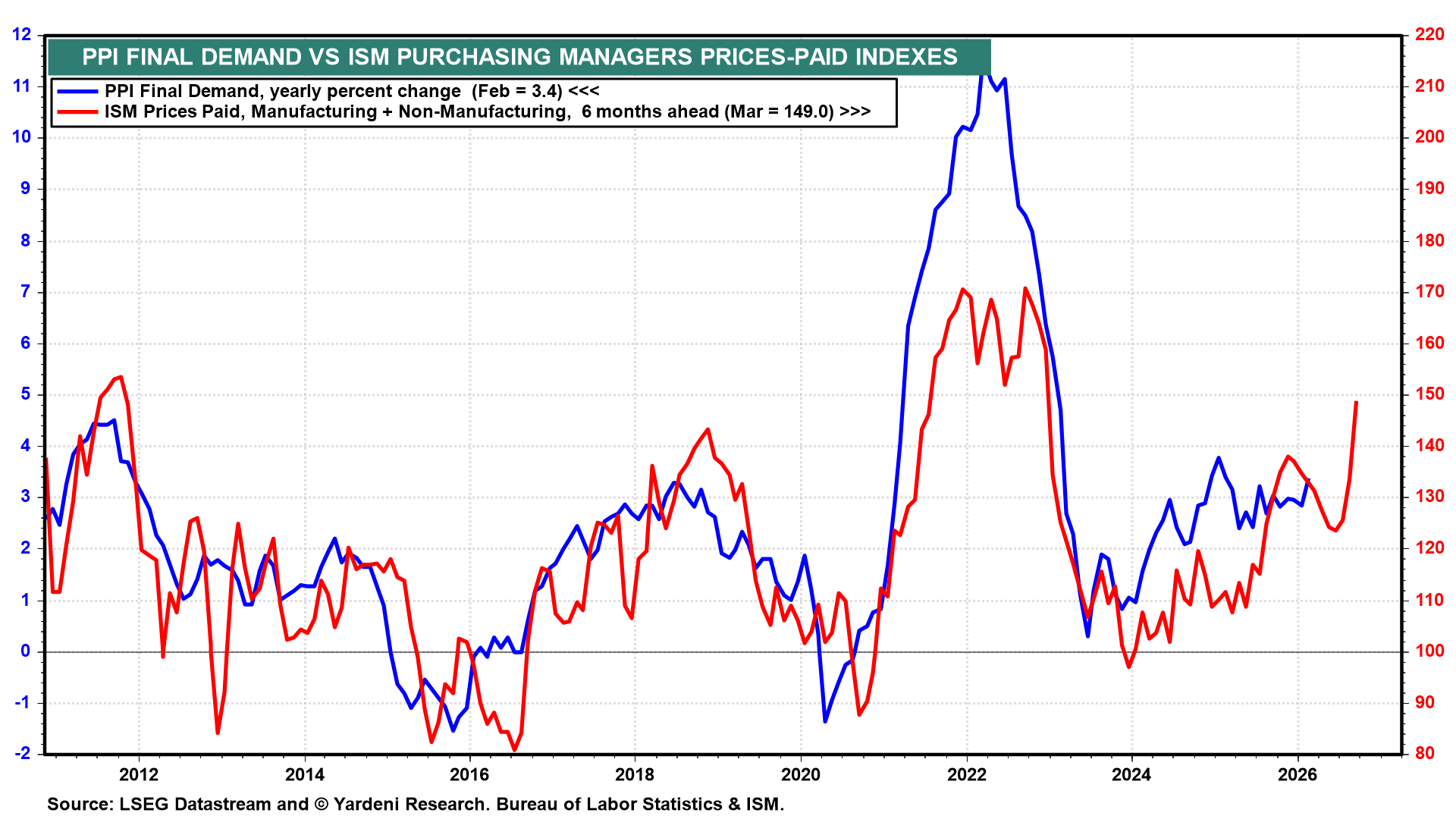

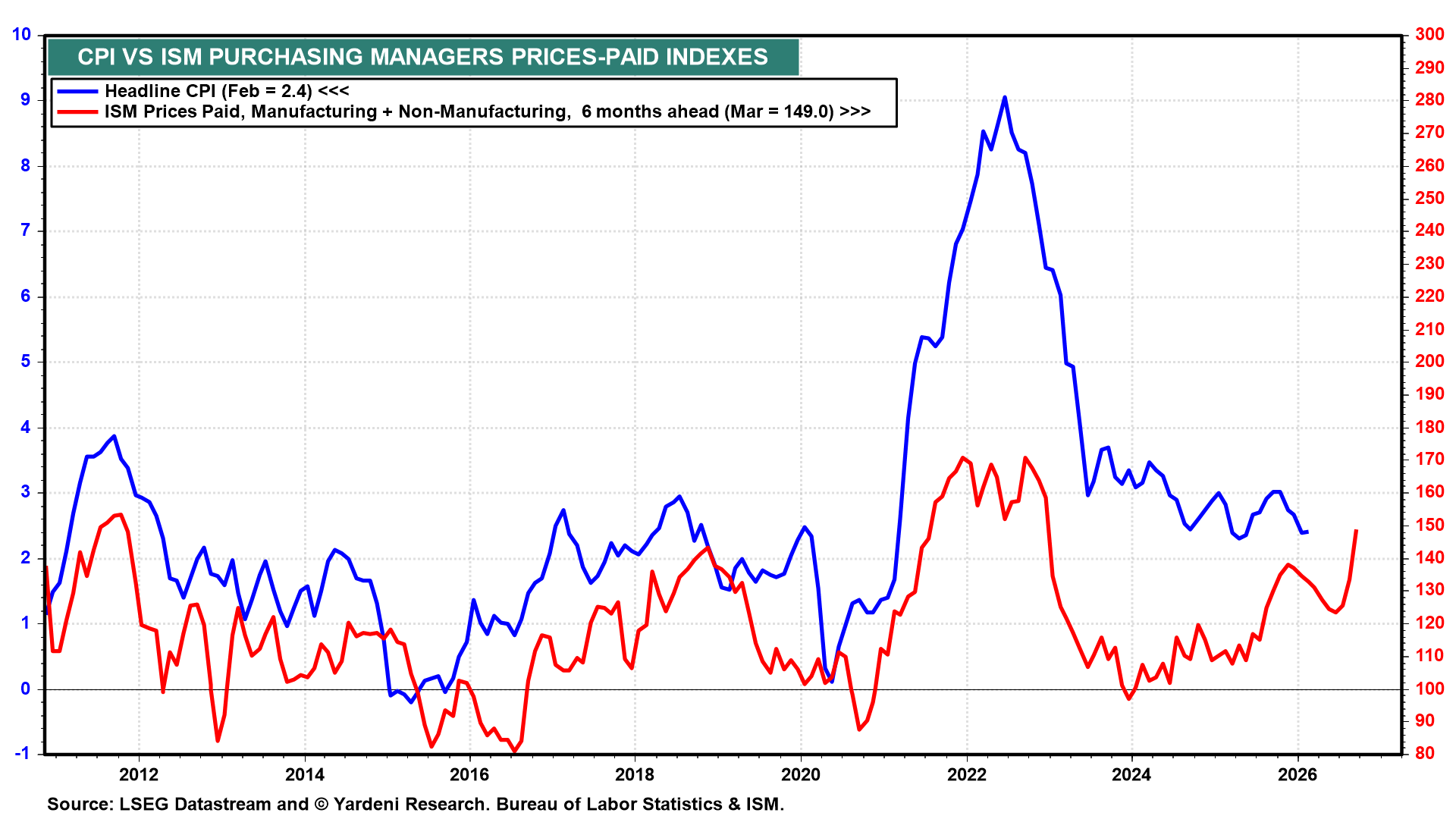

(1) Inflation in the PMIs. The sum of the prices-paid indexes for the M-PMI and NM-PMI is back to its level at the end of 2022 (charts). It tends to lead both the PPI and CPI inflation rates by about six months. So, both inflation rates are likely to rise in the coming months.

(2) M-PMI & the Economy. The manufacturing sector is likely to benefit from defense and energy spending resulting from the war. So it is no surprise to see that M-PMI rose in March to 52.7, the highest level since 2022, marking the third consecutive month of expansion following about three years of readings mostly below 50.0 (chart). Production posted its fifth straight month in expansionary territory, and new orders held comfortably in growth territory for a third consecutive month. Employment stayed in modestly contractionary territory.