The AI-driven semiconductor rally has been remarkable during the current bull market, which started on October 12, 2022. It received a big boost when ChatGPT was introduced on November 30, 2023. Memory chips have been a major driver of this rally, reflecting tight supply and rising content requirements across AI systems.

As AI workloads scale, performance is increasingly determined not just by compute but by memory. High-bandwidth memory (HBM) and advanced dynamic random access memory (DRAM) both are essential for AI training and for AI inference.

In the past, memory was one of the most cyclical segments of the semiconductor industry, characterized by sharp boom-bust dynamics driven by excessive capacity expansion during booms, thus setting the stage for busts. The key question now is whether this cycle might be less pronounced due to the high demand for memory driven by AI infrastructure spending.

Demand for memory is expected to remain elevated into 2027–28 before normalizing as supply catches up. Hyperscaler orders placed well in advance have effectively pulled forward demand visibility, while long lead times for fabs and equipment limit the speed of supply responses.

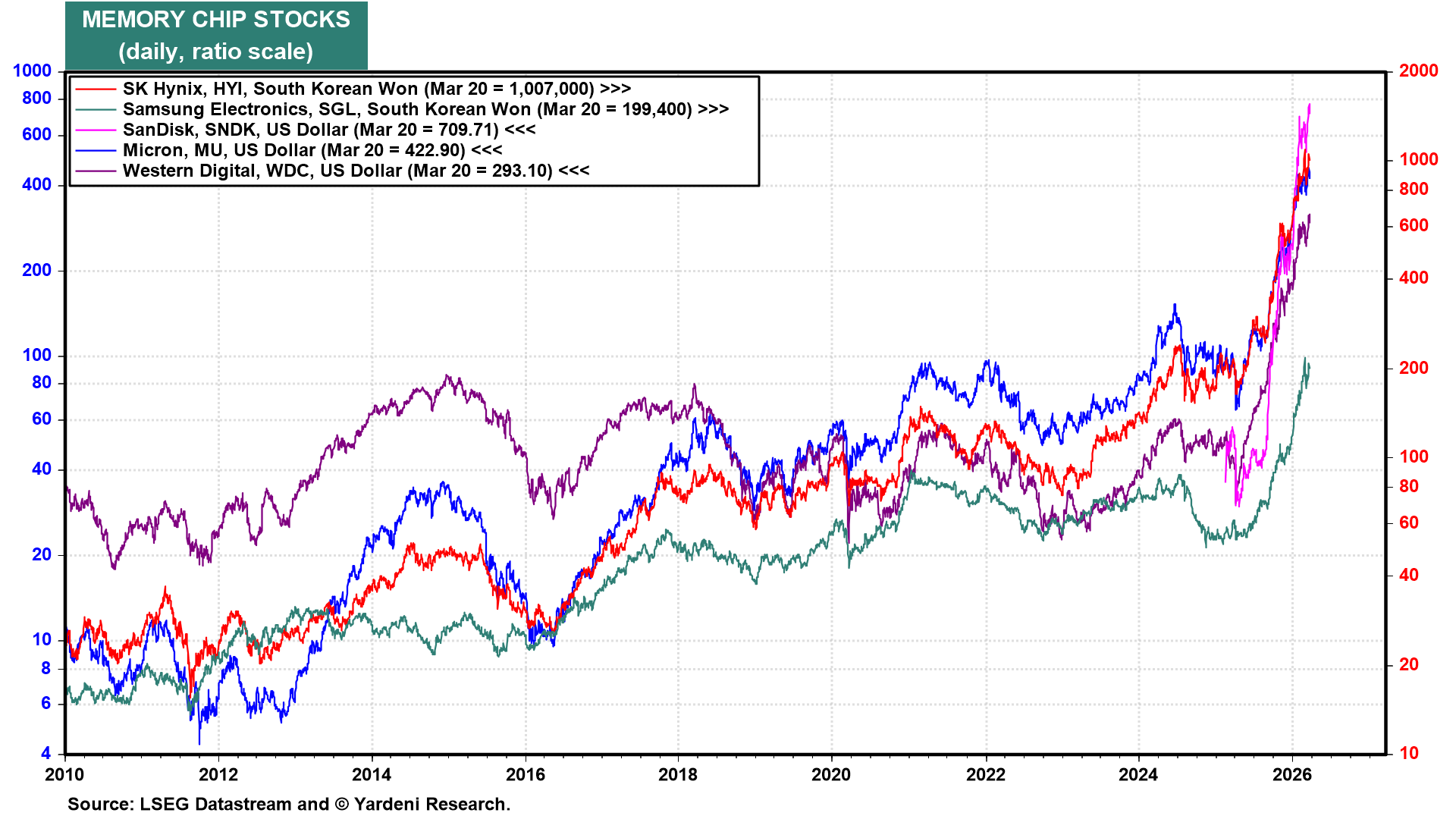

This dynamic is already reflected in market leadership, with memory chip stocks among the strongest performers globally as AI-driven demand continues to tighten supply (chart). Sandisk is a striking example, having successfully raised money with an IPO just 13 months ago, the stock has risen 1,836% from its IPO price, including a remarkable 158% ytd.

This strength is also showing up at the macro level. South Korea’s equity market, heavily exposed to memory and semiconductor exports, has rallied sharply in both local currency and US dollar terms, up 96% in the last year (chart). Notably, Samsung Electronics and SK Hynix alone account for roughly 43% of the iShares MSCI South Korea ETF (EWY), underscoring how the AI buildout is now influencing entire equity markets rather than just individual companies.