The S&P 500 has been meandering around 7,500 since mid-May. Earnings should continue to drive the stock market higher. However, investors may be fretting that expectations for the upcoming earnings reporting season are so high that if they aren't exceeded, the market might swoon again in July as it did in June. If so, dip buyers are likely to limit the downside. We still expect the S&P 500 to hit 8,250 by year-end.

Consider the following:

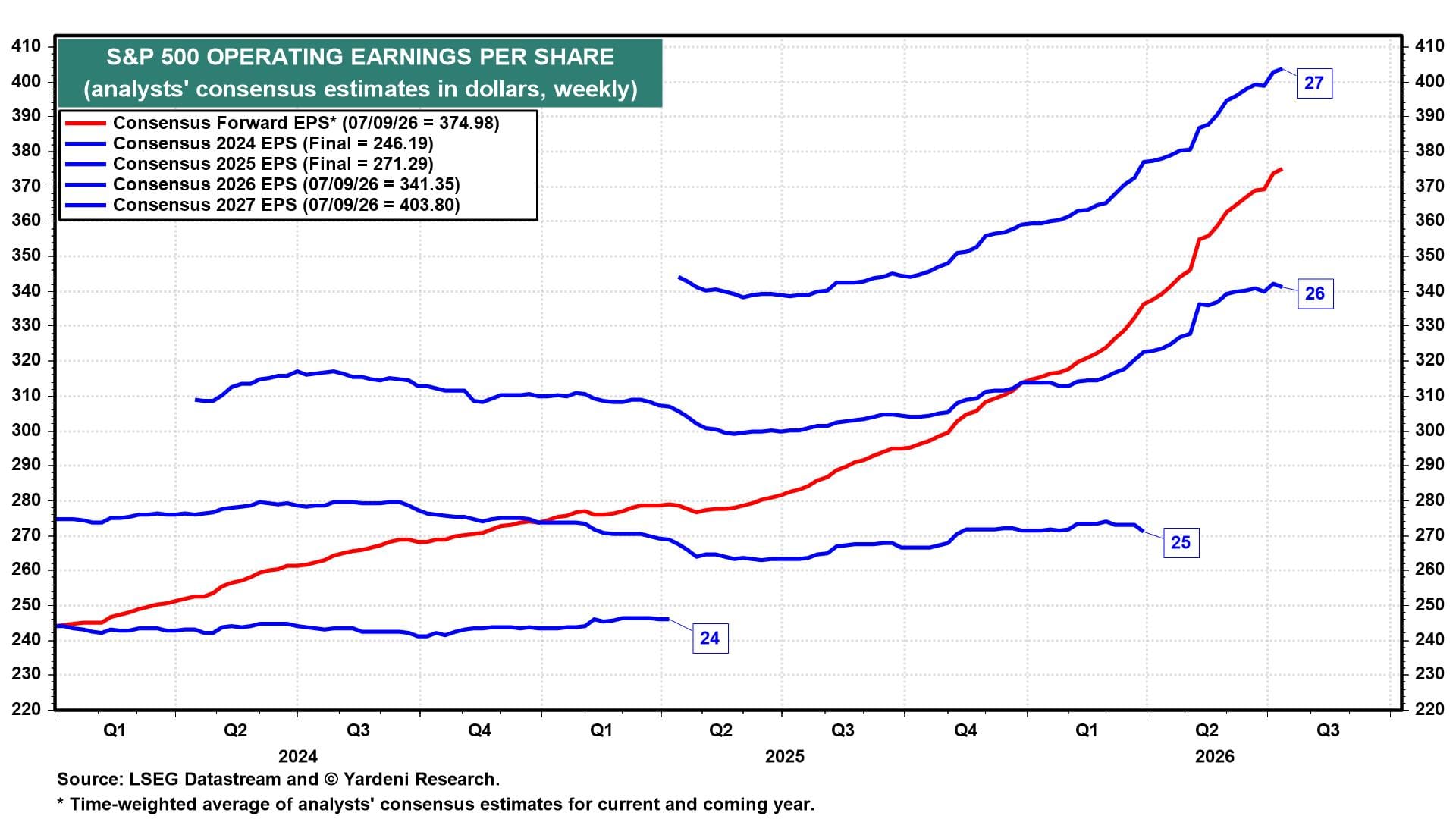

(1) Earnings. Fabulous earnings momentum (FEMO) moderated a bit heading into the Q2-2026 earnings season. S&P 500 companies’ aggregate forward earnings per share rose to yet another record high last week as the consensus 2027 EPS estimate edged higher, while the 2026 estimate dipped (chart). Forward earnings will converge with the 2027 estimate by the end of this year. That estimate is likely to continue to rise. If it reaches $412.50 by the end of this year, a 20.0 forward P/E would imply an S&P 500 level of 8,250. It could also get there with $400 earnings and a 20.6 multiple.

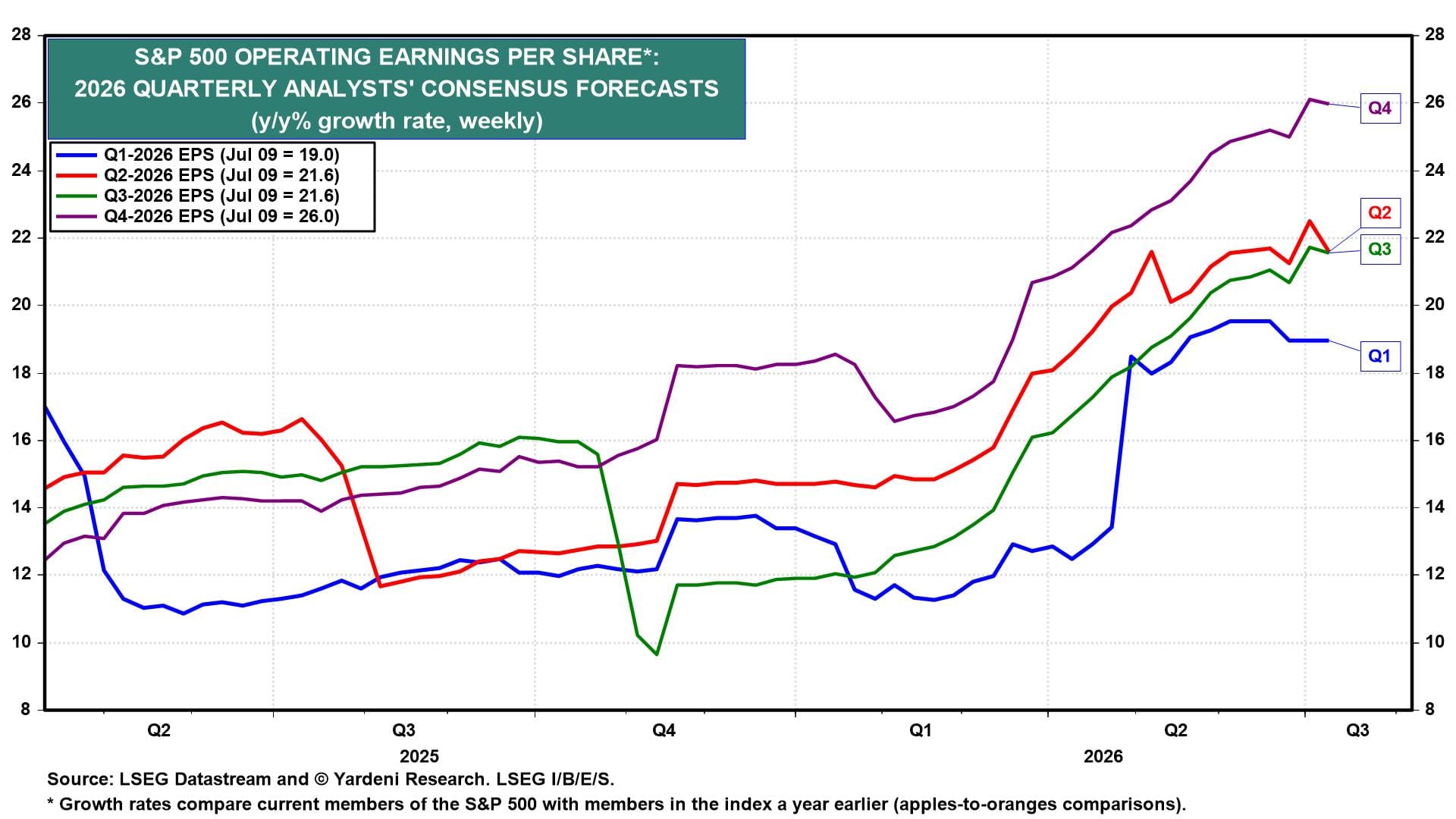

Analysts trimmed their aggregate Q2 earnings expectations slightly last week, but the estimate remains very strong, representing 21.6% y/y growth on an apples-to-oranges basis (chart). Q3 and Q4 are currently expected to be just as strong.

On a pro forma basis, which compares current S&P 500 index members to themselves a year earlier (apples-to-apples), expected Q2 earnings growth is even higher at 23.7% (chart). The Energy and Information Technology sectors are leading the way higher, while Health Care continues to sputter.

It's hard to imagine any upside surprises from here. That could be an issue for the stock market over the rest of this month and early August. But we would expect dip buyers to step in if Q2 earnings merely match rather than exceed expectations.

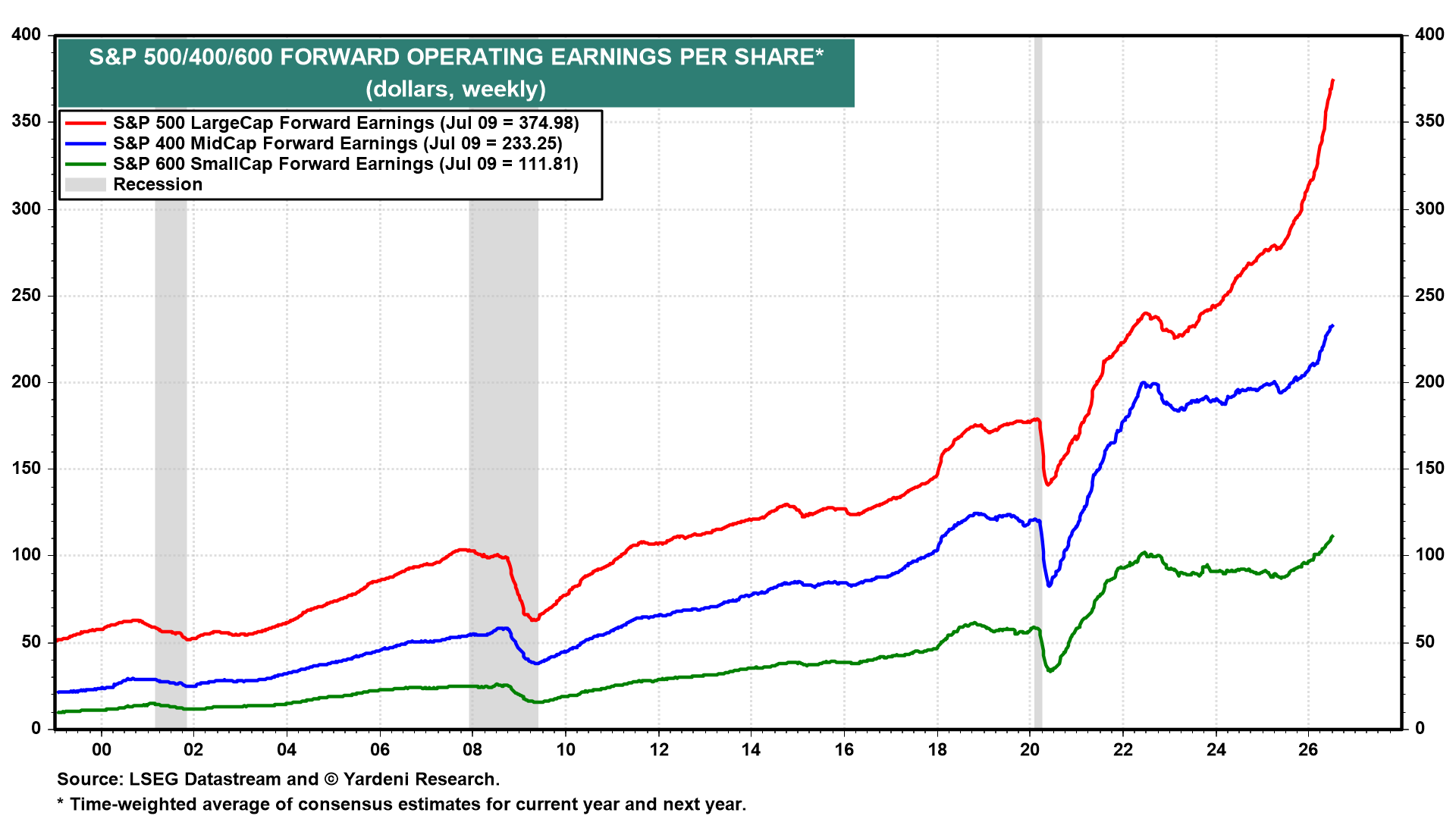

(2) Breadth. Breadth remains healthy, as revenue growth is broadening into earnings gains beyond the S&P 500. S&P 400 and S&P 600 forward earnings are climbing to new record highs along with the S&P 500 forward earnings (chart).

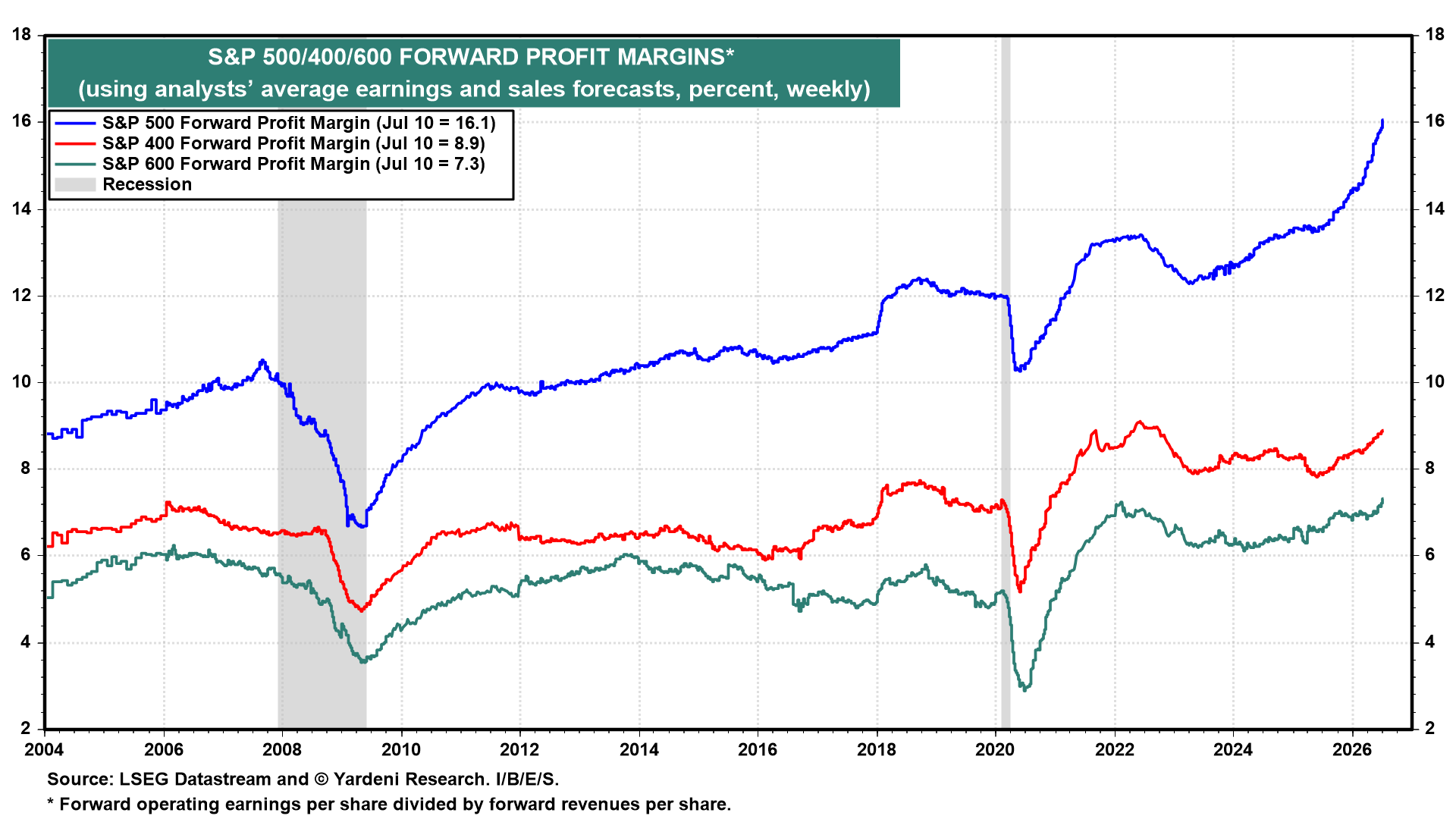

The S&P 500 companies' collective forward profit margin rose to a record 16.1% last week (chart). The forward profit margins of the S&P 400 and S&P 600 are lower, but also closing in on their previous record highs.